United States Fourth-Party Logistics (4PL) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

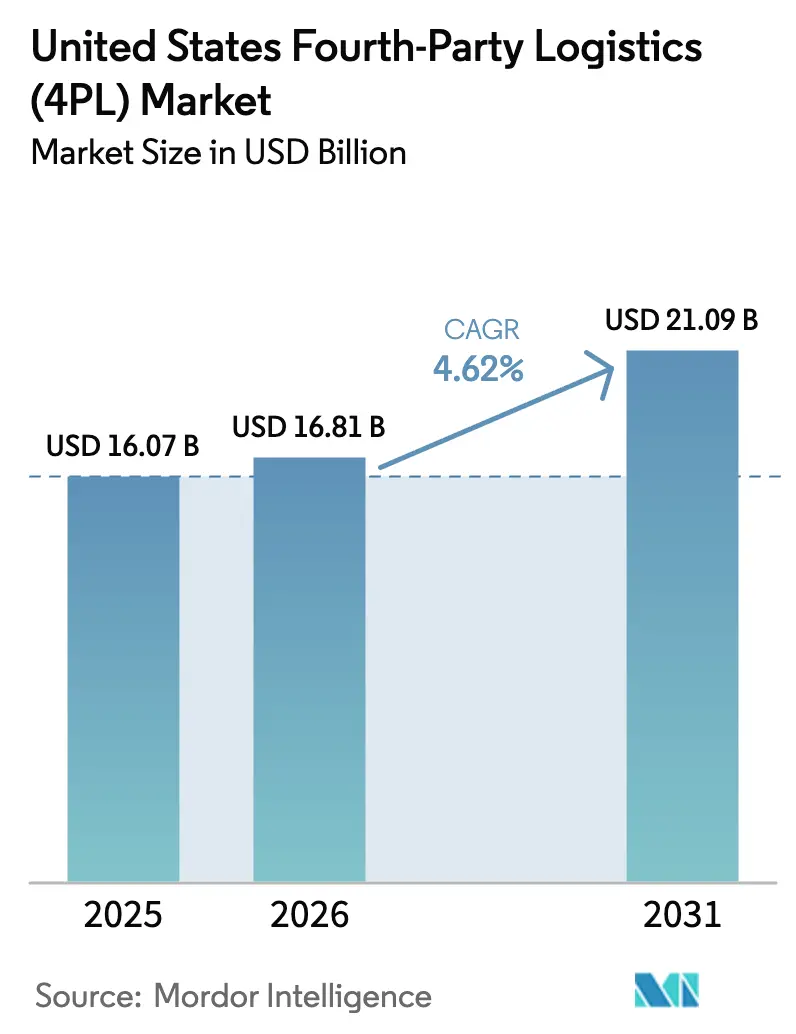

| Base Year Market Size (2025) | USD 16.07 Billion |

| Market Size (2026) | USD 16.81 Billion |

| Market Size (2031) | USD 21.09 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

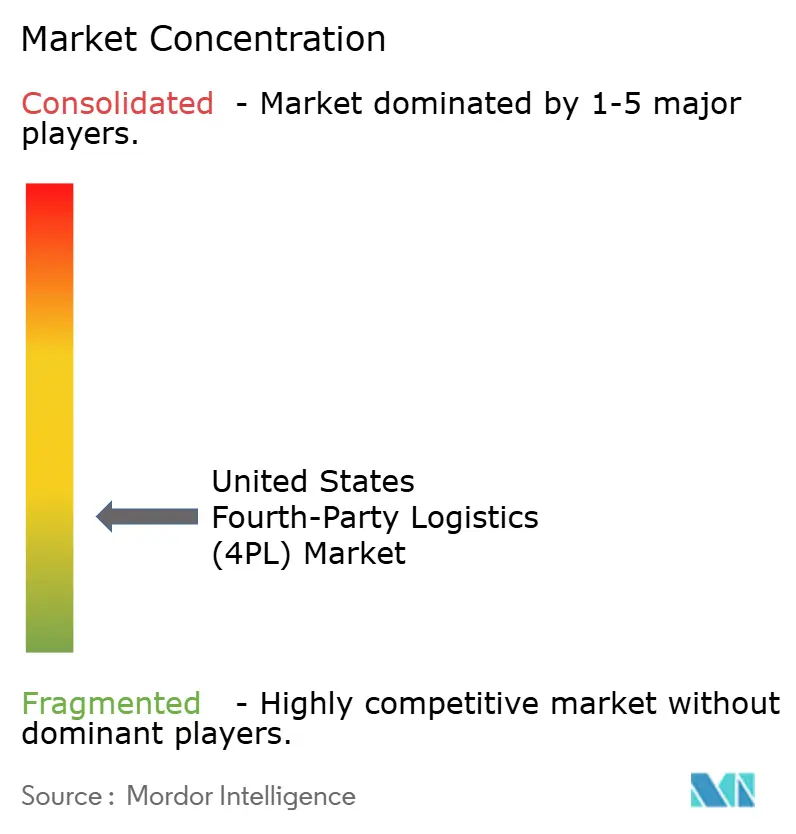

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Fourth-Party Logistics (4PL) Market Analysis by Mordor Intelligence

The United States Fourth-Party Logistics Market size was valued at USD 16.07 billion in 2025 and estimated to grow from USD 16.81 billion in 2026 to reach USD 21.09 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031).

The sustained expansion stems from the pivot away from piecemeal outsourcing toward full-spectrum supply-chain orchestration that positions 4PL providers as control-tower partners rather than transactional vendors. Heightened omnichannel complexity, especially in retail and e-commerce, amplifies demand for real-time visibility, predictive analytics, and nationwide coordination at scale. Enterprises are accelerating adoption of agentic AI, with early movers reporting revenue growth premiums exceeding 60%, which further cements integrated platforms as table stakes. Meanwhile, freight-rate volatility, near-shoring, and cyber-risk exposure continue to push shippers toward asset-light partners who can absorb operational risk in exchange for contractual control. Moderate consolidation highlighted by DSV’s acquisition of Schenker signals rising competitive pressure on midsize specialists to differentiate through technology depth and vertical expertise.

Key Report Takeaways

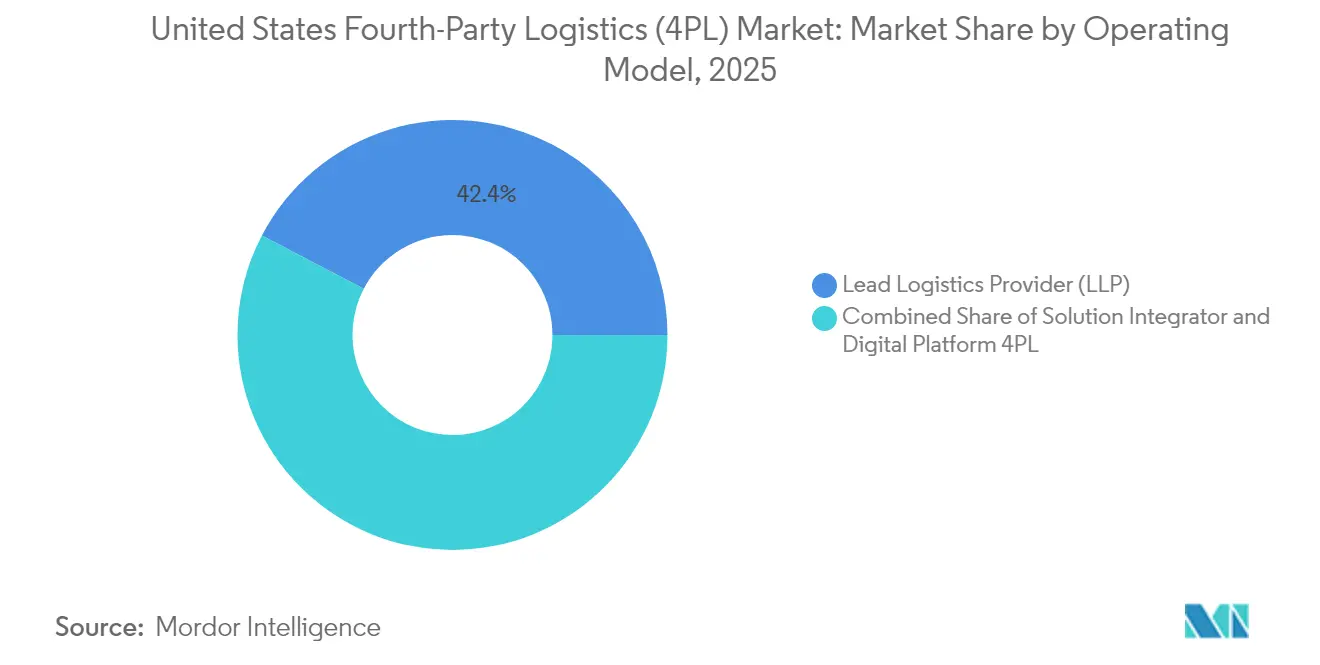

- By operating model, the Lead Logistics Provider segment commanded 42.35% of fourth party logistics market share in 2025, while the Digital Platform 4PL model is projected to expand at a 4.96% CAGR through 2031..

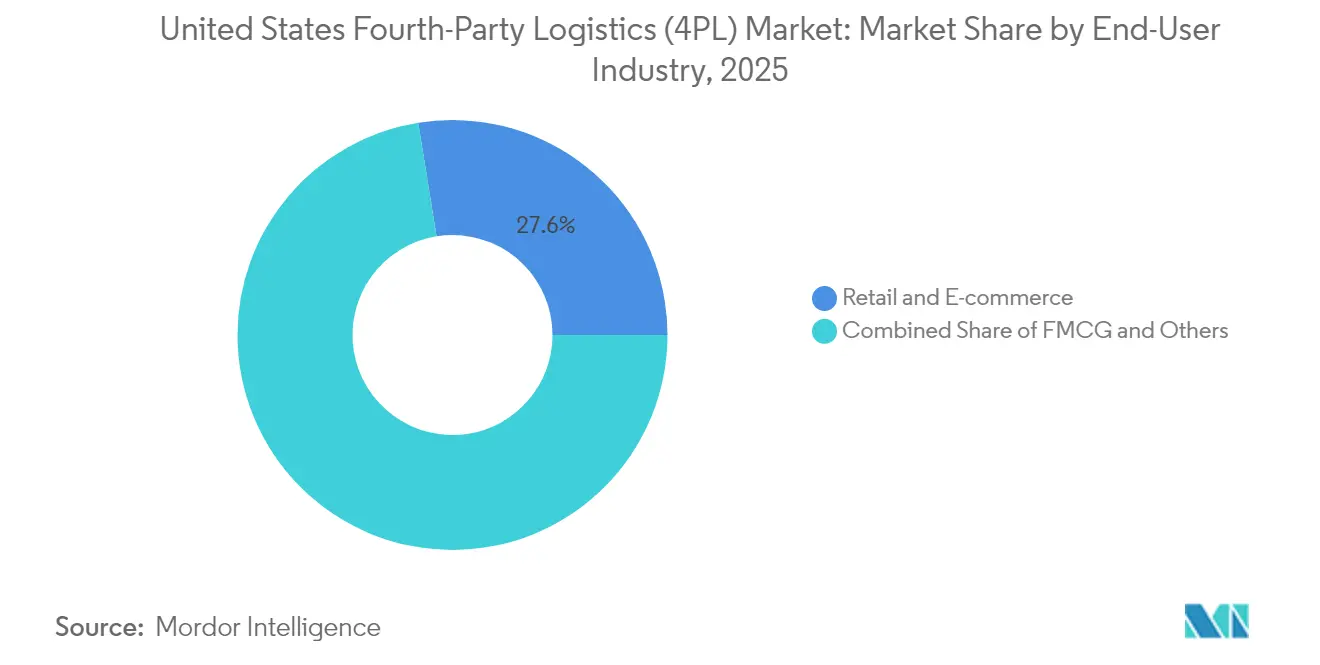

- By end-user industry, retail & e-commerce captured 27.55% of fourth party logistics market share in 2025 and is expected to advance at a 5.06% CAGR to 2031.

- By U.S. region, the South led with 28.60% revenue share in 2025, whereas the Midwest is forecast to register the fastest growth at a 4.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Fourth-Party Logistics (4PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising complexity of omnichannel supply chains | +1.2% | Northeast & West Coast urban centers | Medium term (2-4 years) |

| Increasing adoption of lead-logistics-provider cost-out models | +1.0% | South & Midwest corridors | Short term (≤ 2 years) |

| E-commerce demand for nationwide control-tower orchestration | +1.5% | Major metro distribution hubs | Medium term (2-4 years) |

| Integrated control-tower IT platforms (AI/IoT) | +0.8% | West Coast & Northeast | Long term (≥ 4 years) |

| Near-shoring wave and domestic network re-design | +0.7% | South & Southwest border regions | Medium term (2-4 years) |

| Freight-rate volatility and asset-light risk transfer | +0.9% | Import-dependent coastal regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Complexity of Omnichannel Supply Chains

Retailers deploying omnichannel strategies must synchronize store, online, and marketplace inventory simultaneously, creating orchestration requirements beyond traditional 3PL capabilities. Walmart’s AI-driven network shows how real-time demand sensing, dynamic routing, and predictive replenishment cut stock-outs while maintaining low safety inventory. Amazon’s inbound cross-dock facilities illustrate infrastructure commitments needed to scale unified fulfillment networks. Such complexity elevates digital platform 4PL providers that leverage machine learning for inventory placement and order orchestration. Regulatory frameworks remain permissive, yet emerging data-privacy statutes may constrain how 4PLs aggregate shopper insights across channels. Overall, omnichannel growth locks in structural demand for nationwide control-tower solutions that optimize transport, labor, and inventory concurrently.

Increasing Adoption of Lead-Logistics-Provider Cost-Out Models

Inflation and supply-chain disruption make logistics cost control a board-level priority. Consolidating disparate 3PL contracts under a single LLP generates immediate scale efficiencies and reduces vendor-management overhead. A U.S. manufacturer documented USD 260 million in logistics savings and a 15% cut in transportation spend by embracing an LLP framework. Asset-light providers also shoulder freight-rate volatility, shifting working-capital and capacity risks off corporate balance sheets. Manufacturing firms in automotive and durable goods are leading adopters, but services sectors now view LLPs as strategic hedges against unpredictable capacity markets. Centralized compliance management further appeals to multistate operators wrestling with fragmented labor and safety rules[1]"Why we will be seeing a radical reinvention of supply chains." World Economic Forum, weforum.org.

E-commerce–Driven Demand for Nationwide Control-Tower Orchestration

Same-day and next-day delivery promises raise service-level stakes across parcel, less-than-truckload, and middle-mile moves. Control-tower software integrates order, transport, and warehouse data to orchestrate multi-node fulfillment networks in real time. The control-tower market itself will reach USD 32.14 billion by 2030, growing at 21.3% CAGR more than triple the pace of the broader fourth party logistics market. Advanced platforms combine predictive analytics, automated exception handling, and collaborative tools to enable proactive network management. Companies implementing control-tower solutions report up to 1% revenue gains, 3-5% logistics cost reductions, and 10-20% labor efficiency improvements. Peak-season surges further accelerate adoption as manual coordination across multiple 3PLs proves inadequate for high-volume periods.

Integrated Control-Tower IT Platforms (AI/IoT) Become Table-Stakes

AI and IoT integration has evolved from competitive advantage to market necessity for fourth party logistics providers. UPS demonstrates how agentic AI enables autonomous decision-making across complex networks without human intervention. These platforms predict disruptions, optimize routing, and adjust capacity allocation based on real-time demand signals. C3 AI's multi-hop orchestration agents exemplify the required sophistication, enabling supply chain optimization through autonomous collaboration C3.AI. The technology stack includes IoT sensors for asset tracking, predictive analytics for demand forecasting, and automated workflow engines for exception management. Gartner projects that 25% of logistics KPI reporting will leverage generative AI by 2028, confirming the rapid adoption trajectory[2]"Transforming Supply Chain Optimization with C3 AI's Multi-Hop Orchestration Agents." C3 AI, c3.ai.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & data-ownership concerns | -0.8% | Financial & healthcare sectors | Short term (≤ 2 years) |

| High implementation cost & change-management burden | -1.1% | Mid-market enterprises | Medium term (2-4 years) |

| Scarcity of supply-chain data-science talent | -0.6% | Technology hubs & manufacturing regions | Long term (≥ 4 years) |

| Channel conflict with large incumbent 3PLs | -0.4% | Established logistics corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-security and Data-ownership Concerns

Supply chain digitization creates significant cybersecurity vulnerabilities that constrain fourth party logistics adoption, especially in regulated industries. The World Economic Forum reports 54% of large organizations cite supply chains as major barriers to cyber resilience, with the 2024 global IT outage exposing critical third-party dependencies. Fourth-party logistics providers face unique challenges because they operate without direct oversight of many vendors in their networks, creating potential attack vectors that traditional risk management approaches cannot adequately address. The logistics sector experienced 27 cyber incidents between July 2023 and July 2024, with the cybersecurity market in logistics projected to grow at 12% CAGR from 2024 to 2037, reaching USD 36.6 billion. Data ownership concerns become particularly acute when 4PL providers aggregate information across multiple clients, creating potential conflicts over proprietary business intelligence.

High Implementation Cost and Change-Management Burden

Transitioning to fourth party logistics models requires substantial upfront investments in technology, process redesign, and organizational change management that many enterprises find prohibitive. Ernst & Young research indicates successful digital transformation in logistics requires coordinated investments across people, processes, technology, and data, with many organizations struggling to achieve meaningful integration. The 2025 Annual Third-Party Logistics Study reveals 61% of shippers and 73% of 3PLs consider change management a significant challenge, with only 83% of shippers reporting successful partnerships compared to historical averages above 90%. Implementation complexity increases exponentially when enterprises attempt to integrate legacy systems with advanced 4PL platforms, often requiring complete process reengineering rather than incremental improvements. The challenge becomes particularly acute for mid-market companies lacking internal expertise and financial resources necessary to manage complex transformations while maintaining operational continuity[3]"Accelerating Federal Permitting of Data Center Infrastructure." Federal Register, federalregister.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating Model: Digital Platforms Drive Innovation

Lead Logistics Provider (LLP) commanded 42.35% of the fourth party logistics market size in 2025, reflecting enterprises' preference for comprehensive supply chain management through single-provider relationships that reduce complexity and enhance accountability. The LLP model's dominance stems from its ability to deliver cost synergies through economies of scale while transferring operational risk to specialized providers with deeper logistics expertise. Solution Integrator models occupy the middle ground, focusing on technology-enabled coordination across multiple logistics providers without assuming direct operational responsibility. Digital Platform 4PL emerges as the fastest-growing segment at 4.96% CAGR through 2031, driven by enterprises seeking AI-powered visibility and autonomous decision-making capabilities that traditional models cannot deliver.

The Digital Platform 4PL segment's growth acceleration reflects the fourth party logistics market evolution toward data-driven supply chain orchestration, where real-time analytics and predictive modeling become competitive differentiators rather than operational luxuries. Blue Yonder's Network Ops Agent demonstrates how AI agents can autonomously manage logistics operations, predicting arrival times, clustering shipments, and maximizing resource utilization without human intervention. Solution Integrator models face increasing pressure to differentiate through specialized industry expertise or geographic coverage, as pure coordination functions become commoditized through automation. The regulatory landscape favors platform models that can demonstrate transparency and auditability in their decision-making processes, particularly as data privacy and algorithmic accountability requirements evolve.

By End-User Industry: Retail Dominance Amid Sectoral Diversification

Retail & E-commerce represented both the largest segment at 27.55% of fourth party logistics market share in 2025 and the fastest-growing at 5.06% CAGR through 2031, driven by omnichannel complexity and consumer expectations for rapid fulfillment. The sector's growth reflects the fundamental shift from inventory-centric to demand-sensing supply chains, where 4PL providers must orchestrate real-time inventory optimization across multiple fulfillment channels. FMCG companies increasingly adopt 4PL models to manage complex distribution networks that span multiple product categories and seasonal demand patterns. Technology & Electronics sectors drive innovation adoption, leveraging 4PL capabilities for managing product lifecycles and reverse logistics operations.

Automotive & Mobility segments benefit from nearshoring trends that require domestic network redesign, with 4PL providers facilitating the transition from global to regional supply chains. Refrigerated & Pharma applications demand specialized cold-chain expertise and regulatory compliance capabilities that traditional 3PL providers often lack. Industrial Manufacturing segments increasingly recognize 4PL value propositions for managing complex multi-tier supplier networks and just-in-time delivery requirements. Fashion & Lifestyle industries leverage 4PL capabilities for managing seasonal inventory fluctuations and fast-fashion supply chain requirements. The diversification across industry verticals indicates fourth party logistics market maturation, as 4PL providers develop specialized capabilities tailored to specific sector requirements rather than pursuing one-size-fits-all approaches.

Geography Analysis

The South region's 28.60% fourth party logistics market share in 2025 reflects its strategic advantages in port infrastructure, manufacturing concentration, and business-friendly regulatory environments that attract logistics investments. Major ports in Houston, New Orleans, and Savannah serve as critical gateways for international trade, while the region's automotive and aerospace manufacturing clusters create demand for sophisticated supply chain orchestration. The region benefits from relatively low labor costs and abundant warehouse space, though these advantages face erosion as automation reduces labor intensity and e-commerce drives demand for urban fulfillment centers. Recent infrastructure investments, including port expansions and inland transportation corridors, position the South for continued growth despite increasing competition from other regions. The region's 4PL adoption reflects the complexity of managing multi-modal transportation networks that span ocean, rail, and trucking operations across diverse industry verticals.

The Midwest's emergence as the fastest-growing region at 4.92% CAGR through 2031 represents a fundamental shift in logistics geography, driven by nearshoring trends, automotive sector digitalization, and agricultural supply chain modernization. The region's central location provides cost-effective access to both coasts while offering competitive real estate and labor markets that support large-scale distribution operations. Chicago's position as a major rail hub and Detroit's automotive ecosystem create natural demand for 4PL services that can coordinate complex multi-tier supplier networks. Agricultural sectors increasingly adopt precision logistics for managing seasonal demand fluctuations and cold-chain requirements that traditional 3PL providers struggle to optimize. The region's growth trajectory benefits from federal infrastructure investments and state-level incentives that support advanced manufacturing and logistics technology adoption.

The Northeast and West regions maintain significant positions in the fourth party logistics market through specialization in high-value sectors that demand sophisticated 4PL capabilities. Northeast markets leverage dense population centers, established financial services infrastructure, and proximity to major consumer markets to support premium 4PL services with advanced analytics and risk management capabilities. The region's regulatory complexity, particularly around environmental and labor standards, creates barriers to entry that benefit established 4PL providers with compliance expertise. West Coast markets drive technology innovation and Pacific Rim trade relationships, though increasing costs and regulatory burdens may favor alternative regional solutions for price-sensitive applications. Both regions demonstrate the market's evolution toward value-based differentiation rather than cost-based competition, creating opportunities for 4PL providers that can deliver measurable business outcomes through advanced supply chain orchestration.

Competitive Landscape

The US fourth party logistics market exhibits moderate concentration with accelerating consolidation through strategic acquisitions, exemplified by DSV's EUR 14.3 billion (USD 15.78 billion) acquisition of Schenker in April 2025, creating the world's largest logistics company with EUR 41.6 billion (USD 45.91 billion) in combined revenue. Market leaders pursue differentiation through technology integration, with UPS implementing agentic AI for autonomous logistics operations and Ryder achieving record earnings through Supply Chain Solutions segment growth of 50% in dedicated transportation. Competitive strategies increasingly focus on vertical specialization and geographic expansion, with GEODIS launching its Ambition 2027 strategic plan emphasizing sustainable logistics solutions and digital innovation. The fourth party logistics market structure favors providers capable of delivering end-to-end supply chain orchestration rather than discrete logistics functions, creating barriers to entry for traditional 3PL providers lacking comprehensive technology platforms.

White-space opportunities emerge in specialized industry verticals and emerging technology applications, particularly as 74% of shippers indicate that AI capabilities will influence their 4PL provider selection. Emerging disruptors leverage cloud-native platforms and API-first architectures to deliver rapid implementation and scalable solutions that challenge incumbent providers' legacy systems. Technology adoption patterns reveal competitive advantages for providers investing in autonomous operations, predictive analytics, and real-time visibility platforms that enable proactive supply chain management. The competitive landscape increasingly rewards providers capable of demonstrating measurable ROI through cost reduction, service improvement, and risk mitigation rather than traditional metrics focused on operational efficiency alone. Regulatory compliance capabilities become competitive differentiators as cybersecurity requirements and data privacy regulations create additional complexity for 4PL providers managing multi-client environments.

United States Fourth-Party Logistics (4PL) Industry Leaders

-

UPS Supply Chain Solutions, Inc.

-

GEODIS

-

DSV Solutions

-

XPO Inc.

-

DHL Supply Chain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amazon announced a USD 4 billion investment to expand fulfillment capabilities in rural areas, creating over 100,000 jobs and enabling delivery of over 1 billion additional packages annually to more than 13,000 zip codes. The initiative aims to improve delivery speeds by an average of 50% in underserved regions.

- April 2025: DSV completed its EUR 14.3 billion (USD 15.78 billion) acquisition of DB Schenker, creating the world's largest logistics company with approximately EUR 41.6 billion (USD 45.91 billion) in combined revenue and 160,000 employees across 90+ countries. The transaction represents the largest acquisition in DSV's history and is expected to generate DKK 9.0 billion (USD 1.33 billion) in annual synergies by 2028.

- March 2025: FedEx accelerated its Network 2.0 consolidation, confirming closures of six ship centers and staff cuts across Tennessee, Illinois, Virginia, and West Virginia. The initiative merges Express and Ground operations to achieve a 10% reduction in pickup and delivery costs.

- March 2025: UPS announced strategic initiatives and three-year financial targets, projecting consolidated revenue between USD 108-114 billion by 2026 with adjusted operating margins of at least 12% for its U.S. Domestic Package segment through its "Network of the Future" initiative.

United States Fourth-Party Logistics (4PL) Market Report Scope

A 4PL is a fourth-party logistics provider, and it takes third-party logistics a step further by managing resources, technology, and infrastructure and even managing external 3PLs to design, build, and provide supply chain solutions for businesses.

The largest difference between 3PL and 4PL is that while 3PL oversees part of the logistics for a business, a 4PL is often the single point of contact between the organization and its entire supply chain system.

The United States fourth-party logistics (4PL) market is segmented by operating model(lead logistics provider (LLP), solution integrator model, and digital platform solutions provider (4PL)) and by end-user (FMCG (fast-moving consumer goods - includes products related to beauty and personal care, home care, etc.), retail (hypermarkets, supermarkets, convenience stores, e-commerce channels), fashion and lifestyle (apparel and footwear), reefer (fruits, vegetable, pharmaceuticals, meat, fish, and seafood), technology (consumer electronics and home appliances)), and others end-users).

The report offers market size and forecasts for the united states fourth-party logistics (4PL) market in values (USD) for all the above segments.

| Lead Logistics Provider (LLP) |

| Solution Integrator |

| Digital Platform 4PL |

| FMCG |

| Retail and E-commerce |

| Fashion and Lifestyle |

| Technology and Electronics |

| Refrigerated and Pharma |

| Automotive and Mobility |

| Industrial Manufacturing |

| Others |

| Northeast |

| Midwest |

| South |

| West |

| By Operating Model | Lead Logistics Provider (LLP) |

| Solution Integrator | |

| Digital Platform 4PL | |

| By End-User Industry | FMCG |

| Retail and E-commerce | |

| Fashion and Lifestyle | |

| Technology and Electronics | |

| Refrigerated and Pharma | |

| Automotive and Mobility | |

| Industrial Manufacturing | |

| Others | |

| By US Region | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is fourth party logistics and how does it differ from 3PL?

Fourth party logistics (4PL) providers manage entire supply chain ecosystems rather than discrete functions, acting as orchestrators who coordinate multiple 3PLs and other service providers. Unlike 3PLs that typically own and operate assets, 4PLs focus on control-tower capabilities, technology integration, and strategic oversight while remaining asset-light.

Which industries benefit most from 4PL services?

Retail & e-commerce benefits most, commanding 27.55% market share and growing at 5.06% CAGR through 2031. Other high-value adopters include automotive manufacturing, technology, pharmaceuticals, and FMCG companies with complex omnichannel requirements and nationwide distribution networks.

How is AI transforming the fourth party logistics landscape?

AI enables autonomous supply chain operations through predictive analytics, dynamic routing optimization, and exception management without human intervention. Companies implementing AI report 61% revenue growth premiums, with 74% of shippers indicating AI capabilities will influence their 4PL provider selection.

What are the main challenges in implementing a 4PL solution?

Key challenges include high implementation costs, change management difficulties (cited by 61% of shippers), cybersecurity vulnerabilities, data ownership concerns, and integration with legacy systems. Additionally, 4PL adoption faces resistance from incumbent 3PLs and internal logistics teams.

Which US region shows the strongest growth in 4PL adoption?

The Midwest is the fastest-growing region at 4.92% CAGR through 2031, driven by automotive sector digitalization, agricultural supply chain modernization, and strategic positioning for nearshoring from Mexico. The South remains the largest market with 28.60% share in 2025.

What technology capabilities should companies look for in a 4PL provider?

Companies should prioritize providers with control-tower platforms offering real-time visibility, predictive analytics, autonomous decision-making capabilities, IoT integration, and cybersecurity protections. Additionally, look for API-first architectures that enable rapid integration with existing systems.

Page last updated on: