Sildenafil Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

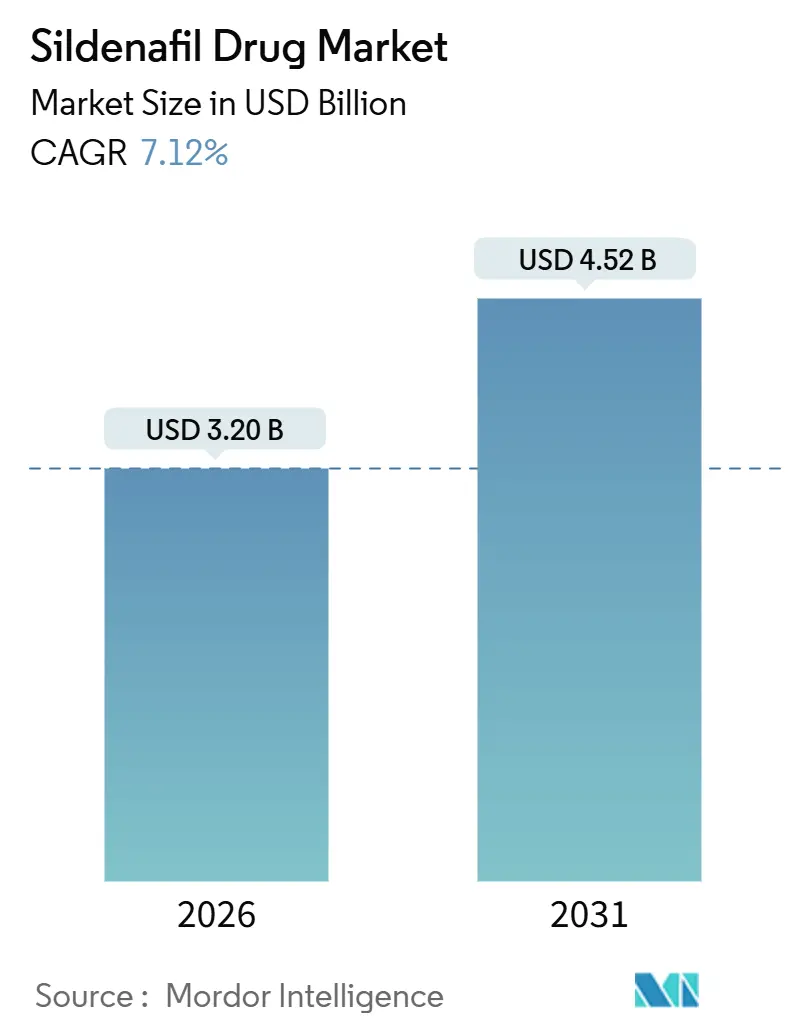

| Market Size (2026) | USD 3.20 Billion |

| Market Size (2031) | USD 4.52 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

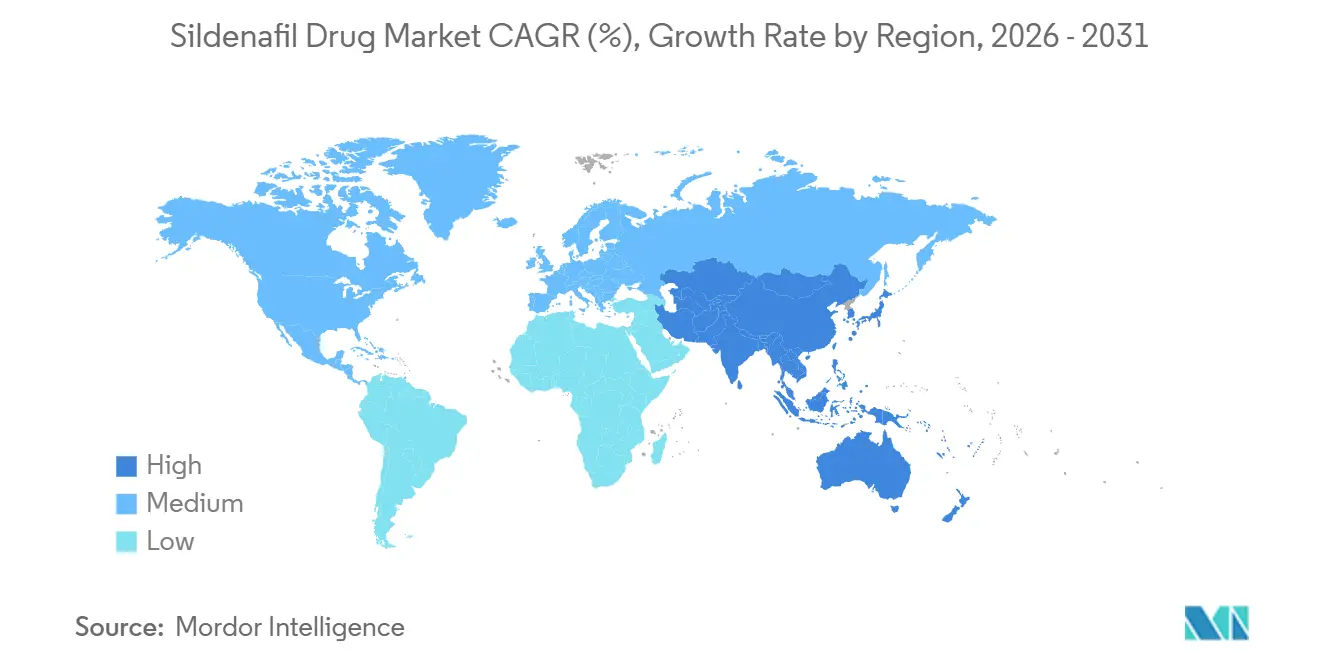

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sildenafil Drug Market Analysis by Mordor Intelligence

The Sildenafil Drug Market size is estimated at USD 3.20 billion in 2026, and is expected to reach USD 4.52 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031).

Aging populations, telemedicine-enabled prescription access, and expanding clinical use in pulmonary arterial hypertension (PAH) are the dominant forces behind the upward curve. Hospital specialists continue to prescribe solid oral tablets widely, yet injectable formats are becoming integral in intensive-care protocols for acute PAH, where oral dosing is not feasible. Parallel growth in direct-to-consumer platforms shows younger men favoring virtual consultations to sidestep the stigma of in-person visits. Meanwhile, generic competition after patent expiry has compressed prices and spurred volume growth, while continued research into cardioprotective and fertility adjunct uses offers longer-term optionality. Together, these threads position the Sildenafil drug market for steady expansion despite intensified price pressure.

Key Report Takeaways

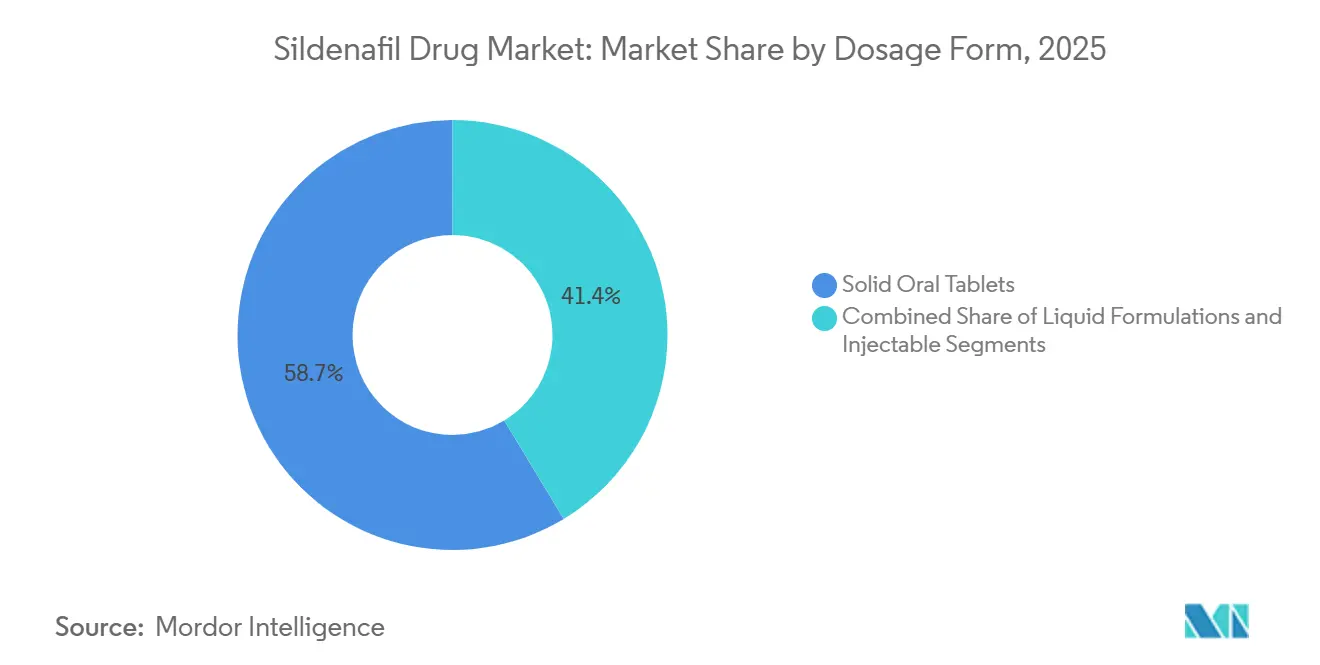

- By dosage form, solid oral tablets led with 58.65% revenue in 2025, while injectable formulations are forecast to expand at a 9.54% CAGR through 2031.

- By distribution channel, hospital pharmacies held 62.34% of the sildenafil drug market share in 2025, whereas e-commerce platforms are projected to grow at a 10.45% CAGR to 2031.

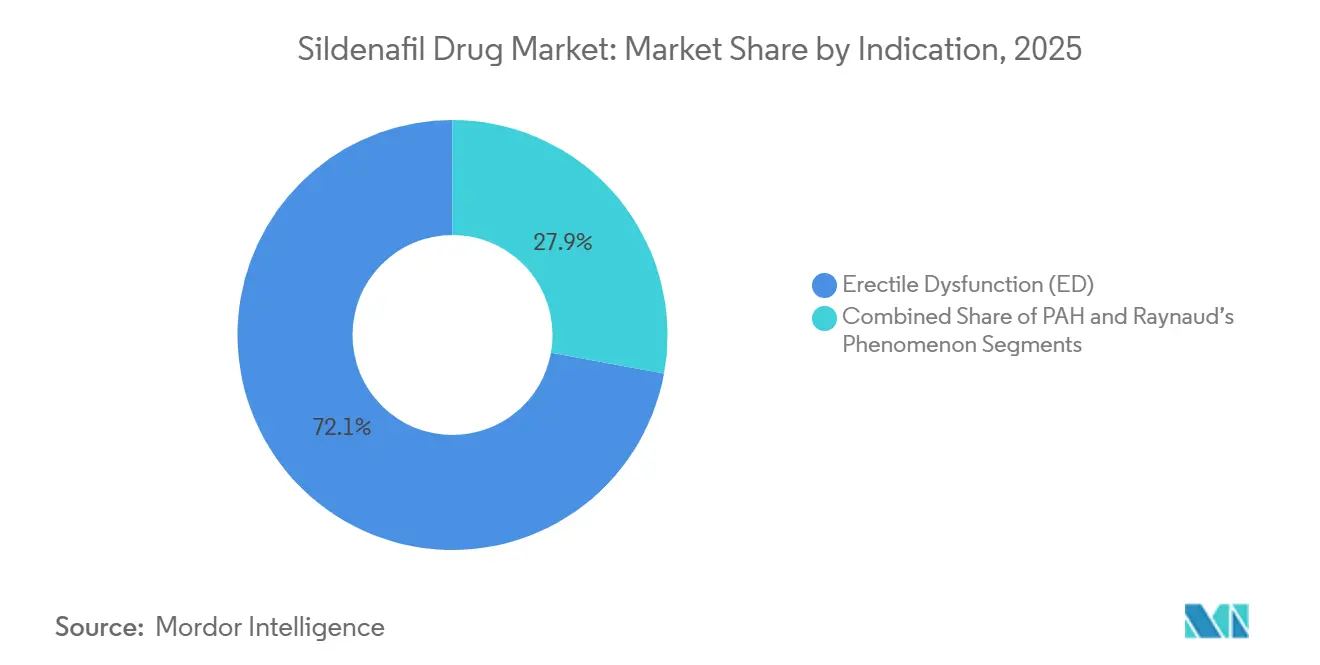

- By indication, erectile dysfunction accounted for 72.14% of the sildenafil drug market size in 2025, and pulmonary arterial hypertension is advancing at a 9.67% CAGR through 2031.

- By geography, North America generated 42.56% of revenue in 2025; Asia-Pacific is expected to post the fastest CAGR of 8.43% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sildenafil Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Erectile Dysfunction | 1.8% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Increasing Awareness & Social Acceptance of ED Treatment | 1.2% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing Geriatric Male Population | 1.5% | Global, peak impact in Japan, Germany, Italy | Long term (≥ 4 years) |

| Technological Advances in Drug Formulations & Alternative Delivery Systems | 1.0% | North America, Europe, India (manufacturing hub) | Medium term (2-4 years) |

| Growth of Tele-Medicine & E-Pharmacy Channels | 1.3% | North America, Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Exploration of Cardioprotective & Fertility Adjunct Indications | 0.6% | North America, Europe (clinical-trial centers) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Erectile Dysfunction

Erectile dysfunction (ED) prevalence accelerates with age; 40% of men over 40 and 70% of men over 70 report symptoms, amounting to a projected 322 million affected individuals worldwide in 2025[1]PubMed Editorial Board, “Global Prevalence of Erectile Dysfunction,” pubmed.ncbi.nlm.nih.gov. Despite the scale, diagnosis and treatment remain low: only 7.7% of men aged 18-40 who experience ED receive care, leaving a sizable reservoir of latent demand[2]JAMA Network Editors, “Direct-to-Consumer Use of Erectile Dysfunction Medicines,” jamanetwork.com. Prescription volumes mirror the demographic curve; England recorded a 110% rise in ED medication dispensing between 2009 and 2019 as awareness campaigns normalized discussion of sexual health. Comorbidities such as diabetes and hypertension further enlarge the treated population. As screening becomes routine in primary care, the Sildenafil drug market gains consistent patient inflow.

Increasing Awareness & Social Acceptance of ED Treatment

Public campaigns, celebrity endorsements, and online communities have recast ED as a manageable medical condition rather than a taboo subject. Surveys conducted in 2024 show that 68% of U.S. men feel comfortable discussing ED with a physician, up from 51% five years earlier. Health systems incorporate ED screening into annual check-ups, generating higher diagnosis rates. Digital health portals supply educational content linked directly to prescription pathways, converting awareness into sales. In turn, rising diagnosis fills the treatment funnel for the Sildenafil drug market, especially among first-time users who prioritize clinically validated therapies over unregulated supplements.

Technological Advances in Drug Formulations & Alternative Delivery Systems

Orally disintegrating tablets, sublingual films, and oral suspensions have transformed adherence by removing water requirements and shortening onset time. A 2024 bioequivalence study confirmed that sublingual films reach therapeutic plasma levels faster than conventional tablets, an advantage for on-demand use. Injectable sildenafil, though a minority format, is gaining traction in critical-care PAH, expanding at a 9.54% CAGR through 2031. Indian producers such as Cipla and Dr. Reddy’s leverage cost-efficient plants to file abbreviated new drug applications for these formats. As convenience and speed eclipse marginal efficacy gains, diversified delivery systems keep patients on therapy and enlarge the sildenafil drug market.

Growth of Tele-Medicine & E-Pharmacy Channels

Direct-to-consumer platforms dismantle traditional prescription pathways. Hims & Hers reported USD 401.6 million in Q3 2024 revenue—up 77% year over year—by selling sildenafil online at USD 6-7 per pill versus a generic wholesale cost of USD 0.32. A 2024 study found that 31.7% of men aged 18-40 with ED obtain medication through telemedicine, a share that rises to 50% among those never consulting a physician. Regulatory acceptance of online prescribing for non-controlled substances accelerates adoption across North America and Europe. While the FDA has admonished rogue pharmacies, compliant platforms are flourishing, funneling incremental volume into the sildenafil drug market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse Effects & Contraindication Concerns | -0.9% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Patent Expiries Driving Intense Generic Price Erosion | -1.4% | North America, Europe, mature Asia-Pacific markets | Short term (≤ 2 years) |

| Stringent Regulatory Scrutiny on Counterfeit & Online Sales | -0.6% | Global, acute in low- and middle-income countries | Medium term (2-4 years) |

| Rising Competition from Novel-Mechanism ED Therapeutics | -0.8% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse Effects & Contraindication Concerns

Sildenafil’s vasodilatory mechanism can trigger hypotension when co-administered with nitrates, excluding many cardiovascular patients from therapy. Reported visual disturbances and rare hearing loss also temper physician enthusiasm in risk-averse settings. As prescribers embrace electronic health record alerts that flag contraindications, cautious dosing reduces adverse-event incidence but slows the initiation of first-line therapy. These safety alarms, amplified by social media anecdotes, dampen conversion rates in the Sildenafil drug market, particularly among older patients with multiple comorbidities.

Patent Expiries Driving Intense Generic Price Erosion

Pfizer’s primary patents lapsed in major markets by 2013, sending average tablet prices down more than 90% within two years; the UK’s National Health Service paid GBP 31.31 per 100 mg tablet in 2012 but only GBP 2.53 by 2014. Margin compression shifted volume toward high-capacity Indian and Israeli generics makers, crowding premium brands. Although lower prices widen access and expand the sildenafil drug market, unit economics for manufacturers weaken, limiting investment in large-scale trials and marketing. Branded labels now rely on formulation innovation to reclaim niche pricing, yet the competitive field remains intense.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Injectables Surge as Oral Tablets Dominate

Solid oral tablets accounted for 58.65% of 2025 revenue, underscoring their status as the default route among urologists and primary care physicians[3]Food and Drug Administration, “Injectable Sildenafil Formulary Update,” fda.gov. Within this cohort, conventional film-coated pills remain prevalent, yet orally disintegrating tablets and sublingual films are gaining visibility, supported by 2024 data demonstrating equivalent bioavailability and faster onset. The Sildenafil drug market size for oral formats is expected to expand steadily as convenience-centric segments, such as younger professionals, opt for discreet administration.

Injectable sildenafil, while accounting for a smaller share, is projected to advance at a 9.54% CAGR through 2031, outpacing all other dosage forms. Critical-care adoption accelerated after the 2024 label revision, permitting 80 mg three times daily dosing for PAH. Hospitals view rapid intravenous vasodilation as lifesaving in refractory cases, justifying premium reimbursement. Manufacturers with sterile manufacturing suites and formulary access stand to deepen penetration, positioning injectables as the fastest-growing segment of the sildenafil drug market.

By Indication: PAH Expansion Challenges ED Dominance

Erectile dysfunction controlled 72.14% of the 2025 volume, anchored by high prevalence and decades of prescriber familiarity. Yet treatment uptake still trails prevalence, signaling headroom for growth as stigma declines. Direct-to-consumer platforms reach underdiagnosed young men, further enlarging the treated cohort. In parallel, off-label use in Raynaud’s phenomenon and male infertility adds incremental prescriptions.

Pulmonary arterial hypertension, though a smaller population, is forecast to grow at a 9.67% CAGR through 2031. The 2024 high-dose dosing allowance has driven hospital uptake, especially for injectable formulations. Specialty centers combine sildenafil with endothelin receptor antagonists to enhance survival in advanced PAH. As payers reimburse higher doses, the sildenafil drug market share attributed to PAH rises, serving as the primary counterweight to ED dominance.

By Distribution Channel: E-Commerce Disrupts Hospital Pharmacy Hegemony

Hospital pharmacies dispensed 62.34% of sildenafil in 2025, reflecting their control over injectables and complex PAH regimens. Multi-disciplinary care teams favor in-house dispensing to manage titration and monitoring. Retail pharmacies remain substantial, but their share erodes as virtual care normalizes.

E-commerce outlets are projected to rise at a 10.45% CAGR to 2031, the highest of all channels. Younger men cite discretion and speed as chief motivators for online ordering, and automated refill programs reinforce adherence. Licensed digital pharmacies that comply with state regulations avoid the FDA’s crackdown on rogue sellers, capturing trust and volume. The Sildenafil drug market size attributed to online sales is therefore set to climb faster than institutional segments, redrawing the channel landscape.

Geography Analysis

North America generated 42.56% of 2025 revenue, underpinned by high disposable income, insurance coverage, and early adoption of telehealth. U.S. demand is amplified by direct-to-consumer success stories such as Hims & Hers, which logged USD 401.6 million in Q3 2024 revenue. Canada benefits from affordable generics, while Mexico sees rising cross-border telemedicine use. The 2024 high-dose PAH label expansion accelerated the use of injectable PAH in U.S. intensive-care units. Despite volume gains, rampant generic competition compresses margins, keeping price sensitivity high across payers.

Europe trails slightly behind North America but maintains robust penetration. England recorded a 110% prescription surge for ED drugs between 2009 and 2019, indicating sustained growth even amid price deflation. Germany, France, and Italy leverage aging demographics to drive consistent demand. EU regulations permit online prescribing for non-controlled substances, yet cultural preference for brick-and-mortar pharmacies tempers the acceleration of e-commerce. National health systems prioritize generics, reinforcing the shift toward low-cost suppliers within the sildenafil drug market.

Asia-Pacific is forecast to post an 8.43% CAGR through 2031, the fastest regional pace. India and China dominate active pharmaceutical ingredient synthesis and finished-dose export, benefiting from scale and cost economics. Japan and Australia yield higher average selling prices due to stringent quality standards and older populations. Telemedicine uptake in South Korea and urban China introduces new channels. Challenges persist: the WHO estimates that 10% of medicines in low- and middle-income countries are substandard or falsified, with sildenafil prominent among counterfeit seizures. Countries with rigorous enforcement, such as Singapore, insulate patients, while less regulated markets risk reputational damage to legitimate producers.

Competitive Landscape

Following Pfizer’s patent expiration, the Sildenafil drug market fragmented rapidly. Teva, Viatris, Cipla, Sun Pharma, Dr. Reddy’s, Lupin, Torrent, Aurobindo, and Glenmark collectively supply large volumes at razor-thin margins. Chinese firms, including Guangzhou Baiyunshan and Zhejiang Hengjin, help meet global demand for active ingredients. Brand-loyal segments still purchase Pfizer’s Viagra at premium prices, yet this niche shrinks as younger cohorts embrace lower-cost generics.

Strategic differentiation now hinges on formulation and distribution. Companies that secure hospital formulary status for injectables capture higher reimbursement and defend margins. Others partner with telemedicine platforms, embedding automatic refills and discrete packaging into subscription models. Serialized packaging and blockchain traceability combat counterfeits, appealing to regulators and hospital buyers alike.

Novel-mechanism competitors encroach on the PDE5 class. Avanafil delivers a faster onset, while melanocortin agonist bremelanotide signals future male indications. Although PDE5 inhibitors remain first-line, the threat of share erosion grows as payers embrace therapeutic substitution. Manufacturers diversifying into alternative delivery systems, combination therapies, or pipeline assets enjoy a broader hedge against commoditization within the sildenafil drug industry.

Sildenafil Drug Industry Leaders

Teva Pharmaceutical Industries Ltd.

Viatris Inc.

Sun Pharmaceutical Industries Ltd.

Cipla Ltd.

Lupin Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Daré Bioscience, Inc., a biopharmaceutical company with a sole focus on closing the gap in women’s health between promising science and real solutions, and Rosy Wellness, a pioneering digital platform focused on providing lifespan support for women, launched the first phase of a consumer awareness campaign to support the upcoming introduction of DARE to PLAY Sildenafil Cream.

- November 2024: The FDA issued warning letters to online pharmacies selling unapproved sildenafil, reinforcing regulatory oversight

Global Sildenafil Drug Market Report Scope

As per scope of the report, sildenafil is a medication primarily used to treat erectile dysfunction and sometimes pulmonary hypertension. It works by relaxing blood vessels to increase blood flow. It is commonly known by the brand name Viagra.

The Sildenafil Drug Market is Segmented by Dosage Form (Solid Oral Tablets, Liquid Formulations, and Injectable), Indication (Erectile Dysfunction, Pulmonary Arterial Hypertension, and Raynaud's Phenomenon & Other Off-label Uses), Distribution Channel (Hospital Pharmacy, Retail Pharmacy/Drug Store, E-Commerce Pharmacy, and Mail-Order Pharmacy), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Solid Oral Tablets | Conventional Film-Coated Tablet |

| Orally Disintegrating Tablet (ODT) | |

| Sublingual Film / Strip | |

| Liquid Formulations | Oral Suspension |

| Pediatric Drops | |

| Injectable |

| Erectile Dysfunction (ED) |

| Pulmonary Arterial Hypertension (PAH) |

| Raynaud's Phenomenon & Other Off-label Uses |

| Hospital Pharmacy |

| Retail Pharmacy / Drug Store |

| E-Commerce Pharmacy |

| Mail-Order Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Dosage Form | Solid Oral Tablets | Conventional Film-Coated Tablet |

| Orally Disintegrating Tablet (ODT) | ||

| Sublingual Film / Strip | ||

| Liquid Formulations | Oral Suspension | |

| Pediatric Drops | ||

| Injectable | ||

| By Indication | Erectile Dysfunction (ED) | |

| Pulmonary Arterial Hypertension (PAH) | ||

| Raynaud's Phenomenon & Other Off-label Uses | ||

| By Distribution Channel | Hospital Pharmacy | |

| Retail Pharmacy / Drug Store | ||

| E-Commerce Pharmacy | ||

| Mail-Order Pharmacy | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the sildenafil drug market in 2026?

The sildenafil drug market size reached USD 3.20 billion in 2026 and is on track to hit USD 4.52 billion by 2031.

What is the expected growth rate for sildenafil injectables?

Injectable formulations are forecast to grow at a 9.54% CAGR through 2031 as hospitals adopt high-dose PAH protocols.

Which region is the fastest growing for sildenafil sales?

Asia-Pacific is forecast to expand at an 8.43% CAGR through 2031, outpacing all other regions.

Why are telemedicine channels important for sildenafil?

Telemedicine platforms offer discretion and convenience, already fulfilling 31.7% of prescriptions among U.S. men aged 18-40.

Who are the leading sildenafil manufacturers after patent expiry?

Teva, Viatris, Cipla, Sun Pharma, and Dr. Reddy's dominate post-patent volumes, while Pfizer retains a shrinking premium niche.

What safety concern limits sildenafil use?

Concomitant nitrate therapy can precipitate dangerous hypotension, restricting prescribing in patients with cardiovascular disease.

Page last updated on: