Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

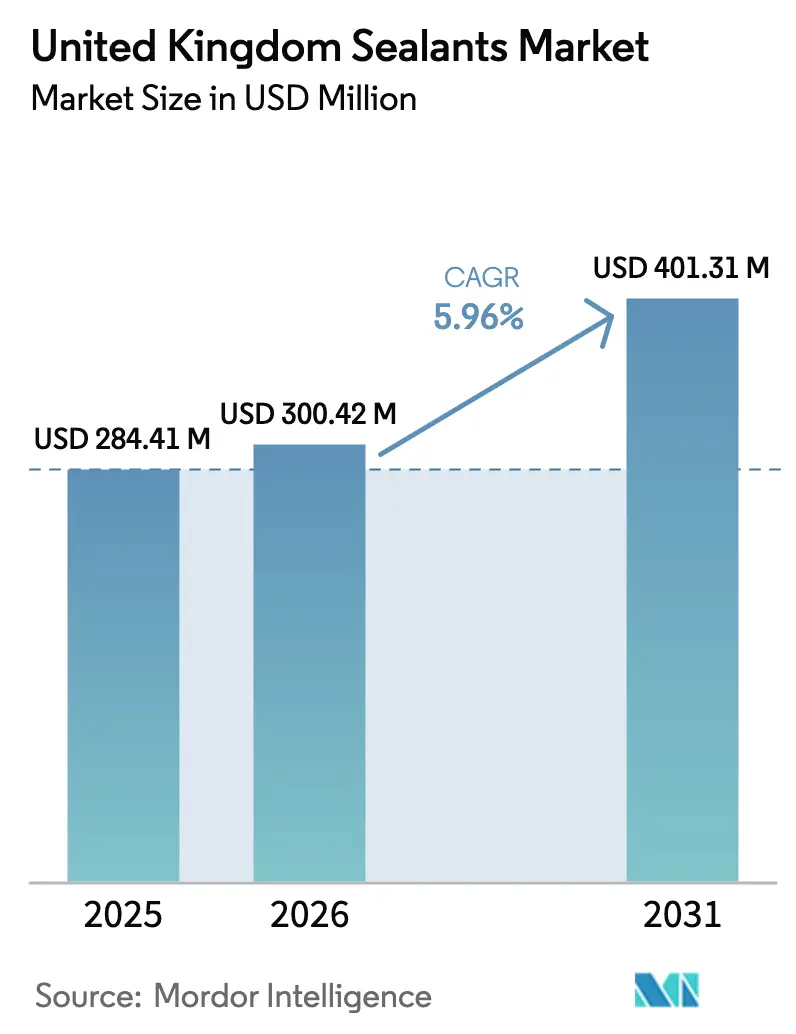

| Base Year Market Size (2025) | USD 284.41 Million |

| Market Size (2026) | USD 300.42 Million |

| Market Size (2031) | USD 401.31 Million |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Sealants Market Analysis by Mordor Intelligence

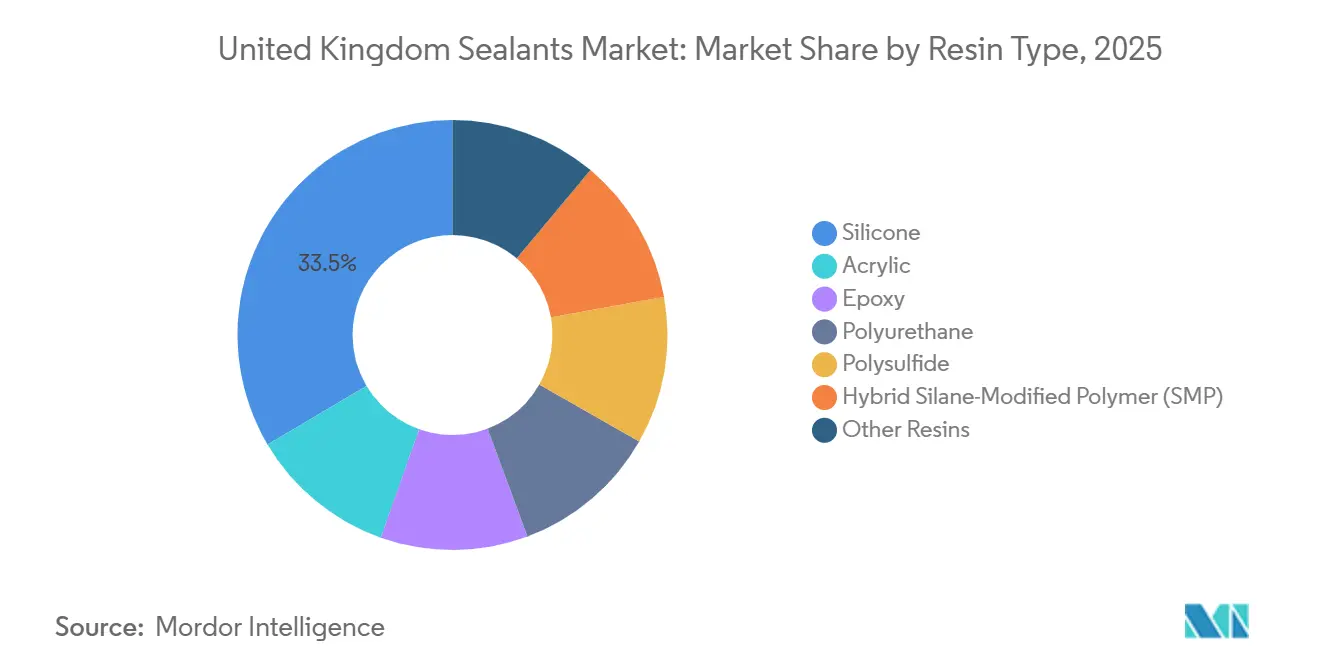

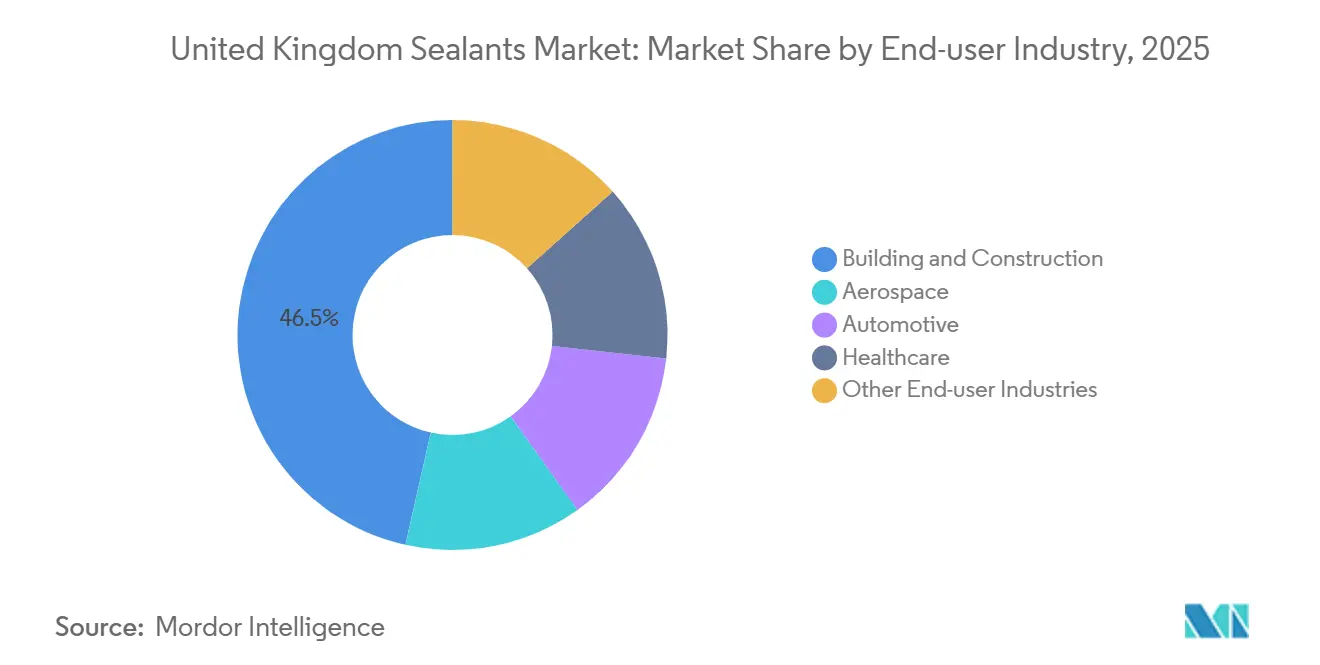

The United Kingdom Sealants Market size is projected to expand from USD 284.41 million in 2025 and USD 300.42 million in 2026 to USD 401.31 million by 2031, registering a CAGR of 5.96% between 2026 and 2031. The value trajectory reflects regulatory pressure that is steering specifiers toward premium, compliance-heavy chemistries rather than pure volume recovery. Infrastructure stimulus, Building Safety Act mandates, and tightening VOC caps are together lifting average selling prices while redistributing demand toward silicone and hybrid silane-modified polymer (SMP) grades. Silicone held 33.50% share in 2025 on the strength of healthcare and fire-rated uses, where EN 15651 certification restricts substitution. Hybrid SMP grades are advancing fastest as contractors favor one-component, isocyanate-free systems to satisfy SI 2012/1715 VOC limits. Building and construction contributed 46.50% of the 2025 volume, yet its growth is tilting toward civil works because residential completions dropped to 37,350 units in Q3 2025, the softest quarterly total since 2014.

Key Report Takeaways

- By resin type, silicone commanded 33.50% of the United Kingdom Sealants market share in 2025, while hybrid Silane-Modified Polymer (SMP) is forecast to expand at a 7.12% CAGR through 2031.

- By end-user industry, building and construction held 46.50% revenue share in 2025; the healthcare industry is projected to grow at 6.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for fire-resistant sealants in UK high-rise refurbishments | +1.80% | National, concentrated in London, Manchester, Birmingham high-rise clusters | Medium term (2-4 years) |

| Stricter VOC regulations pushing shift to hybrid silane-terminated polymers | +1.50% | National, with early adoption in public-sector projects and NHS estates | Long term (≥ 4 years) |

| Post-Brexit infrastructure stimulus accelerating construction sealant consumption | +1.90% | National, with infrastructure gains in Midlands, North West, and HS2 corridor | Short term (≤ 2 years) |

| Rising electric-vehicle battery-pack sealing needs | +0.70% | National, concentrated in automotive manufacturing clusters (West Midlands, North East, North West) | Medium term (2-4 years) |

| NHS estate maintenance backlog driving healthcare-facility refurbishment | +1.20% | National, concentrated in NHS trusts with critical-risk estates (London, North West, Yorkshire) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Fire-Resistant Sealants in UK High-Rise Refurbishments

The Building Safety Act is transforming fire-rated sealants from optional upgrades to compulsory products across roughly 12,500 high-rise dwellings in England[1]UK Government, “Building Safety Act 2022,” gov.uk. Intumescent acrylics and silicones must now achieve EN 13501-1 classification and prove compatibility with cavity-barrier systems, shifting procurement toward brands that can present third-party test evidence. Post-Grenfell inquiries traced smoke spread to joint failures, raising client scrutiny and lengthening approval cycles for unproven chemistries. Infrastructure upgrades in rail hubs and airports also require dual fire and acoustic ratings, which narrows the supplier pool and supports premium pricing. Smaller formulators lacking EN-certified lines are ceding share to multinational suppliers that can finance continuous testing, while demand remains concentrated in London and Manchester, where labor and logistics costs already elevate project budgets.

Stricter VOC Regulations Pushing Shift to Hybrid Silane-Terminated Polymers

SI 2012/1715 caps VOC content in construction sealants at 5-10 g/L, and intensified site inspections since 2024 have made compliance visible to contractors. Hybrid SMP grades meet the limit with negligible emissions, cure through ambient moisture, and avoid isocyanate labeling, which makes them the default choice in many framework contracts. Europe holds 44% of global SMP capacity, and the United Kingdom is the region’s fastest adopter because public-sector buyers mandate Environmental Product Declarations in tender documents. Suppliers such as Wacker Chemie and KCC Corporation have expanded UK technical teams to train applicators on moisture-sensitive handling. The transition raises costs by 15-25% per liter compared with solvent-borne polyurethane but positions contractors for forthcoming lifecycle-carbon rules that could expedite the exit of legacy solvent systems.

Post-Brexit Infrastructure Stimulus Accelerating Construction Sealant Consumption

Government allocations across transport, energy, and water are forecast to lift the United Kingdom Sealants market demand as civil projects specify long-life joints resistant to cyclic movement and chemical exposure. HS2’s Colne Valley Viaduct employed polyurethane and polysulfide grades for expansion joints and deck waterproofing, whereas Dover’s Western Docks Revival relied on immersion-rated polysulfide for cargo handling areas. Infrastructure output is projected to grow 3.9-4.4% in 2026, outpacing the 1-2% trend in residential completions, which is steering distributor inventories toward bulk packaging and technical-grade formulations. Long project timelines also lock in supply contracts, limiting smaller firms from being able to post performance bonds or offer multi-year warranties.

NHS Estate Maintenance Backlog Driving Healthcare-Facility Refurbishment

The NHS estate carries a GBP 15.9 billion (USD 20.97 billion) maintenance backlog, with GBP 3.5 billion (USD 4.62 billion) deemed high-risk where joint integrity affects infection control. HTM 03-01 ventilation rules require sealants to emit fewer than 0.5 mg/m³ VOCs and withstand hospital-grade disinfectants, criteria that favor silicone and low-modulus polyurethane. Procurement is protracted because frameworks demand UKAS-accredited data, yet continuity clauses enable incumbents to retain supply during review periods. Aging urban hospitals in London, the North West, and Yorkshire dominate refurbishment activity, and listed facades force bespoke sealing solutions that smaller suppliers sometimes develop in partnership with facilities-management contractors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in silicon-metal and MDI raw-material prices | -1.40% | National, with exposure to global feedstock markets (China silicon, European MDI) | Short term (≤ 2 years) |

| Skilled applicator shortage causing project delays | -1.10% | National, acute in London, South East, and major infrastructure corridors | Medium term (2-4 years) |

| Competition from prefabricated gasket solutions | -0.60% | National, concentrated in automotive OEM assembly and industrial equipment manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Silicon-Metal and MDI Raw-Material Prices

Silicon metal declined 14.98% year-on-year to March 2026 on Chinese oversupply, while European MDI rose 7.9% in February 2026, and aniline rose 18% in Q4 2024[2]BASF SE, “European Isocyanate Update,” basf.com. Polyurethane producers, therefore, face margin compression because residential contractors resist full pass-through price increases. Divergent raw-material trends are shifting share toward silicone in premium applications, while polyurethane suppliers are experimenting with TDI blends that raise occupational-exposure risks. Freight disruptions through the Red Sea add 10-14 days to lead times, compelling distributors to carry higher inventories that tie up working capital.

Skilled Applicator Shortage Causing Project Delays

The construction workforce shrank 10.8% since the pandemic, leaving a gap of roughly 266,000 workers by 2026, and sealant application is among the hardest trades to staff. EU labor in London construction fell from 42% in 2018 to 8% in 2021, while visa thresholds deter new entrants. Complex jobs such as fire-rated cavity barriers require six-month certification, yet training enrollments are down 40% since 2019. Contractors are switching from two-component systems to easier SMP products where specifications permit, but legacy requirements and engineering conservatism limit widespread change. Wage premiums of 25-30% above Midlands rates now prevail in London, and some firms fly crews from Scotland to meet deadlines, raising mobilization costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Dominance and Accelerating Hybrid Polymer Uptake

Silicone grades accounted for 33.50% of 2025 demand, anchored by EN 15651-certified applications in healthcare and fire-rated façades. Hybrid Silane-Modified Polymer (SMP) products are forecast to grow at a CAGR of 7.12% annually during the forecast period (2026-2031), the fastest among all resins. That rise aligns with contractor preference for one-component, label-free systems that comply with tightening VOC caps. Polyurethane retains relevance in EV battery packs and industrial flooring because of its chemical resistance and adhesion to dissimilar substrates. Acrylic and polysulfide persist in interior decoration and immersion-zone civil works. Regulatory convergence around ISO 11600 and ASTM C920 is elevating performance thresholds, which is accelerating research and development spend on silicone, SMP, and polyurethane while niche chemistries stagnate.

The competitive effects are already visible. Wacker Chemie expanded UK technical support in 2025, and Sika AG introduced Sikaflex-268 PowerCure for rail carriages, aiming to displace polysulfide with faster SMP curing. Smaller formulators focusing on polysulfide now confine their offers to marine and tidal applications where immersion durability still commands a premium. As building-control officers increasingly request EPDs, suppliers that cannot finance lifecycle assessments are losing specification visibility, reinforcing the leadership of vertically integrated silicone and SMP producers.

By End-User Industry: Infrastructure Weighting Versus Healthcare Upswing

Building and construction provided 46.50% of 2025 revenue, but within that total, infrastructure is now the prime growth vector while residential activity remains weak. Healthcare is the fastest-growing end-user, advancing at 6.89% CAGR during the forecast period (2026-2031) because GBP 15.9 billion (USD 20.97 billion) of maintenance backlog covers vital HVAC and sterile-zone resealing. Commercial construction has stabilized as developers retrofit façades to meet Part L energy-performance rules, favoring premium sealants with proven airtightness. Automotive demand is pivoting toward IP67-rated silicone and polyurethane for EV battery housing, offsetting the taper in internal-combustion assembly plants. Aerospace and marine each remain niches yet yield high margins because specifications mandate long service lives and strict VOC compliance.

End-user fragmentation is reorganizing distributor portfolios. Merchant chains allocate more shelf space to SMP and silicone cartridges suited for mixed civil-works and healthcare orders, while residential acrylics occupy a shrinking share. Sealant suppliers increasingly cluster offers around compliance bundles, fire plus VOC or durability plus embodied carbon, rather than around traditional sector segmentation.

Geography Analysis

London, the South East, and the North West accounted for the majority of the United Kingdom Sealants market demand in 2025. London’s consumption is dominated by fire-rated retrofits and high-rise façades, a direct outcome of Building Safety Act enforcement. The South East benefits from 28,400 housing starts and proximity to HS2, Lower Thames Crossing, and Dover upgrades, supporting distributor density. The North West’s share exceeds housing metrics because HS2, motorway refurbishments, and NHS estate upgrades amplify usage of technical-grade polyurethane and polysulfide systems. Scotland and Wales contribute smaller absolute volumes but display distinctive procurement patterns. Scottish frameworks emphasize whole-life costing, driving early adoption of SMP, whereas Wales saw 22.4% year-on-year growth in housing starts during Q3 2025, which could revive acrylic and polyurethane volume if sustained. Northern Ireland remains supply-constrained, yet cross-border trade with the Republic of Ireland allows distributors to arbitrage dual regulations.

Regional fragmentation is forcing national distributors to carry location-specific inventory, intumescent stocks in London, marine-grade polysulfide in the South West, and cost-driven acrylic in the Midlands to preserve service levels. Logistics costs are rising as a result, but higher fill rates are reducing project delays related to material shortages.

Competitive Landscape

The United Kingdom Sealants market is moderately consolidated. Competitive advantages increasingly rest on compliance capability. Suppliers with UKAS-accredited fire-testing facilities and in-house EPD generation turn specification queries around in days, whereas smaller formulators reliant on external labs can lose tenders during wait times. Digital-native distributors are eroding traditional merchant hegemony by offering next-day delivery and AI-based product selection, but they still depend on major brands for technical support.

United Kingdom Sealants Industry Leaders

Dow

Henkel AG & Co. KGaA

Sika AG

Soudal Holding N.V.

Tremco CPG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: BRB International B.V. teamed up with Tennants Distribution Ltd, a chemical distributor based in the United Kingdom. This alliance aims to distribute BRB's Silanes product range throughout the country, with a focus on industries such as sealants, adhesives, coatings, glass fibre, and construction.

- March 2025: Sika AG acquired Cromar Building Products, a United Kingdom-based firm. Cromar's offerings span from membranes and liquid-applied solutions to sealants and adhesives, catering to both residential and large-scale applications.

United Kingdom Sealants Market Report Scope

Sealants, flexible and paste-like, fill gaps, joints, and cracks between surfaces, effectively blocking air, water, moisture, and dust. Widely utilized in aerospace, construction, automotive, and healthcare, sealants protect joints. Unlike adhesives, sealants focus on providing water resistance and sealing, rather than structural bonding.

The United Kingdom Sealants market report is segmented by resin (acrylic, epoxy, polyurethane, silicone, polysulfide, hybrid silane-modified polymer (SMP), and other resins) and end-user industry (aerospace, automotive, building and construction, healthcare, and other end-user industries). The market size and forecasts are provided in terms of value (USD).

By Resin Type

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Polysulfide |

| Hybrid Silane-Modified Polymer (SMP) |

| Other Resins |

By End-user Industry

| Aerospace | |

| Automotive | |

| Building and Construction | Residential |

| Commercial | |

| Infrastructure | |

| Healthcare | |

| Other End-user Industries |

| By Resin Type | Acrylic | |

| Epoxy | ||

| Polyurethane | ||

| Silicone | ||

| Polysulfide | ||

| Hybrid Silane-Modified Polymer (SMP) | ||

| Other Resins | ||

| By End-user Industry | Aerospace | |

| Automotive | ||

| Building and Construction | Residential | |

| Commercial | ||

| Infrastructure | ||

| Healthcare | ||

| Other End-user Industries | ||

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms