Solid Tumor Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

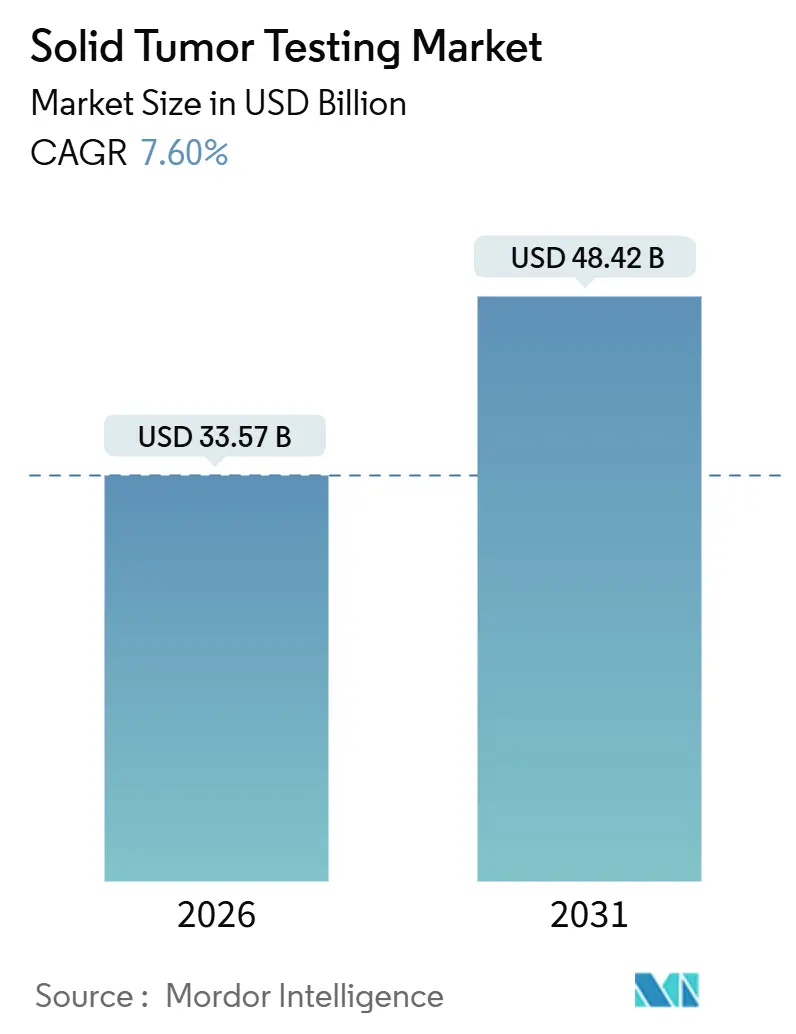

| Market Size (2026) | USD 33.57 Billion |

| Market Size (2031) | USD 48.42 Billion |

| Growth Rate (2026 - 2031) | 7.60% CAGR |

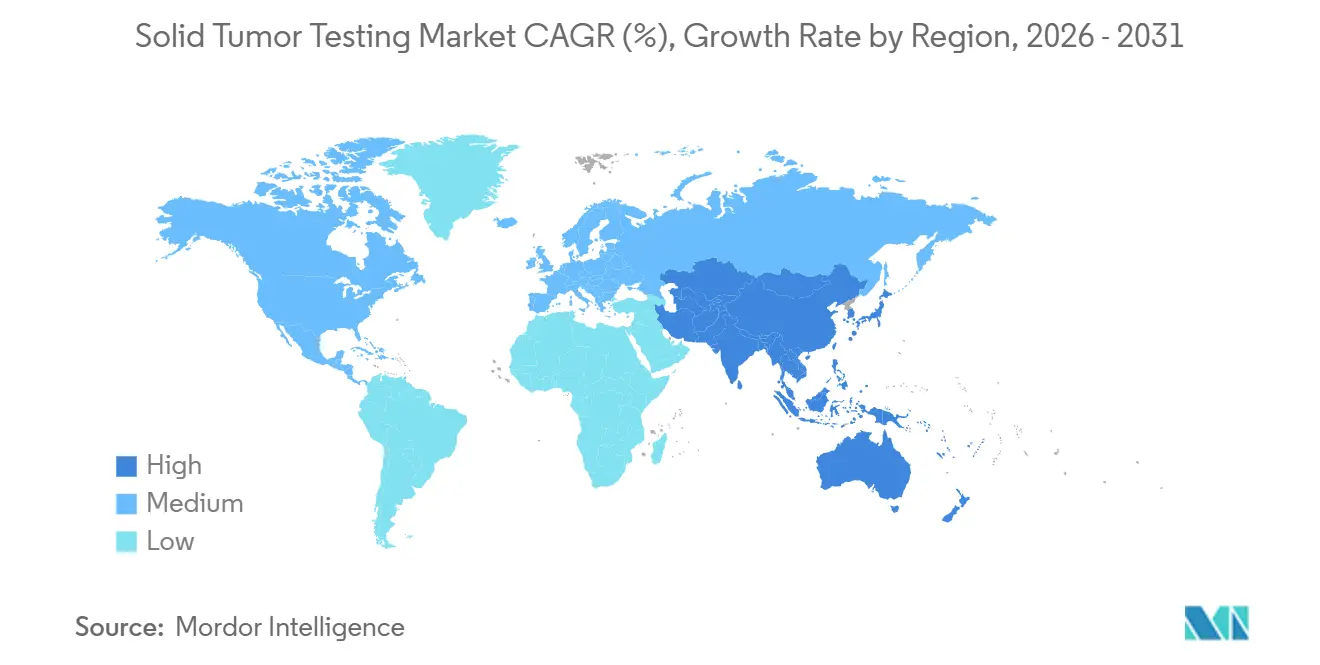

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solid Tumor Testing Market Analysis by Mordor Intelligence

The Solid Tumor Testing Market size is estimated at USD 33.57 billion in 2026, and is expected to reach USD 48.42 billion by 2031, at a CAGR of 7.60% during the forecast period (2026-2031).

Growth stems from the convergence of demographic aging, precision-oncology guidelines, and falling sequencing costs that embed molecular profiling into standard pathways for breast, lung, colorectal, and other malignancies. Liquid biopsy is gaining ground as a minimally invasive option for serial monitoring, while tissue testing retains a dominant position because of higher tumor-fraction yield and long-established reimbursement codes. Regulatory approvals of tumor-agnostic therapies, particularly in the United States and Europe, are further accelerating demand for broad panels that can detect rare fusions across histologies. Competitive pressure continues to rise as reference laboratories, hospitals, and IVD manufacturers pursue scale economies, data monetization, and AI-based interpretation to differentiate service offerings.

Key Report Takeaways

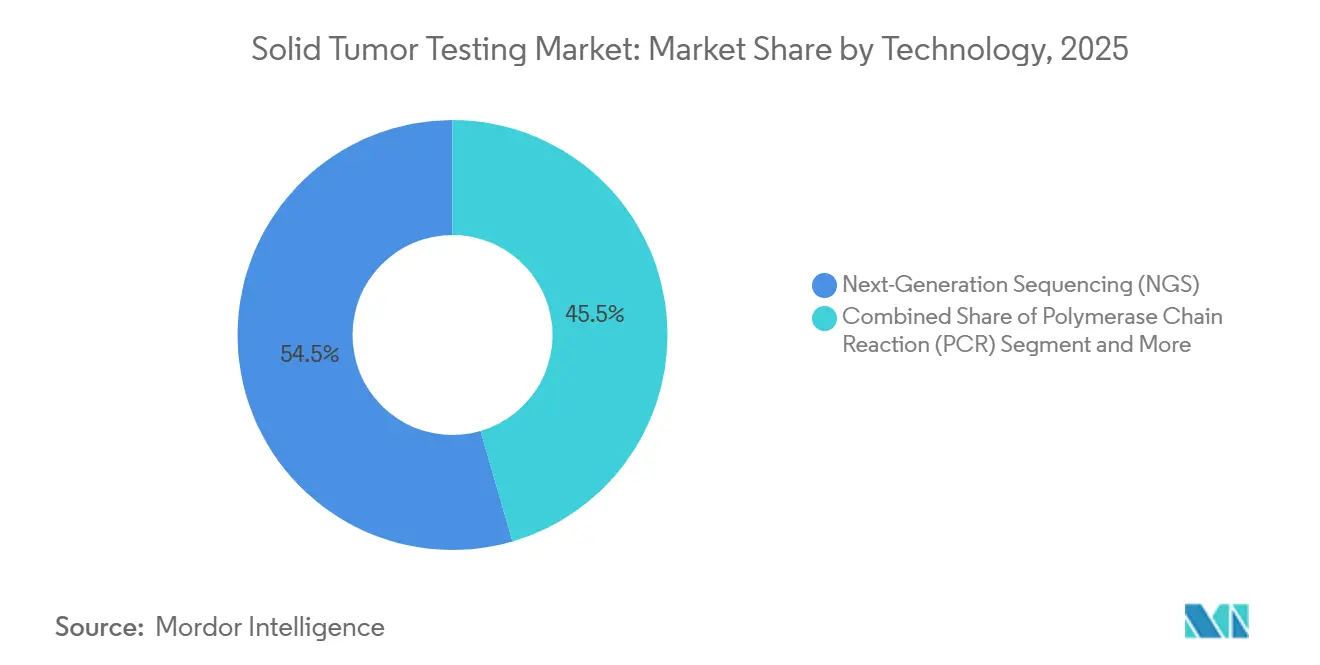

- By technology, next-generation sequencing held 54.55% of solid tumor testing market share in 2025, whereas fluorescence in-situ hybridization is forecast to grow at a 10.25% CAGR through 2031.

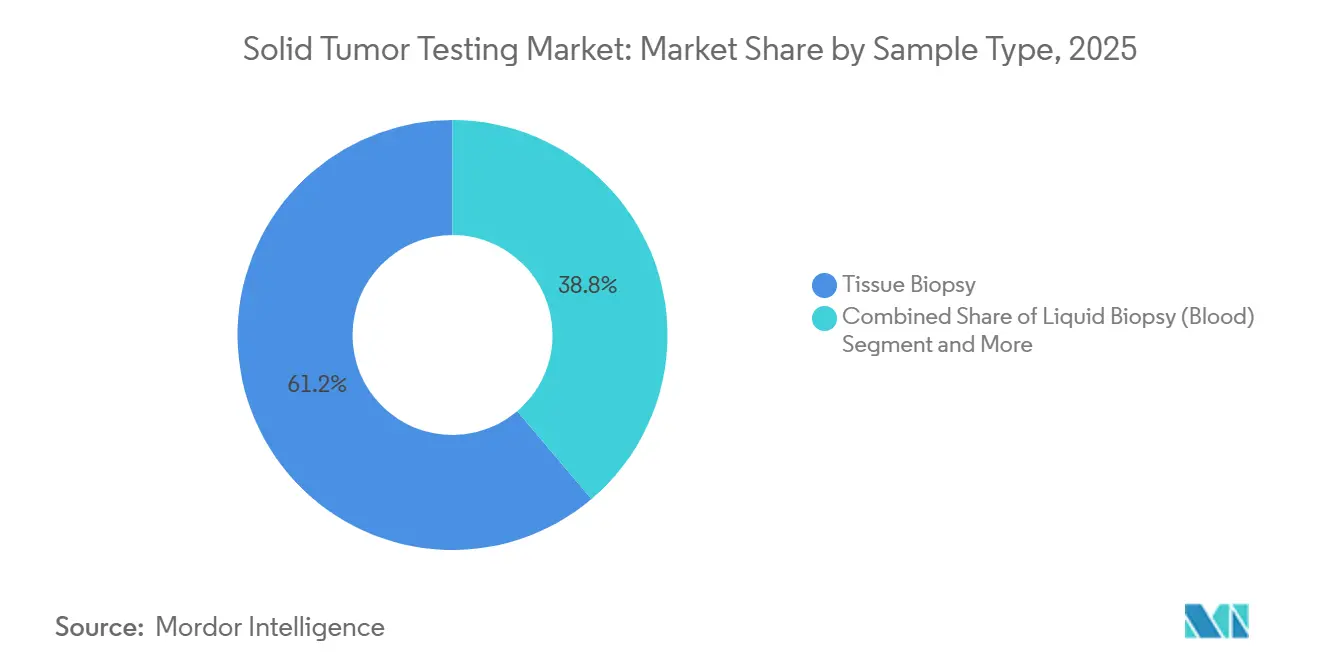

- By sample type, tissue accounted for a 61.23% share of the solid tumor testing market size in 2025, while liquid biopsy is advancing at a 15.55% CAGR to 2031.

- By geography, North America led with 42.25% revenue share in 2025; Asia-Pacific is projected to expand at a 12.21% CAGR through 2031.

- By cancer type, lung testing commanded a 10.85% CAGR outlook to 2031, whereas breast cancer contributed an 18.53% share in 2025.

- By end user, diagnostic and reference laboratories captured a 10.11% CAGR, outpacing hospitals and cancer centers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solid Tumor Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-driven incidence & precision-medicine adoption | +1.8% | Global, concentrated in North America, Europe, Japan | Long term (≥ 4 years) |

| Falling NGS cost curve | +1.5% | Global, accelerating in Asia-Pacific | Medium term (2-4 years) |

| Regulatory approvals of tumor-agnostic therapies | +1.2% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Hospital shift to in-house CGP IVD kits | +0.9% | North America, Western Europe | Medium term (2-4 years) |

| AI-assisted multi-omic variant interpretation | +0.8% | Global, early adoption in US academic centers | Long term (≥ 4 years) |

| Core-biopsy compatible manufacturing workflows | +0.6% | Global, benefits low-resource settings in MEA, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging-Driven Incidence & Precision-Medicine Adoption

Cancer incidence rises steeply with age, and populations in high-income countries are aging rapidly. Japan’s over-65 cohort reached 29% in 2024, while the United States is projected to hit 21% by 2030, sustaining test demand. Precision-medicine guidelines now mandate molecular profiling for most advanced solid tumors, embedding testing into routine care. The American Society of Clinical Oncology updated its lung-cancer guideline in 2024 to require reflex NGS or sequential assays for at least eight biomarkers before first-line therapy selection. Oncologists increasingly consider molecular reports essential, ensuring durable volume growth even when reimbursement is flat.

Falling NGS Cost Curve

Sequencing reagent prices have dropped by an order of magnitude in the past decade. Illumina’s NovaSeq X Plus targets a USD 600 genome by 2025, while BGI Genomics advertises sub-USD 100 costs at scale[1]Illumina Inc., “Investor Presentation Q2 2024,” illumina.com. A 2024 costing study demonstrated that per-sample expenses fall from USD 377 to USD 128 when throughput rises from 600 to 5,000 samples, incentivizing high-volume reference labs. Cost deflation widens laboratory margins, funding automation and AI interpretation that reinforce competitive barriers.

Regulatory Approvals of Tumor-Agnostic Therapies

The FDA cleared multiple tumor-agnostic drugs in 2024, including Bizengri for NRG1-fusion tumors and repotrectinib for NTRK-positive cancers. These approvals require assays capable of detecting rare fusions, amplifying demand for broad panels. Pharma sponsors are prioritizing pan-cancer trials, creating a feedback loop in which more approvals justify wider testing, and wider testing generates real-world evidence for further approvals.

Hospital Shift to In-House CGP IVD Kits

Academic medical centers and large health systems increasingly run comprehensive panels in-house to shorten turnaround and retain pathology revenue. FDA-cleared kits such as TruSight Oncology 500 enable hospitals to operate without developing lab-developed tests under CLIA. A 2024 U.S. survey showed that 38% of cancer centers already perform NGS internally, primarily to deliver results within ten days.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High comprehensive-panel cost & patchy reimbursement | -0.7% | Global, acute in emerging markets and US community oncology | Short term (≤ 2 years) |

| Shortage of trained molecular pathologists | -0.5% | Global, most severe in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| EU IVDR certification bottleneck | -0.4% | Europe, indirect impact on global product roadmaps | Medium term (2-4 years) |

| Low-shedding tumors limit liquid-biopsy sensitivity | -0.3% | Global, affects early-stage and certain histologies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Comprehensive-Panel Cost & Patchy Reimbursement

Panels priced between USD 3,000 and USD 5,000 strain oncology budgets outside academic centers. Medicare reimburses under NCD 90.2, but many commercial payers impose prior-authorization hurdles that delay adoption. Europe remains fragmented; Germany broadened NGS coverage in 2024, whereas France still mandates case-by-case approval via molecular tumor boards. This patchwork sustains demand for single-gene assays in community settings, slowing panel-first workflows.

Shortage of Trained Molecular Pathologists

Fewer than 200 new U.S. specialists graduate each year, well below projected needs[2]American Society for Clinical Pathology, “Molecular Pathology Workforce Study 2024,” ascp.org. India counts fewer than 50 certified molecular pathologists for a population of 1.4 billion, highlighting a global skills gap that lengthens turnaround times and raises labor costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: NGS Dominance Meets FISH Resurgence

Next-generation sequencing accounted for 54.55% of 2025 revenue, making it the largest component of the solid tumor testing market. NGS panels condense hundreds of genes into a single run, supporting targeted therapy selection, immunotherapy biomarkers, and tumor-agnostic indications. Fluorescence in-situ hybridization is projected to grow at a 10.25% CAGR through 2031 as guidelines continue to list FISH as the gold-standard confirmatory method for HER2 amplification and ALK rearrangement.

Automation is extending FISH’s lifespan; a 2025 study showed AI-assisted digital pathology reduced interpretation time by 40% and improved concordance to 96%. Should payers tighten authorization for broad panels, FISH and PCR could regain share by offering faster paths to coverage. Conversely, if comprehensive panels secure wider reimbursement, single-biomarker assays will recede to niche roles.

By Cancer Type: Lung Surges on Immunotherapy Tailoring

Lung cancer testing is expected to post a 10.85% CAGR, the fastest among tumor types, fueled by reflex profiling for EGFR, ALK, KRAS G12C, and PD-L1 before first-line therapy. Breast cancer maintained an 18.53% contribution to 2025 revenue through universal HER2 screening and emerging PIK3CA and ESR1 assays.

The pipeline of targeted drugs expands the solid tumor testing market by adding new biomarkers, while negative trials can slow uptake. Colorectal, prostate, and rare tumors such as cholangiocarcinoma all benefit from the expanding actionable-mutation list, supporting broader panel adoption.

By Sample Type: Liquid Biopsy’s MRD Catalyst

Tissue retained a 61.23% share of the solid tumor testing market size in 2025, benefiting from higher tumor content and clear coverage pathways. Liquid biopsy, however, is forecast to grow 15.55% annually as clinicians embrace serial ctDNA testing for minimal-residual-disease monitoring and resistance tracking.

Sensitivity remains histology-dependent, yet FDA approval of Guardant’s Shield for colorectal-cancer screening signals regulatory confidence in blood-based assays. Pre-analytical standardization will determine how quickly liquid biopsy displaces tissue outside low-shedding tumors.

By End User: Reference Labs Capture Scale Economies

Diagnostic and reference laboratories are projected to expand at 10.11% annually as they pool high volumes and amortize the cost of molecular pathologists. NeoGenomics and Guardant Health reported double-digit revenue growth in 2024 by emphasizing broad menus and rapid turnaround.

Hospitals and cancer centers hold 48.03% of 2025 revenue but exhibit divergent strategies; academic centers internalize testing, while many community hospitals outsource complex assays. Reimbursement incentives and IVDR compliance costs will shape future test-allocation models.

Geography Analysis

North America generated 42.25% of 2025 revenue, reflecting broad Medicare coverage and a mature ecosystem of reference laboratories and hospital molecular programs. The United States accounts for the bulk of regional activity, aided by per-test payment levels that exceed USD 3,000 under CPT 81455, whereas Canada and Mexico lag behind due to provincial funding variability and private-insurance dependence. Continued approvals of tumor-agnostic therapies should sustain volume growth, although commercial payers are tightening prior-authorization criteria that could temper expansion in community oncology.

Asia-Pacific posted the highest projected growth, a 12.21% CAGR, fueled by policy reforms and falling sequencing costs. China’s 2024 inclusion of NGS panels in provincial reimbursement catalogs has stimulated adoption beyond tier-1 cities, while Japan’s universal-coverage system supports genomic medicine for its rapidly aging population. India’s National Cancer Grid is scaling molecular hubs across 50 cities despite infrastructure gaps. Regional players like BGI and Macrogen leverage localized manufacturing to undercut imported assays, positioning the region for sustained uptake of liquid biopsy and AI-assisted interpretation.

Europe occupies an intermediate position. Germany broadened statutory coverage in 2024, and the U.K. expanded whole-genome sequencing through the NHS Genomic Medicine Service. Nonetheless, IVDR conformity bottlenecks slow new-test introductions, especially for smaller vendors, and reimbursement remains fragmented in southern Europe. In Latin America, Middle East, and Africa, testing volume is concentrated in private hospitals that serve affluent patients and expatriates, while public systems grapple with competing health priorities and budget constraints.

Competitive Landscape

Global competition is moderate and data-driven. Illumina capitalizes on a 20,000-unit instrument base that creates reagent lock-in, whereas Guardant Health and Foundation Medicine leverage FDA-cleared assays and pharma partnerships to dominate send-out volume. Tempus Labs’ USD 6.1 billion IPO in 2024 underscored investor appetite for AI-enhanced multi-omic platforms that transform raw sequence data into clinical insight. Reference laboratories such as Labcorp and Quest Diagnostics compete on test breadth and national logistics networks but face margin compression as academic centers internalize sequencing.

Patent portfolios are becoming key differentiators. A 2024 USPTO review found that Illumina, Guardant Health, and Thermo Fisher collectively hold more than 300 patents covering ctDNA detection and AI-based variant classification[3]United States Patent and Trademark Office, “Patent Database: Liquid Biopsy and Variant Classification,” uspto.gov. Regulatory compliance adds another barrier: CLIA, CAP, and IVDR certifications require robust quality-management systems that favor well-capitalized entities. Niche specialists including NeoGenomics and Caris Life Sciences focus on subsegments such as hematologic malignancies or high-complexity RNA fusion assays, exploiting gaps left by larger players.

Strategic moves illustrate vertical integration. Exact Sciences’ roll-up of Genomic Health and Paradigm aligns screening, treatment selection, and monitoring under one roof. Roche’s ownership of Foundation Medicine allows end-to-end control from tissue collection through data interpretation. M&A activity is expected to persist as vendors seek scale, proprietary data, and geographic expansion into Asia-Pacific and Latin America, where local reimbursement growth is outpacing established markets.

Solid Tumor Testing Industry Leaders

F. Hoffmann-La Roche Ltd

Illumina Inc.

Thermo Fisher Scientific Inc.

Guardant Health Inc.

QIAGEN N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NeoGenomics introduced PanTracer Tissue, a next-generation assay with optional HRD testing.

- May 2025: Guardant Health added a full suite of immunohistochemistry tests covering lung, breast, gastric, and ovarian cancers.

Global Solid Tumor Testing Market Report Scope

As per the scope of the report, solid tumor testing refers to a series of diagnostic procedures used to identify, characterize, and evaluate solid tumors, abnormal masses of tissue that arise from organs or tissues such as the breast, lung, prostate, or skin.

The solid tumor testing market is segmented by technology, cancer type, sample type, end user, and geography. By technology, the market includes next-generation sequencing (NGS), polymerase chain reaction (PCR), immunohistochemistry (IHC), fluorescence in-situ hybridization (FISH), and other technologies (microarray, ELISA, LC-MS). By cancer type, the segmentation covers breast, lung, colorectal, prostate, liver, and other solid tumors. By sample type, the market is divided into tissue biopsy, liquid biopsy (blood), and other body fluids. By end user, the segmentation includes hospitals & cancer centers, diagnostic & reference laboratories, and other end users. By geography, the market is categorized into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Next-Generation Sequencing (NGS) |

| Polymerase Chain Reaction (PCR) |

| Immunohistochemistry (IHC) |

| Fluorescence In-Situ Hybridization (FISH) |

| Other Technologies (Microarray, ELISA, LC-MS) |

| Breast |

| Lung |

| Colorectal |

| Prostate |

| Liver |

| Other Solid Tumors |

| Tissue Biopsy |

| Liquid Biopsy (Blood) |

| Other Body Fluids |

| Hospitals & Cancer Centers |

| Diagnostic & Reference Laboratories |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Next-Generation Sequencing (NGS) | |

| Polymerase Chain Reaction (PCR) | ||

| Immunohistochemistry (IHC) | ||

| Fluorescence In-Situ Hybridization (FISH) | ||

| Other Technologies (Microarray, ELISA, LC-MS) | ||

| By Cancer Type | Breast | |

| Lung | ||

| Colorectal | ||

| Prostate | ||

| Liver | ||

| Other Solid Tumors | ||

| By Sample Type | Tissue Biopsy | |

| Liquid Biopsy (Blood) | ||

| Other Body Fluids | ||

| By End User | Hospitals & Cancer Centers | |

| Diagnostic & Reference Laboratories | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the solid tumor testing market today?

The solid tumor testing market size stands at USD 33.57 billion in 2026 and is forecast to reach USD 48.42 billion by 2031.

Which technology leads current adoption?

Next-generation sequencing holds 54.55% of 2025 revenue due to its ability to interrogate hundreds of genes in one run.

Why is liquid biopsy growing faster than tissue testing?

Liquid biopsy supports serial minimal-residual-disease monitoring and is projected to grow 15.55% annually through 2031.

Which region is expected to expand most rapidly?

Asia-Pacific shows the highest projected CAGR at 12.21% owing to policy reforms and falling sequencing costs.

What are the main barriers to broader panel adoption?

High test prices, variable reimbursement, and a shortage of molecular pathologists slow uptake outside major centers.

Page last updated on: