Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

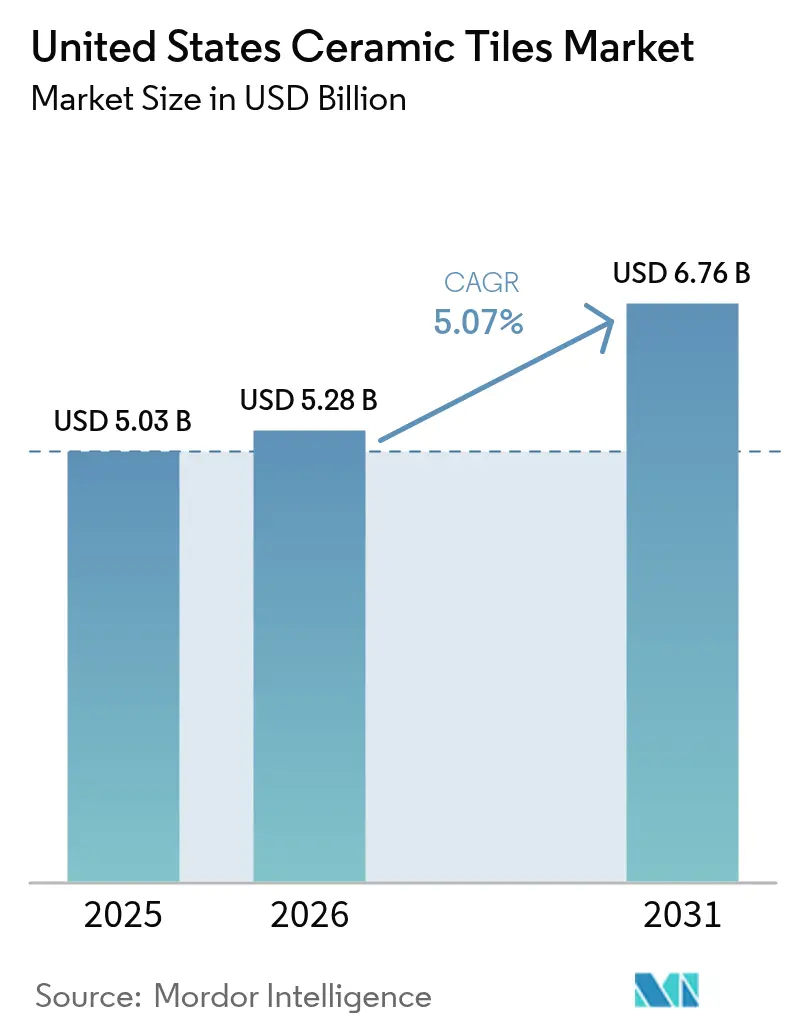

| Base Year Market Size (2025) | USD 5.03 Billion |

| Market Size (2026) | USD 5.28 Billion |

| Market Size (2031) | USD 6.76 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Ceramic Tiles Market Analysis by Mordor Intelligence

The United States ceramic tiles market size reached USD 5.03 billion in 2025, is on track to reach USD 5.28 billion in 2026, and is projected to grow to USD 6.76 billion by 2031, registering a 5.07% CAGR during 2026-2031. In 2026, porcelain tiles are expected to dominate product-type demand, while digital printing enhances design quality, offering a broader selection at reduced costs. Residential demand remains strong in 2026, but commercial sectors such as hospitality, healthcare, and transport are advancing at a faster pace. This growth is driven by the adoption of zero-VOC surfaces and antimicrobial glazes, which align with the health, safety, and cleaning standards emphasized by facility owners in the post-pandemic landscape. Domestic producers benefit from trade remedies that are shifting sourcing away from high-duty origins. However, challenges such as energy inflation and a shortage of skilled labor are moderating profit margins and throughput in the United States ceramic tiles market. Renovation and replacement activities account for 61.72% of the market share, reflecting an aging housing stock and sustained remodeling trends. The National Association of Home Builders Q4 2025 survey identified bathroom remodeling as the most common project, with an average score of 4.1 out of 5.0[1]National Association of Home Builders, “Top Remodel Projects 2025,” NAHB, nahb.org . Additionally, Realm Home projects that total home renovation spending in the United States will reach a record USD 524 billion by early 2026.

Key Report Takeaways

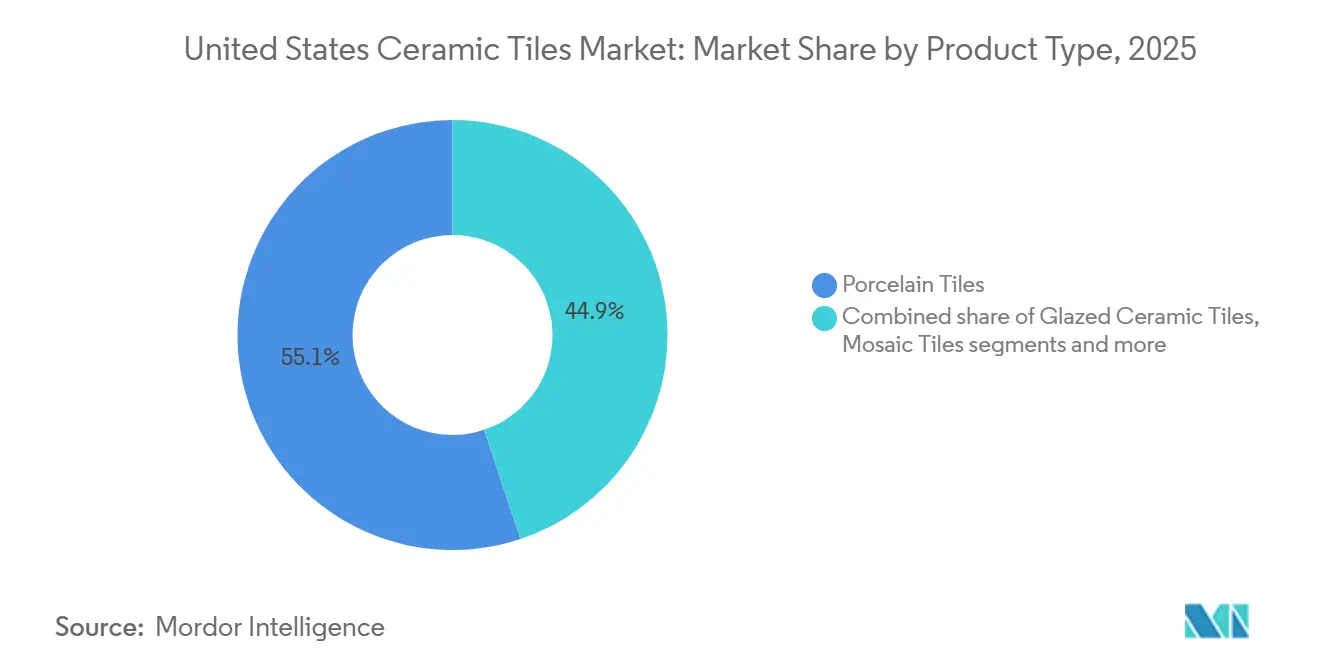

- By product type, porcelain led with 55.12% market share in 2025 and is forecast to expand at a 6.31% CAGR through 2031.

- By application, floor installations accounted for a 68.05% share of the United States ceramic tiles market size in 2025, and walls are projected to advance at a 5.59% CAGR through 2031.

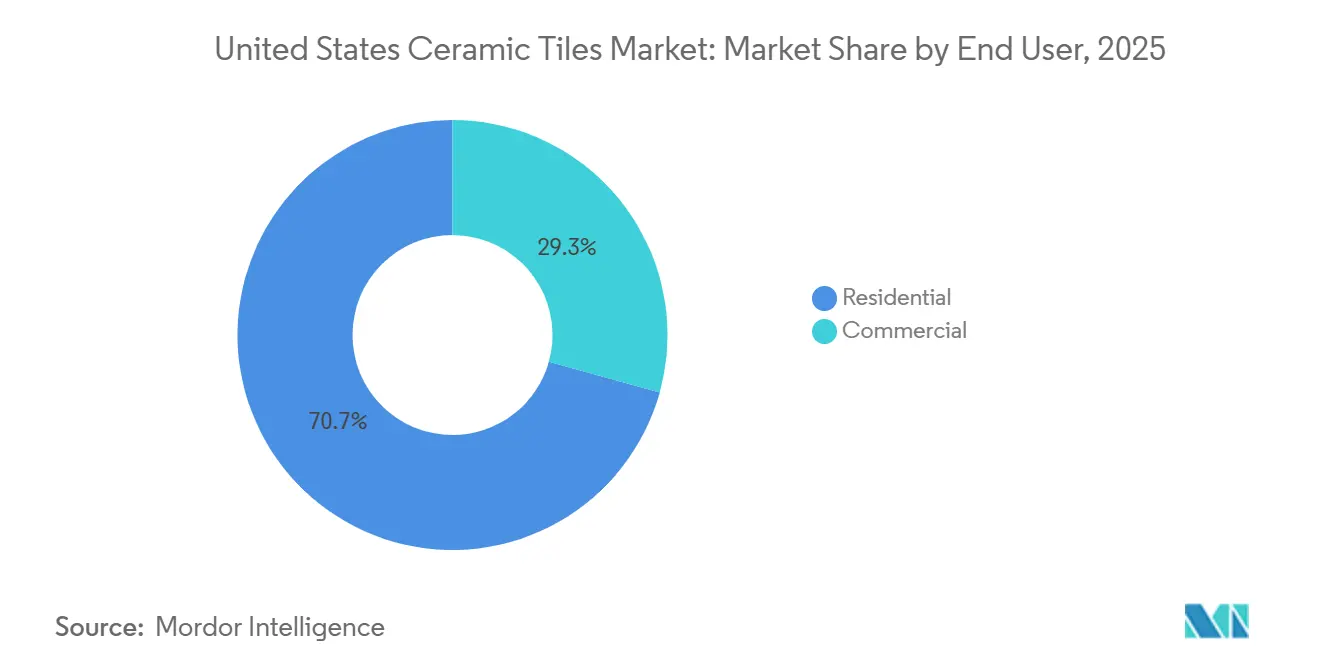

- By end-user, residential held 70.70% of the 2025 demand, while commercial is projected to record the highest CAGR at 5.81% through 2031.

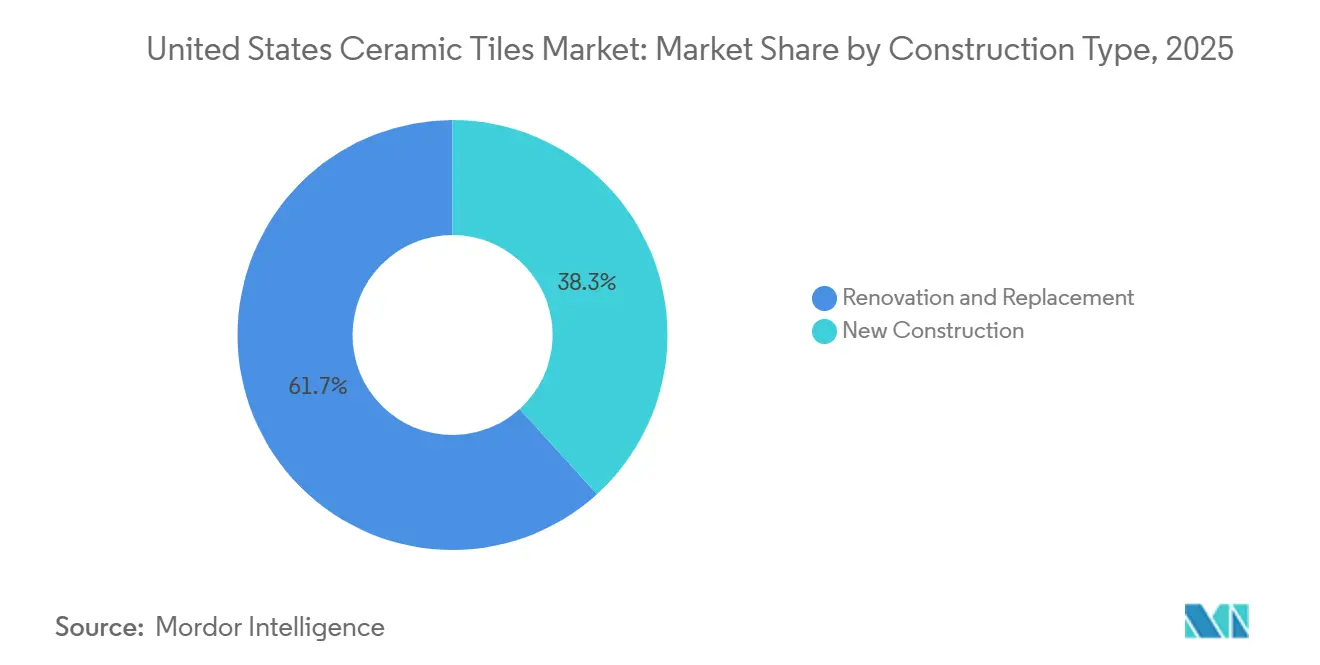

- By construction type, renovation and replacement commanded 61.72% of the United States ceramic tiles market size in 2025, whereas new construction is forecast to grow at a 5.67% CAGR through 2031.

- By distribution channel, specialty tile and stone stores held 42.10% of 2025 revenue, and online retail is projected to grow fastest at 6.18% CAGR through 2031.

- By geography, the Southeast accounted for 28.85% of 2025 revenue, while the West is projected to record the fastest CAGR at 5.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remodeling Momentum in Kitchens/Baths | +1.5% | National, strongest in the Northeast and Southeast, aging stock | Medium term (2-4 years) |

| Design and Technology Upgrades | +1.2% | National, premium uptake in the West and the urban Northeast | Short term (≤ 2 years) |

| Hygiene, Moisture Resistance, and Durability in Wet/High-Traffic Areas | +0.9% | National, heightened in commercial healthcare and hospitality | Medium term (2-4 years) |

| Sustainability Alignment with EPDs and LEED v4.1 | +0.7% | National, led by California, Oregon, and Washington | Long term (≥ 4 years) |

| Trade Remedies Supporting Domestic and Mear-Shore Supply | +0.6% | National, production concentrated in Tennessee and Alabama | Medium term (2-4 years) |

| Climate-Disaster Rebuilding Favors Resilient Finishes | +0.4% | Southeast coastal, Southwest wildfire zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Remodeling Momentum in Kitchens and Baths

Bathroom and kitchen remodeling ranked as the two most frequent residential projects, with NAHB data showing bathroom work scoring 4.1 and kitchen work 3.9 on a 5.0 scale in Q4 2025, which signaled broad-based intent and strong project pipelines for tile selections in 2026. Mid-tier budgets often prioritize glazed ceramic for visual upgrades and long service life, while premium remodels move to large-format porcelain slabs that deliver stone-like continuity with lower maintenance. Ceramic’s moisture resistance and long lifespan in wet zones protect resale value in high-humidity and coastal metros where buyers value durable, easy-to-sanitize surfaces. As renovation spending remains elevated, distributors and specialty retailers benefit from steady replacement cycles that reduce reliance on new-home construction. The USD 524 billion renovation spending forecast for early 2026 signals sustained replacement cycles even if new-construction starts plateau, de-risking volume for tile distributors and specialty retailers[2]Realm Home. "2026 Home Renovation Trends: What 2025 Taught Us and What's Next," Realm Home, realmhome.com.

Design and Technology Upgrades

Digital inkjet systems now deliver wood, marble, and concrete visuals with high fidelity, which compresses design cycles and encourages annual refreshes rather than biennial updates across many United States assortments. Large-format tiles, 24x48-inch formats standard, with 16x32-inch and 32x32-inch emerging, reduce grout-line density, accelerate installation, and amplify slab-like continuity prized in minimalist and transitional design schemes[3]MSI Surfaces, “Textured Porcelain for Walls and Floors,” MSI Surfaces, msisurfaces.com . Tactile innovation raises the ceiling on visual realism, with Daltile’s RevealSync3D and MSI’s TileTouch synchronizing texture and graphics to reduce misalignment between what users see and what they feel. These advances reinforce domestic design leadership and make it harder for commodity imports to compete on look and feel at similar price points. In 2026, the United States ceramic tiles market benefits from showroom merchandise with fewer SKUs with a broader range, then pair them with visualization tools to help buyers make choices faster. Continued investment in presses and surface technologies sustains a quality gap that supports a premium mix while keeping value-grade glazed ceramic relevant for price-sensitive remodels.

Hygiene, Moisture Resistance, Durability in Wet/High-Traffic Areas

Corporate and institutional upgrades maintain a preference for hard, low-porosity surfaces that tolerate frequent cleaning without degrading, which reinforces ceramic’s role in healthcare, education, and passenger hubs that need high abrasion resistance and color stability. Ceramic emits zero VOCs at the product level, supports healthier interior environments when paired with compliant grouts and adhesives, and aligns with design standards that prioritize low-emitting materials. In high-traffic corridors and wet areas, porcelain’s ≤0.5% water absorption meets ASTM C373 performance needs and retains function through repeated exposure to cleaning agents. Facility owners also weigh the total cost of maintenance over a decade and report lower cleaning labor requirements with ceramic compared to soft surface options, which strengthens the lifecycle value case in operations-driven budgets. Commercial specifiers also seek predictable slip resistance and abrasion performance, making DCOF and PEI ratings part of routine submittals and approval processes under ANSI A137.1 and related standards. These attributes keep ceramic central to resilient design criteria where hygiene, moisture management, and safety documentation are procurement prerequisites.

Sustainability Alignment (EPDs, LEED v4.1 credit pathways)

Crossville's entire US-manufactured porcelain portfolio carries Green Squared certification (ANSI A138.1), enabling automatic LEED v4.1 material-ingredient disclosure and regional-materials credits for projects within 100 miles of Tennessee production[4]Crossville Inc., “Green Squared and LEED Documentation,” Crossville Inc., crossvilleinc.com. Crossville maintains Green Squared certification across its United States porcelain portfolio, providing a recognized framework for responsible manufacturing alongside documented EPDs that procurement teams can audit. Florim United States advanced differentiation by introducing carbon-neutral tile collections and achieving B Corp certification in 2025, which positioned the company to compete for ESG-driven RFPs in hospitality and healthcare. Recycled content strategies, factory upgrades, and energy credit programs together lower the embodied carbon profile without trading off durability or cleanability that building operators demand. As codes and owner standards evolve into 2026, the United States ceramic tiles market sees more bid documents referencing EPDs, third-party validations, and Green Squared eligibility as table stakes in public and private solicitations. These documented attributes reduce submittal friction and help domestic brands meet regional-materials preferences where applicable.

Restraints Impact Analysis*

| Restraint | Geographic Relevance | Impact Timeline | |

|---|---|---|---|

| Competitive Displacement by Resilient Flooring in Remodel and Multifamily | -0.8% | National, acute in multifamily and budget-remodel Southeast | Medium term (2-4 years) |

| Skilled Labor Scarcity and Rising Installation Labor Rates | -0.6% | National, severe in urban Northeast and West high-wage markets | Long term (≥ 4 years) |

| Silica-Dust Compliance Costs and Work-Practice Constraints | -0.3% | National, elevated in contractor-heavy Northeast and West | Medium term (2-4 years) |

| High Import Exposure and Logistics, and Port Bottlenecks | -0.4% | National, concentrated in coastal gateway ports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competitive Displacement by Resilient Flooring (LVT, SPC, engineered wood) in Remodel and Multifamily Segments

Resilient categories such as LVT and SPC compete on lower installed cost and faster throughput, which makes these options attractive in value-focused remodels and multifamily turn projects where time to rent is critical. Builders often choose resilient when they seek less substrate preparation compared with tile installations that may require underlayment and leveling in older buildings. Style replication has improved in resilient formats, yet ceramic maintains an advantage in scratch resistance, UV stability, and long service life that matters more in high-traffic zones and premium residential spaces. The displacement pressure is most visible where first cost dominates the decision process, whereas projects that weigh lifecycle costs and hygiene profiles tend to keep ceramic in scope. Large-format porcelain and thin panels help ceramic compete by reducing labor hours and grout joints, narrowing the install-speed gap on suitable substrates. In 2026, the United States ceramic tiles market continues to face this competitive dynamic, so brands emphasize lifecycle value, indoor air quality, and durability to defend share in mixed-material bid lists.

Skilled Labor Scarcity and Rising Installation Labor Rates Constrain Project Throughput and Affordability

Installers with advanced tile-setting skills remain in short supply as retirements outpace apprenticeship completions, and this scarcity sustains wage pressure across many urban markets. Contractors report tight schedules and limited crew capacity, which constrain the number of simultaneous tile jobs they can staff during peak months. Hourly earnings trends and overtime premiums lift installed costs, which weakens the value case for ceramic in some budget-constrained remodels where a simpler resilient solution can be self-installed. Multifamily and commercial program managers react by standardizing formats and layouts that speed coverage, while also shifting some projects to materials that need fewer specialized skills. The United States ceramic tiles market adapts by promoting modular large-format options and job-site tools that compress layout and cutting times without compromising finish quality. Even with these workflow improvements, labor availability remains a structural headwind on throughput and affordability in 2026, especially in high-wage coastal metros.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Dominance Expands Across Applications

Porcelain tiles commanded 55.12% of the United States ceramic tiles market share in 2025 and are forecast to grow at a 6.31% CAGR through 2031. Outdoor applications benefit from 2cm pavers that provide slip resistance and thermal stability, while 6mm ultra-thin panels simplify overlays in renovation work and keep demolition and disposal to a minimum. Manufacturers deploy next-generation presses to deliver large slabs with consistent veining and minimal warpage, which extends porcelain’s reach in commercial lobbies and open-plan homes. Daltile’s portfolio expansion in large-format and textured surfaces illustrates how synchronized graphics and relief can improve the perceived value of porcelain in premium projects. Glazed ceramic remains important for feature walls and moderate-traffic interiors where rich graphics matter most and budgets favor lighter-duty performance profiles. Unglazed options maintain a niche presence in high-slip-risk outdoor and industrial locations where friction performance is a core requirement, although periodic sealing and maintenance can raise ownership costs over time. Mosaics resurge in backsplashes and accent zones as fabricators cut custom patterns from larger panels to deliver tailored designs at scale. Decorative and handmade tiles remain a protected premium tier, with artisanal finishes and small-batch production appealing to restoration and luxury buyers who prioritize uniqueness over speed.

Porcelain’s performance case resonates as project scopes widen into outdoor living, hospitality corridors, and healthcare spaces that demand durability under intense cleaning requirements. Material advances also support the United States ceramic tiles industry as domestic plants integrate technologies that enhance strength and surface realism. Continued product development in thin panels helps installers reduce labor hours and grout joints, supporting a smoother path to project acceptance on time-constrained jobs. As remodelers and fabricators embrace slab formats, porcelain’s competitive set shifts more squarely toward natural stone and engineered surfaces rather than resilient flooring. Over 2026, marketing and showroom strategies concentrate on fewer but more capable lines that cover residential, commercial, indoor, and outdoor needs with cohesive color systems. This approach helps buyers navigate choice without sacrificing design range, and it reinforces porcelain’s leadership within product-type demand in the United States ceramic tiles market.

By Application: Floor Installations Lead, While Wall Segments Capitalize on Digital Printing

Floor applications accounted for 68.05% of the United States ceramic tiles market share in 2025, with specifications supported by abrasion resistance targets at PEI 4 to 5 and stable DCOF performance under ANSI A137.1, while wall segments are projected to accelerate at a 5.59% CAGR through 2031 as photorealistic visuals substitute for stone in vertical installations. Large-format tiles reduce the number of grout joints, improve aesthetics, and shorten installation timelines in living areas, kitchens, and commercial traffic zones. Wall programs leverage lighter, thin panels that reduce structural load and speed application for feature walls, shower surrounds, and lobby statements. Digital printing keeps expanding design palettes across marble, terrazzo, concrete, and wood looks, enabling cohesive floor-to-wall pairings. Outdoor floors, pools, and decks benefit from 2cm porcelain pavers, which offer thermal stability and slip resistance in climates with heat extremes. Roofing remains a niche application in selected architectural styles where fire resistance and service life are priorities, although competing systems gain share on weight and installed cost.

In showers and backsplashes, larger formats minimize potential water ingress points and reduce maintenance by cutting grout exposure. Three-dimensional surface technologies allow designers to introduce tactile depth on walls while maintaining cleanability, raising the perceived value of premium wall tiles in commercial and residential projects. In offices, education, and healthcare, vertical surfaces that meet strict cleaning protocols can support overall hygiene strategies and resist discoloration under routine disinfection. Product development continues to narrow the gap between wall and floor capabilities through color-matched systems that allow consistent design language across zones. The result is steady growth in wall demand, which diversifies project mix beyond floors and sustains incremental value per project for the United States ceramic tiles market.

By Construction Type: Renovation Dominates as New Construction Gains Momentum

Renovation and replacement captured 61.72% of the United States ceramic tiles market size in 2025, reflecting an aging housing stock where bathrooms and kitchens are recurring upgrade priorities for homeowners. Thin porcelain panels allow direct overlays on suitable substrates, which helps control demolition, dust, and disposal costs and accelerates job timelines. In high-humidity regions, ceramic becomes the default choice in showers and wet rooms when budgets permit a long-lifespan solution. Homeowners balancing cost and performance often phase projects, and ceramic packages fit those plans as specialty retailers help align selections with scope and budget. The work is steady and can be scheduled year-round, which reduces seasonality in contractor pipelines and keeps tile distributors engaged with local remodelers.

New construction holds 38.28% in 2025 and is projected to grow at a 5.67% CAGR through 2031, supported by household formation and population migration trends in the Sun Belt, where builders prioritize ceramic in wet zones to reduce future callbacks. Recovery programs after climate events add a layer of demand for resilient interiors where ceramics’ moisture resistance and non-combustible nature are useful. Builders also seek installation efficiencies, so large-format floor tiles and coordinated wall systems speed coverage during tight closings. As national and regional builders integrate tile packages into standard offerings, supply partners with domestic capacity and tight logistics gain share on reliability. Across both construction types, installers value stable shade and size calibrations, and domestic producers reinforce this through tighter process controls and documented quality standards in 2026.

By End-User: Residential Volume Anchors Market While Commercial Growth Accelerates

Residential accounted for 70.70% of the United States ceramic tiles market size in 2025, underpinned by the frequency of bathroom and kitchen remodeling projects validated by NAHB’s Q4 2025 rankings for project commonality. Households that move beyond resilient flooring price bands tend to favor ceramic for wet rooms and high-traffic zones where longevity and resale value matter. In premium segments, large-format porcelain slabs create seamless looks that substitute for natural stone without maintenance burdens. In the mid-market, glazed ceramic provides a budget-sensitive aesthetic upgrade with a wide range of styles. Commercial demand is projected to grow faster at a 5.81% CAGR through 2031 as healthcare systems, institutions, and hospitality chains maintain investments in cleanable, low-VOC finishes.

Hospitality and retail settings often specify porcelain in lobbies, corridors, and high-traffic sales areas where abrasion resistance and rolling-load durability are essential. Airports and transit hubs require slip resistance and water absorption compliance under ANSI and ASTM references, and tile meets these criteria without the delamination risks associated with adhesive-backed systems in temperature-cycling zones. Offices and institutional projects incorporate ceramic to meet documentation requirements for material health and embodied carbon through EPDs and Green Squared credentials. The United States ceramic tiles industry supports these end-user needs with verified testing and submittal packages that simplify approval across owner and building-code workflows. As owners standardize finish schedules for new builds and refreshes, ceramic’s documented performance supports consistent procurement across large property portfolios in 2026.

By Distribution Channel: Specialty Stores Lead as Online Retail Surges

Specialty tile and stone stores held 42.10% of 2025 revenue and continue to lead on complex projects where designers, contractors, and homeowners need technical guidance, sample depth, and submittal documentation. These locations support code questions, slip resistance, cleaning chemistry, and installation planning that exceed the scope of typical retail environments. Home improvement chains are important for DIY and basic pro projects and continue to refine omnichannel order pickup, volume pricing, and core SKU availability. Online retail grows fastest at a projected 6.18% CAGR as augmented-reality and visualization tools let buyers preview finishes in real spaces and reduce regret-driven returns. Direct sales teams support commercial bids with project staging and job-site delivery, which is a critical enabler on multi-location rollouts. E-commerce benefits from lower overhead, yet logistics demands for heavy, fragile products keep professional channels important for large projects, shade control, and claim resolution. Producer websites and showrooms supply ANSI, ASTM, and ISO documentation that specifiers expect in submittals, which sustains the role of expert-assisted channels for code-compliant jobs.

Geography Analysis

The Southeast accounted for 28.85% of the 2025 market size, supported by hurricane recovery, population inflows, and high humidity conditions that keep tile central in baths, kitchens, and entries; the region’s share reflects its deep pipeline of renovations and new builds that specify ceramic for durability and moisture control. Builders in Georgia and the Carolinas continue to include tile as a differentiator in wet zones to reduce service calls that may occur with less stable finishes. Florida’s recovery and resilience standards maintain a preference for flood-resistant and mold-resistant interiors, which underpins steady demand for tile on ground floors. Comparing historical momentum to the current cycle, the Southeast’s acceleration comes from a mix of disaster rebuilds, remodel intensity, and code-conscious new construction that values material longevity. The United States ceramic tiles market also benefits from the Southeast’s proximity to domestic production in Tennessee, which improves fulfillment time for common sizes and colors. As 2026 progresses, installer capacity and job-site coordination remain the gating factors on throughput rather than end-user demand.

The West is projected to grow fastest at a 5.65% CAGR through 2031, led by California and Pacific Northwest metros where energy codes, wildfire resilience, and design-forward preferences align with ceramic’s performance and aesthetics. Large-format slabs and thin panels are popular in open-plan remodels and commercial lobbies in San Francisco, Seattle, and Portland, and slip-resistant outdoor pavers see traction around pools, patios, and rooftop spaces exposed to heat and sun. Builders in wildfire-prone areas continue to seek non-combustible finishes for critical zones, and owners specify easy-to-clean surfaces for frequent maintenance cycles. In dense urban markets, thin panels reduce structural loads and simplify vertical logistics in elevator-served projects. Specialty retailers and distributors in the West collaborate closely with installers to ensure calibrated lots for large jobs, which reduces shade variation risks on walls and floors. The United States ceramic tiles market gains from design leadership in this region, which often sets style direction for other metros through national retail and hospitality concepts.

The Midwest and Northeast deliver consistent remodel activity, supported by older housing stock and institutional refresh programs that value ceramic’s lifecycle performance. Midwestern producers benefit from favorable kiln energy economics that help balance margin pressure from freight and labor. In the Northeast, high labor rates encourage the use of large formats and efficient layouts that reduce grout work and speed coverage on union crews. Multifamily retrofits and brownstone renovations in New York and Boston rely on thin panels for feature walls due to weight and logistics constraints. The Southwest’s heat exposure supports demand for outdoor pavers that resist thermal shock and UV discoloration, especially in Arizona and Nevada. Across regions, state-level regulations and health standards reinforce material selection, including Proposition 65 limits on heavy metals in glazes that domestic producers address through compliant formulations. LEED v4.1 and EPD documentation from leading domestic brands simplify submittals for public and private owners, which strengthens regional uptake where sustainability documentation is part of standard bid packets.

Competitive Landscape

The United States ceramic tiles market shows moderate concentration, with a group of domestic brands and major import distributors competing across price tiers and channels rather than a single dominant player. Domestic manufacturers such as Daltile, Crossville, Florida Tile, StonePeak, Portobello America, and Florim United States leverage tariff protections and expanded United States capacity to reduce lead times and raise service reliability for national accounts. Product strategy emphasizes synchronized surface textures, large-format slabs, and verified technical performance under ANSI and ASTM standards to support specifications in commercial programs. On sustainability, manufacturers promote Green Squared certification, EPDs, and carbon-neutral lines to meet LEED v4.1 requirements and buyer ESG mandates without sacrificing performance in wet or high-traffic zones.

Omnichannel reach is another point of differentiation. Specialty tile and stone stores provide technical selling and sample depth for complex jobs, big-box partnerships expand exposure on core SKUs for DIY and pro shoppers, and digital visualizers on brand sites help buyers shorten decision cycles. Distributor consolidation increases purchasing leverage, highlighted by the creation and expansion of Artivo Surfaces, which aligns Virginia Tile and Galleher, and later acquired Walker Zanger and Anthology to strengthen high-end showrooms across many United States markets. Manufacturers respond by offering national assortments, exclusive programs by channel, and rapid replenishment from domestic plants. The United States ceramic tiles market also features innovation from thin panel specialists and outdoor paver lines that address roof decks, patios, and plazas where slip resistance and thermal stability are essential.

Daltile’s trend reports and domestic new collections demonstrate ongoing investment in large-format, synchronized textures and through-body options that improve edge aesthetics on cuts. MSI’s TileTouch raises tactile realism in porcelain lines and reinforces the role of visualization, AR, and digital content in merchandising and selection. Crossville expanded carbon-neutral collections and rolled out thin panels with recycled content that meet documentation needs for institutional owners. Florim USA’s B Corp certification and carbon-neutral series add a distinctive sustainability signal in competitive bids and align with corporate procurement standards. Portobello America’s capacity ramp in Tennessee improves regional availability and cost control for United States projects that prefer domestic sourcing due to lead times and tariff sensitivity. Together, these moves shape a market that rewards product performance, documentation, speed, and national service coverage in 2026.

United States Ceramic Tiles Industry Leaders

-

Daltile

-

Anatolia Tile & Stone

-

Emser Tile

-

MSI Surfaces

-

Crossville Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Artivo Surfaces Expands Portfolio with Walker Zanger and Anthology Brands Acquisition Artivo Surfaces, backed by Transom Capital, finalized an agreement to acquire luxury brands Walker Zanger and Anthology from Mosaic Companies.

- March 2025: Daltile launched its ONE Quartz extra-large slab portfolio at KBIS 2025, introducing eight marble-inspired designs for high-traffic commercial surfaces.

United States Ceramic Tiles Market Report Scope

The ceramic tiles market involves the production, distribution, and consumption of ceramic tiles, including porcelain and stoneware types. It encompasses applications in residential, commercial, and industrial settings, with distribution through retail, online platforms, and wholesalers, reflecting trends in eco-friendliness and design innovation.

The ceramic tiles market in the United States is segmented by product (glazed, porcelain, scratch-free, and other products), application (floor tiles, wall tiles, and other applications), construction type (new construction and replacement & renovation), end user (residential, and commercial), and distribution channel (home centers, specialty stores, online, distributors, and other distribution channels). The market size and forecast are provided in value (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By Construction Type

| New Construction |

| Renovation and Replacement |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Northeast |

| Midwest |

| Southeast |

| Southwest |

| West |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Northeast | |

| Midwest | ||

| Southeast | ||

| Southwest | ||

| West | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the United States ceramic tiles market?

The United States ceramic tiles market size reached USD 5.03 billion in 2025, is on track for USD 5.28 billion in 2026, and is projected to reach USD 6.76 billion by 2031 at a 5.07% CAGR.

Which product type leads demand in the United States ceramic tiles market?

Porcelain led in 2025 with 55.12% share and is also the fastest growing product type through 2031 due to low water absorption, slab formats, and 2cm pavers.

Where is demand strongest by application in the United States ceramic tiles market?

Floor installations dominate with a 68.05% share, while walls are projected to grow faster on the back of digital printing and thin panel adoption in remodels.

Which end-user segments are advancing fastest in 2026?

Commercial programs are projected to grow at a 5.81% CAGR through 2031, driven by healthcare, hospitality, education, and transport hubs that prioritize durable and low-VOC surfaces.

How are trade remedies affecting the United States ceramic tiles market?

Sustained anti-dumping and countervailing duty actions on selected import origins support domestic capacity

Page last updated on: