Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

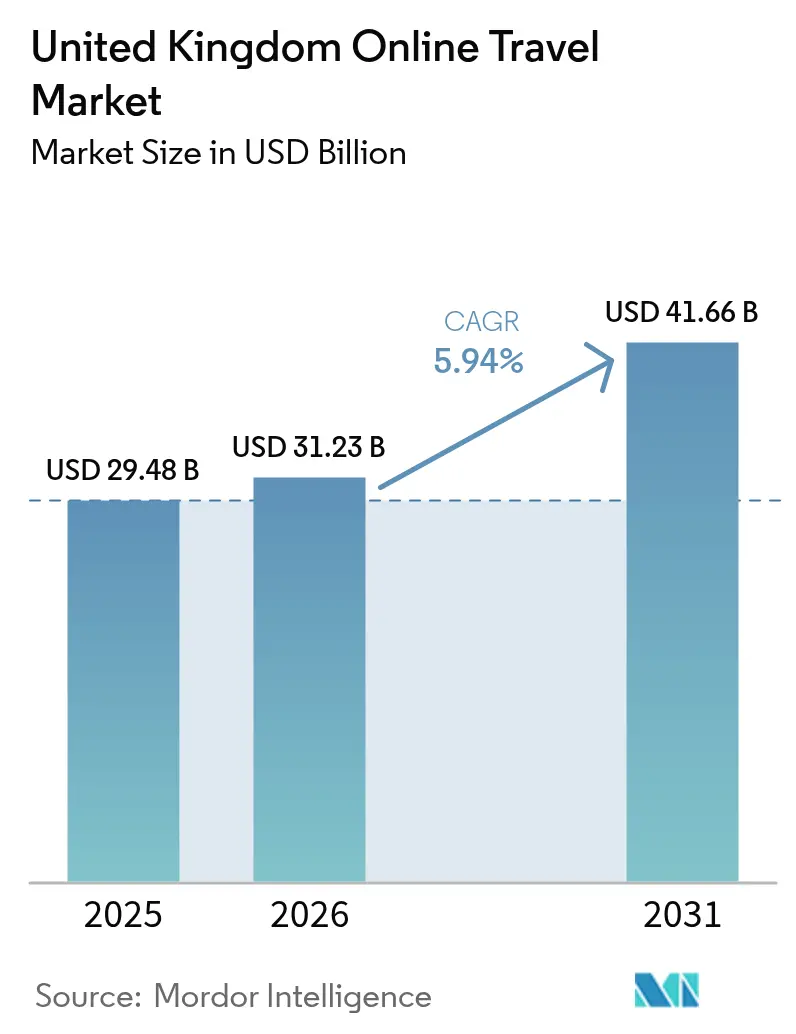

| Base Year Market Size (2025) | USD 29.48 Billion |

| Market Size (2026) | USD 31.23 Billion |

| Market Size (2031) | USD 41.66 Billion |

| Growth Rate (2026 - 2031) | 5.94% CAGR |

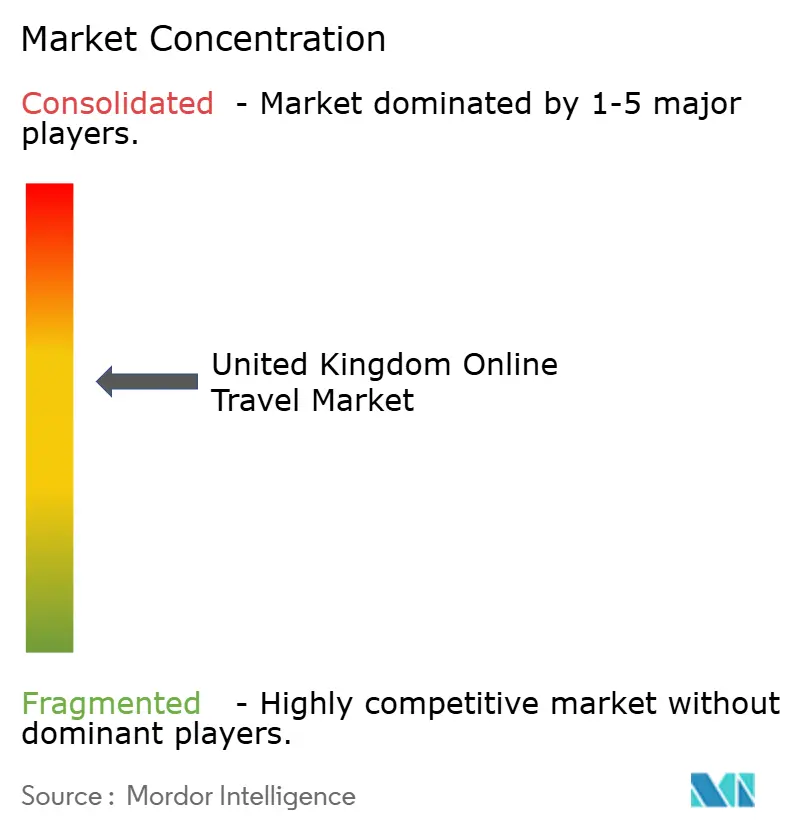

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Online Travel Market Analysis by Mordor Intelligence

The United Kingdom Online Travel Market size market size is expected to grow from USD 29.48 billion in 2025 to USD 31.23 billion in 2026, and is projected to reach USD 41.66 billion by 2031, reflecting a 5.94% CAGR. Robust inbound momentum, stronger household prioritization of travel, and a mobile-first booking shift underpin present growth, while reforms to package-travel rules and greater adoption of open banking improve conversion and margins for digital platforms. Inbound visits hit a record level in 2024 and are forecast to continue rising into 2026, reinforcing sustained demand for inventory across accommodation and transportation. Households are shifting travel spending from discretionary to essential in 2026, with surveys indicating a rising intent to increase holiday budgets and a clearer preference for packaged options that simplify decisions and control total costs. Platforms are shifting strategy toward experience bundling, mobile-native checkout, instant refunds, and loyalty-driven retention, while regulatory changes expand the addressable pool of dynamic packages at lower compliance friction. Open Banking’s rapid uptake improves settlement speed and reduces fees and chargebacks, which supports reinvestment into product innovation and marketing efficiency.

Key Report Takeaways

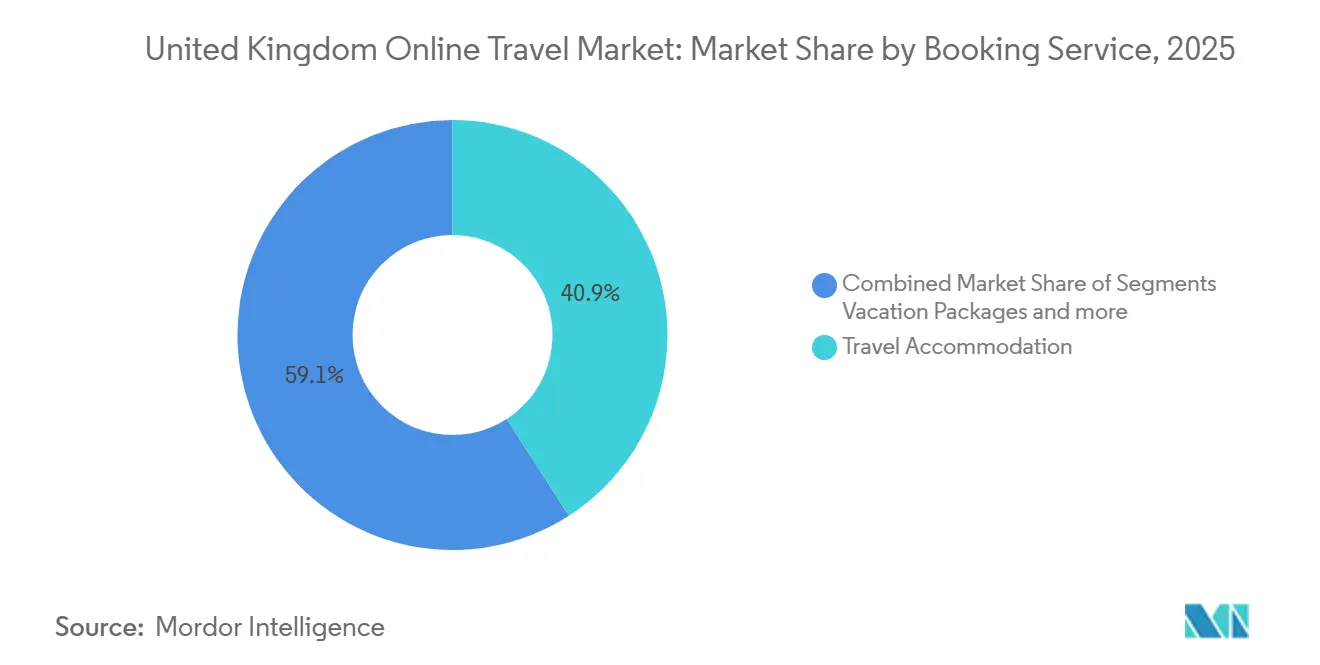

- By booking service, travel accommodation held 40.88% of the United Kingdom online travel market share in 2025, whereas Vacation Packages are advancing at a 10.14% CAGR through 2031.

- By device type, mobile booked 67.34% of the United Kingdom online travel market size in 2025 and is forecast to expand at a 9.49% CAGR to 2031.

- By platform type, online travel agencies captured 65.05% revenue share of the United Kingdom online travel market in 2025, while meta-search engines are projected to grow at 10.90% CAGR.

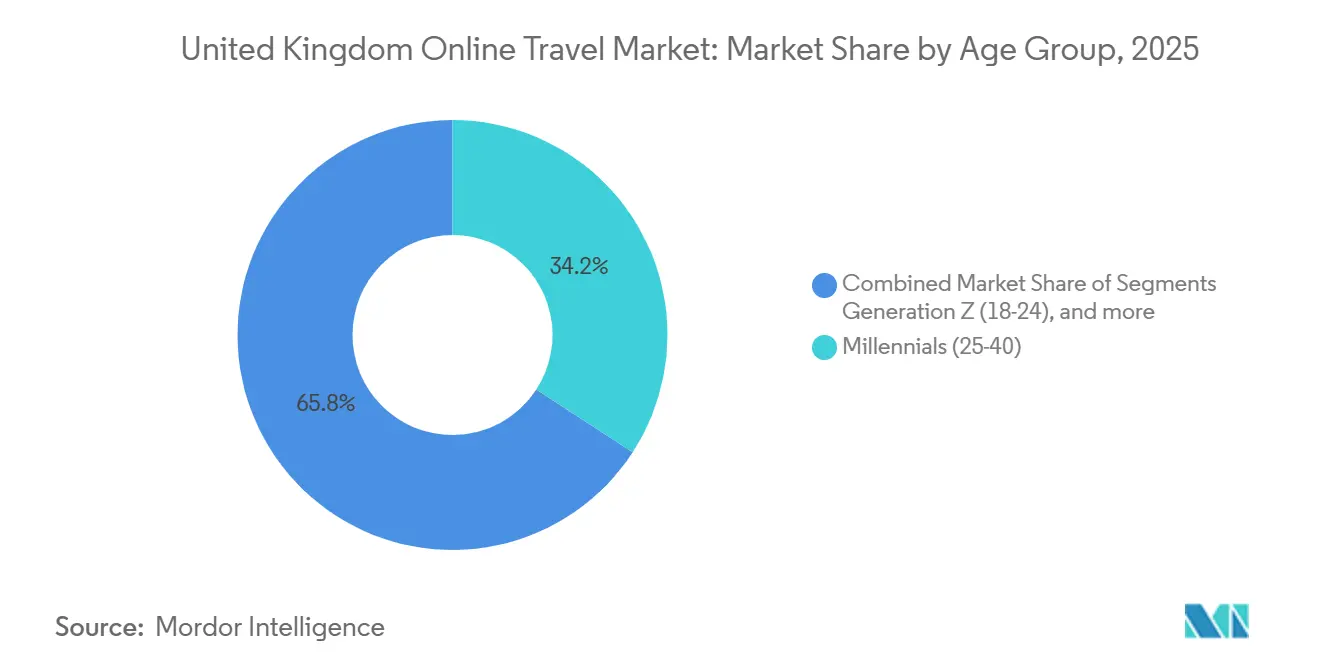

- By age group, millennials controlled 34.18% of the segment revenue of the United Kingdom online travel market in 2025, yet Generation Z usage is scaling at an 7.94% CAGR through 2031.

- By traveller type, leisure trips represented 64.62% of bookings of the United Kingdom online travel market in 2025; the visiting-friends-and-relatives niche is growing fastest at 7.39% CAGR.

- By geography, England accounted for 66.95% of the United Kingdom's online travel market 2025 spend, with Scotland forecast to post the strongest 6.55% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Online Travel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Leisure rebounds as pent-up demand surges post-pandemic | +1.8% | Global, concentrated in England and Scotland | Short term (≤ 2 years) |

| Mobile bookings and in-app payments see rapid acceleration | +1.5% | Global, led by Asia-Pacific spillover and United Kingdom mobile-first Gen Z | Medium term (2-4 years) |

| Dynamic packaging legislation raises commission caps | +0.9% | National, early gains in England, Scotland, Wales | Medium term (2-4 years) |

| "Work-from-anywhere" travel policies gain mainstream acceptance | +0.7% | Global, strongest in urban England and Scotland hubs | Long term (≥ 4 years) |

| Digital twins of heritage sites enhance immersive trip planning | +0.5% | National, United Kingdom heritage sites; spillover to European operators | Long term (≥ 4 years) |

| Instant refunds via open banking bolster customer trust | +0.5% | Global, regulatory tailwinds in United Kingdom and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Leisure rebounds as pent-up demand surges post-pandemic

Inbound visits set a new high in 2024 and are forecast to rise further through 2026, signaling that the demand recovery has moved into a steady expansion phase rather than a short-term spike. Large consumer panels in 2025 indicated that holidays moved up the household priority list, with a rising share of Britons planning to increase spending on trips through 2026. Household data points to travel as one of the fastest-growing categories of outlay, reinforcing that leisure has become a non-negotiable line item in many budgets. This demand shows resilience in the face of currency swings, which suggests that value perception is anchored more in experience quality than in exchange-rate sensitivity. Packaged offers that deliver clarity on total cost and convenience are seeing stronger consideration, which creates room for platforms to scale dynamic combinations of flights, accommodation, and activities.

Mobile bookings and in-app payments see rapid acceleration

Mobile accounted for two-thirds of digital bookings in 2025 and is growing faster than desktop, reflecting consumer comfort with researching and completing purchases on phones. Account-to-account payments gained traction in 2025 as open banking enabled instant settlement, lower processing fees, and fewer chargebacks across large travel portfolios. These rails reduce friction at checkout, which improves conversion on mobile and frees up margin that operators can deploy into pricing, service, and loyalty initiatives. The rise of conversational discovery tools is collapsing the gap between inspiration and purchase, which shifts value toward platforms that can capture intent and close the sale within a single mobile session. As adoption of mobile-native features such as stored profiles, flexible payments, and instant refunds expands, retention improves, and cost to serve declines for well-optimized apps.

Dynamic packaging legislation raises commission caps

UK reforms finalized in December 2025 will be legislated by June 2026, absorbing Linked Travel Arrangement Type A into package definitions, removing Type B, and setting a 14-day refund period, which simplifies compliance for digital organizers[1]Source: Department for Business & Trade, “Government response to 'Package travel – updating the framework 2025' consultation“, GOV.UK. The government expects these changes to stimulate significant incremental domestic expenditure and job creation by making it easier for smaller firms and platforms to compete with packaged itineraries. For online intermediaries, removing Type B reduces the risk of inadvertently triggering organizer obligations when customers assemble trips, which allows monetization of planning tools without disproportionate liability[2]Source: Department for Business & Trade, “Government response to 'Package travel – updating the framework 2025' consultation“, GOV.UK. The reforms land as traveler interest in packages increases into 2026, which aligns regulatory tailwinds with consumer demand and supports faster growth for platforms that master compliant dynamic assembly. UK-focused players with modular tech stacks can code jurisdiction-specific rules for each component, enabling cross-border scaling while the EU proceeds with its own directive changes.

"Work-from-anywhere" travel policies gain mainstream acceptance

Corporate travel patterns in 2026 show more blending of business and leisure, as remote and hybrid policies encourage extended stays that cross weekday and weekend demand. Urban hubs tied to coworking and transport infrastructure see steadier midweek occupancy, while coastal and resort areas capture incremental nights from remote workers who prioritize wellness and connectivity. Younger professionals now weigh amenities such as gyms, spa access, and reliable broadband when choosing properties for trips that include work obligations. Platforms can create new yield by surfacing filters for workspace needs and re-pricing longer stays to convert traditional weekend breaks into week-long workations. The Digital Markets, Competition and Consumers Act requires clear total-price display, which helps travelers compare bleisure packages across providers without hidden fees undermining transparency.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UK card issuers are raising merchant service fees | -0.4% | National, concentrated among OTAs with high card-payment share | Short term (≤ 2 years) |

| Airlines face a capacity crunch due to slot constraints at Heathrow | -0.6% | National, bottleneck at Heathrow; spillover to Manchester, Gatwick | Medium term (2-4 years) |

| Data privacy regulations are tightening, especially on third-party cookie tracking | -0.3% | Cross-border, UK operators serving EU markets | Medium term (2-4 years) |

| Fluctuating GBP-EUR exchange rates are compressing OTA margins | -0.2% | Global, affecting UK traffic mix across web, meta, and chat | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

United Kingdom card issuers are raising merchant service fees

Higher card-processing costs in the United Kingdom are tightening margins for intermediaries that rely on card rails for a large portion of transactions. This pressure is accelerating the shift to open banking and account-to-account options that offer lower fees, immediate settlement, and better chargeback profiles. As more volume moves to these rails, operators can protect unit economics on price-sensitive segments while improving checkout experience on mobile. The DMCC Act increases enforcement risks around mislabeling or drip pricing, which makes transparent communication of any payment surcharges a compliance priority[3]Source: GOV.UK, “Guidance on Unfair commercial practices”, GOV.UK. Together, these dynamics create margin divergence between platforms that modernize payment stacks and those constrained by legacy arrangements.

Airlines face a capacity crunch due to slot constraints at Heathrow

Heathrow continues to operate near movement and passenger limits, which caps growth for peak-demand routes that anchor many packaged itineraries. The airport selected a large expansion plan in 2025, but timelines extend well beyond the current forecast period, which means seat availability remains tight in the near term. Capacity constraints give price power to incumbents with established slot portfolios, while pushing some demand to secondary airports and rail alternatives. Operators and tour brands are responding by adding lift from other London-area airports and regional bases to diversify supply for sun and city routes. Until new runway and terminal capacity come online, online booking platforms must optimize inventory mix, flexible dates, and multi-airport search to mitigate supply bottlenecks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Service: Packages Propel Multi-Vertical Expansion

Travel Accommodation held 40.88% of the United Kingdom Online Travel Market share in 2025, while Vacation Packages is forecast to scale at a 10.14% CAGR through 2031. Package consideration is rising into 2026 as travelers seek predictable total cost, streamlined planning, and protection within a single transaction. Regulatory reform scheduled for June 2026 reduces administrative friction for dynamic packaging and clarifies refund obligations, which can expand inventory variety while preserving consumer safeguards. As supply normalizes across airlines and hotels, platforms can scale multi-vertical transactions by combining air, stay, and activities under one itinerary to boost attachment and margin. Larger brands and fast-growing UK specialists are also retooling content partnerships to add cruises, experiences, and insurance, which creates more cross-sell potential across the booking journey.

Vacation Packages benefit from clearer rules around Linked Travel Arrangements, which frees organizers to suggest relevant add-ons without unintentionally assuming organizer liability when the customer assembles the trip. Transportation sub-categories, such as rail and bus, see digital growth as distribution integrates with OTA and corporate channels, while cruise gains visibility through new retailing features. Alternative lodging continues to expand within the accommodation stack, although some urban short-stay categories are navigating tighter local registration and compliance protocols. Ancillaries like tours, activities, and flexible protection products are favorable for contribution margins and can be embedded into flows via APIs. Across these booking services, the United Kingdom Online Travel Industry is prioritizing data governance, consent, and age-appropriate design in line with new data-use rules that phase in from 2025.

By Device Type: Mobile Commands Two-Thirds, Desktop Holds Complex Itineraries

Mobile devices booked 67.34% of the United Kingdom Online Travel Market size in 2025 and are forecast to expand at a 9.49% CAGR through 2031. The shift is reinforced by open banking payments that settle instantly, carry lower fees, and reduce disputes, which strengthens unit economics for app transactions. Conversational discovery and assistive AI reduce the number of steps from inspiration to checkout, which gives mobile an advantage in closing intent fast. Younger cohorts continue to research and book on phones at high rates, which supports long-run share gains for mobile in the United Kingdom Online Travel Market.

Desktop and laptop remain important for complex, multi-stop itineraries, where larger screens help compare options across dates, cities, and components. Many shoppers start discovery on mobile and finish purchase on desktop for intricate trips, which means cross-device session stitching and saved carts matter for conversion. Platforms that make total pricing transparent on small screens comply with DMCC obligations while reducing unexpected fees at checkout. Social commerce features embedded into apps deepen engagement by turning trip planning into a collaborative activity rather than a single-user task. This device split allows targeted UX investment by journey type, with mobile optimized for speed and desktop optimized for comparison in the United Kingdom Online Travel Market.

By Platform Type: OTAs Dominate, Meta-Search Scales Fastest

Online Travel Agencies captured 65.05% of the United Kingdom Online Travel Market share in 2025, while meta-search engines are projected to grow at the fastest rate with a 10.90% CAGR through 2031. OTAs maintain leadership thanks to the breadth of inventory and loyalty integrations that simplify cross-vertical shopping and after-sales support. Discovery is changing as AI-powered meta-search experiences filter options faster and route ready-to-buy traffic into supplier or OTA funnels. Direct supplier sites continue to invest in merchandising, payment choice, and loyalty benefits to reduce dependency on intermediaries.

B2B infrastructure is an expanding focus area for leading platforms, which unbundle payments, fraud prevention, and inventory as modular services for partners. New features like package comparison aim to aggregate millions of offers daily and help consumers evaluate total price and inclusions with more clarity. The United Kingdom Online Travel Industry is also adding conversational interfaces that support natural language planning and rapid quoting for multi-component trips. Regulatory enforcement on ranking transparency and drip pricing continues to shape platform presentation and fee disclosure. These shifts keep competition intense while opening niches for specialists that solve high-frihigh frictiones in the United Kingdom Online Travel Market.

By Traveller Type: Leisure Dominates, VFR Grows Fastest

Leisure accounted for 64.62% of bookings in 2025 in the United Kingdom Online Travel Market size, while Visiting Friends and Relatives is the fastest growing purpose at a 7.39% CAGR through 2031. Inbound and domestic indicators for 2025 and 2026 point to sustained holiday demand, which remains the primary engine of growth for platforms. VFR outperformed other journey purposes in 2025, aided by reconnecting families and diaspora travel that extends the length of stay and flexibility windows. Business travel has stabilized, while blended itineraries create cross-sell opportunities for upgrades and add-ons over longer stays. Transparent total pricing rules under the DMCC Act enable clearer comparison for multi-traveler bookings, which supports trust across leisure and VFR segments.

Leisure is fragmenting into premium and value tiers, with luxury travelers prioritizing new experiences and wellness, and budget travelers optimizing for longer trips via flexible dates and alternative lodging. VFR itineraries favor flexibility and proximity over bundled activities, but attachment rates for rail, coach, and insurance are rising as platforms surface relevant options. Corporate APIs that expose multi-modal inventory are helping travel managers support bleisure policies, which bridge business and leisure distribution. Across traveler types, refund speed and payment choice have become deciding factors, where open banking adoption continues to build confidence. These patterns reinforce the central position of leisure and the accelerating role of VFR in shaping inventory and merchandising in the United Kingdom Online Travel Market.

By Age Group: Millennials Lead Spend, Gen Z Scales Fastest via AI

Millennials accounted for 34.18% of spending in 2025, reflecting peak income years and higher trip frequency across domestic and international categories. Generation Z is the fastest-growing cohort with a 7.94% CAGR to 2031, lifted by higher confidence in AI planning tools and heavier reliance on mobile-led discovery. Younger adults show rising willingness to use AI for research and option comparison, and they consume travel inspiration heavily on short-form video. Millennials continue to book end-to-end online at the highest rate among cohorts, which keeps OTAs central to their purchase paths. Older travelers, especially those 65-plus, are maintaining strong travel intent and higher per-trip spend, which supports a wide range of property and itinerary types.

Gen Z and Millennials both value clear pricing, strong reviews, and flexible payments, although younger travelers display more budget-stretching tactics such as off-peak timing and shared stays. Sustainability preference is strongest among Gen Z, with a majority willing to pay more for companies with demonstrable environmental practices. Content and community features matter for discovery and trust, which favors app ecosystems that integrate profiles, messaging, and social proof. The United Kingdom Online Travel Industry is incorporating age-appropriate design and consent flows as new data-use provisions phase in, which is essential for products aimed at younger audiences. These cohort dynamics guide product roadmaps that balance personalization with transparency across the United Kingdom Online Travel Market.

Geography Analysis

England accounted for 66.95% of the spend in 2025, while Scotland is forecast to post the strongest 6.55% CAGR through 2031 in the United Kingdom Online Travel Market size. England generated the vast majority of Great Britain's overnight trips, nights, and spending across January to September 2025, supported by London’s global draw and a deep mix of regional attractions. Scotland delivered growth in domestic overnight trips and spend in January to September 2025, the only nation in Great Britain to post gains in that window. Edinburgh and Glasgow anchor international arrivals, and strong regional performance is lifting occupancy and spend across more destinations. Forecast growth reflects a rotation toward heritage, culture, and nature that supports year-round itineraries in Scotland.

Wales recorded millions of overnight trips and significant spend in January to September 2025, with a strong third quarter in trips and nights that confirms improving momentum. Coast and countryside remain central to Wales’s appeal, and inbound spend showed positive movement through the first three quarters of 2025. Northern Ireland remains a smaller component of the United Kingdom Online Travel Market, though digital discovery and cross-Irish Sea connectivity help support steady demand for city breaks and nature-led trips. National tourism organizations coordinate promotion and reporting, while sustainability standards and local certifications require careful listing compliance for regional inventory. These geographic patterns suggest targeted opportunities for platforms to localize content and optimize channel mix by nation within the United Kingdom Online Travel Market.

Competitive Landscape

The United Kingdom Online Travel Market shows moderate-to-high concentration, with large global OTAs leading revenue while regional and vertical specialists scale through product and distribution innovation. Booking Holdings reported double-digit growth in Q4 2025 room nights and gross bookings and highlighted rising multi-vertical transactions in the high-20% range year-over-year, supported by a 25-to-1 stock split effective April 2026 and a higher dividend. Expedia continues to expand its B2B Partner Solutions to monetize payment, fraud detection, and inventory services beyond consumer-facing travel, emphasizing infrastructure distribution. UK-focused operators are adding capacity and new products, which creates alternatives to Heathrow-centric supply while deepening package choice for sun and city routes. These moves sustain competitive pressure while increasing the role of platform infrastructure in the United Kingdom Online Travel Market.

Trainline is scaling AI-enabled customer support and compensation features, processing near seven-figure totals in automated delay-repay during H1 FY2026 and raising full-year guidance on improving profitability. On the Beach executed share buybacks, expanded into cruises and new geographies, and upgraded profitability, which reflects disciplined capital allocation and product diversification. lastminute.com launched a Model Context Protocol server for flights that integrates with conversational AI ecosystems, with hotel and dynamic-packaging capabilities in development. Hostelworld is growing engagement through social features and member-led discovery, which increases app conversion and lifetime value. Together, these examples show how UK-aligned players can win share by combining mobile-native UX, AI, and infrastructure offerings in the United Kingdom Online Travel Market.

Airport capacity constraints and compliance rules shape strategy for 2026. Heathrow’s capacity timeline stretches into the next decade, prompting carriers and tour operators to add lift from other airports and adjust route plans. Jet2 announced a 27% capacity increase from London Gatwick for Summer 2027, with first flights starting in March 2026, which diversifies access for popular leisure destinations. Package regulation reform clarifies organizer liabilities and refunds, which supports dynamic packaging growth for platforms that can encode rules and deliver transparent total pricing. These macro and regulatory factors will continue to reward operators that align with transparency, fast refunds, and mobile-led booking in the United Kingdom Online Travel Market.

United Kingdom Online Travel Industry Leaders

Booking Holdings Inc.

Expedia Group Inc.

Airbnb Inc.

TUI Group

On the Beach Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Jet2 announced a 27% capacity increase from London Gatwick for Summer 2027, reaching 1.1 million seats across 35 sun and leisure city destinations, including an exclusive weekly service to Lesvos, Greece, with first flights commencing March 26, 2026.

- January 2026: Skyscanner launched a package-holiday comparison tool aggregating over 25 million packages daily and rolled out a Cheapest Destination Planner feature as part of an experience that serves over 110 million monthly users and more than 200 million travel plans annually.

- January 2026: lastminute.com introduced the travel industry’s first Model Context Protocol server for flights, listed on Anthropic Marketplace for integration, with plans announced for hotel and dynamic-packaging MCP servers.

- December 2025: The UK government finalized reforms to the Package Travel Regulations to be legislated by June 2026, absorbing Linked Travel Arrangement Type A into package definitions, removing Type B, and establishing a 14-day refund period, with expected gains in domestic expenditure and job creation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom online travel market as all consumer bookings for domestic or outbound transportation, lodging, vacation packages, and ancillary travel services that are transacted and paid for through internet-enabled interfaces on desktops, laptops, or mobile devices, whether via an online travel agency, metasearch site, or a supplier's own portal, and expressed in gross booking value before commissions.

Scope Exclusion: Purchases completed through bricks-and-mortar travel shops, call centers, or corporate self-booking tools fall outside this market.

Segmentation Overview

- By Booking Service

- Transportation

- Air Travel

- Bus & Coach Travel

- Rail Travel

- Car Rental

- Cruise

- Travel Accommodation

- Hotels & Resorts

- Alternative Lodging / Rentals

- Vacation Packages

- Others (Activities, Travel Insurance, Ancillary)

- Transportation

- By Device Type

- Desktop & Laptop

- Mobile (Smartphone & Tablet)

- By Platform Type

- Online Travel Agencies (OTAs)

- Direct Supplier Websites

- Meta-search Engines

- By Traveler Type

- Leisure

- Business

- Visiting Friends & Relatives (VFR)

- By Age Group

- Generation Z (18-24)

- Millennials (25-40)

- Generation X (41-56)

- Baby Boomers (57-75)

- By Region

- England

- Scotland

- Wales

- Northern Ireland

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed airline revenue-management executives, OTA category managers, hotel distribution heads, and payment-gateway providers across England, Scotland, and Wales. These conversations clarified ride-sharing bundling rates, mobile-only promo adoption, and seasonality inflections, letting us refine assumptions and close gaps spotted in desk work.

Desk Research

We began with publicly available macro data, monthly inbound and outbound traveler volumes from the UK Office for National Statistics, Civil Aviation Authority passenger counts, the Bank of England's card-spend series, and Ofcom's annual internet-penetration survey to anchor demand, spend, and digital reach. Trade bodies such as ABTA, WTTC, and the European Travel Commission supplied trend notes on booking channel shifts, while company 10-Ks and investor decks helped us benchmark average selling prices and take rates. Select paid repositories, notably D&B Hoovers for revenue splits and Dow Jones Factiva for press releases, rounded out firm-level inputs. The sources cited are illustrative rather than exhaustive; many additional references informed data checks.

Market-Sizing & Forecasting

A top-down build starts with traveler counts by purpose and trip length, multiplied by spend per trip adjusted for the share booked online. Results are cross-checked through sampled OTA gross bookings, supplier-direct digital sales, and channel take-rate disclosures. Key model variables include smartphone penetration, outbound holiday frequency, average airfares, accommodation ADR, and promotional discount depth. Multivariate regression, incorporating GDP per capita and real exchange-rate swings, projects these drivers to 2030. Where supplier roll-ups ran thin, calibration occurred once senior interviewees validated realistic conversion funnels.

Data Validation & Update Cycle

Outputs face two tiers of scrutiny. First, built-in variance tests flag outliers against historic ratios; second, a senior peer reviews every worksheet before sign-off. We refresh models annually and trigger interim revisions after material events such as a VAT change or major platform merger, ensuring clients always receive a current viewpoint.

Why Mordor's United Kingdom Online Travel Baseline Rings True

Published numbers often diverge because analysts choose different scopes, base years, or digital-spend definitions.

By aligning our scope tightly to gross online bookings and applying recent 2024 card-spend benchmarks, Mordor minimizes such drift.

Key gap drivers include whether peer reports fold in offline agency websites, how they treat peer-to-peer rentals, their currency-conversion date, and the cadence at which assumptions are refreshed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 29.48 B (2025) | Mordor Intelligence | |

| USD 42.60 B (2024) | Global Consultancy A | Includes offline agency web bookings and service-fee markups |

| USD 26.20 B (2021) | Industry Analysis B | Older base year; excludes peer-to-peer lodging yet applies global CAGR to UK |

The comparison shows that once outdated bases, wider scopes, or unverified markups are stripped away, our disciplined variable selection and yearly refresh provide a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the United Kingdom online travel market?

The market reached USD 29.48 billion in 2025, stands at USD 31.23 billion in 2026, and is projected to reach USD 41.66 billion by 2031 at a 5.94% CAGR.

Which booking service segment is growing fastest?

Vacation Packages lead with a 10.14% CAGR through 2031, supported by dynamic packaging regulations that removed commission caps.

How is mobile shaping the United Kingdom Online Travel Market?

Mobile accounted for 67.34% of bookings in 2025 and is set to grow at a 9.49% CAGR, aided by open banking that reduces fees and speeds refunds.

What policy changes are most important to watch in 2026?

UK package-travel reforms legislated by June 2026 will absorb LTA Type A, remove Type B, and set 14-day refunds, which simplifies dynamic packaging and improves buyer protection.

Which traveler segments are driving demand in the United Kingdom Online Travel Market?

Leisure accounted for 64.62% of bookings in 2025 and Visiting Friends and Relatives is the fastest growing purpose through 2031, with Gen Z accelerating due to higher trust in AI tools.

Which regions within the UK are most important for digital travel demand?

England accounted for 66.95% of 2025 spend, while Scotland is forecast to post the strongest CAGR over the outlook period on the back of solid domestic overnight growth.

Page last updated on: