Pastries Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 43.76 Billion |

| Market Size (2031) | USD 52.97 Billion |

| Growth Rate (2026 - 2031) | 3.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pastries Market Analysis by Mordor Intelligence

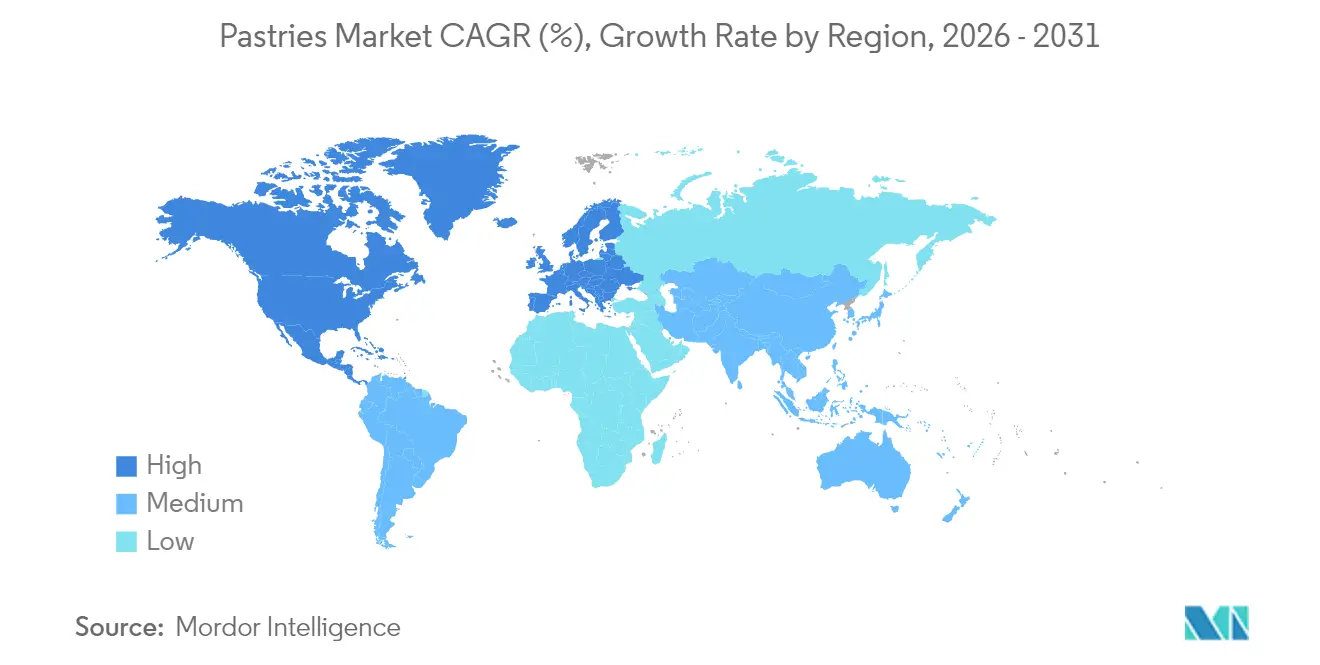

Pastries market size in 2026 is estimated at USD 43.76 billion, growing from 2025 value of USD 42.12 billion with 2031 projections showing USD 52.97 billion, growing at 3.9% CAGR over 2026-2031. The moderate expansion reflects balanced growth drivers: premiumization, clean-label reformulation, and convenience demand offsetting raw-material cost inflation. Retail remains the mainstay as 69.70% of global value flows through supermarkets, hypermarkets, convenience stores, and e-commerce, yet foodservice is regaining momentum as pandemic disruptions fade. Europe leads the pastries market with 39.60% share, thanks to strong artisanal traditions, while Asia-Pacific’s 8.56% CAGR signals rising urban incomes and Western dietary adoption. Technology now underpins competitive advantage; artificial-intelligence systems already cut bakery waste, helping manufacturers protect margins amid volatile egg, cocoa, and sugar prices. Consolidation is accelerating as global players pursue scale and health-centric capabilities, highlighted by Mars’s USD 35.9 billion acquisition of Kellanova in 2024 and Flowers Foods’s USD 795 million purchase of Simple Mills in January 2025.

Key Report Takeaways

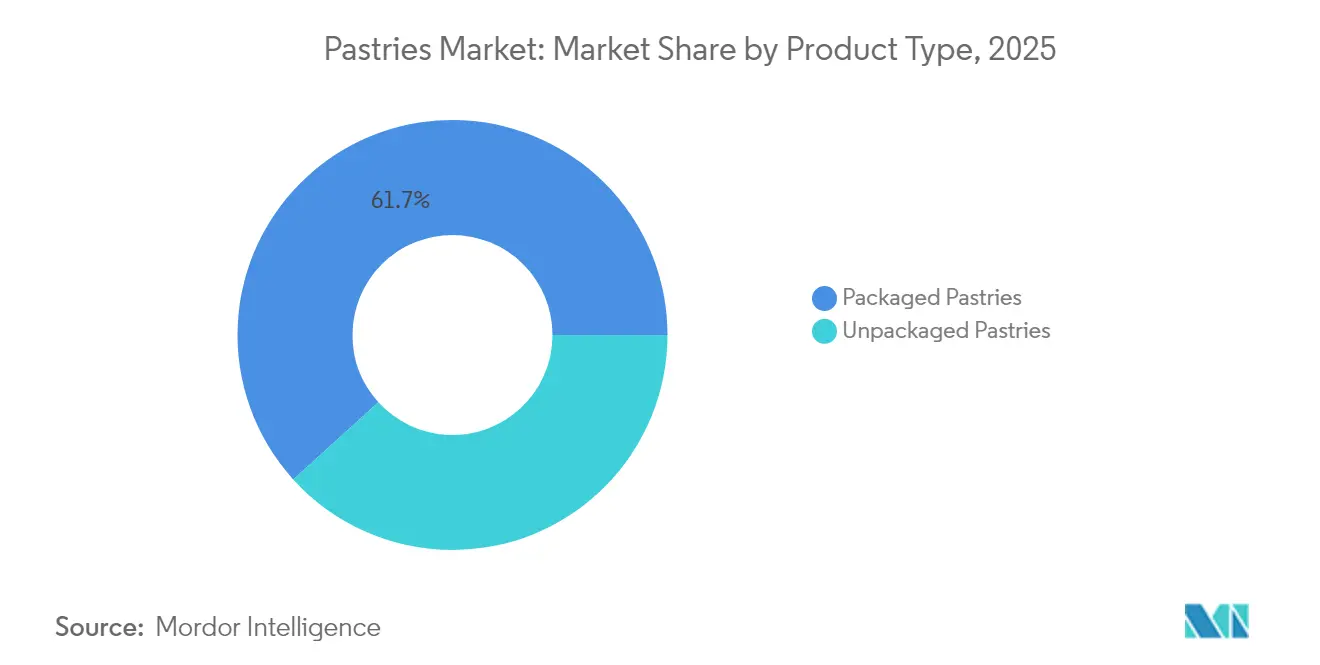

- By product type, packaged pastries captured 61.72% of the pastries market share in 2025, while unpackaged pastries are forecast to expand at a 6.05% CAGR through 2031.

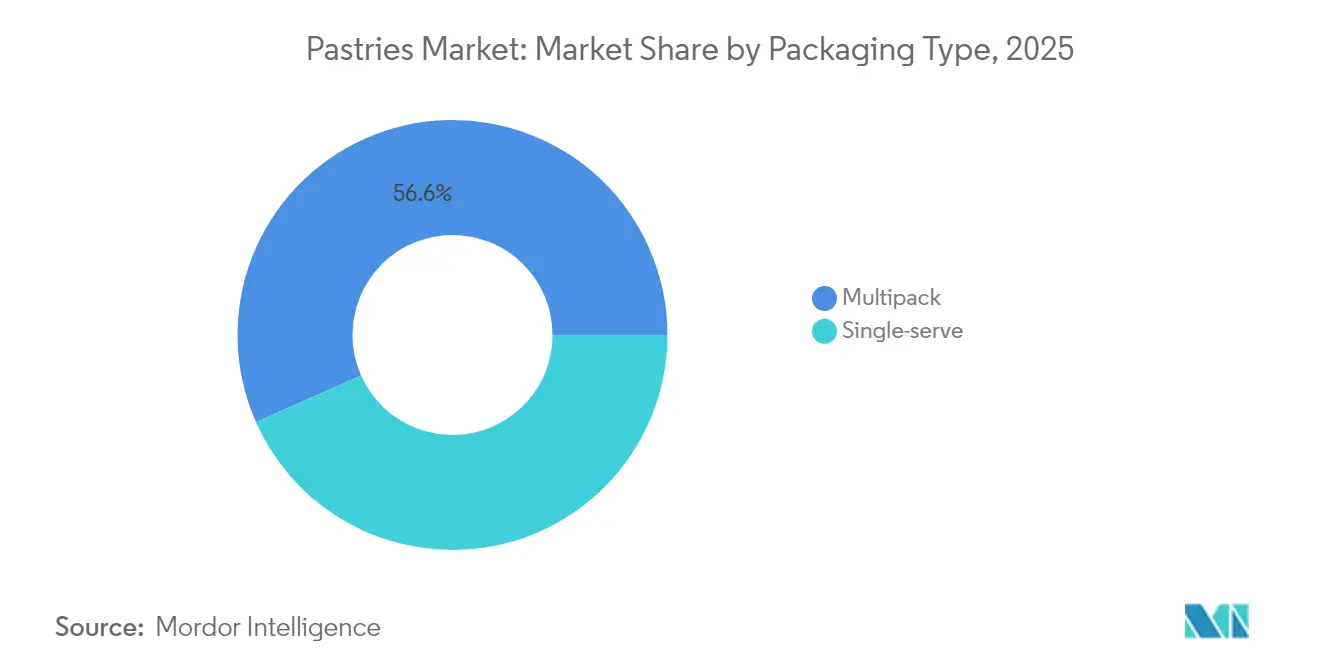

- By Packaging type, multipack formats held 56.64% share of the pastries market size in 2025, and single-serve packaging is advancing at a 7.62% CAGR to 2031.

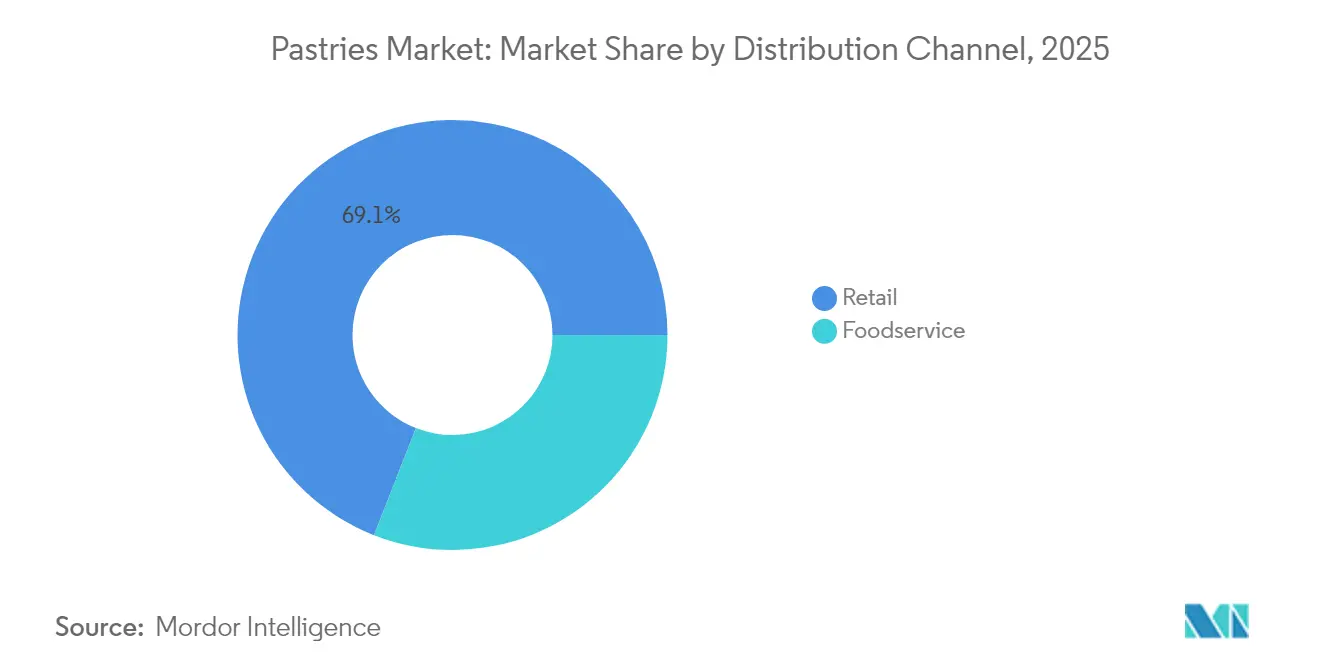

- By distribution channel, retail accounted for 69.05% of global sales in 2025, and foodservice is projected to post the fastest channel growth at 6.88% CAGR during the outlook period.

- By geography, Europe commanded 39.22% of global sales in 2025, whereas the Asia-Pacific is set to deliver the highest regional CAGR of 8.21% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pastries Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenient, ready-to-eat, and frozen pastry products | +1.2% | Global, with early gains in North America, Europe | Medium term (3-4 years) |

| Rising popularity of premium, artisanal, and gourmet pastries | +0.8% | Europe, North America core, spill-over to Asia-Pacific | Long term (≥ 5 years) |

| Emergence of clean-label and specialty diet products | +0.6% | North America and Europe, expanding to Asia-Pacific | Medium term (3-4 years) |

| Flavor innovation and localization | +0.4% | Asia-Pacific core, with adaptation in Middle East and Africa and South America | Short term (≤ 2 years) |

| Technological advancements in baking and preservation | +0.5% | Global, with early adoption in developed markets | Medium term (3-4 years) |

| Increased focus on sustainability and ethical sourcing | +0.3% | Europe and North America, expanding globally | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Growing demand for convenient, ready-to-eat, and frozen pastry products

Consumer lifestyle acceleration has fundamentally shifted purchasing patterns toward convenience-oriented pastry solutions, with frozen bakery products experiencing robust demand due to the extended shelf life capabilities of 6-18 months without preservatives. Post-COVID consumer behavior reinforced trust in frozen products' safety and hygiene standards, while technological advances in production methods, including unfermented, pre-fermented, par-baked, fully baked, and thaw-and-serve processes, enable manufacturers to cater to diverse preparation preferences. Regulatory compliance frameworks like the FDA's FSMA preventive controls enhance consumer confidence in frozen pastry safety and traceability. In addition, frozen and RTE pastries offer significant convenience and have a much longer shelf life (6-18 months) compared to fresh products, which helps reduce food waste for both consumers and businesses. This longevity allows consumers to stock up and enjoy pastries at their leisure. For instance, according to the Department for Environment, Food and Rural Affairs, in 2022/2023, an average of 95 pence per person per week was spent on cakes, buns, and pastries in the United Kingdom[1]Source: Department for Environment, Food and Rural Affairs, "Family Food Survey 2022/2023", gov.uk. Moreover, delivery preferences have intensified, with 30% of consumers now favoring delivery for sweet baked goods, while grab-and-go products surged 50% as convenience becomes paramount.

Rising popularity of premium, artisanal, and gourmet pastries

The premiumization trend has transformed pastry consumption from commodity to experiential indulgence, with Sydney's bakery landscape exemplifying this shift through new artisan establishments opening every two weeks in 2024. Innovative pastries like chocolate bar croissants and miso-glazed Portuguese tarts command premium pricing despite quick sellouts, reflecting consumers' willingness to pay for craftsmanship and unique flavor profiles. This evolution extends beyond traditional offerings to include twice-baked croissants, loaded flatbreads, Basque cheesecake, kouign-amann, and croissant-shell tarts, showcasing creativity and technical expertise. The trend aligns with "affordable luxury" psychology during economic uncertainty, where consumers seek small indulgences as emotional comfort. Moreover, culinary fusion has emerged as a defining characteristic, with pastries incorporating cocktail-inspired flavors, exotic citrus fruits, vinegars, fermented products, and spice combinations that stimulate multiple senses. European markets particularly embrace this trend, with EMEA's cakes and pastries segment representing prominent growth, driven by consumer demand for extraordinary experiences and visual appeal.

Emergence of clean-label and specialty diet products

Health-conscious consumption patterns have catalyzed unprecedented innovation in clean-label pastry formulations, with consumers globally actively limiting sugar intake and seeking transparency in ingredient sourcing. According to the International Food Information Council, in 2023, approximately 29% of respondents in the United States mentioned that they buy food and beverages on a regular basis because they are labeled as "clean ingredients"[2]Source: International Food Information Council, "Food & Health Survey 2023", ific.org. In line with this, manufacturers are responding through sophisticated reformulation strategies, utilizing natural sweeteners like allulose, monk fruit, and stevia blends to maintain sensory properties while addressing health concerns. Plant-based innovations have gained particular traction, with dedicated facilities like Dee's One Smart Cookie eliminating gluten, dairy, soy, peanuts, and tree nuts while maintaining taste integrity through alternative flours including brown rice, sorghum, and millet. Similarly, functional ingredients are increasingly incorporated, with pastries featuring added proteins, superfoods, and hidden vegetables to deliver guilt-free indulgence. Regulatory frameworks like HFSS regulations in the UK are accelerating this transformation, requiring manufacturers to achieve Health Star Ratings of 3.5 or higher, as demonstrated by Grupo Bimbo's commitment to reformulate 100% of core products by end-2025.

Flavor innovation and localization

Regional taste preferences are driving sophisticated localization strategies that extend beyond traditional flavor profiles to embrace cultural fusion and indigenous ingredients. Asia-Pacific markets demonstrate particular dynamism, creating opportunities for pastry manufacturers to integrate local flavors like red bean, matcha, and tropical fruits. For instance, the number of factories of Grupo Bimbo in Asia and Africa amounted to 25; 12 were located in India, 10 in China, 2 in South Africa, and 1 in Morocco. Indian market evolution showcases similar innovation, with ice cream flavors like chilli basil, betel leaf, and masala chai indicating consumer appetite for adventurous taste combinations that could translate to pastry applications. Technological advancement enables precision in flavor development, with AI systems like Kimuraya Sohonten's AI Romance Bread creating emotion-inspired flavor profiles that resonate with local consumer psychology. Hispanic pastries experienced prominent sales growth in the US market, demonstrating crossover appeal beyond ethnic communities and validating localization strategies. The "newstalgia" trend blends familiar childhood foods with modern interpretations, while seasonal and limited-time offerings enable manufacturers to test innovative combinations before full-scale launches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising input and raw material costs | -0.9% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Health concerns over sugar and additives | -0.5% | North America and Europe primarily, expanding globally | Medium term (3-4 years) |

| Growing competition across market segments | -0.4% | Global, with intensity in mature markets | Medium term (3-4 years) |

| Regulatory uncertainty and compliance complexity | -0.3% | Europe and North America core, expanding to Asia-Pacific | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Rising input and raw material costs

In 2024, egg prices in the U.S. jumped to USD 4.15 per dozen, up from USD 2.51 in 2023, as reported by the Bureau of Labor Statistics[3]Source: Bureau of Labor Statistics, "Average Retail Food and Energy Prices, U.S. and Midwest Region,", bls.gov. This surge, with forecasts of further increases in 2025, was attributed to supply chain disruptions, avian flu outbreaks, and industry consolidation. Meanwhile, in India, the Office of the Economic Adviser noted that the Wholesale Price Index for eggs, meat, and fish hit around 172 in the financial year 2024, marking a consistent rise since 2013. Cocoa prices soared to crisis levels, nearing USD 10,000 per metric ton, due to adverse weather in West Africa, with the International Cocoa Organization warning of significant production deficits. Sugar prices reached their highest since 2011, with the FAO noting a 0.8% monthly uptick in the Sugar Price Index, driven by climate change's impact on EU sugar beet crops and Brazilian sugar cane production. U.S. bakeries grappled with new tariffs, escalating costs by 25-35% on essential ingredients. In 2024, the U.S. imported USD 977 million from Canada, USD 679 million from Mexico, and USD 395 million from China. Compounding these challenges, labor shortages led to wage inflation in the baking industry, as documented by the U.S. Bureau of Labor Statistics, pushing production costs higher.

Health concerns over sugar and additives

Consumer health consciousness has fundamentally altered pastry consumption patterns, with two-thirds of consumers actively trying to limit sugar intake and demanding transparency in ingredient composition. This shift extends beyond sugar reduction to encompass broader clean-label expectations, with consumers scrutinizing artificial colors, preservatives, and additives in baked goods. The UK's HFSS regulations in September 2023 exemplify regulatory responses, requiring reformulation of sweet products to meet specific nutritional criteria while maintaining consumer appeal. Cross-cultural research reveals varying motivations for sweet baked product consumption, with sensory appeal remaining the primary driver despite health concerns, creating tension between indulgence desires and wellness goals. Manufacturers are responding through sophisticated reformulation strategies, utilizing precision fermentation and molecular farming to produce alternative sweeteners that replicate sugar's functional properties without compromising taste or texture. The challenge intensifies in emerging markets where traditional sweet preferences conflict with growing health awareness, requiring nuanced approaches that balance cultural expectations with nutritional improvements. Moreover, regulatory compliance frameworks like FDA labeling requirements and EU health claims regulations create additional complexity for manufacturers operating across multiple jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Packaged Dominance Meets Unpackaged Innovation

Packaged pastries commanded 61.72% market share in 2025, reflecting consumer preferences for convenience, extended shelf life, and portion control in increasingly busy lifestyles. This dominance stems from packaged products' superior distribution capabilities, enabling manufacturers to reach diverse retail channels while maintaining product integrity and food safety standards. However, unpackaged pastries are experiencing remarkable growth at 6.05% CAGR through 2031, driven by the artisanal movement and consumers' desire for fresh, customizable experiences that packaged alternatives cannot replicate.

The unpackaged segment benefits from the premiumization trend, with artisan bakeries commanding higher margins through craft positioning and local sourcing narratives. Technological innovations are blurring traditional boundaries, with modified atmosphere packaging and smart packaging solutions extending unpackaged pastries' viability while preserving their fresh appeal. Individual wrapping within the packaged segment has gained particular traction, addressing hygiene concerns while maintaining convenience benefits. The foodservice channel increasingly favors unpackaged options for customization capabilities, while retail environments continue gravitating toward packaged solutions for operational efficiency. Regulatory frameworks like the FDA's FSMA preventive controls apply more stringent requirements to packaged products, creating compliance advantages for established manufacturers with robust quality systems.

By Packaging Type: Single-Serve Surge Challenges Multipack Tradition

Multipack formats maintained 56.64% market share in 2025, leveraging cost efficiency and bulk purchasing appeal among value-conscious consumers and families seeking convenient meal solutions. These formats excel in retail environments where shelf space optimization and inventory turnover drive purchasing decisions, while offering manufacturers economies of scale in production and packaging. Single-serve packaging is disrupting this dynamic with 7.62% CAGR growth through 2031, reflecting fundamental shifts in consumption patterns toward portion control, on-the-go consumption, and individual dietary management.

The single-serve surge aligns with health-conscious trends, enabling consumers to practice mindful indulgence while maintaining caloric awareness. Sustainability considerations increasingly favor single-serve formats that reduce food waste, despite packaging material concerns that manufacturers are addressing through recyclable and compostable innovations. Premium positioning opportunities in single-serve formats enable higher per-unit margins, compensating for increased packaging costs. E-commerce growth particularly benefits single-serve formats, which ship more efficiently and appeal to trial-seeking online consumers exploring new products.

By Distribution Channel: Retail Resilience Meets Foodservice Recovery

Retail channels dominated with 69.05% market share in 2025, demonstrating remarkable resilience through pandemic disruptions and evolving consumer shopping behaviors. Supermarkets and hypermarkets within retail continue leading through extensive product assortments, competitive pricing, and integrated bakery departments that combine convenience with fresh appeal. However, foodservice is experiencing accelerated recovery at 6.88% CAGR through 2031, driven by normalized dining patterns, workplace return trends, and innovative service models that blend retail and foodservice experiences. E-commerce within retail has emerged as a critical growth vector, with online pastry sales benefiting from subscription models, specialty diet categories, and premium product positioning that traditional retail struggles to support.

The convenience store segment within retail demonstrates particular dynamism, with grab-and-go pastry options experiencing 50% growth as consumers seek quick indulgence solutions during daily routines. Foodservice recovery varies by segment, with hotels and catering showing stronger momentum than restaurants, which face ongoing labor challenges and margin pressures. Hybrid models are emerging, with retail bakeries expanding foodservice capabilities through in-store cafes, while foodservice operators develop retail product lines for take-home consumption. Digital integration across both channels enables personalized experiences and loyalty programs that drive repeat purchases and customer lifetime value.

Geography Analysis

Europe’s pastries market leadership rests on a 39.22% revenue share in 2025, anchored by centuries-old patisserie culture and consumer willingness to pay premiums for provenance and craftsmanship. The broader EMEA bakery segment has been growing despite tightened environmental and sugar-reduction rules, accelerated recipe innovation, and sustainable packaging adoption. Energy-cost inflation and post-Brexit supply-chain recalibration remain operational challenges but also spur regional sourcing initiatives that reinforce local authenticity narratives.

Asia-Pacific delivers the fastest pastries market CAGR at 8.21%, propelled by urbanization, rising household incomes, and social-media-driven taste experimentation. China’s snack-food sector is on the growth curve, making localized red-bean croissants and mango-filled Danish staples for Gen Z consumers. India’s middle class multiplies pastry sales as Western-style cafés expand beyond Tier 1 cities, while Southeast Asian markets incorporate pandan, durian, and ube into laminated dough products. Regulatory diversity compels tailored labeling and fortification strategies across countries.

North America records measured growth as premium, clean-label, and single-serve innovations offset mature category volumes. Mexico’s integration within USMCA supply networks yields raw-material cost advantages, though recent U.S. tariffs inject uncertainty. Canadian markets emphasize organic certification and bilingual labeling that increase compliance costs but enable premium positioning. The Middle East and Africa remain nascent yet promising; the UAE and South Africa anchor investment thanks to tourism, expat populations, and rising modern retail penetration. Infrastructure gaps and currency volatility restrain wider regional uptake for now.

Competitive Landscape

Industry structure remains moderately fragmented; no brand controls more than mid-single-digit global pastries market share, yet consolidation is accelerating. Mars’s USD 35.9 billion bid for Kellanova and Flowers Foods’ USD 795 million Simple Mills deal exemplify strategic moves toward health-oriented, higher-margin snack categories. Similarly, Grupo Bimbo invests USD 2 billion through 2027 in automation and sustainability projects, targeting a 3.5 or higher Health Star Rating for all flagship SKUs.

Technology adoption diverges: multinationals deploy AI root-cause analysis to trim dough waste, while SME bakeries ‘rent’ capacity in shared facilities to access high-speed sheeters without heavy capex. White-space opportunities abound in plant-based, gluten-free, and culturally fused pastries, areas where agile direct-to-consumer brands leverage social commerce and local sourcing stories to scale quickly.

Retailer private labels extend reach through artisan-style launches at value price points, putting margin pressure on branded incumbents. Meanwhile, ingredient suppliers deepen collaboration on sugar-reduced fillings and cocoa-butter equivalents that meet upcoming emission targets. Venture capital targets refrigerated-dough start-ups offering cleaner labels and simplified ingredient decks, underscoring continued innovation potential within the pastries market.

Pastries Industry Leaders

-

Grupo Bimbo

-

Aryzta AG

-

Flowers Foods, Inc.

-

Mondelez International

-

Yamazaki Baking Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Delice de France launched 42 new products, including international flavors in breads, pastries, cakes, and drinks. Notable pastry items included Greek filo pastry rolls (spinach and feta, chicken and BBQ sauce), a pistachio-filled doughnut, churros, and authentic Portuguese Pastel de Nata in Original, Salted Caramel, and Apple varieties.

- December 2024: M’s Bakery introduced a unique fusion pastry combining kimchi and smoked cheese in a laminated bear claw pastry. It was designed with on-trend Asian flavors and gut health benefits wrapped in a convenient snack format, earning accolades at the Baking Industry Awards.

- June 2024: Asda introduced a tiramisu-flavored Danish pastry filled with aromatic coffee and creamy mascarpone, topped with cocoa powder, and asserted it to be a classic dessert flavor in baked goods in a convenient ready-to-eat format.

- March 2024: Marks & Spencer (M&S) launched a premium range of celebration pastries, including the Brown Sugar and Salted Caramel Cake. This cake featured a brown sugar sponge enriched with dates, sticky salted caramel sauce, and a salty-sweet miso buttercream topping.

Global Pastries Market Report Scope

Pastries are various baked products made from flour, sugar, milk, butter, shortening, baking powder, and eggs. Pastries are considered bakers' confectionery products. The global pastry market is segmented by flavor, product type, distribution channel, and geography. By flavor, the market includes sweet and savory pastries. By product type, the market is segmented into packaged pastries and unpackaged or artisanal pastries. By distribution channel, the market is segmented into on-trade and off-trade channels. Off-trade channels further include supermarkets/hypermarkets, convenience/grocery stores, specialty stores, online retail stores, and other distribution channels. Moreover, the study analyzes the pastries market in the emerging and established markets worldwide, including North America, Europe, Asia-Pacific, South America, and Middle-East & Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Packaged Pastries |

| Unpackaged Pastries |

| Single-serve |

| Multipack |

| Foodservice | Restaurants |

| Hotels | |

| Catering | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Retail Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Packaged Pastries | |

| Unpackaged Pastries | ||

| By Packaging Type | Single-serve | |

| Multipack | ||

| By Distribution Channel | Foodservice | Restaurants |

| Hotels | ||

| Catering | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the pastries market?

The pastries market was valued at USD 43.76 billion in 2026, with projections pointing to USD 52.97 billion by 2031.

Which region leads sales of pastries worldwide?

Europe holds the largest share at 39.22% of 2025 global revenue, thanks to entrenched patisserie traditions and premium consumer preferences.

Which region is growing fastest for pastries?

Asia Pacific posts the highest CAGR at 8.21% through 2031, driven by rising incomes and Western-style snack adoption.

How are health trends influencing pastry formulation?

Brands are reformulating with clean-label ingredients, sugar substitutes, and specialty-diet recipes to meet demand from 83% of consumers seeking lower sugar intake.

What packaging format is gaining traction in pastries?

Single-serve packs are outpacing multipacks with a 7.62% CAGR to 2031 because they support portion control and on-the-go snacking.

How is technology helping pastry manufacturers?

AI-enabled root-cause analysis has reduced production waste by up to 37%, improving margins amid volatile ingredient prices.

Page last updated on: