Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

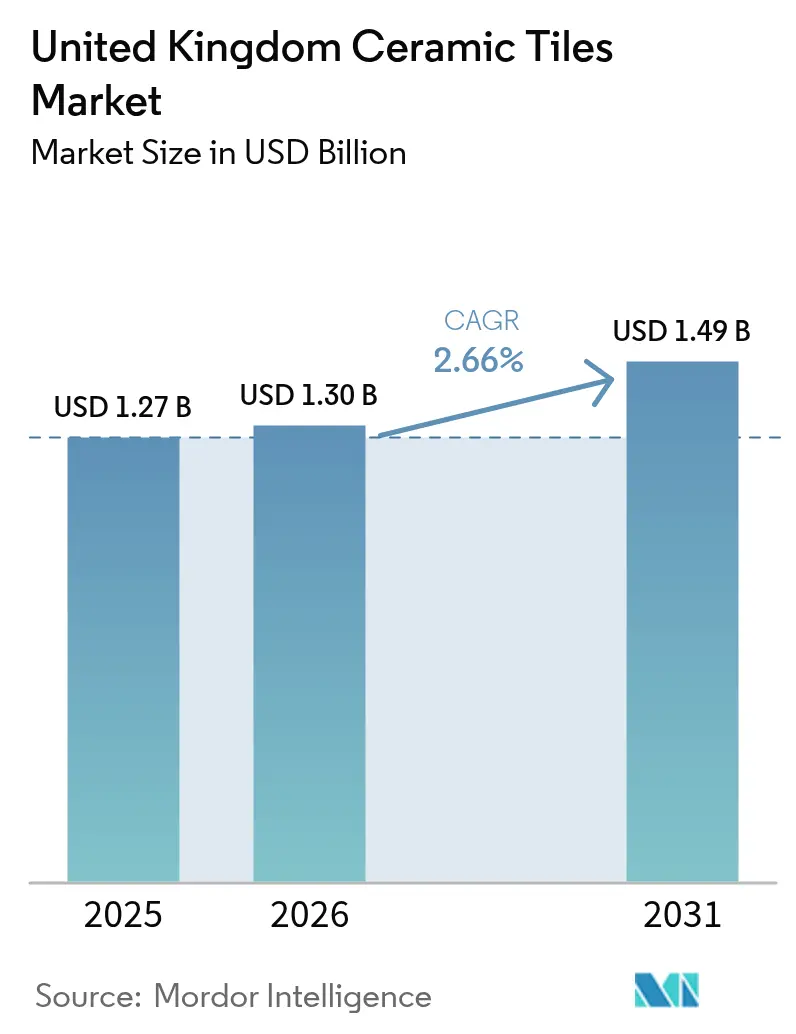

| Base Year Market Size (2025) | USD 1.27 Billion |

| Market Size (2026) | USD 1.3 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 2.66% CAGR |

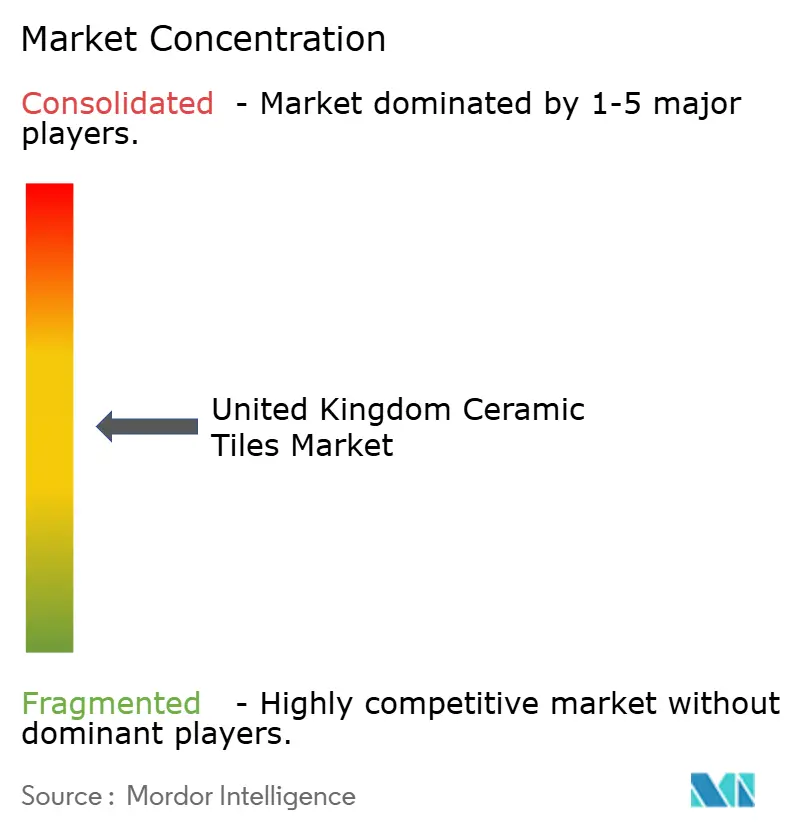

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Ceramic Tiles Market Analysis by Mordor Intelligence

The United Kingdom ceramic tiles market size is expected to grow from USD 1.27 billion in 2025 to USD 1.3 billion in 2026 and is forecast to reach USD 1.49 billion by 2031 at 2.66% CAGR over 2026-2031. Steady renovation activity, the growing preference for large-format porcelain in prestige commercial projects and rising demand for energy-efficient flooring compatible with under-floor heating keep demand resilient even as wider construction indicators soften. Manufacturers are cushioning energy-price headwinds by upgrading kilns and adopting digital printing, which shortens design cycles and cuts waste. Import frictions caused by HGV driver shortages are nudging distributors to hold larger inventories and diversify sourcing, marginally lengthening lead times but preserving supply continuity[1] Source: U.K. Government, “Future Homes Standard and Approved Document L Updates,” gov.uk. Competition from luxury vinyl tile and stone-polymer composite flooring is intensifying price sensitivity in the residential segment, yet ceramic’s durability, low lifecycle cost, and regulatory alignment maintain its value proposition.

Key Report Takeaways

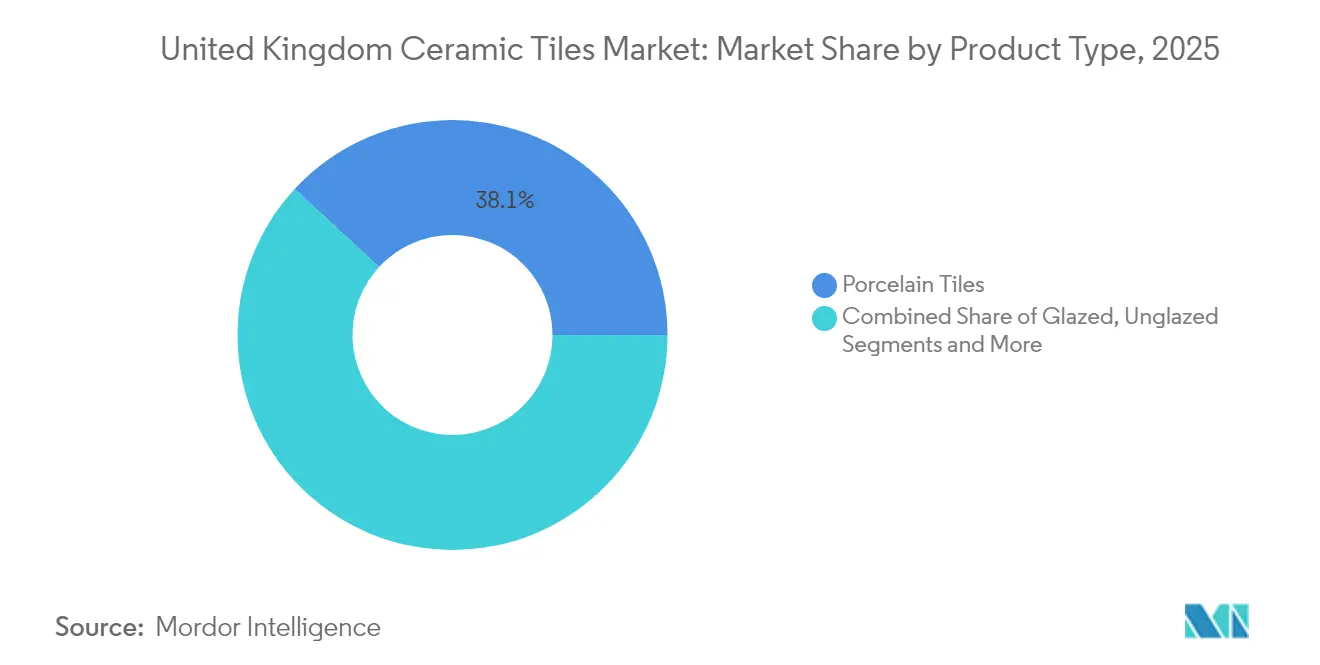

- By product type, porcelain led with 38.12% United Kingdom ceramic tiles market share in 2025, while mosaic tiles posted the fastest 3.04% CAGR through 2031.

- By application, floor installations commanded 62.54% of the United Kingdom ceramic tiles market size in 2025, and wall applications are projected to expand at a 2.94% CAGR to 2031.

- By end-user, residential projects accounted for 61.35% share of the United Kingdom ceramic tiles market size in 2025, as commercial projects registered a 2.39% CAGR outlook to 2031.

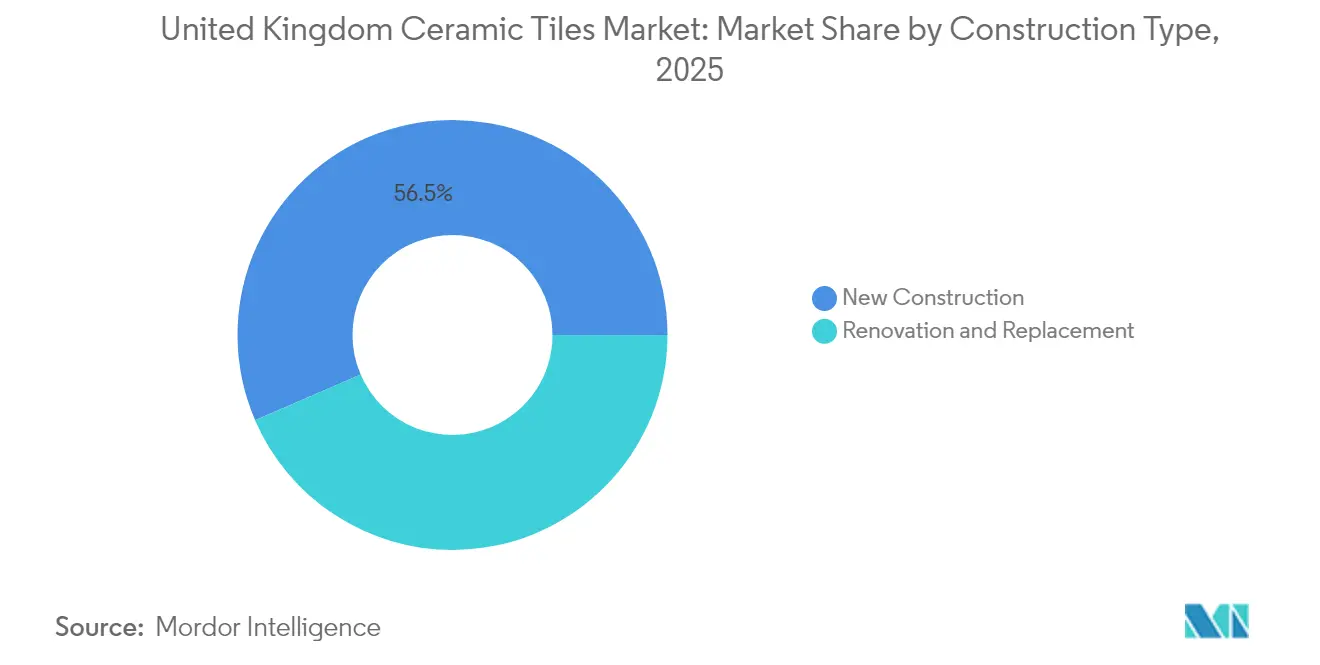

- By construction type, new-build represented 56.48% of the United Kingdom ceramic tiles market activity in 2025, whereas renovation and replacement rose at a 3.12% CAGR over the forecast period.

- By distribution channel, specialty tile stores held a 39.85% share in 2025, and online retail is set to accelerate at a 4.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic home-improvement boom sustains retail tile demand | +0.8% | England and Wales core, spillover to Scotland | Medium term (2-4 years) |

| Surge in large-format porcelain adoption for upscale commercial fit-outs | +0.6% | England metropolitan areas, Scotland urban centers | Long term (≥ 4 years) |

| UK-wide push for energy-efficient under-floor heating compatible tiles | +0.4% | National, with early gains in England, Scotland | Long term (≥ 4 years) |

| Digital ink-jet printing cuts design cycle & cost for niche producers | +0.3% | England manufacturing hubs, Wales production centers | Medium term (2-4 years) |

| Growth of modular off-site construction using lightweight tile panels | +0.2% | England and Scotland construction corridors | Long term (≥ 4 years) |

| Mandatory slip-resistance norms in healthcare & transport hubs | +0.2% | National, concentrated in urban transport networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-pandemic home-improvement boom sustains retail tile demand

Extended periods of home occupancy during 2020–2022 recalibrated household spending toward renovation, a pattern that has endured through 2025 despite macroeconomic uncertainty. Non-food retail volumes tied to home improvement rose 1.9% year-on-year in late 2024, and ceramic retailers with upgraded e-commerce sites captured a disproportionate share of that growth. Consumers increasingly prioritize durable, low-maintenance surfaces that add resale value, positioning ceramic tiles ahead of short-lived laminates in kitchen and bathroom upgrades[2]Source: British Ceramic Confederation, “Ceramic Sector Pathway to Net Zero,” britishceramicconfederation.org.uk. HD ink-jet lines commissioned at Johnson Tiles and British Ceramic Tile enable rapid roll-outs of marble- and wood-look collections that cater to bespoke interior themes. Together, these elements underpin a stable residential demand base that cushions cyclical swings in new-build activity.

Surge in large-format porcelain adoption for upscale commercial fit-outs

Flagship commercial refurbishments, airports, and premium retail chains now routinely specify 1,200 × 600 mm or larger porcelain panels to achieve monolithic aesthetics with lower maintenance outlays. The Gatwick Airport Station redevelopment demonstrated large-format tiles’ ability to handle continuous footfall while simplifying cleaning regimes, reinforcing confidence among architects and facility managers. Hotels upgrading lobbies and spas prefer expansive slabs that emulate natural stone yet comply with hygiene and slip-resistance standards without sealing treatments. Precision-cut edges and minimal grout lines also shorten installation times on high-value projects where shutdown windows are tight. As corporate real-estate owners pursue statement interiors to lure employees back on-site, demand for premium porcelain is forecast to extend well into the next decade.

UK-wide push for energy-efficient under-floor heating compatible tiles

Ceramic tiles’ high thermal conductivity enables faster heat transfer than vinyl or laminate, improving system responsiveness and cutting energy bills by up to 15% in comparative trials. Developers of Build-to-Rent apartments in Manchester and Birmingham specify porcelain floors over hydronic coils to meet EPC B ratings without compromising design flexibility. The British Ceramic Confederation estimates that aligning tile installations with low-temperature heat pumps could abate 120,000 tons of CO₂ annually by 2030. Consequently, cross-trade collaboration among tile makers, adhesive suppliers, and HVAC contractors is deepening to deliver standardized, warrantied flooring packages for mass adoption.

Digital ink-jet printing cuts design cycle and cost for niche producers

Ink-jet heads capable of 400 dpi resolution now replicate veining and texture previously achievable only through screen printing, slashing set-up times from weeks to hours and lowering minimum economic batch sizes. Smaller UK producers leverage this agility to serve boutique orders for hospitality refurbishments without holding large inventories. Color management software further enables rapid tonal tweaks that match interior designers’ palettes, enhancing perceived customization without disrupting process flow. Operating efficiencies partly offset higher kiln energy bills, preserving margins and sustaining domestic production volumes in the face of import competition. The technology’s spillover benefits include reduced ink waste and the ability to incorporate recycled raw materials without color variance penalties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural-gas prices inflating kiln firing costs | -0.9% | National, concentrated in manufacturing regions | Short term (≤ 2 years) |

| Shortage of HGV drivers disrupting imports from Spain & Italy | -0.4% | England and Wales import corridors | Medium term (2-4 years) |

| Competition from LVT & SPC rigid-core flooring alternatives | -0.3% | National, particularly residential segment | Long term (≥ 4 years) |

| Limited domestic clay reserves restricting scale-up of local production | -0.2% | England and Wales production centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile natural-gas prices inflating kiln firing costs

Spot natural-gas quotations more than doubled between late 2021 and mid-2023, inflating ceramic tile production costs because firing at 1,200 °C accounts for roughly 35% of factory operating expenses. The glass, ceramics, and stone sector’s gross value added consequently sank 46.5% from Q1 2021 levels, eroding working capital for capex upgrades. Producers are piloting hybrid kilns that blend biomethane or hydrogen to curb gas dependency, yet commercial deployment remains hampered by infrastructure gaps and funding hurdles[3]Source: St Helens Borough Council, “Glass Futures Low-Carbon Kiln Demonstrator,” sthelens.gov.uk. Energy-cost uncertainty steers some buyers toward import sourcing, though anti-dumping duties on Chinese tiles limit substitution effects and keep domestic capacity relevant. Persistent volatility could delay investment in next-generation presses, slowing product innovation and marginally tempering the United Kingdom ceramic tiles market trajectory.

Shortage of HGV drivers disrupting imports from Spain and Italy

Post-Brexit licensing rules and pandemic-era retirements left the UK short of an estimated 50,000 qualified drivers by late 2024, stretching delivery lead times for pallets arriving via Dover and Felixstowe. Average transit from Castellón, Spain—the EU’s largest tile hub—lengthened to 6.8 days in 2024 versus 5.1 days in 2019, compelling distributors to raise safety-stock holdings. Spot freight charges climbed 14% year-on-year, squeezing margins for independent retailers with limited pricing power. Some wholesalers switched to break-bulk shipping through Liverpool to diversify risk, yet port capacity constraints restrict rapid scaling. The driver deficit is expected to ease gradually as apprenticeship grants and fast-track testing beds are put in place, but structural logistics costs will likely remain above pre-2020 norms over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Tiles Cement Premium Leadership

Porcelain tiles secured 38.12% United Kingdom ceramic tiles market share in 2025 owing to less than 0.5% water absorption, frost resistance, and high breaking strength that suit both external façades and heavy-traffic interiors. The United Kingdom ceramic tiles market size for porcelain reached USD 484.1 million in 2025 and is projected to expand at a 2.78% CAGR through 2031 as format enlargement drives value per square meter. Mosaic tiles, although only 4.6% of volume, register the fastest 3.04% CAGR as bathroom and kitchen designers favor personalized accent walls with recycled-glass mosaics that satisfy sustainability briefs. Glazed ceramic remains the workhorse for residential wall cladding, while unglazed variants dominate safety-critical floors where EN 16165 slip ratings are mandatory in healthcare and transport hubs.

Demand differentials reflect maintenance expectations and installation economics rather than unit price alone. Porcelain’s life-cycle cost advantage over natural marble strengthens its appeal among commercial landlords who amortize interiors across long leases. Mosaic importers lean on just-in-time ordering from Italian producers; however, recent logistics bottlenecks spur interest in UK-made glass mosaics that cut lead times by 40%. Glazed wall tile consumption remains sensitive to fashion cycles, compelling manufacturers to roll out seasonal colorways every six months using agile ink-jet lines.

By Application: Floor Installations Dominate Performance-Driven Demand

Flooring represented 62.54% United Kingdom ceramic tiles market share in 2025 because tiles outlast vinyl by up to 20 years under comparable foot traffic, reducing total facilities-management expense. Wall cladding, while smaller at USD 408.6 million, outpaces with a 2.94% CAGR due to expansion of open-plan living spaces that employ feature walls for zoning purposes. Roofing applications represent a specialized niche focused on traditional clay tiles for heritage and architectural restoration projects, though this segment faces pressure from modern roofing alternatives. The floor segment's dominance reflects ceramic tiles' technical advantages in commercial applications, where lifecycle cost considerations favor materials that withstand heavy use while maintaining aesthetic appeal. Residential floor applications benefit from ceramic tiles' compatibility with underfloor heating systems, aligning with energy efficiency trends that prioritize thermal conductivity and heat retention properties.

Within commercial refurbishments, facility managers increasingly convert carpeted lobbies into large-format porcelain for easier sanitation, a priority highlighted during the pandemic. Residential floors gain additional momentum from the under-floor heating boom, where ceramic rapid heat transfer improves comfort ratings in EPC assessments. Wall tile growth is bolstered by digital influencers showcasing full-height shower enclosures clad in marble-look slabs, spurring retail pickups among millennial homeowners. Installation innovations such as lightweight honeycomb-backed panels reduce structural loads, extending ceramic use to refurbishments previously deterred by weight constraints.

By End-User: Residential Renovation Anchors Growth Momentum

Residential customers held a 61.35% share of 2025 transactions, with the United Kingdom ceramic tiles market size for household upgrades forecast to rise at a 3.01% CAGR to 2031. Work-from-home arrangements have redefined kitchens as multipurpose hubs, prompting higher-spec flooring selections that deliver both aesthetics and resilience against increased wear. Commercial demand, contributing 38.65%, is diversifying beyond retail to healthcare, education, and transport infrastructure, each governed by technical standards that favor ceramic over vinyl composites. Healthcare estates extend porcelain corridors to ensure chemical resistance against stringent cleaning regimens, while universities increasingly retrofit lecture theaters with slip-resistant tiles to comply with accessibility mandates.

Consumer attitudes in the residential arena lean toward investments that elevate property valuations amid a cooling housing market, sustaining expenditure on durable finishes despite tighter mortgage lending. Government support for decarbonizing public buildings funnels grants into ceramic-based refurbishment packages consistent with net-zero pathways. Facility managers deploy ceramics strategically to cut life-cycle maintenance, an imperative when custodial budgets face inflationary pressure on labor. In hospitality, a rebound in occupancy rates revives capex for lobby and bathroom upgrades where marble-effect porcelain delivers luxury perception without porous surface drawbacks.

By Construction Type: Renovation Demand Outpaces New-Build Growth

New construction generated 56.48% of tile placements in 2025, yet renovation is projected to record the sharper 3.12% CAGR through 2031 as the United Kingdom’s aging building stock demands upgrades. Government data show that more than 3.8 million dwellings predate 1945, many of which undergo phased modernization that includes energy-efficient floor finishes. Declines in speculative housing starts during 2023-2024 shifted installer capacity toward bathroom and kitchen remodels that typically specify mid-range porcelain. Commercial landlords embark on façade refits to comply with Minimum Energy Efficiency Standards, often integrating ventilated porcelain cladding panels that improve thermal performance.

Renovation campaigns frequently combine surface replacement with under-floor heating retrofits, compounding tile volumes per project compared with cosmetic-only upgrades. Heritage conversions employ handmade clay tiles to satisfy conservation officers, sustaining artisanal production lines in Shropshire and Devon. Modular off-site extensions prefabricated with lightweight porcelain panels shorten on-site schedules, appealing to logistics-challenged city-center plots. Energy-efficiency subsidies such as the Boiler Upgrade Scheme indirectly boost demand because occupants often coordinate heating upgrades with new tile floors. The convergence of sustainability incentives and demographic shifts toward stay-in-place aging supports a stable, renovation-led outlook for the United Kingdom ceramic tiles market.

By Distribution Channel: Digital Transformation Redefines Sales Mix

Specialty tile and stone stores retained 39.85% channel share in 2025 thanks to in-store design advice and sample libraries that guide technical product selection. Online platforms, while only 12.05% today, advance at a 4.07% CAGR as logistics networks and augmented-reality visualization tools overcome the tactile gap in remote purchasing. Home-improvement warehouses such as B&Q and Wickes serve price-sensitive DIY customers, yet even they integrate click-and-collect features that blend digital convenience with physical verification. Direct-to-contractor agreements streamline procurement on large commercial jobs, with platforms offering bundled pricing that includes adhesives and grouts delivered on synchronized schedules. Showrooms like Domus Clerkenwell merge immersive displays with tablet-based configurators, illustrating the omnichannel future of tile retailing.

Specialty retailers defend margins by offering project management services and accredited installer referrals, differentiating against pure-play e-commerce rivals focused on volume. Online marketplaces widen geographic reach for boutique brands, exposing rural consumers to premium Italian porcelain formerly confined to London showrooms. Integrated stock-management APIs enable real-time availability checks that reduce abandoned carts due to back-order risk. Freight surcharges linked to driver shortages challenge free-delivery promotions, prompting platforms to experiment with micro-fulfillment nodes near urban centers.

Geography Analysis

England accounted for 63.55% of 2025 revenue as London’s high-density residential conversions and corporate headquarters refurbishments maintain premium tile uptake. The region's market leadership reflects its economic concentration, with London and surrounding metropolitan areas generating substantial demand for both residential renovation projects and commercial installations. Scotland delivered the fastest regional 3.45% CAGR propelled by affordable-housing completions under the Scottish Government’s Housing 2040 strategy, coupled with Glasgow’s initiative to retrofit public buildings for net-zero compliance. Wales, contributing 6.86% share, relies mainly on residential renovations in Cardiff and Swansea, moderated by a limited pipeline of large commercial projects. Northern Ireland remains the smallest at 3.76% share, constrained by lower disposable incomes and cautious real-estate investment sentiment.

Regional construction cultures influence product mix: London architects specify extra-large porcelain slabs for landmark lobbies, whereas Edinburgh housing associations prioritize cost-effective glazed ceramic for mid-rise apartment corridors. England’s established installer base supports complex façade jobs, while Scotland’s growth is tilted toward new-build residential where tile volumes per unit are lower but rising. Logistics cost disparities shape pricing; tiles landed at Felixstowe reach Birmingham warehouses 8% cheaper than deliveries routed via Cairnryan to central Scotland. Climate variables also play a role as porcelain’s frost resistance is a selling point in the Scottish Highlands, whereas lighter-weight ceramic dominates London high-rise interiors where load limits apply. Across all nations, government retrofit funding aligns with decarbonization deadlines, embedding a steady undercurrent of demand through 2030.

Urban centers lead specification trends that ripple outward; Manchester’s Ancoats district popularized concrete-look porcelain now stocked nationwide, and Glasgow’s Merchant City adoption of terrazzo-inspired slabs is influencing Northern English showrooms. England’s renovation emphasis sustains artisanal clay-tile producers along the Staffordshire Potteries, protecting regional employment and heritage skills. Scotland’s public-sector building drive integrates slip-resistant stoneware in transport interchanges, supporting local distributors that specialize in technical grades. Welsh tourism growth fuels hospitality refurbishments along the Pembrokeshire Coast, whose operators favor easy-clean porcelain to withstand sand ingress. Northern Ireland’s modest but stable market hinges on subsidy-supported social housing upgrades where value engineering determines material selection.

Competitive Landscape

The United Kingdom ceramic tiles market hosts a moderately fragmented roster where the top five players hold major market share in 2024. Spanish-headquartered Porcelanosa leads online brand visibility, translating digital reach into showroom traffic across London, Chelsea, and Watford outlets. RAK Ceramics capitalizes on a UK distribution center in Northamptonshire guarantees 48-hour delivery of 3 mm slim-slab panels destined for office retrofits. Mohawk-owned Marazzi leverages vertically integrated logistics to mitigate freight volatility, while Johnson Tiles uses domestic production flexibility to win short-lead hospitality jobs. British Ceramic Tile’s investment in advanced ink-jet lines positions it to supply bespoke backsplash collections for national kitchen retailers, reinforcing domestic share against Italian imports.

Strategic moves increasingly center on sustainability: Mohawk is trialing kiln electrification powered by renewable PPAs, and RAK Ceramics announced a recycled-water loop that cuts process consumption by 30%. Anti-dumping duties of 14%–70% on small-format Chinese tiles remain in force through 2026, granting European producers a price umbrella that underwrites investments in low-carbon manufacturing. Companies differentiate through value-added services such as BIM-ready product libraries that expedite specification on government projects requiring digital twins. Collaboration with adhesive specialists like Mapei yields system warranties prized by facility managers seeking single-point accountability for tiled assemblies. Digital marketing, particularly augmented-reality room viewers, has become table stakes, with Porcelanosa reporting a 37% conversion uplift among users engaging its 3D visualizer before showroom visits.

M&A activity remains selective; larger groups eye niche mosaic makers to capture decorative margins, while family-owned clay-roof-tile firms attract private-equity interest due to stable restoration demand. Supply-chain partnerships extend to logistics, where consortia of manufacturers co-load trailers to optimize scarce HGV capacity and reduce per-pallet cost amid driver shortages. Innovation pipelines are rich with photocatalytic, NOx-reducing glaze technologies that promise indoor air-quality benefits sought in post-pandemic office refurbishments. Start-ups developing AI-driven defect-inspection cameras attract venture capital, aiming to lift first-pass yield and shrink energy intensity per usable square meter. Overall, the competitive theater balances economies of scale with design agility, ensuring that both international giants and local specialists retain well-defined competitive moats through 2030.

United Kingdom Ceramic Tiles Industry Leaders

Prism Johnson Ltd.

Porcelanosa Grupo

Ceramica Marazzi

CTD Tiles

Mohawk Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: British Ceramic Tile invested GBP 1.3 million (USD 1.7 million) in HD ink-jet equipment to accelerate marble-look launches and cut design-to-market lead time to four weeks.

- February 2024: British Ceramic Tile invested GBP 1.3 million (USD 1.7 million) in HD ink-jet equipment to accelerate marble-look launches and cut design-to-market lead time to four weeks.

- March 2024: Domus opened a 12,000 ft² immersive showroom in Clerkenwell integrating VR visualization pods for architects specifying tiles on commercial schemes.

- October 2024: The Trade Remedies Authority upheld anti-dumping tariffs on Chinese ceramic tiles sized ≤ 3,600 cm², maintaining rates between 14% and 70% until 2026.

United Kingdom Ceramic Tiles Market Report Scope

Ceramic Tiles are made up of sand, natural products, and clays and once it is moulded into a shape then they are fired into a kiln. Ceramic tiles are durable, resistant to water, moisture and fire and are cheap as compared to other flooring products. United Kingdom Ceramic Tiles Market is segmented By Product (Glazed, Porcelain, Scratch Free, Other Products), By Application (Floor Tiles, Wall Tiles, Other Applications), By Construction Type (New Construction, Replacement, and Renovation) and By End User (Residential, Commercial).

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the current value of the United Kingdom ceramic tiles market?

The market is valued at USD 1.3 billion in 2026 and is projected to grow to USD 1.49 billion by 2031 at a 2.66% CAGR.

Which product category leads sales within the United Kingdom ceramic tiles space?

Porcelain tiles dominate with a 38.12% share because of their low water absorption, high strength, and versatility in both residential and commercial projects.

How fast is online retail for ceramic tiles expanding across the United Kingdom?

E-commerce sales are advancing at a 4.07% CAGR as virtual showrooms, AR tools, and faster delivery options encourage remote purchasing.

Why are ceramic tiles preferred for under-floor heating installations?

Tiles’ high thermal conductivity and durability optimize heat transfer, helping buildings meet tighter energy-efficiency standards under Approved Document L.

Which U.K. region shows the quickest rise in ceramic tile demand?

Scotland records the fastest 3.45% CAGR, driven by infrastructure spending and energy-efficient residential developments backed by devolved government policies.

Page last updated on: