Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

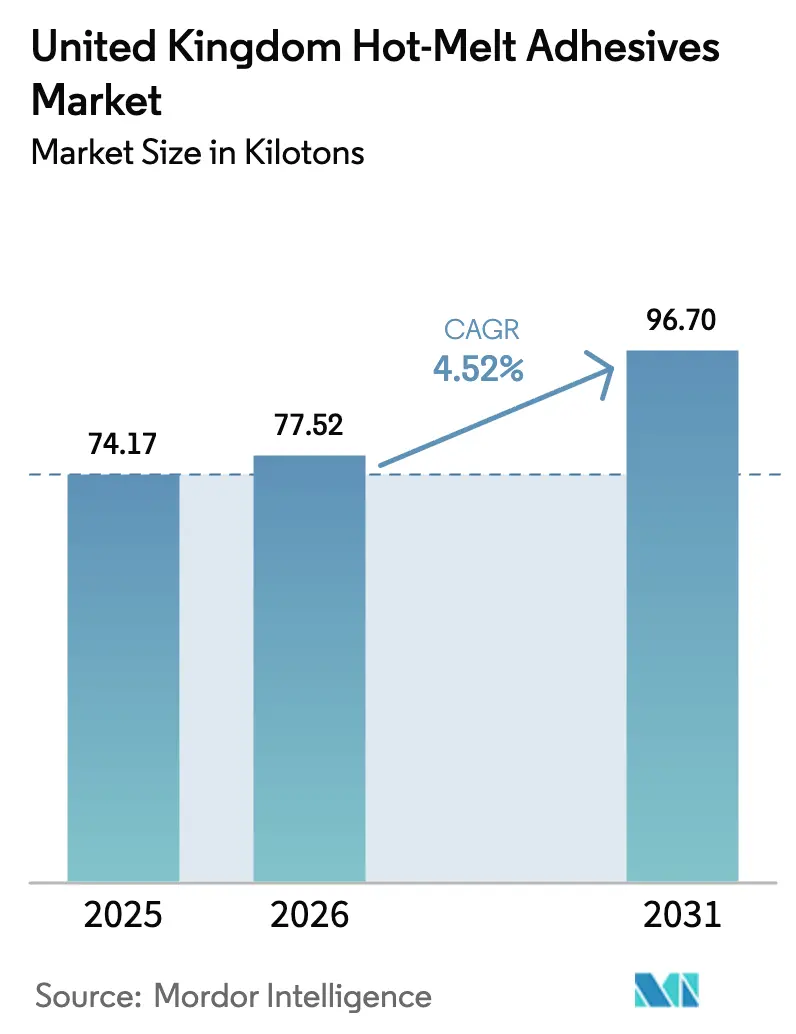

| Base Year Market Size (2025) | 74.17 kilotons |

| Market Volume (2026) | 77.52 kilotons |

| Market Volume (2031) | 96.70 kilotons |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Hot-Melt Adhesives Market Analysis by Mordor Intelligence

The United Kingdom Hot-Melt Adhesives Market size is expected to increase from 74.17 kilotons in 2025 to 77.52 kilotons in 2026 and reach 96.70 kilotons by 2031, growing at a CAGR of 4.52% over 2026-2031. As e-commerce parcel traffic surges and the Plastic Packaging Tax takes effect, converters are pivoting towards bio-derived and water-compatible chemistries. These choices not only support substrates with recycled content but also maintain production line speeds. This shift is particularly evident in corrugated and flexible-film lines, which are now opting for lower-temperature, faster-curing resins to avoid bottlenecks. This transition has been made possible by advancements in metallocene polyolefin technology. At the same time, a decline in automotive output and tightening limits on diisocyanate exposure are pressuring legacy polyurethane demand. However, sectors such as modular construction and medical devices are emerging as stabilizing volume pockets. Currently, suppliers find a competitive edge not only in selling adhesives but also in bundling formulation expertise, dispensing equipment, and regulatory insights.

Key Report Takeaways

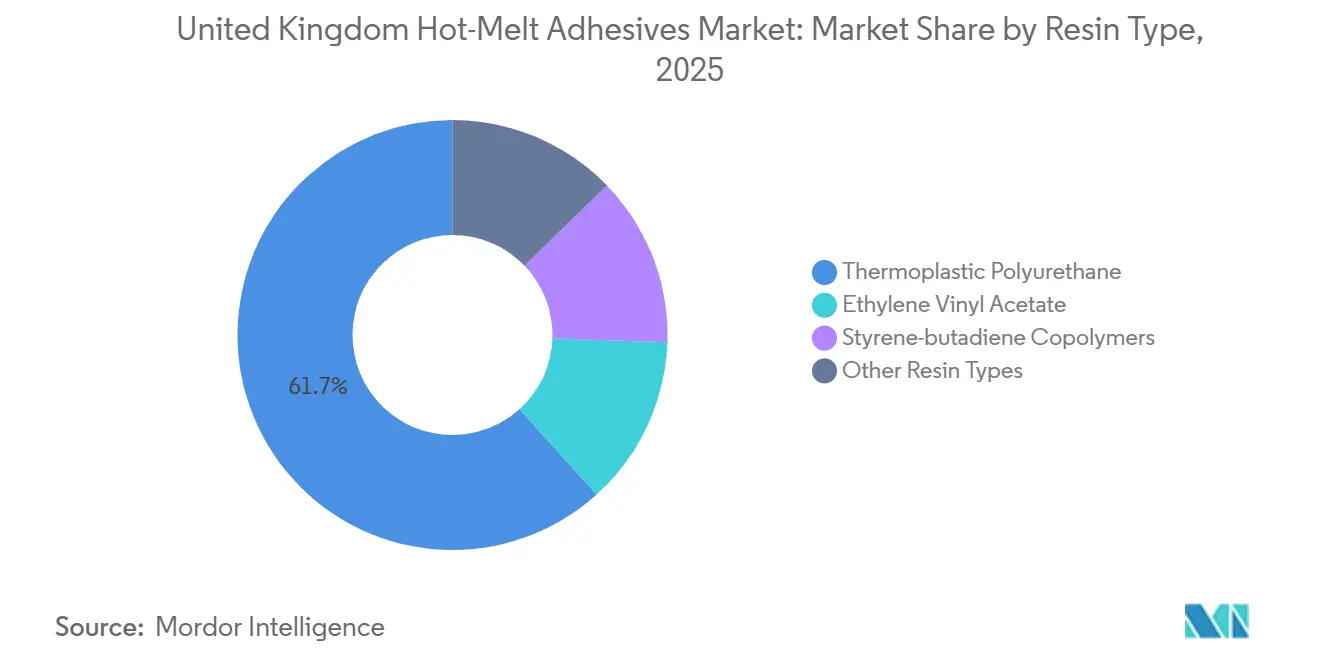

- By resin type, thermoplastic polyurethane captured 61.69% of the United Kingdom hot-melt adhesives market share in 2025, whereas styrenic-butadiene copolymers are forecast to post the fastest 5.78% CAGR through 2031.

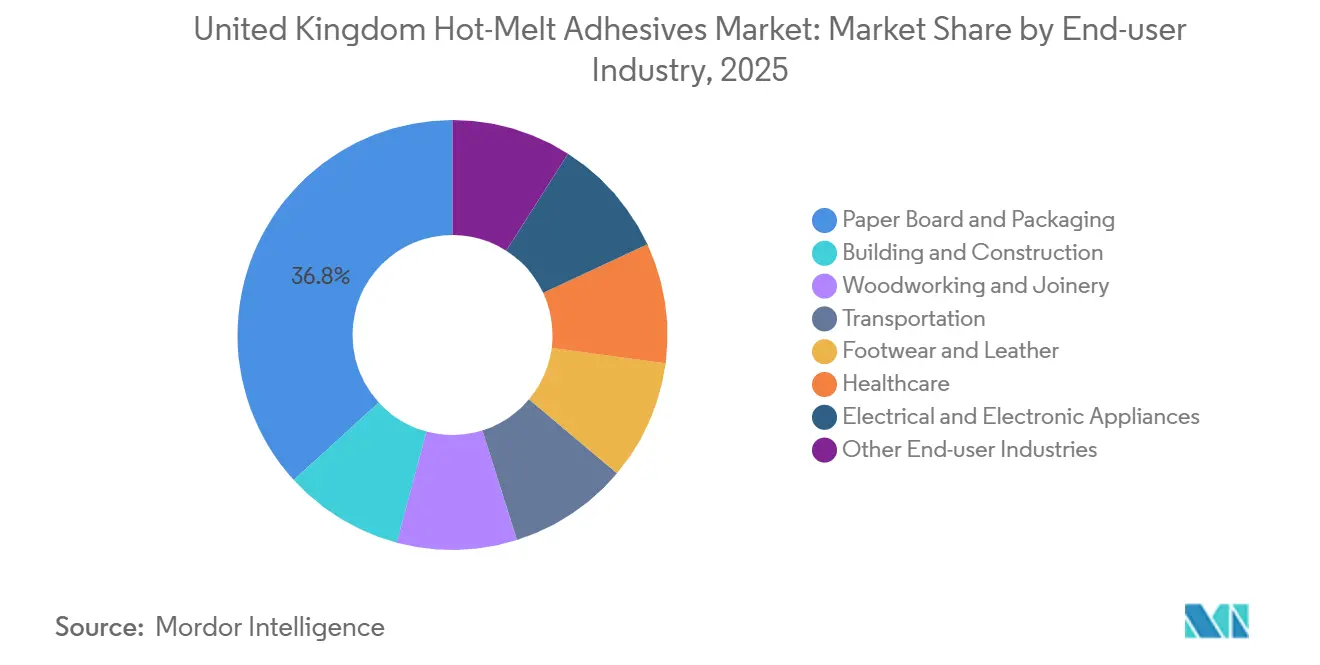

- By end-user Industry, paper board and packaging held 36.78% of volume in 2025 and is expected to advance at a 5.09% CAGR during 2026-2031, outpacing all other end-user segments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Hot-Melt Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce packaging boom post-Brexit | +1.20% | National, strongest in Southeast distribution hubs | Short term (≤ 2 years) |

| UK Plastic Packaging Tax pushes recyclable adhesives | +0.90% | National, early adopters in London, Manchester, Birmingham | Medium term (2-4 years) |

| Low-temperature metallocene HMA adoption | +0.60% | National, led by food and beverage packers | Medium term (2-4 years) |

| Surge in off-site modular construction | +0.50% | National, pronounced in Scotland and Northern England | Long term (≥ 4 years) |

| NHS shift to solvent-free medical devices | +0.30% | National, procurement-driven via NHS Supply Chain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

UK Plastic Packaging Tax Pushes Recyclable Adhesives

In 2024, a significant portion of the registered tonnage claimed an exemption from the levy on packaging with less than 30% recycled content. However, compliance is tightening with the certification mandate set for April 2027. Formulators are now ensuring that adhesive residues separate in float-sink tanks at temperatures below 60 degrees Celsius, a requirement that eliminates many high-crosslink EVA grades. Henkel, highlighting a shift toward solutions compatible with existing lines and maintaining recyclability, has introduced bio-attributed drop-in alternatives certified under ISCC PLUS. As the levy adjusts with inflation, the cost disparity between virgin and recycled substrates is expected to grow, solidifying recyclability as a key criterion in adhesive selection within the United Kingdom hot-melt adhesives market.

Low-Temperature Metallocene HMA Adoption

Metallocene-catalyzed polyolefin hot melts bond at lower temperatures than conventional EVA, saving energy and allowing the use of heat-sensitive labels without distortion. These lower bonding temperatures also reduce cool-down dwell time, enabling increased line speed without extra applicators. This is particularly beneficial for beverage plants aiming for sustainability. Additionally, strong peel adhesion on non-polar films allows converters to reduce coat weight, cutting emissions and material costs. With rising electricity tariffs, these practices have seen increased adoption, leading to tangible paybacks and enhancing the technology's appeal in the United Kingdom hot-melt adhesives market

Surge in Off-Site Modular Construction

Off-site timber and light-steel modules significantly cut on-site labor, a benefit given the United Kingdom's skilled trades shortage. In controlled factory settings, hot melts swiftly bond oriented strand board (OSB) sheathing to studs, achieving faster line takt times than nailed assemblies. SikaMelt grades, favored for their gap-filling and thermal cycling accommodation, are popular among social housing builders in Scotland. While planning-permission delays have moderated growth, the rising trend of modular builds suggests sustained demand for high-performance grades in the United Kingdom hot-melt adhesives market

NHS Shift to Solvent-Free Medical Devices

NHS Supply Chain advocates for the use of VOC-free adhesives to reduce staff exposure during medical device assembly and sterilization[1]Medicines and Healthcare Products Regulatory Agency, “Medical Devices Guidance,” gov.uk . Hot-melt pressure-sensitive adhesives, which bypass a lengthy outgassing period, are expediting lead times for ostomy and wound care products. 3M has rolled out acrylate-free products to tackle allergen issues, but their uptake is limited to high-acuity applications due to a price premium. Nonetheless, this policy guarantees a steady demand for biocompatible chemistries in the United Kingdom hot-melt adhesives market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled applicator shortage for automation | -0.70% | National, acute in Midlands and Northeast | Short term (≤ 2 years) |

| UK REACH-style limits on isocyanates | -0.50% | National, enforced by HSE | Medium term (2-4 years) |

| Sluggish domestic auto production | -0.40% | West Midlands, Sunderland, Ellesmere Port | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Applicator Shortage for Automation

In the United Kingdom, apprenticeships are falling short, producing fewer certified technicians than the hot-melt adhesive sector demands. As a result, converters are turning to manual guns, which leads to increased adhesive waste and a rise in defect rates. Although the IoT-enabled melters with predictive maintenance provide some assistance, they cannot replace the need for hands-on problem-solving on the shop floor. Without an enhancement in technical college curricula, this talent gap continues to hinder productivity in the United Kingdom's hot-melt adhesives market.

UK REACH-Style Limits on Isocyanates

New HSE regulations, which took effect in August 2023, require facilities dealing with products containing significant amounts of free MDI to invest in training and respirators, leading to increased compliance costs[2]Health and Safety Executive, “Diisocyanates,” hse.gov.uk . Smaller toll blenders, unable to invest in retrofitted ventilation, are stepping back from reactive polyurethane grades, unintentionally increasing demand for larger multinationals. While quasi-prepolymer alternatives are available, they may jeopardize early green strength, making them less desirable for industries such as footwear and transport interiors in the United Kingdom's hot-melt adhesives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Performance Versus Cost Trade-Offs Shape Adoption

In 2025, thermoplastic polyurethane captured 61.69% of the United Kingdom hot-melt adhesives market, due to its unique combination of flexibility, abrasion resistance, and bond strength. These qualities make it a preferred choice for diverse applications, including automotive interiors, footwear, and high-barrier film lamination. Huntsman’s IROGRAN grades, designed for broad spray applications in laminations, feature melt viscosities dropping below 10,000 cP at 180°C. Ethylene-vinyl acetate, traditionally favored for carton sealing due to its cost-effectiveness, is losing ground as converters turn to faster-curing and lower-temperature options. Styrenic-butadiene copolymers, set to grow at a 5.78% CAGR through the forecast period of 2026-2031, are closing in on polypropylene labels, especially in applications prioritizing peel strength and recyclability. With brand owners shifting towards mono-material flexible packs, the demand for styrenic-butadiene copolymers in the United Kingdom hot-melt adhesives market is increasing, particularly for adhesives that preserve the integrity of polyethylene streams.

Converters, facing margin pressures, are increasingly exploring hybrid blends that merge thermoplastic polyurethane with polyolefin elastomers, achieving a balance between cost and performance. Covestro’s bio-attributed Desmomelt line aligns with sustainability objectives and offers thermal stability, but its uptake is limited to original equipment manufacturers (OEMs) ready to pay a premium. While polyamide grades still lead in high-temperature textiles, metallocene polyolefins are gaining traction, especially where energy efficiency on the production line is prioritized over the conventional 120°C service temperature. Today's resin choices are influenced by taxation and recyclability factors, highlighting that the future of the United Kingdom hot-melt adhesives market will hinge more on formulation science than on pricing alone.

By End-User Industry: Packaging Dominates While Healthcare Accelerates

In 2025, paper board and packaging accounted for 36.78% of the volume and are projected to grow at a CAGR of 5.09% through the forecast period of 2026-2031. This growth is closely tied to the e-commerce boom, the rising popularity of ready-meal trays, and a significant shift from metal staples to adhesive closures, which boost recycling efficiency. Hot-melt systems, offering energy savings over water-based ones, also maximize floor space, enabling the addition of more converting lines. The building and construction sector benefits from modular prefab, though regional permitting inconsistencies can temper national averages. In woodworking, there's a shift towards instant-cure edge-banding on CNC routers to enhance production throughput.

While transportation demand mirrors automotive output, niche areas like aftermarket repairs and EV battery potting demonstrate resilience. Footwear manufacturers opt for TPU in sole bonding for durability during repeated flex cycles, and premium safety-boot producers invest in its extended longevity. The healthcare sector, though smaller in volume, commands premium pricing. NHS frameworks, with a focus on ISO 10993 compliance, limit the vendor pool, often favoring multinationals. These diverse dynamics showcase how end-use diversification buffers against cyclical fluctuations, driving growth in the United Kingdom hot-melt adhesives market.

Geography Analysis

London and the Southeast, pivotal to the nation's consumption, utilize dense packaging lines to serve both domestic and continental markets via Channel ports. The Midlands, once dominated by the automotive sector, is now branching into packaging and construction adhesives, even as OEM volumes wane. Regional technical clusters ensure that formulation expertise remains rooted locally. In Northern England, hygiene-product facilities in Manchester and West Yorkshire, bolstered by regional demographics, consistently tap into non-woven bonding grades, strengthening the UK's hot-melt adhesives market.

Scotland's burgeoning modular-housing sector fuels demand for moisture-resistant grades, with Glasgow distributors maintaining buffer stock to sidestep ferry delays. While Wales's contribution is modest, Cardiff's food-processing sector is pivoting its fast-moving consumer-goods packaging to metallocene polyolefin, targeting energy savings. Northern Ireland, navigating dual compliance documentation under the Windsor Framework and aligning with EU rules, feels only a slight volume impact due to its limited industrial base.

The pound's depreciation against the euro has increased resin import costs, leading formulators to hedge against currency swings and prompting consolidations among smaller blenders. Amidst this landscape, multinational suppliers with UK facilities are increasingly bringing compounding processes in-house. This strategy not only mitigates customs delays for customers but also highlights a shift towards locally produced, globally certified materials in the United Kingdom hot-melt adhesives market.

Competitive Landscape

The United Kingdom hot-melt adhesives market is moderately consolidated. Major players such as Henkel, HB Fuller, 3M, Arkema, and Avery Dennison Corporation command a substantial volume share in the United Kingdom hot-melt adhesives market. Field-service teams, skilled in fine-tuning nozzle angles and melt-tank temperatures, forge robust customer relationships, a challenge for standalone resin vendors. Patent filings spotlight moisture-cure systems with less than 0.08 percent free MDI, underscoring the industry's sprint to meet HSE regulations without sacrificing structural integrity.

Mid-tier players such as Jowat UK, strategically located near Midlands packaging hubs, guarantee swift sample turnarounds, a speed that eludes some multinationals. However, the necessity for ventilation-capex and compliance reporting skews advantages towards larger firms, igniting talks of private-equity roll-ups that could merge several specialists into a dominant national player.

Technology stands as the industry's frontier. HB Fuller’s TEC Connect melters, which relay pressure and temperature data to the cloud, promise predictive downtime savings, securing contracts even at premium rates. Simultaneously, Dow’s metallocene products not only enhance line speeds but also spotlight resin innovation as a driver for lucrative bundled agreements. As sustainability audits gain traction, suppliers equipped with ISCC PLUS documentation and application know-how are set to eclipse commodity importers, underscoring a quality-centric trend in the UK's hot-melt adhesives market.

United Kingdom Hot-Melt Adhesives Industry Leaders

Arkema

3M

Avery Dennison Corporation

HB Fuller Company

Henkel AG & Company KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Henkel and Dow have expanded their partnership to accelerate decarbonization in adhesive manufacturing. Henkel will incorporate low-carbon feedstocks and renewable electricity into its hot melt adhesive production, reducing the product carbon footprint by 20 to 40 percent, depending on the product line.

- August 2025: Henkel has introduced Technomelt EM 335 RE, a hot melt adhesive specifically developed to address the shortcomings of conventional hot melt adhesives and ensure the clean separation of labels from PET bottles.

United Kingdom Hot-Melt Adhesives Market Report Scope

Hot-melt adhesives are generally composed of 100% solid components. The hot melts are sold in a solid state at room temperature and are activated by heating beyond their softening point. After melting, an adhesive may be applied to the substrate in a liquid state. The hot melt coats the substrate, penetrating the surface, and then solidifies to ensure uniformness. It takes very little time for this setting and cooling process.

The United Kingdom Hot-Melt Adhesives Market is segmented by resin type and end-user industry. By resin type, the market is segmented into thermoplastic polyurethane, ethylene vinyl acetate, styrene-butadiene copolymers, and other resin types. By end-user industry, the market is segmented into building and construction, paper board, and packaging, woodworking and joinery, transportation, footwear and leather, healthcare, electrical and electronic appliances, and other end-user industries. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

By Resin Type

| Thermoplastic Polyurethane |

| Ethylene Vinyl Acetate |

| Styrene-butadiene Copolymers |

| Other Resin Types |

By End-user Industry

| Building and Construction |

| Paper Board and Packaging |

| Woodworking and Joinery |

| Transportation |

| Footwear and Leather |

| Healthcare |

| Electrical and Electronic Appliances |

| Other End-user Industries |

| By Resin Type | Thermoplastic Polyurethane |

| Ethylene Vinyl Acetate | |

| Styrene-butadiene Copolymers | |

| Other Resin Types | |

| By End-user Industry | Building and Construction |

| Paper Board and Packaging | |

| Woodworking and Joinery | |

| Transportation | |

| Footwear and Leather | |

| Healthcare | |

| Electrical and Electronic Appliances | |

| Other End-user Industries |

Key Questions Answered in the Report

What volume growth is projected for the United Kingdom hot-melt adhesives market through 2031?

The United Kingdom hot-melt adhesives market size stands at 77.52 kilotons in 2026, and it is projected to reach 96.70 kilotons by 2031 at a 4.52% CAGR.

Which resin commands the largest share today?

Thermoplastic polyurethane leads with 61.69% share thanks to its superior flexibility and bonding strength.

How is the Plastic Packaging Tax influencing adhesive formulation?

It is accelerating the shift toward bio-attributed and recycling-compatible hot-melts that avoid contaminating polyethylene and polypropylene streams.

Why are metallocene polyolefin hot-melts gaining traction?

They bond at 90-110°C, cut energy use by about 30%, and enable higher line speeds without damaging heat-sensitive films.

Which end-user sector is expected to grow the fastest?

Paper board and packaging is projected to post a 5.09% CAGR through 2031, driven by sustained e-commerce parcel volumes.

Page last updated on: