Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.73 Billion |

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.45 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Adhesives Market Analysis by Mordor Intelligence

The United Kingdom Adhesives Market size is projected to be USD 1.73 billion in 2025, USD 1.83 billion in 2026, and reach USD 2.45 billion by 2031, growing at a CAGR of 5.98% from 2026 to 2031. Regulatory realignment with EU SVHC updates, rapid uptake of water-borne chemistries, and heavier use of lightweight substrates in mobility, construction, and packaging continue to redefine adhesives from commodity inputs to performance-enabling materials. Water-borne grades already dominate regulatory-sensitive applications, while hot-melt lines capture e-commerce packaging runs that demand sub-60-second set times. Suppliers are improving filler loading and shifting to reactive or bio-based systems to balance raw-material volatility and VOC compliance. Consolidation among global majors is intensifying as acquisition targets supply local production footprints, technical service teams, and regional distribution depth.

Key Report Takeaways

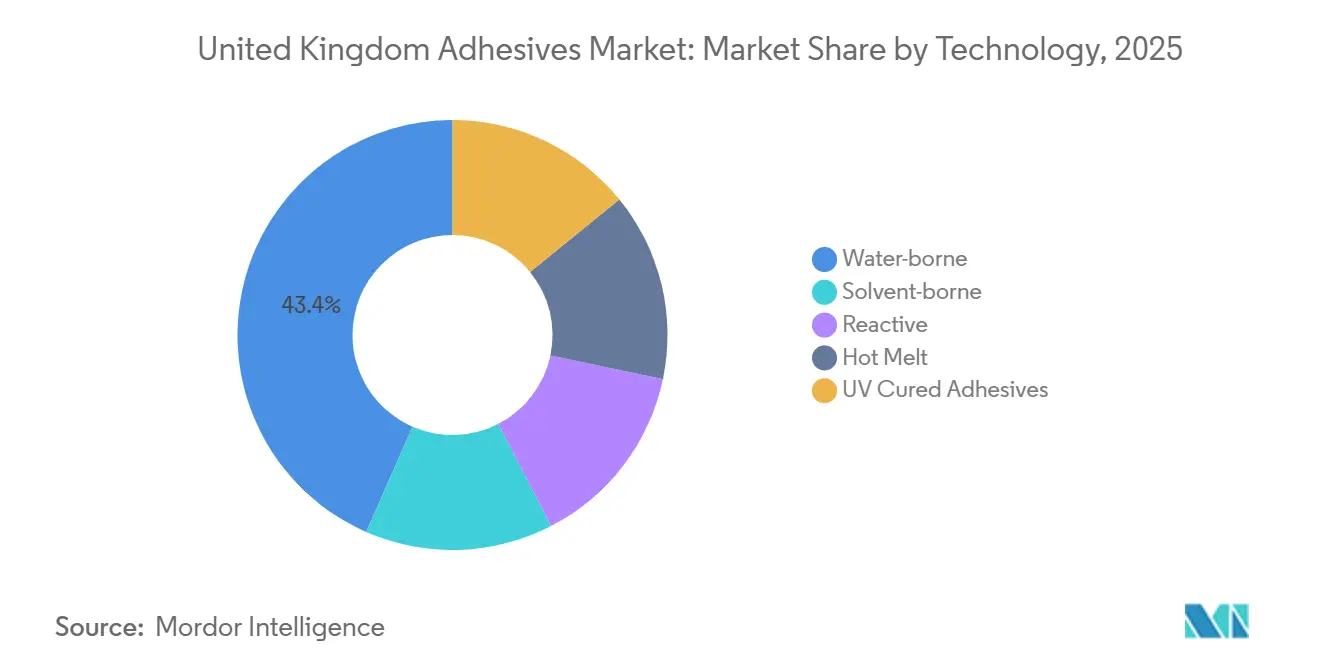

- By technology, water-borne held the largest market share of 43.44% in 2025, and the demand for hot-melt-based ones is expected to grow with a CAGR of 6.26% during the forecast period (2026-2031).

- By resin, acrylic had the largest share of 27.67% in 2025, and VAE/EVA's demand is expected to grow at a CAGR of 6.45% during the forecast period (2026-2031).

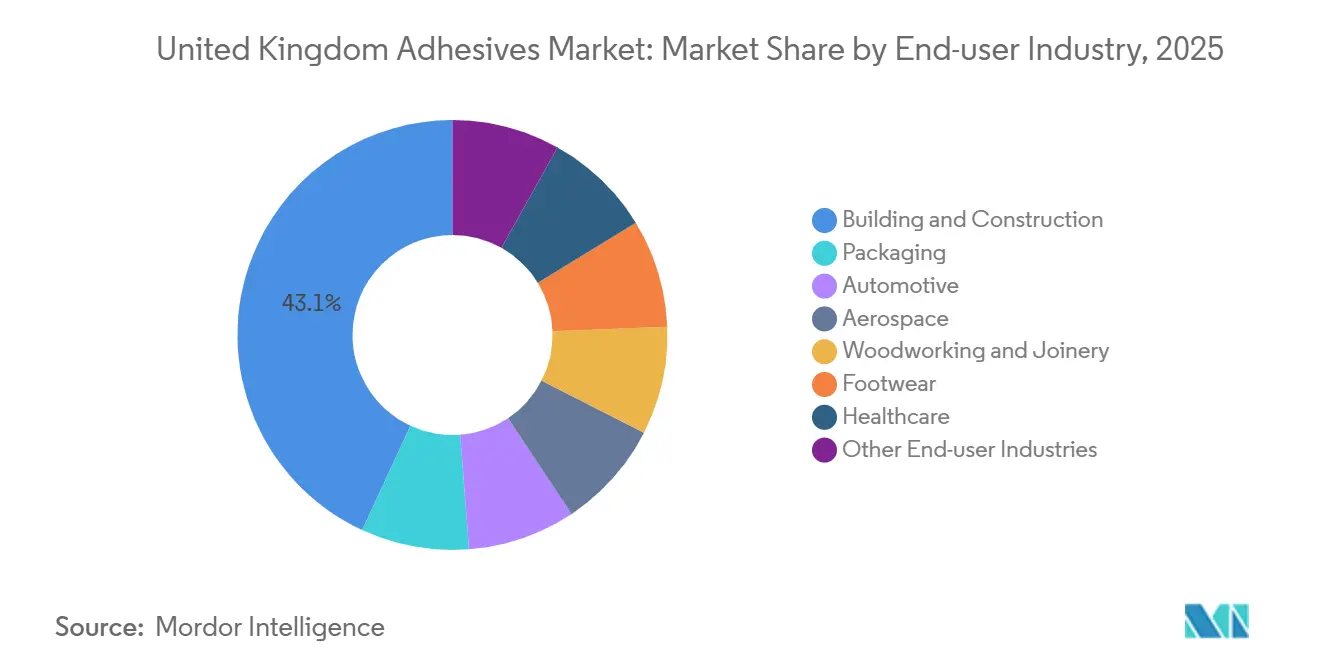

- By end-user industry, building and construction had a market share of 43.11% in 2025, and the automotive industry's share is expected to increase at a CAGR of 6.31% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of lightweight composites in UK automotive manufacturing | +0.8% | England (West Midlands, Coventry), Wales (Bridgend) | Medium term (2-4 years) |

| Increase in modular off-site construction techniques boosting adhesive demand | +1.2% | England (Southeast, Northwest), Scotland (Central Belt) | Short term (≤ 2 years) |

| Rising use of bio-based adhesive formulations driven by UK sustainability mandates | +0.6% | National, with early adoption in public procurement (NHS, local authorities) | Long term (≥ 4 years) |

| Expansion of e-commerce packaging volumes requiring high-performance adhesives | +1.4% | National, concentrated in logistics hubs (East Midlands, Yorkshire, Southeast) | Short term (≤ 2 years) |

| Surge in niche aerospace MRO activities around UK regional airports | +0.3% | England (East Midlands, Southwest), Scotland (Prestwick), Wales (Cardiff) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Lightweight Composites in UK Automotive Manufacturing

Jaguar Land Rover’s GBP 6.3 million (USD 8.31 million) SCALE-UP program is scaling composite doors and recycled carbon-fiber wheels, creating demand for adhesives that bond mixed substrates and survive battery-electric vehicle thermal loads. Henkel’s 2026 agreement to acquire ATP Adhesive Systems adds low-VOC specialty tapes that align with Euro 7 recyclability goals[1]Henkel Investor Relations, “Henkel to Acquire ATP Adhesive Systems,” henkel.com. Digital modelling within SCALE-UP now predicts bond-line performance, shrinking development cycles for suppliers. Polyurethane and epoxy chemistries still dominate structural joints, but cyanoacrylate and silane-terminated polymer options are gaining share where sub-60-second takt times matter. Composite adoption is forecast to trim vehicle mass by 35 kg, reinforcing long-term pull for structural adhesives over mechanical fasteners.

Increase in Modular Off-Site Construction Techniques Boosting Adhesive Demand

Sika’s UK network sells polyurethane and hybrid systems such as SikaTack Panel and Sikaflex-545 that give off-site builders airtight, vibration-tolerant joints without mechanical fixings. Factory controls cut cure-time variance and allow wider roll formats, reducing waste by roughly 30%. Dedicated MMC divisions at several suppliers now offer line-integration support and operator training. Sandwich-panel production speeds reportedly rise 30% when SikaForce systems replace rivets. Hybrid adhesives’ ±25% movement capability minimizes cracking during module transport, a key benefit as housebuilders boost prefabrication to ease labor shortages.

Rising Use of Bio-Based Adhesive Formulations Driven by UK Sustainability Mandates

The United Kingdom bioeconomy logged GBP 12.5 billion (USD 15.97 billion) in revenue in 2024 and is channeling funds into nanocellulose, protein, and PLA adhesive platforms. BASF and partners target 100% bio-based, formaldehyde-free board adhesives under the SUSBOARD project. A lab-scale tannic-acid adhesive retained 70-80% strength after 100 recycling loops, underlining closed-loop potential. Fiscal levers, including Plastic Packaging Tax reform and a bio-preferred procurement scheme, are under review to narrow the current 2-3 times cost premium over petro-based grades. NHS purchasing power, GBP 6.7 billion (USD 8.83 billion) on single-use plastics, could accelerate commercial scale-up pending tax alignment.

Expansion of E-Commerce Packaging Volumes Requiring High-Performance Adhesives

Online retail represented 31.3% of the United Kingdom sales in 2025, far above continental averages, and parcel growth demands hot-melt lines compatible with automated right-sizing systems. H.B. Fuller’s Beardow Adams buyout bolsters paper-friendly formulations sized for high-speed corrugators. The April 2026 Plastic Packaging Tax hike to GBP 228.82 (USD 308.88) per tonne accelerates the swap from plastics to paper void-fill, boosting demand for fast-set paper-to-paper adhesives. Henkel has invested EUR 20 million (USD 21.64 million) in its Bopfingen plant to lift hot-melt and PU capacity aimed squarely at these high-throughput lines. Required properties now include less than 50-minute skin time, low stringing, and fiber-safe debonding during papermill re-pulping.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in raw-material prices linked to petrochemical supply-chain disruptions | -1.1% | National, with acute impact on polyurethane and epoxy formulators | Short term (≤ 2 years) |

| Stringent VOC-emission limits under UK REACH regulations increasing compliance costs | -0.7% | National, particularly affecting solvent-borne adhesive producers | Medium term (2-4 years) |

| Skills shortage in advanced adhesive-application technicians | -0.4% | National, concentrated in manufacturing regions (Midlands, Northwest, Scotland) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw-Material Prices Linked to Petrochemical Supply-Chain Disruptions

Henkel projects low single-digit cost inflation for isocyanates, epoxies, and acrylic monomers in 2026, yet 15-25% quarterly spot swings remain common for some feedstocks[2]Henkel Investor Relations, “Henkel to Acquire ATP Adhesive Systems,” henkel.com. SME formulators, which dominate local supply, lack hedging power and often absorb margin hits or delay capacity upgrades. PFAS and flame-retardant scrutiny within the UK REACH Rolling Action Plan adds further uncertainty. Larger players are countering by boosting mineral-filler loading, but viscosity and application limits cap this tactic. Cost turbulence ultimately favors integrated multinationals with forward-buying leverage and global supply webs.

Stringent VOC-Emission Limits Under UK REACH Regulations Increasing Compliance Costs

The February 2026 policy shift aligns United Kingdom Substances of Very High Concern (SVHC) listings with the European Union schedule, raising the probability that octamethyltrisiloxane, Tris(nonylphenyl)phosphite (TNPP), and other adhesive inputs will face accelerated restriction. Authorisation pathways impose analytical testing, SCIP submissions, and possible sunset-date exemptions, burdens that weigh heaviest on SMEs. PFAS class-based proposals remain under consultation, signaling multi-year compliance preparation. Water-borne lamination systems such as BASF’s Epotal range help converters avoid PAAs during recycling and comply with the EU PPWR recyclability rules effective August 2026. Yet capital spends on drying ovens, humidity control, and solvent-capture upgrades challenge sites running legacy solvent-borne lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Systems Consolidate Regulatory Advantage

Water-borne chemistries accounted for 43.44% of the United Kingdom adhesives market share in 2025, a lead reinforced by the UK’s tighter VOC trajectory and by exporters’ need to satisfy EU PPWR recyclability criteria. Hot-melt products, while smaller in base, are on track for a 6.26% CAGR as the UK adhesives market size tied to e-commerce grows in step with automated parcel lines and paper-based void-fill adoption.

Solvent-borne products confront rising compliance costs and shrinking target niches, though they still win select flooring and exterior joinery work that demands deep substrate wetting. Reactive polyurethane and epoxy systems remain indispensable for structural bonding in composites and modular construction; BASF and Sika’s Baxxodur EC 151 hardener, with 90% lower VOC release, exemplifies the pivot toward low-emission reactive grades. UV-cure lines, though a small slice, are expanding in medical and electronics assembly for instant curing and zero-emission factory floors.

By Resin: Acrylic Leadership With VAE/EVA in Fast-Growth Lane

Acrylics delivered 27.67% of the United Kingdom Adhesives market size in 2025, valued for high-tack transfer tapes, low-fog automotive interiors, and UV-stable façade joints. Vinyl acetate-ethylene systems are outpacing all other resins at a 6.45% CAGR as flexible packaging converters pivot to mono-material films needing low-VOC, plasticizer-resistant bonds.

Polyurethanes rule structural joints where shear strength and vibration damping are paramount, while epoxies answer high-temperature aerospace and industrial assembly needs. Cyanoacrylate demand is rising in medical contexts after H.B. Fuller’s dual 2024 acquisitions added CE-marked tissue-sealant lines to UK-proximate capacity. Silicone formulations remain essential for engines and sanitary sealants that endure up to 300°C.

By End-User Industry: Construction Scale Versus Automotive Momentum

Building and construction absorbed 43.11% share of the market in 2025 as adhesives replaced mechanical fixings in off-site timber panel, volumetric, and sandwich-panel plants. The United Kingdom adhesives market size tied to housing retrofit also benefits from airtightness standards in Part L and PAS 2035 upgrades.

Automotive demand, while smaller, is the fastest-moving slice at a 6.31% CAGR through 2031. Battery-electric platforms need light, corrosion-free composite modules that rely on structural adhesives rather than welds. Packaging follows closely owing to its forecast growth in European e-commerce secondary packaging, pushing hot-melt and VAE lines into multi-shift production arcs. Aerospace MRO, woodworking, footwear, and healthcare each contribute niche but steady pull, with medical device assembly climbing after new clean-room capacities came online in late 2025.

Geography Analysis

England anchors the UK adhesives market with dense clusters around West Midlands automotive plants and Southeast packaging hubs, each serviced by nearby formulators and distributors. Sika’s Welwyn Garden City headquarters coordinates a five-site manufacturing footprint that supplies both factory-built housing lines and national merchant channels.

Scotland’s Central Belt leverages modular timber and renewable-energy projects, drawing hybrid sealants and butyl tapes from local depots. Wales combines Bridgend automotive castings and Cardiff aerospace MRO, supported by H.B. Fuller’s butyl-tape plant acquired in 2024.

Regulatory convergence with EU REACH reduces divergence risk for cross-border supply chains, while Northern Ireland stays under EU chemical rules per the protocol. The British Adhesives & Sealants Association’s January 2026 skills roadmap targets Midlands and Northwest labor pools to remedy technician shortages, offering apprenticeship navigation tools for SME employers.

Competitive Landscape

The UK Adhesives market is moderately concentrated. Domestic specialists such as Hodgson Sealants and BAL Adhesives defend share via technical training and installer guarantees, while disruptors pursue closed-loop bio-based recipes that dissolve on command for recycling. Investment is flowing into AI-driven formulation labs, robotic dispensing trials, and predictive debonding simulations aimed at battery pack refurbishability.

United Kingdom Adhesives Industry Leaders

Arkema Group

Beardow Adams

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: APPLIED Adhesives, a provider of custom adhesive solutions, announced the acquisition of Interlock Adhesives, a United Kingdom-based adhesive technology company. This acquisition represents a significant milestone for APPLIED Adhesives and establishes the company’s presence in the country.

- February 2025: Power Adhesives, a United Kingdom-based global player in hot melt adhesive technology, launched its new bulk adhesive range for industrial applications.

United Kingdom Adhesives Market Report Scope

Adhesives, including glue and paste, bond two surfaces together, preventing their separation. Available in forms like liquid, paste, or tape, these substances are defined by their stickiness, allowing them to adhere to materials such as wood, metal, or skin.

The United Kingdom Adhesives Market is segmented by technology, resin, and end-user industry. By Technology, the market is segmented into water-borne, solvent-borne, reactive, hot melt, and UV-cured adhesives. By Resin, the market is segmented into polyurethane, epoxy, acrylic, cyanoacrylate, VAE/EVA, silicone, and other resins. By End-user Industry, the market is segmented into building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user industries. The market sizes and forecasts are provided in terms of value (USD).

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV Cured Adhesives |

By Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Cyanoacrylate |

| VAE/EVA |

| Silicone |

| Other Resins |

By End-user Industry

| Building and Construction |

| Packaging |

| Automotive |

| Aerospace |

| Woodworking and Joinery |

| Footwear |

| Healthcare |

| Other End-user Industries |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot Melt | |

| UV Cured Adhesives | |

| By Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Cyanoacrylate | |

| VAE/EVA | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Building and Construction |

| Packaging | |

| Automotive | |

| Aerospace | |

| Woodworking and Joinery | |

| Footwear | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms