Metering Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.79 Billion |

| Market Size (2031) | USD 9.44 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

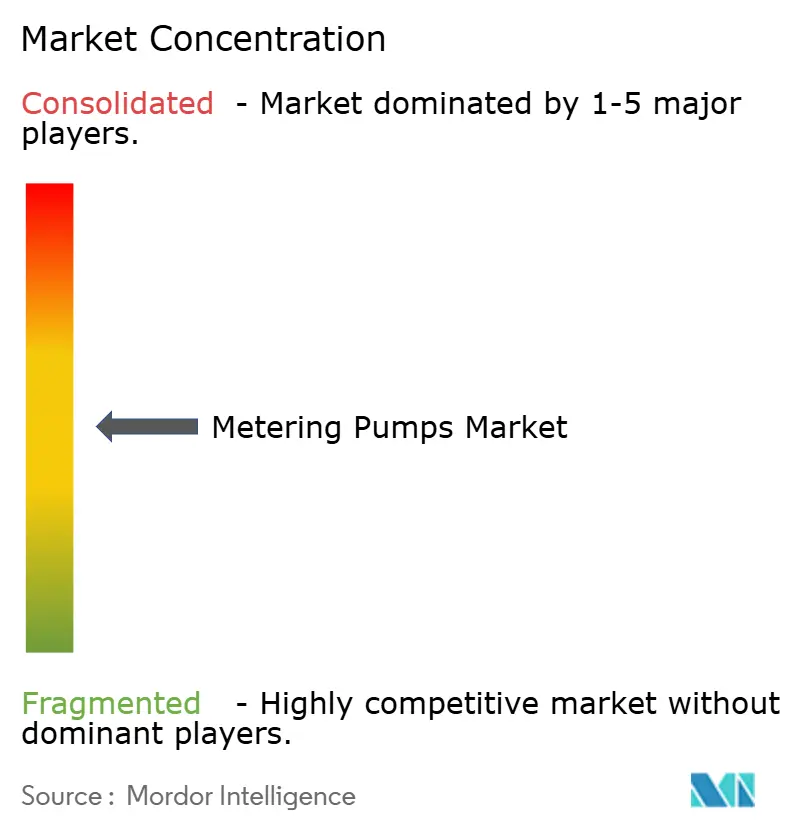

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metering Pumps Market Analysis by Mordor Intelligence

The metering pumps market size was valued at USD 7.5 billion in 2025 and estimated to grow from USD 7.79 billion in 2026 to reach USD 9.44 billion by 2031, at a CAGR of 3.92% during the forecast period (2026-2031). Steady growth reflects the technology’s entrenched role in precision fluid handling for water, chemicals, and high-purity manufacturing. Water treatment remains the single largest demand center, accounting for 41% of 2024 revenue, backed by tightening global discharge limits. Pharmaceutical plants are the fastest-expanding user group at a 6.8% CAGR as continuous-flow production lines seek ultra-accurate dosing. Asia-Pacific leads the metering pumps market with a 40% share in 2024 because China and India continue to invest in wastewater upgrades and stricter effluent controls. Competitive dynamics are shifting toward IIoT-enabled smart dosing systems, a trend that is accelerating sales of solenoid-driven units growing 6.2% per year. Diaphragm technology commands 64% of 2024 sales, yet plunger designs are climbing 7.5% annually to meet higher-pressure chemical injection needs. Mid-pressure (51-100 bar) applications are expanding 5.4% per year as complex industrial chemistries become the norm.

Key Report Takeaways

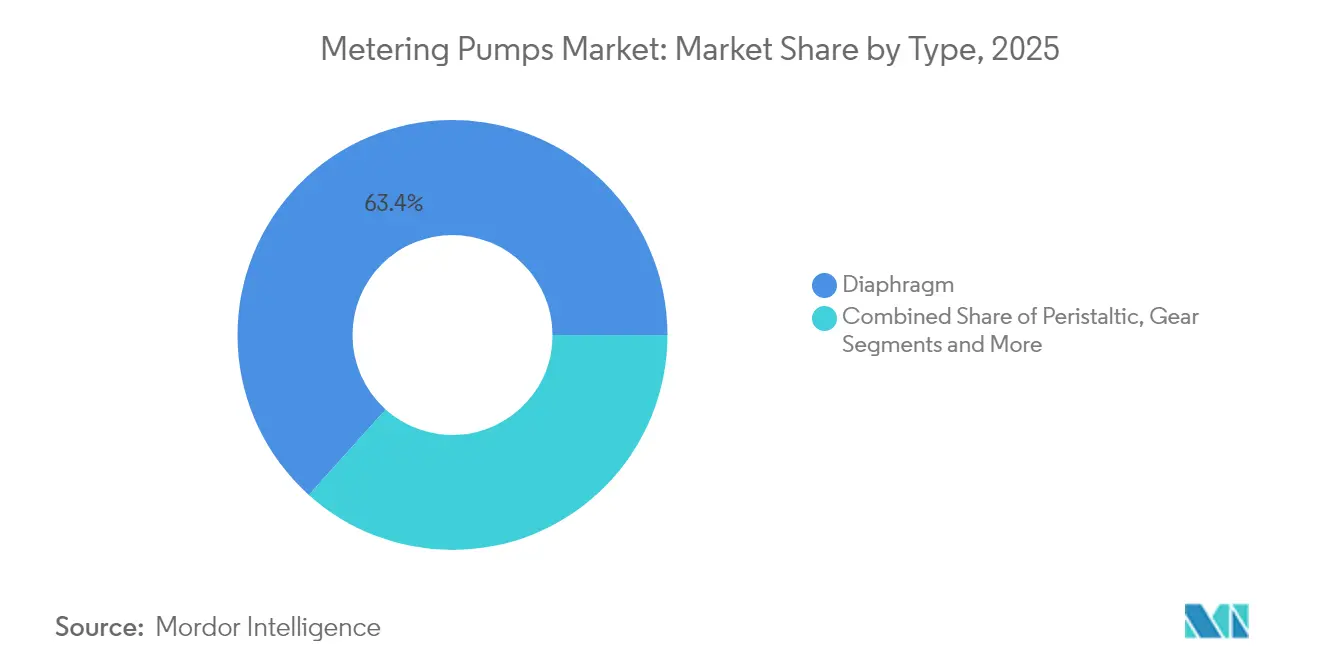

- By pump type, diaphragm units held 63.35% of the metering pumps market share in 2025, while plunger/piston designs are projected to post the fastest 7.02% CAGR through 2031.

- By drive mechanism, motor-driven pumps led with 54.45% revenue share in 2025; solenoid-driven variants are on track for a 5.88% CAGR over the same period.

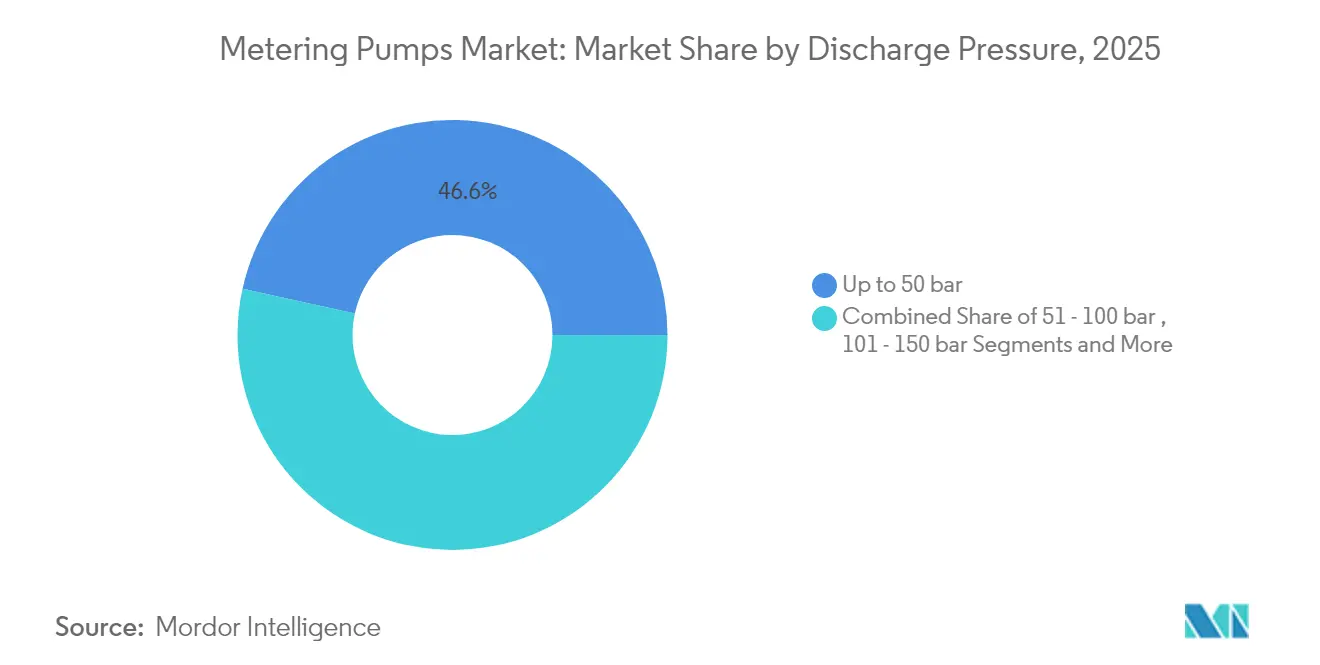

- By discharge pressure, the up-to-50 bar range accounted for 46.55% of the metering pumps market size in 2025; the 51-100 bar tier is expected to record the highest 5.18% CAGR between 2026 and 2031.

- By end-user, water treatment secured 40.62% of 2025 revenue, whereas pharmaceuticals will rise the fastest at a 6.42% CAGR through 2031.

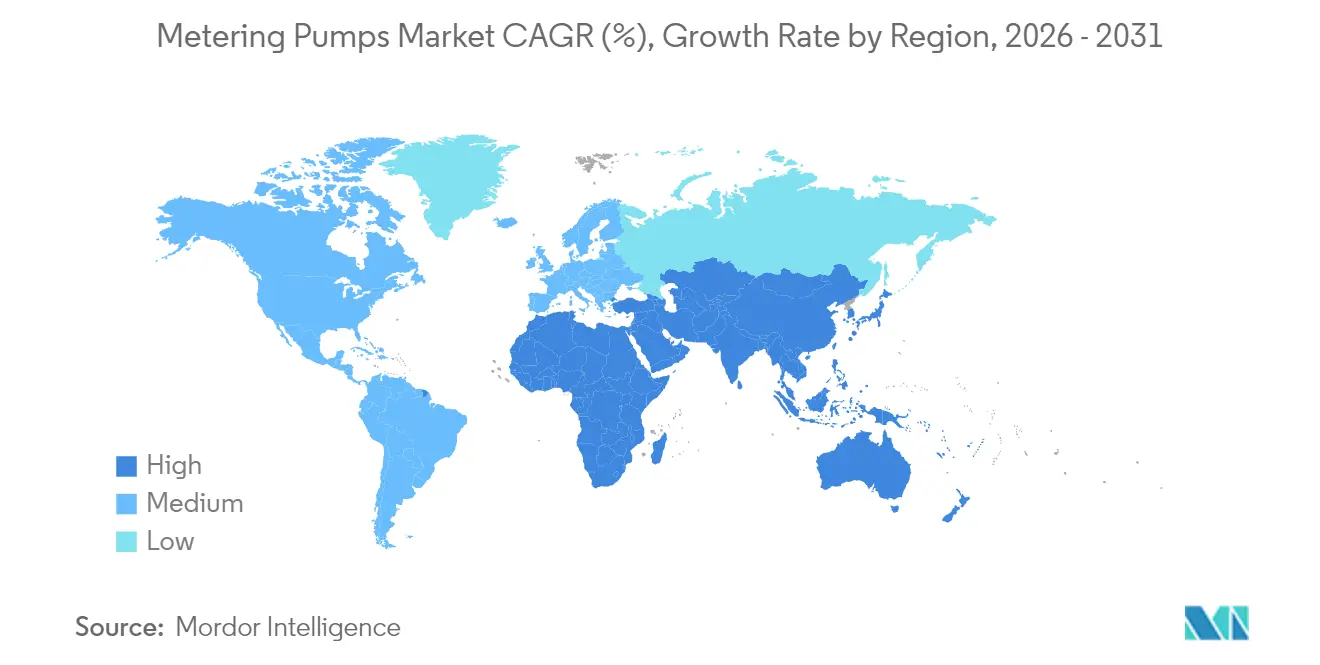

- By geography, Asia-Pacific dominated with 39.55% of 2025 revenue, while Latin America is set to expand at a 5.27% CAGR to 2031.

- Grundfos, IDEX, Dover, SPX Flow, and LEWA collectively controlled roughly 44.70% of global revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metering Pumps Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Strict Industrial Waste-water Norms Accelerating Chemical Dosing in Asia | 1.5% | Asia-Pacific, with spillover to Middle East & Africa | Medium term (2-4 years) |

| Rapid Digitalization of Water Utilities Demanding Smart Dosing Accuracy | 1.2% | North America, Europe, Advanced Asia-Pacific economies | Medium term (2-4 years) |

| Fertigation Boom in High-Value Horticulture across the Middle East | 0.8% | Middle East, North Africa, Mediterranean Europe | Short term (≤ 2 years) |

| Increasing Offshore Enhanced-Oil-Recovery (EOR) Chemical Injection Needs | 0.6% | North America, Latin America, Middle East | Long term (≥ 4 years) |

| Growing Use of High-Purity API Skids in Continuous-Flow Pharma Plants | 0.6% | North America, Europe, Advanced Asia-Pacific economies | Medium term (2-4 years) |

| Extensive Demand from Chemical Plants | 0.6% | Global, with concentration in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Industrial Waste-water Norms Accelerating Chemical Dosing in Asia

Sweeping 2024 amendments to China’s Water Pollution Prevention and Control Law cut allowable effluent loads by 40%, forcing roughly 65,000 factories to add multiple chemical dosing points and digital data logging. Upgrades across electroplating, textile, and pharma corridors now account for 35% of all new installs in Asia, with IIoT-ready pumps preferred to satisfy record-keeping mandates mee.gov.cn. These standards are expected to ripple through Southeast Asia and India over the next three years, underpinning consistent demand growth within the metering pumps market.

Rapid Digitalization of Water Utilities Demanding Smart Dosing Accuracy

Utilities integrating SCADA and IoT platforms have uncovered 15-22% chemical savings when pumps adjust doses in real time. The shift is shortening replacement cycles from 12 years to near 8 years and raising average selling prices by one-quarter. Regions facing water scarcity, such as the US Southwest and parts of Spain, are early adopters as they balance quality assurance with chemical cost control. Service-based revenue models around predictive maintenance are emerging, enlarging the opportunity set for vendors.[1]US Environmental Protection Agency, “Chemical Optimization through Smart Dosing,” epa.gov

Fertigation Boom in High-Value Horticulture across the Middle East

Controlled-environment farms in UAE and Saudi Arabia rely on multi-channel dosing stations that fine-tune nutrients by crop stage. Yield gains of 25-40% and fertilizer use cuts of 30% justify higher outlays, stimulating a niche yet vibrant demand pocket for corrosion-resistant pumps able to withstand aggressive fertilizer concentrates.

Increasing Offshore Enhanced-Oil-Recovery Chemical Injection Needs

Maturing offshore fields now deploy high-pressure polymer and surfactant injection systems exceeding 150 bar, valuing compact API 675-compliant packages with redundant designs. The premium nature of these orders, often priced 3-4 times higher than standard models, sustains a lucrative sub-segment within the broader metering pumps market despite lower volumes.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Requirement of Frequent Maintenance | -0.5% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Growing Customization Demands (Fluid-Property-Driven Design Tweaks) | -0.3% | Global, with concentration in specialty chemical and pharmaceutical sectors | Short term (≤ 2 years) |

| Cavitation Risk in High-Viscosity Peristaltic Lines Limiting Adoption | -0.4% | Global, with particular impact in polymer processing and food industries | Medium term (2-4 years) |

| Availability of Low-cost Chinese Knock-offs Eroding Margins Globally | -0.6% | Global, with highest impact in price-sensitive emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Requirement of Frequent Maintenance

Mechanical diaphragm pumps often need service after 4,000-6,000 hours, interrupting continuous processes that can lose USD 5,000-15,000 per hour during downtime. Emerging markets suffer most because skilled technicians are scarce, prompting some operators to consider less precise but lower-maintenance alternatives.[2]Dow Chemical Company, “Continuous Process Downtime Cost Analysis,” dow.com

Growing Customization Demands (Fluid-Property-Driven Design Tweaks)

Custom builds now exceed 40% of OEM order books, driving up inventories and extending lead times. Smaller suppliers lacking broad engineering benches struggle to meet prescriptions for high-viscosity polymers or shear-sensitive biologics, dampening overall throughput within the metering pumps market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Diaphragm Dominates While Plunger Accelerates

Diaphragm pumps controlled 63.35% of global revenue in 2025. Their leak-free architecture fits corrosive water-treatment chemistries, cementing leadership across compliance-driven markets. Plunger/piston models are expanding at 7.02% annually as upstream operators push injection pressures above 100 bar. This differential signals a migration toward high-pressure niches where flow stability under extreme conditions outweighs higher lifecycle costs. Gear, rotary lobe, and peristaltic designs address narrower needs such as pulse-free polymer blending or hygienic pharma fills.

Recent elastomer advances have extended peristaltic tube life by 40%, elevating their appeal in sterile dosing lines. Gear and lobe pumps maintain steady uptake in polymer compounding where continuous, shear-controlled feed rates matter. Collectively, these trends support a diverse technology mix inside the metering pumps market.

By Drive Mechanism: Motor-Driven Reliability Meets Solenoid Innovation

Motor-driven units captured 54.45% of 2025 sales thanks to rugged construction and simple integration with legacy control loops. Solenoid-driven pumps, though smaller in absolute value, are climbing 5.88% per year on the back of energy efficiency and digital-native design. New magnetic circuit geometries raise their flow and pressure ceiling by almost one-third while trimming power draw roughly 30%. Pneumatic and hydraulic drives retain roles in hazardous or power-poor sites, yet their share is stable rather than rising.

Solenoid evolution dovetails with the surge in smart water and chemical plants, positioning this architecture as a growth engine for the metering pumps market through 2031

By Discharge Pressure: Mid-Range Pressure Applications Accelerate

Applications below 50 bar represented 46.55% of 2025 revenue and remain the volume backbone for municipal water and general chemical processing. The 51-100 bar tier is advancing at 5.18% CAGR as intensified industrial chemistries demand tighter control under higher heads. Above 100 bar remains a premium enclave in oil and gas and high-pressure synthesis. Ceramic plunger inserts and duplex alloys now extend service life at 150 bar plus, safeguarding accuracy even with abrasive or acidic reagents.

By End-User Industry: Water Treatment Leads While Pharmaceuticals Surge

Water treatment held 40.62% revenue in 2025, driven by new disinfection and nutrient-removal mandates. Pharmaceuticals will post the swiftest 6.42% CAGR on rising continuous-manufacturing capacity and GMP demands for closed, cleanable dosing skids. Oil and gas maintains cyclical yet sizable orders for corrosion inhibitors and hydrate-control chemicals, especially in offshore installations. Food and beverage processors are specifying sanitary diaphragm pumps for flavor, acid, and enzyme dosing, expanding the addressable base. Agriculture is an emerging niche, aligning with Middle-Eastern fertigation schemes that improve water efficiency per hectare.

Geography Analysis

Asia-Pacific dominated the metering pumps market with 39.55% of 2025 revenue. China’s latest five-year plan earmarks widespread industrial effluent upgrades, while India’s Jal Jeevan Mission drives rural water quality investments. High-purity pharma growth in Singapore and South Korea stimulates demand for skid-mounted, digitally certified dosing modules. Local manufacturers undercut imported models in commodity ranges, yet Western brands keep premium share in high-pressure or exotic-material builds.

South America is the fastest-growing geography at a 5.27% CAGR to 2031. Brazil’s new sanitation law triggers chlorination and pH control rollouts, and other countries in South America export manufacturing sector increases solvent recycling and wastewater neutralization installations. Vendors emphasize voltage-tolerant drives and simplified service kits to suit local infrastructure.

North America and Europe are mature but innovation-intensive. Utility operators here spearhead integration of pumps with cloud-hosted dashboards, favoring solutions that broadcast status over MQTT or OPC UA. The US EPA’s lead and copper rule revisions and Europe’s tightening of PFAS discharge limits both raise dosing accuracy thresholds. Meanwhile, Gulf producers and arid African nations channel spending toward desalination and reuse, preserving a steady pipeline of orders for corrosion-resistant PVDF and super-duplex pumps.

Competitive Landscape

The metering pumps market is moderately concentrated. The five largest suppliers—Grundfos, IDEX, Dover (PSG), SPX Flow, and LEWA—command about 45% of revenue, protected by strong brands, application know-how, and extensive service coverage. Asian entrants gain ground in standardized ≤50 bar products through cost advantages, but high-pressure and pharmaceutical niches remain dominated by incumbents. The competitive contest is now rooted in digital fluency. Grundfos iSOLUTIONS and ProMinent DULCONNEX exemplify the pivot from hardware sales to holistic chemical-management platforms featuring predictive maintenance and dosing optimization.

Mid-sized specialists exploit white-space opportunities. Blue-White Industries’ multi-diaphragm innovation mitigates vapor lock in sodium hypochlorite dosing, capturing share among US utilities. Niche firms focused on ceramic plungers or expendable pump cartridges also outflank larger rivals in specialized chemistries. Mergers, typified by IDEX’s 2025 purchase of Mott Corporation, reflect a race to assemble broader fluid-handling portfolios that stretch from dosing pumps to filtration and sensing.

Metering Pumps Industry Leaders

Grundfos Holding A/S

IDEX Corp. (Milton Roy, Pulsafeeder)

PSG – Dover Corp. (Neptune, Wilden)

SPX Flow, Inc.

ProMinent GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nordson EFD received the 2024 Edge Award for its PICO Nexμs jetting system, which integrates with Industry 4.0 technologies through Industrial Ethernet protocols. This innovation represents a significant advancement in precision fluid dispensing, allowing users to control and monitor dispensing functions remotely while improving productivity and process control.

- March 2025: ProMinent showcased its latest metering pump innovations at ACHEMA 2024, including the Sigma/X product range featuring robust pumps with a patented multi-layer safety diaphragm and the gamma/X range with digitally controlled solenoid drives. These products highlight the industry trend toward enhanced safety features and digital integration capabilities.

- January 2025: IDEX Corporation completed the acquisition of Mott Corporation, a manufacturer of precision filtration and flow control products, strengthening its position in high-purity fluid handling applications. The USD 295 million transaction expands IDEX's capabilities in pharmaceutical and biopharmaceutical markets, complementing its existing metering pump portfolio.

- November 2024: ProMinent announced that its metering pumps have reached a global installation base of 1.6 million units, highlighting the company's market penetration and product reliability. The announcement emphasized the integration of these pumps with the DULCONNEX IIoT platform for enhanced monitoring and control capabilities.

Global Metering Pumps Market Report Scope

Metering pumps and dosing pumps are designed to dispense specific amounts of fluid and measure flow control. They use expanding and contracting chambers to move the liquids. They have a high accuracy over time and can pump many liquids, including corrosives, acids, bases, slurries, and viscous liquids.

The Global Metering Pumps Market is Segmented by Type (Diaphragm, Piston/Plunger), End-User (Oil & Gas, Water Treatment, Chemical Processing, Pharmaceuticals, Food & Beverage), and Geography.

| Diaphragm |

| Piston / Plunger |

| Peristaltic |

| Gear |

| Rotary Lobe |

| Motor-Driven |

| Solenoid-Driven |

| Hydraulic-Driven |

| Pneumatic-Driven |

| Up to 50 bar |

| 51 - 100 bar |

| 101 - 150 bar |

| Above 150 bar |

| Metallic (Stainless-steel, Alloy-20, Duplex) |

| Non-Metallic (PVC, PVDF, PP) |

| Water Treatment |

| Oil and Gas |

| Chemical Processing |

| Pharmaceuticals |

| Food and Beverage |

| Pulp and Paper |

| Agriculture and Fertigation |

| Mining and Minerals |

| Textiles |

| Power Generation and Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Diaphragm | |

| Piston / Plunger | ||

| Peristaltic | ||

| Gear | ||

| Rotary Lobe | ||

| By Drive Mechanism | Motor-Driven | |

| Solenoid-Driven | ||

| Hydraulic-Driven | ||

| Pneumatic-Driven | ||

| By Discharge Pressure | Up to 50 bar | |

| 51 - 100 bar | ||

| 101 - 150 bar | ||

| Above 150 bar | ||

| By Pump Material | Metallic (Stainless-steel, Alloy-20, Duplex) | |

| Non-Metallic (PVC, PVDF, PP) | ||

| By End-User Industry | Water Treatment | |

| Oil and Gas | ||

| Chemical Processing | ||

| Pharmaceuticals | ||

| Food and Beverage | ||

| Pulp and Paper | ||

| Agriculture and Fertigation | ||

| Mining and Minerals | ||

| Textiles | ||

| Power Generation and Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the metering pumps market?

The metering pumps market stands at USD 7.79 billion in 2026 and is expected to reach USD 9.44 billion by 2031.

Which end-user industry generates the most demand?

Water treatment leads, representing 40.62% of 2025 revenue due to stricter global water quality regulations.

Which region is growing the fastest?

Latin America is projected to post the highest 5.27% CAGR between 2026 and 2031, driven by water infrastructure upgrades in Brazil and Mexico.

What technology segment is expanding most quickly?

Plunger/piston pumps are forecast to grow 7.02% per year as high-pressure chemical injection applications increase.

How are smart features influencing procurement?

Utilities adopting IoT platforms prefer digitally enabled pumps that can interface with SCADA, shortening replacement cycles and raising average selling prices.

Who are the leading players in the market?

Grundfos, IDEX, Dover (PSG), SPX Flow, and LEWA account for about 44.70% of global revenue, reflecting moderate concentration.

Page last updated on: