Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

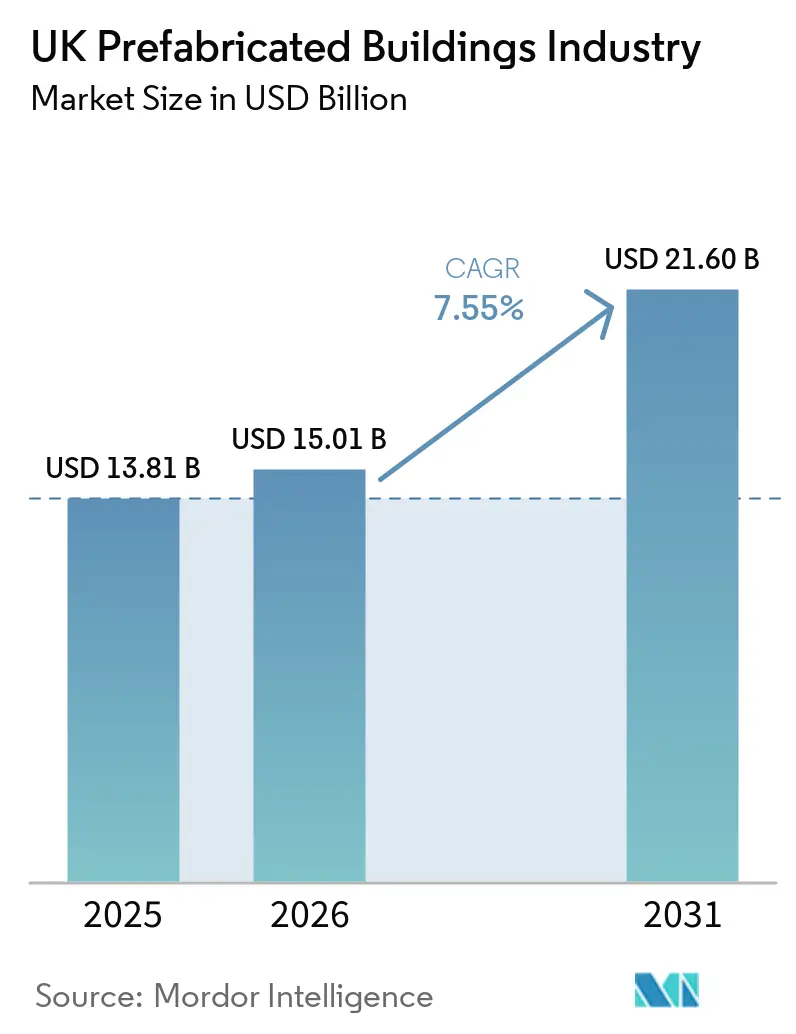

| Base Year Market Size (2025) | USD 13.81 Billion |

| Market Size (2026) | USD 15.01 Billion |

| Market Size (2031) | USD 21.60 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Prefabricated Buildings Industry Analysis by Mordor Intelligence

The UK prefabricated buildings market size was valued at USD 13.81 billion in 2025 and estimated to grow from USD 15.01 billion in 2026 to reach USD 21.60 billion by 2031, at a CAGR of 7.55% during the forecast period (2026-2031). The persistent housing shortfall, stricter net-zero rules, and a shrinking skilled-labor pool are steering developers toward factory-assembled solutions that compress programs and lower embodied carbon[1]GOV.UK, “Government unveils comprehensive plan to build 1.5 million homes,” gov.uk. Public procurement frameworks now embed modern methods of construction (MMC) specifications, guaranteeing multi-year demand that underpins factory utilization. Institutional investors are channeling record capital into modular build-to-rent assets to hit environmental, social, and governance (ESG) targets while securing predictable yields. Meanwhile, tightening road transport regulations, mortgage scrutiny of non-traditional dwellings, and high upfront factory costs remain live constraints that shape product design and financing strategies.

Key Report Takeaways

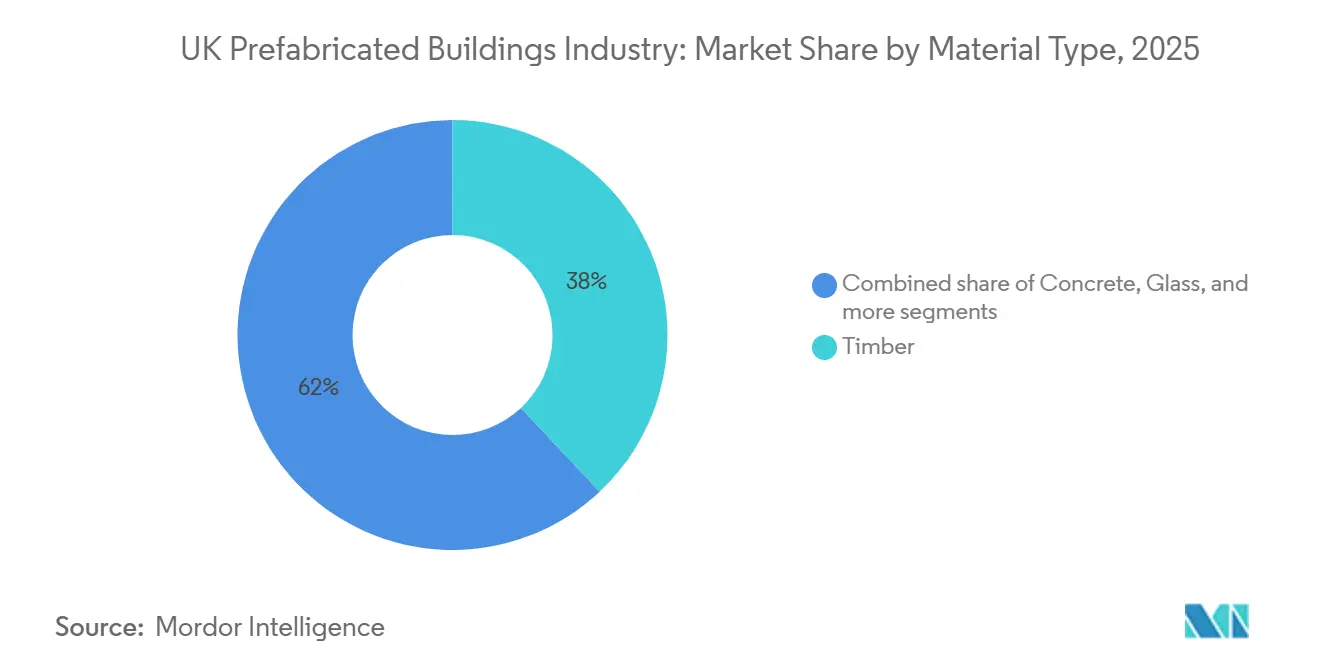

- By material type, timber led with 38% of the UK prefabricated buildings market share in 2025, whereas other materials are projected to expand at an 8.9% CAGR to 2031.

- By application, residential captured a 42% share in 2025, while public and institutional projects are forecast to grow fastest at a 9.5% CAGR through 2031.

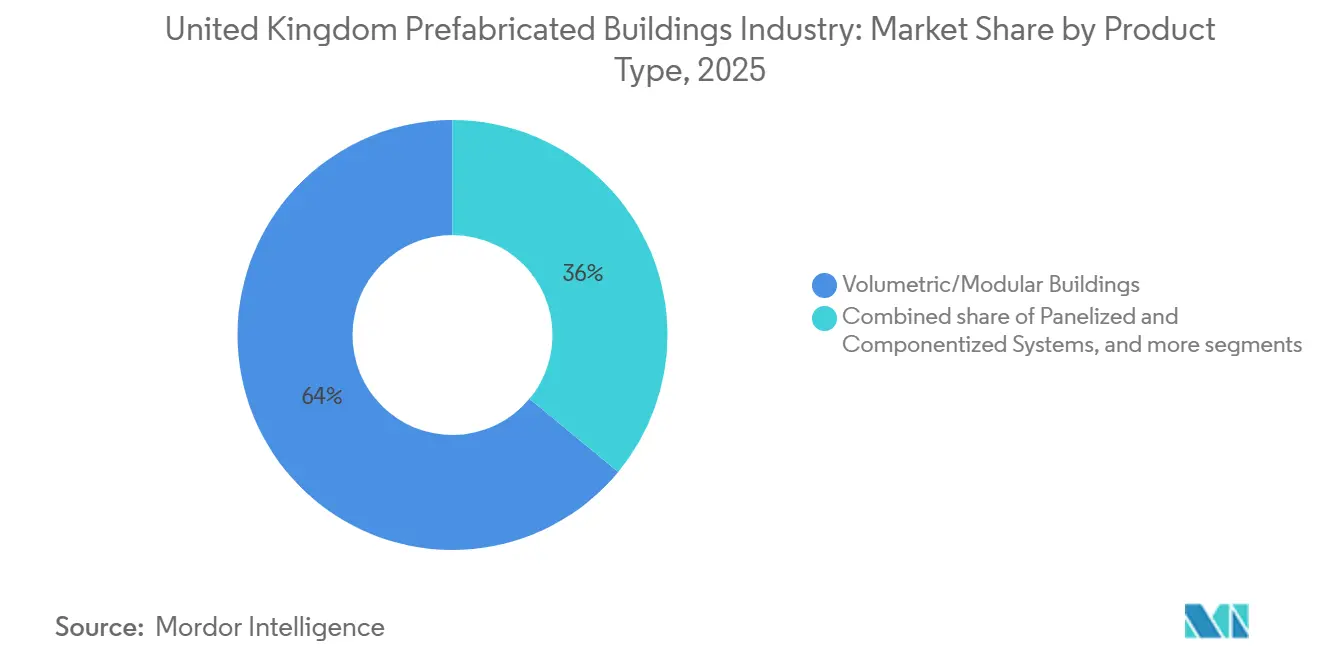

- By product type, volumetric/modular buildings held 64% of the UK prefabricated buildings market size in 2025, and hybrid solutions are advancing at a 15.3% CAGR between 2026 and 2031.

- By region, England accounted for 70% of the overall value in 2025, whereas Scotland is pacing the region with an 8.8% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Prefabricated Buildings Industry Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government ‘300 k-homes’ target accelerating MMC adoption | +1.8% | England, Scotland, Wales | Medium term (2–4 years) |

| Post-Brexit skilled-labour crunch inflating on-site costs | +1.5% | UK-wide, acute in London and South-East | Short term (≤ 2 years) |

| Net-zero & circular-economy mandates favour low-waste off-site methods | +1.2% | UK-wide, policy leadership in Scotland | Long term (≥ 4 years) |

| Public-procurement frameworks (DfE MMC, NHS P23) favour volumetric bids | +1.0% | England health and education pipelines | Medium term (2–4 years) |

| Institutional investors chasing ESG scores via modular BTR assets | +0.9% | Major English cities, notably Birmingham | Medium term (2–4 years) |

| Idle pandemic ICU-module lines repurposed for school classrooms | +0.3% | England and Wales (highest demand from Department for Education projects) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government ‘300 k-homes’ Target Accelerating MMC Adoption

Westminster’s target of 370,000 annual completions and 1.5 million new units by 2030 quadruples the output gap that traditional trades can realistically fill[2]Office for National Statistics, “UK labour market,” ons.gov.uk. Long-run pipeline visibility is encouraging contractors to scale facilities such as Laing O’Rourke’s 25,000 m² Explore Manufacturing plant, which shifted from bespoke precast to standardized volumetric products. Scotland’s Housing Emergency Action Plan allocates USD 6.1 billion and already shows 90% MMC penetration across funded schemes, offering proof of concept for volume certainty. Wales and Northern Ireland backstop roll-outs with dedicated MMC grant lines, creating a UK-wide policy flywheel. The predictable demand stream lowers investment risk and accelerates lender comfort with factory amortization horizons.

Post-Brexit Skilled-Labour Crunch Inflating On-Site Costs

More than 500,000 skilled construction workers are projected to retire by 2030, while EU inflows remain muted, driving wages in London up by 15-20% since 2024. Volumetric manufacturing can trim on-site hours by as much as 40% and substitute capital equipment for scarce trades. Projects such as ZED PODS’ 12-unit Marshall Walk scheme delivered in Bristol during 2025 showcased how short-cycle factory roles filled by re-skilled workers can hit program dates even amid acute labor gaps. Faster delivery and lower exposure to labor volatility reinforce the cost case for the UK prefabricated buildings market.

Net-Zero & Circular-Economy Mandates Favour Low-Waste Off-Site Methods

Part Z carbon accounting, due to enter Building Regulations in 2027, will oblige developers to disclose embodied emissions upfront, tilting material choices toward timber, recycled steel, and low-carbon concrete[3]NHS England, “NHS Modular Buildings Framework,” supplychain.nhs.uk . Laing O’Rourke’s move to all-electric curing lines and 95% low-carbon concrete output proves how plant-level changes can de-risk future compliance. Timber-rich schemes such as Paradise SE11 in London sequestered roughly 2,400 tCO₂e, an outcome hard to replicate in situ. Scotland’s Affordable Housing Supply Programme (AHSP) offers cash uplifts for zero-emissions heating, enabling solar arrays and heat pumps to be factory-installed with less waste. Together, these measures crystallize a structural preference for the UK prefabricated buildings market over conventional builds.

Public-Procurement Frameworks (DfE MMC, NHS P23) Favour Volumetric Bids

The NHS Modular Buildings 3 framework (USD 3.3 billion cap) and the Department for Education’s Category 1 MMC lot pre-qualify suppliers that meet BOPAS, Golden Thread, and digital-twin clauses. Streamlined call-off processes slash procurement lead times, pushing volumetric classrooms and ward blocks onto 12-16-week programs, roughly half traditional schedules. Smaller firms gain route-to-market certainty, while larger players secure baseline orders that improve factory utilization. These frameworks also standardize quality thresholds, lifting buyer confidence and anchoring longer financing tenors. Consequently, public tenders remain the single largest accelerator for the UK prefabricated buildings market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and variable factory loading | -0.8% | UK-wide, heaviest on new entrants | Medium term (2–4 years) |

| Mortgage and valuation hurdles for modular homes | -0.6% | English owner-occupier market | Short term (≤ 2 years) |

| Insolvency shocks eroding supply-chain trust | -0.5% | UK-wide | Short term (≤ 2 years) |

| Road-width limits restricting module size | -0.4% | Urban England and Wales | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX & Uncertain Factory Utilisation

Launching a fully automated line can require USD 13-65 million before a single module ships. Utilization below 60% renders the economy fragile, as Ilke Homes’ 2023 collapse under USD 405 million debt laid bare. Fragmented demand still forces many plants to chase low-margin tenders, delaying break-even timelines. Scotland’s AHSP and England’s NHS frameworks now offer four-year pipelines that stabilize throughput, yet smaller fabricators remain equity-constrained. Consolidation or strategic partnerships are becoming prerequisites to unlock bank financing and sustain the UK prefabricated buildings market.

Mortgage and Valuation Hurdles for Non-Traditional Dwellings

Mainstream lenders insist on BOPAS certification, 30-year design-life evidence, and bespoke surveys before releasing funds, adding weeks to closing and trimming loan-to-value ratios by up to 10 points. The Royal Institution of Chartered Surveyors has yet to publish definitive guidance, leaving valuers to mark down residual values for perceived obsolescence risk. Institutional rentals dodge the issue, but individual buyers face thinner credit options and higher rates. Until standardized appraisal protocols emerge, friction will temper residential uptake within the UK prefabricated buildings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Timber Retains Carbon-Smart Lead

Timber secured 38% of the UK prefabricated buildings market share in 2025, a position underpinned by cross-laminated timber’s favorable carbon profile and structural compatibility with volumetric workflows. Residential mid-rise blocks such as Paradise SE11 used 2,100 m³ of CLT in 2025, offsetting around 2,400 tCO₂e against a concrete frame benchmark. Wooden shells also meet Scotland’s energy-uplift criteria, which add USD 5,900 per unit in grant support, reinforcing cost parity. Other materials, including composite sandwich panels and hybrid steel-timber blends, should accelerate at an 8.9% CAGR, buoyed by the EU’s Carbon Border Adjustment Mechanism that penalizes carbon-rich imports from 2027.

Hybrid assemblies are widening material choice. Explore Manufacturing’s low-carbon concrete now contains 55% recycled aggregates, shrinking embodied emissions by 43% against 2022 baselines. Steel remains indispensable for long-span roofs and industrial bays, yet automated welding cells curb labor reliance. Triple-glazed glass, though still niche, is appearing on panelized façades to meet overheating regulations. Taken together, the material palette supports a flexible supply chain that de-risks sourcing shocks and underwrites the UK prefabricated buildings market size.

By Application: Public & Institutional Pipeline Surges

Residential kept 42% of revenue in 2025, but public & institutional workstreams are pacing growth with a 9.5% CAGR outlook. The NHS Modular Buildings 3 framework streamlines modular healthcare procurement across NHS estates, while the Department for Education's Category 1 MMC program delivers classrooms in about one school term. Swanwick School’s USD 2.6 million two-storey block arrived on-site in July 2025 and opened for pupils that November. For hospitals, volumetric ward pods mitigate infection-control risks by slashing on-site trades, a benefit that resonates in the post-COVID era.

Commercial offices lag as hybrid working dents tenant demand, but logistics sheds and data centers are scaling insulated panel solutions that shrink build schedules by up to 35%. Industrial & Logistics clients appreciate predictable MEP integration and higher thermal performance, critical for cold storage. Public clients’ multi-year budgeting cycles and mandatory social-value scoring guarantee repeat orders, anchoring production forecasts and inflating the UK prefabricated buildings market size for institutional projects.

By Product Type: Hybrid Systems Accelerate

Volumetric/modular buildings controlled 64% of 2025 turnover because turnkey bathroom, kitchen, and plant pods crush on-site durations. Yet road constraints, tall-building fire rules, and bespoke aesthetics drive a 15.3% CAGR for hybrid (volumetric and panels) formats through 2031. Brent Cross Plot 1 demonstrates the model with 4,700 precast and engineered-timber components tracked via a federated digital twin, satisfying Building Safety Act gateway rules without oversize loads. Panelized kits thrive where on-site cranage is easy, and access roads are tight, as seen in Portakabin’s USD 0.8 million lease to City of Liverpool College.

Temporary structures, site offices, and event venues remain a smaller slice, but rising demand for flexible vaccination hubs and disaster relief shelters injects counter-cyclical sales. Overall, product diversification cushions factories against single-segment slowdowns and keeps the UK prefabricated buildings market responsive to shifting regulatory and logistical realities.

Geography Analysis

England contributed 70% of 2025 value, anchored by deep housing demand, the largest NHS estate, and a concentration of institutional capital around the London-Birmingham corridor. Legal & General’s vertically integrated pipeline added over 10,000 modular units by 2025, reinforcing supplier clustering in Yorkshire and the Midlands. Transport bottlenecks are most acute here, prompting hybrid assemblies that fit under 5-m road limits without Special Orders.

Scotland is poised for an 8.8% CAGR to 2031, propelled by a USD 6.1 billion four-year commitment to deliver 36,000 affordable homes and per-unit grant uplifts for zero-emission heating. AHSP data showing 90% MMC uptake validates modular norms, while the Infrastructure Delivery Pipeline 2026 lists school and health projects ideal for volumetric roll-outs. Factory capacity north of the border remains slim, inviting cross-border suppliers to set up satellite lines.

Wales earmarked USD 76 million for its Innovative Housing Programme in 2025 and published pattern-book designs to streamline approvals, a boon for smaller BOPAS-certified firms. Northern Ireland’s rural dispersion calls for transportable pod systems assembled off-grid, and its Housing Supply Strategy 2024-2039 explicitly cites MMC as the lever for cost-effective rollout. Regional nuances in policy and logistics collectively deepen market resilience and spread the risk profile across the UK prefabricated buildings market.

Competitive Landscape

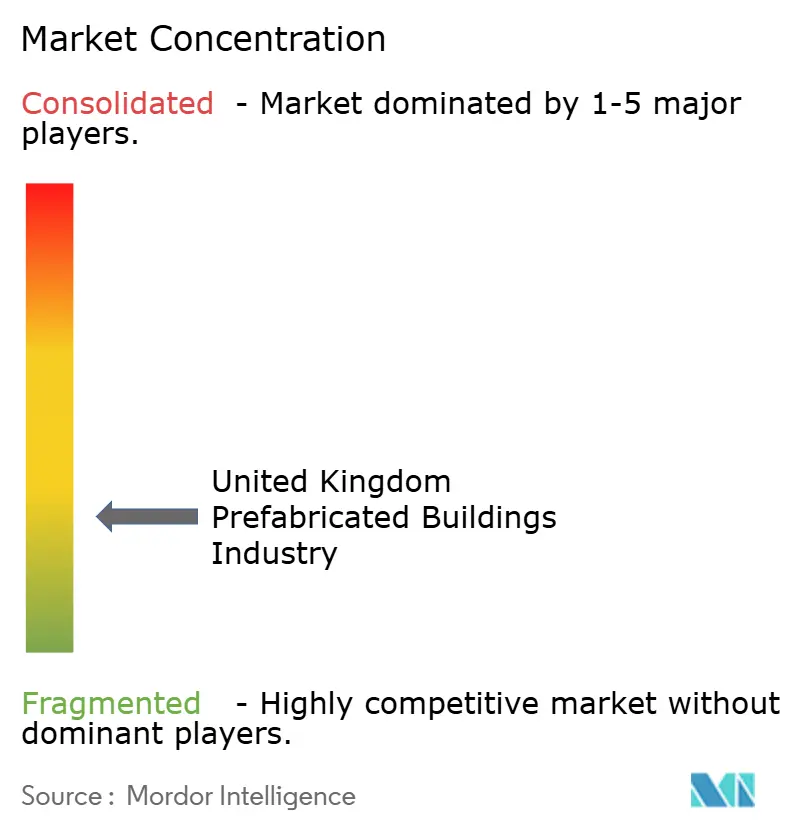

The UK prefabricated buildings market is fragmented in nature. Legal & General’s c handoff model secures land, manufactures modules, and holds assets, squeezing out margins that vertically disintegrated rivals cannot match. Laing O’Rourke repurposed its precast heritage to mass-produce volumetric cores, leveraging existing yards to sidestep greenfield CAPEX.

Framework pre-qualification is a gatekeeper; Portakabin and Premier Modular retained spots on both NHS and LHC panels by meeting Golden Thread and digital-twin clauses. New entrants such as Vision Built Structures focus on niche adaptive-reuse projects where lightweight pods slot into constrained sites. The Ilke Homes collapse raised cautionary flags, but it also opened acquisition opportunities for cash-rich incumbents eager to buy under-utilized factories at distressed prices.

Technology adoption defines the current arms race. Explore Manufacturing deploys automated rebar bending, while PCELtd’s hybrid skeleton carries QR-coded plates for end-to-end traceability. Digital twins reduce post-handover maintenance, an attractive feature for pension funds seeking lifecycle certainty. In this environment, scale, certification breadth, and data fluency determine who captures the next wave of contracts pouring into the UK prefabricated buildings market.

UK Prefabricated Buildings Market Leaders

TopHat

Legal & General Modular Homes

Portakabin Limited

Premier Modular

Laing O’Rourke

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Scottish Government released the Infrastructure Delivery Pipeline 2026, listing housing, health, and education schemes suitable for off-site delivery, giving suppliers long-range line-of-sight on demand.

- November 2025: NHS England unveiled a USD 1.3 billion Commercial Solutions framework with USD 760 million ring-fenced for modular builds to 2029.

- September 2025: Scotland’s Housing Emergency Action Plan allocated USD 6.1 billion over four years and mandated MMC for 90% of funded dwellings.

- July 2025: ZED PODS completed the 12-unit Marshall Walk project in Bristol, meeting social-value KPIs by training day-release prisoners and cutting re-offending rates below 3%.

UK Prefabricated Buildings Industry Report Scope

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Public & Institutional |

| Industrial & Logistics |

By Product Type

| Volumetric/Modular Buildings |

| Panelised & Componentised Systems |

| Hybrid (Volumetric and Panels) |

| Other Prefab Types |

By Region

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Public & Institutional | |

| Industrial & Logistics | |

| By Product Type | Volumetric/Modular Buildings |

| Panelised & Componentised Systems | |

| Hybrid (Volumetric and Panels) | |

| Other Prefab Types | |

| By Region | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Key Questions Answered in the Report

How large is the current UK prefabricated buildings market?

It stood at USD 15.01 billion in 2026 and is on track to reach USD 21.60 billion by 2031.

Which material dominates factory-built projects across the UK?

Timber holds the top spot with 38% share thanks to embodied-carbon advantages and regulatory incentives.

Why is Scotland viewed as a high-growth region?

A USD 6.1 billion four-year housing plan mandates MMC for most funded homes, giving Scotland an 8.8% CAGR outlook.

How are public frameworks shaping demand?

NHS and Department for Education frameworks pre-qualify suppliers and guarantee multi-year call-offs, anchoring factory utilization.

What keeps mortgage lenders cautious about modular homes?

They require BOPAS certification, long-term durability proof, and specialized valuations, adding extra steps to loan approvals.

Page last updated on: