Hygiene Adhesives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.51 Billion |

| Market Size (2031) | USD 4.39 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

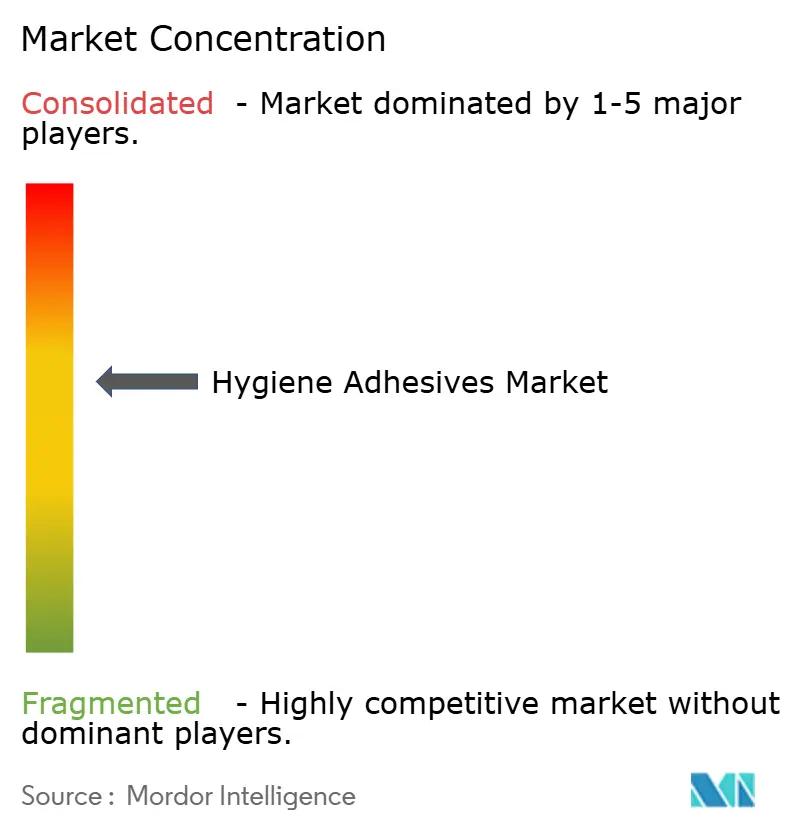

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hygiene Adhesives Market Analysis by Mordor Intelligence

Hygiene Adhesives Market size in 2026 is estimated at USD 3.51 billion, growing from 2025 value of USD 3.36 billion with 2031 projections showing USD 4.39 billion, growing at 4.55% CAGR over 2026-2031. This expansion is driven by population aging in developed economies, rising middle-class purchasing power in Asia, and stricter regulations on volatile organic compound emissions, which encourage a shift from petroleum-based resins to bio-based chemistries. Rapid diaper line speeds exceeding 1,000 pieces per minute are driving demand towards ultra-fast-curing hot-melt technologies. Meanwhile, circular-economy regulations in Europe and Japan are creating niches for washable diaper shells and hybrid pads bonded with low-odor, reusable adhesives. Producers continue to balance feedstock cost volatility against the need for higher heat resistance, driving adoption of styrene-ethylene-butadiene-styrene (SEBS) in premium adult and baby products. Regional supply chains are also localizing as manufacturers seek tariff protection and lower freight expenses, especially across China, India, and Southeast Asia. Finally, bio-based polyurethane hot-melts that meet ISO 14855 biodegradability requirements are starting to win pilot orders from premium brands that can absorb the current 20%–30% price premium.

Key Report Takeaways

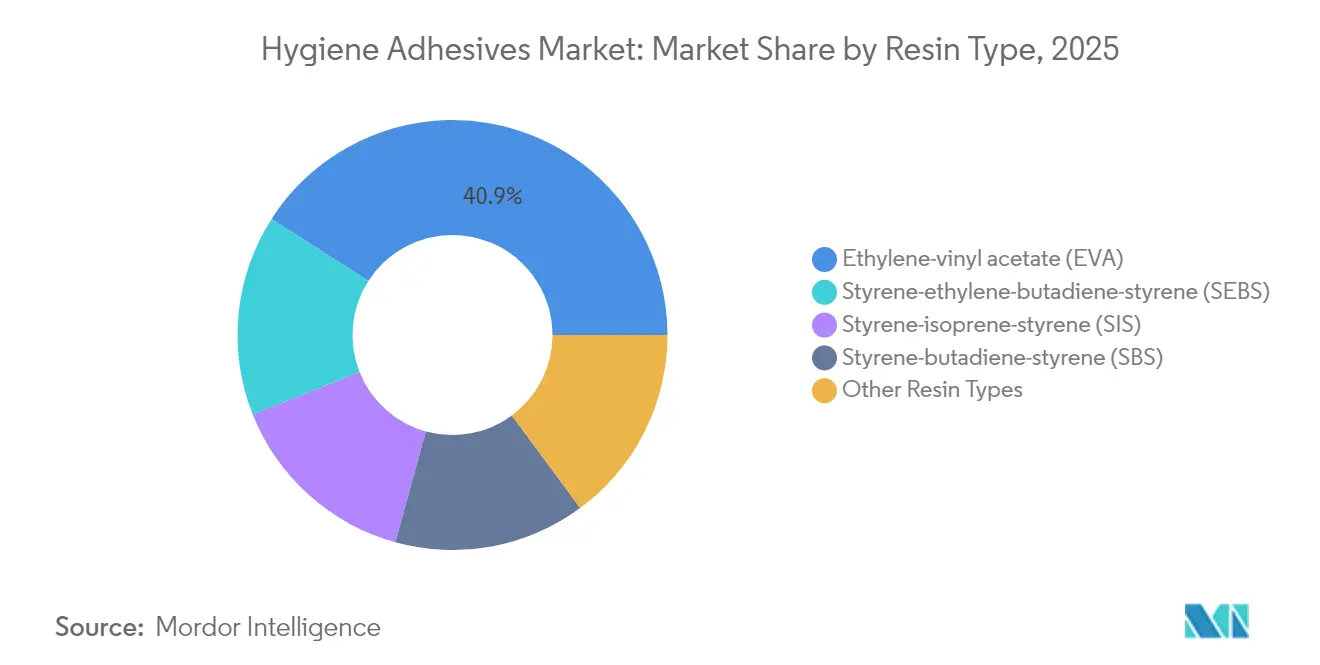

- By resin type, ethylene-vinyl acetate held 40.92% of the hygiene adhesives market share in 2025; SEBS is forecast to grow at a 6.12% CAGR through 2031.

- By product type, non-woven applications captured 66.88% of the hygiene adhesives market size in 2025, while woven substrates are projected to advance at a 5.62% CAGR through 2031.

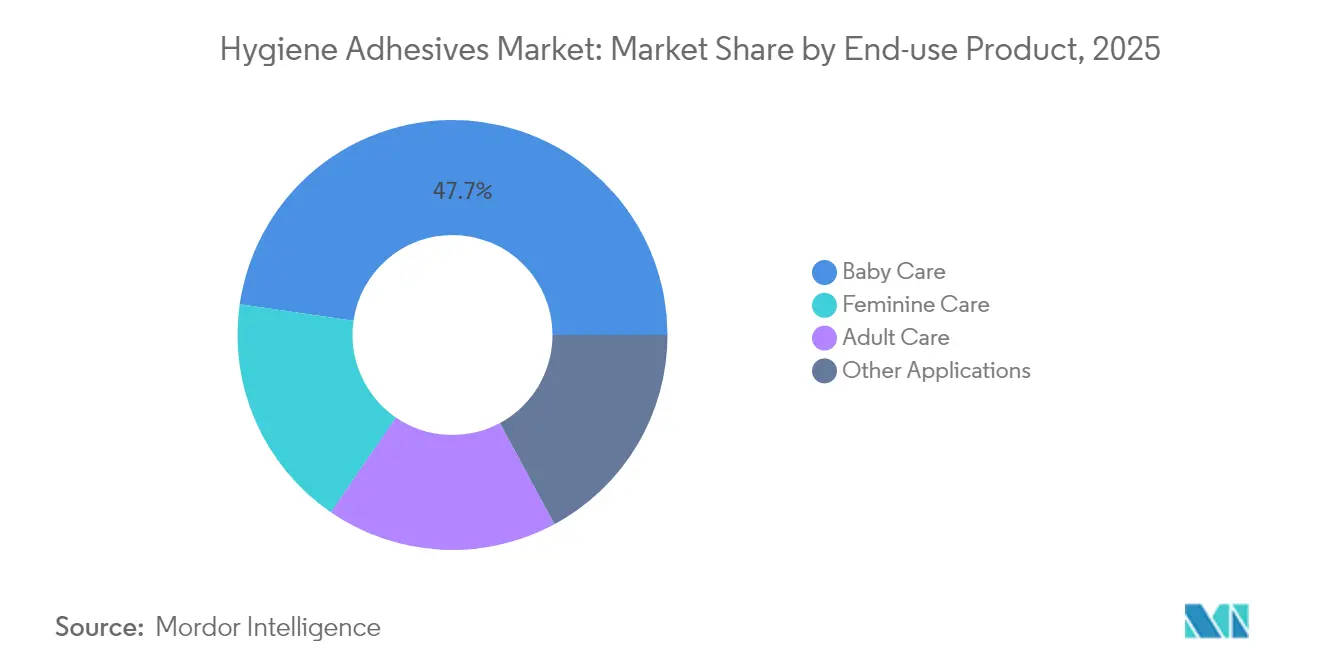

- By end-use product, baby care led with 47.72% revenue share in 2025; feminine care is projected to expand at a 6.04% CAGR through 2031.

- By region, the Asia-Pacific commanded a 46.10% share of the hygiene adhesives market size in 2025, whereas the Middle East and Africa are growing at the fastest rate, with a 5.74% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Hygiene Adhesives Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of disposable baby diapers worldwide | +1.2% | Global, with concentration in APAC (China, India, ASEAN) and emerging MEA markets | Medium term (2-4 years) |

| Accelerating feminine hygiene adoption in emerging Asia | +1.5% | India, Indonesia, Vietnam, Philippines; spill-over to Sub-Saharan Africa | Short term (≤ 2 years) |

| Aging populations boosting adult-incontinence demand | +1.0% | Japan, Germany, Italy, South Korea; North America (United States, Canada) | Long term (≥ 4 years) |

| Sustainability push toward low-VOC and bio-based chemistries | +0.8% | Europe (Germany, France, Nordics), North America; regulatory influence spreading to APAC | Medium term (2-4 years) |

| Automation need for ultra-fast-setting hot-melt systems | +0.6% | Global, led by high-volume manufacturers in China, United States, Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Consumption of Disposable Baby Diapers Worldwide

China’s diaper penetration climbed from 81.5% in 2021 to 89% in 2023, and parents are trading up to thinner, hypoallergenic designs that rely on advanced SEBS-based elastic adhesives[1]China Diaper Association, “T/CPA 005-2024 Quality Standard,” chinadiaper.org. Although the adhesive weight per diaper is falling by roughly 30% compared to 2020 designs, the value per unit is rising because premium elastic systems carry 15%–20% price increases. Multinationals such as Procter & Gamble and Unicharm have localized production to reduce tariffs and freight time, which allows regional formulators to co-develop tailored grades. Extended-wear and overnight products further drive demand for moisture-resistant construction adhesives that retain bond strength under sustained exposure to liquids. The baby segment, therefore, remains the single largest volume outlet for the hygiene adhesives market despite slower birth rates in East Asia.

Accelerating Feminine Hygiene Adoption in Emerging Asia

India’s sanitary-pad sales are expected to expand from USD 1.5 billion in 2024 to USD 3.0 billion by 2030, driven by the 2018 removal of a 12% goods and services tax and public-sector distribution in rural districts, where pad usage stood at only 33.5%. Rising demand translates into higher construction-adhesive volumes to bond super-absorbent cores and into pressure-sensitive grades for wings. Suppliers are prioritizing low-odor, ISO 10993-compliant chemistries to mitigate skin-irritation complaints and capture market share among first-time users. State mandates for compostable pads in parts of India, Indonesia, and the Philippines are stimulating R&D in bio-based hot-melts derived from plant oils and starches that disintegrate alongside cellulose substrates.

Aging Populations Boosting Adult-Incontinence Demand

Japan became the first country where adult diaper sales exceeded baby volumes in 2024, highlighting a demographic swing that is reshaping resin selection. Adult briefs demand higher peel strength, elevated heat resistance, and superior elastic recovery for extended wear, benefits that favor SEBS over SIS or SBS. Institutional buyers, such as hospitals, tolerate higher unit costs, enabling the inclusion of recycled or bio-based polyols that support sustainability claims. Europe and North America account for 54% of global adult-care adhesive consumption, yet rapid aging in South Korea, Taiwan, and urban China is narrowing the gap.

Sustainability Push Toward Low-VOC and Bio-Based Chemistries

REACH in Europe and China’s new T/CPA 005-2024 rule caps residual monomer and VOC limits, forcing reformulation of legacy EVA and SIS grades[2]China Diaper Association, “T/CPA 005-2024 Quality Standard,” chinadiaper.org. Pilot xylan-based polyurethane hot melts now meet ISO 14855 biodegradability standards and deliver peel adhesion within 5% of petroleum benchmarks. Evonik’s sale of its Coating & Adhesive Resins unit underlines a pivot toward specialty additives that enable waterborne and solvent-free systems. Reactive hot-melts that cure with ambient moisture cut line energy by up to 40% and eliminate high-temperature application, but still carry double-digit cost premiums.

Restraints Impact Analysis of Hygiene Adhesives Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petro-resin price volatility eroding producer margins | -0.60% | Global, acute in regions dependent on imported feedstocks (Europe, Japan, India, Southeast Asia) | Short term (≤ 2 years) |

| Adhesive bleed and odour raising consumer complaints | -0.30% | Concentrated in low-cost segments across India, Southeast Asia, Sub-Saharan Africa; quality-sensitive markets in China post-T/CPA 005-2024 | Medium term (2-4 years) |

| Emerging ultrasonic bonding reducing adhesive usage | -0.40% | Premium tiers in North America, Europe, Japan; gradual spill-over to high-volume Asian converters with capital budgets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Petro-Resin Price Volatility Eroding Producer Margins

Ethylene and propylene costs track crude swings and refinery run rates. EVA prices softened in late 2024 amid inventory overhang in China, yet underinvestment in cracker capacity since 2020 signals a likely deficit by 2026. Hygiene adhesive formulators average 8%–12% EBITDA margins and seldom pass through feedstock spikes in full, prompting experiments with hybrid EVA-SEBS blends that temper cost risk without compromising cure speed. Larger diaper converters are studying backward integration to secure resin supply and capture added value.

Adhesive Bleed and Odor; Emerging Ultrasonic Bonding

Hot-melt migration through breathable non-wovens triggers skin-contact complaints, while tackifier volatiles create odor that hurts brand perception. China’s T/CPA 005-2024 now caps acrylic residuals at 500 mg/kg, hastening the shift to low-odor grades. Parallel growth in ultrasonic welding for leg cuffs and waistbands can eliminate the need for adhesive: suppliers such as Dukane report up to 90% material savings. However, capital outlays of USD 50,000–200,000 per line and limited suitability for multilayer laminates restrict adoption to premium converters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Hygiene Adhesives Market Segment Analysis

By Resin Type:

SEBS Scaling on Thermal PerformanceEthylene-vinyl acetate controlled 40.92% hygiene adhesives market share in 2025, reflecting its competitive cost and broad equipment compatibility. SEBS, however, is forecasted to grow at a 6.12% CAGR through 2031, outstripping the overall hygiene adhesives market as converters prioritize heat resistance that maintains bond integrity at body temperature over extended wear. SIS continues to lead in construction adhesives that anchor super-absorbent cores thanks to its fast-tack nature, while SBS remains a niche in pressure-sensitive tapes. Hybrid EVA-SEBS systems, commercialized in H.B. Fuller’s Full-Hook line during 2024, demonstrate how formulators balance cost with thermal durability.

Regional preferences amplify divergence. Chinese producers stay with EVA because supply chains are entrenched and formulation tweaks are minimal. In contrast, Japanese and European converters are accelerating the adoption of SEBS to meet REACH emission ceilings. Patent filings in 2024 covering modified styrene block copolymers with longer open time indicate sustained innovation aimed at line speeds above 1,000 pieces per minute.

By Product Type:

Non-Woven Dominance, Woven EmergenceNon-woven substrates accounted for 66.88% of the hygiene adhesives market size in 2025, driven by polypropylene spunbond and meltblown fabrics that accept hot-melt penetration without stiffening. High-speed automation further solidifies non-woven demand: Henkel’s Easyflow cuts waste by 81% while synchronizing bead placement with substrate feed at millisecond intervals. Woven applications, although smaller, are growing at a 5.62% CAGR as circular-economy rules in Europe and Japan spur the adoption of washable diaper shells and reusable menstrual underwear. These substrates require pressure-sensitive or silicone-based adhesives that can withstand laundering and retain repositionability.

Innovation is also addressing softness mandates. China’s T/CPA 005-2024 specifies a minimum air permeance, pushing formulators toward lower-viscosity grades that avoid fiber compression. Meanwhile, breathable back-sheet designs require adhesives that bond across layered laminates without blocking vent pores, a challenge being met by low-density, high-tack hot-melts with microcrystalline wax modifiers.

By End-Use Product:

Feminine Care AscendsBaby diapers remained the volume leader, with a 47.72% share in 2025; however, growth is tapering as penetration nears saturation in East Asia and fertility declines in Europe. Parents are trading up to ultra-thin designs, utilizing SEBS elastic adhesives and moisture-resistant construction grades, which raises the value per unit even as the grams of adhesive decrease. Feminine care, in contrast, is expected to outpace all other segments at a 6.04% CAGR through 2031, driven by rural subsidy programs and tax exemptions in India, as well as rapid adoption in Indonesia and the Philippines.

Product design complexity drives adhesive differentiation. Pads require low-odor construction adhesives that preserve acquisition speed, as well as garment-safe pressure-sensitive grades for wings. Suppliers are also targeting biodegradable pads in Indian pilot schemes, utilizing bio-based hot melts that compost alongside cellulose substrates. Adult care continues to grow steadily, driven by aging demographics and increasing adhesive intensity per unit. Institutional buyers’ focus on durability and odor control favors SEBS-based systems that withstand extended use without tack loss.

Geography Analysis

APAC Hygiene Adhesives Market

The Asia-Pacific region dominated the hygiene adhesives market with a 46.10% market share in 2025, underpinned by China’s forecasted demand of 160,000 tonnes of hot-melt adhesives in 2026 and India’s rapid uptake of sanitary pads. Chinese consumers continue to shift toward premium diaper formats that require high-performance elastic adhesives, while Indian initiatives aim to increase pad penetration in rural villages. Japan exemplifies demographic inversion as adult diapers overtake baby volumes, spurring demand for high-peel SEBS adhesives that maintain bond integrity at body temperature. Quickly urbanizing ASEAN economies supply greenfield growth, although distribution fragmentation keeps service intensity high for suppliers.

North America and Europe Hygiene Adhesives Market

North America and Europe are mature but lucrative markets, driven by premiumization and stringent environmental regulations. Dow reported softer 2024 sales yet continues to invest in specialty resins, and Henkel’s US automation upgrades demonstrate a continued commitment to machine-friendly chemistries. Extended producer responsibility statutes in Europe are accelerating the switch to bio-based and waterborne adhesives, with Evonik divesting its commodity business to fund specialty additive development.

MEA and South America Hygiene Adhesives Market

The Middle East and Africa, while only a midsize base today, are expected to grow at 5.74% CAGR to 2031 on the back of Saudi Vision 2030 healthcare build-outs and a projected UAE health spend rise from USD 20.8 billion in 2023 to USD 26.7 billion by 2028. Expanding retail infrastructure and improved cold chains widen distribution for hygiene products. Brazil anchors South America yet faces currency uncertainty; however, stable inflation paths could unleash latent demand in the latter half of the decade.

Competitive Landscape

The Hygiene Adhesives Market is moderately concentrated. Tier-1 vendors channel capital into automation-compatible lines and sustainability branding: Henkel’s Easyflow reduced waste by 81%, and H.B. Fuller’s Full-Hook hybrid formulation offers elastic durability with cost parity to pure SEBS. Regional suppliers compete on customized blends for biodegradable pads and reusable inserts, leveraging shorter lead times and lower overhead. M&A is reshaping portfolios. Sika’s CHF 7.5 billion acquisition of MBCC in 2024 expanded its adhesive reach, while 3M spun off its healthcare business to focus on industrial tapes, freeing up capital for high-speed manufacturing platforms. Backward integration by large diaper makers in Asia remains a strategic wildcard that could squeeze independent formulators’ volumes later in the decade.

Hygiene Adhesives Industry Leaders

3M

Dow

Henkel AG & Co. KGaA

H. B. Fuller Company

Arkema

- *Disclaimer: Major Players sorted in no particular order

Hygiene Adhesives Market Companies Covered in this Report

- 3M

- Abifor AG

- ADTEK Malaysia Sdn Bhd

- Arkema

- Avery Dennison Corporation

- Colquimica Adhesives

- Dow

- Evonik Industries AG

- Exxon Mobil Corporation

- Focus Hotmelt Company

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman Corporation

- ICHEMCO s.r.l.

- Jowat AG

- Lohmann GmbH & Co. KG

- NANPAO RESINS CHEMICAL GROUP

- OMNOVA Solutions Inc.

- Palmetto Adhesives

- Savare Specialty Adhesives LLC

- Sika AG

- TEX YEAR INDUSTRIES INC.

Recent Industry Developments in Hygiene Adhesives Market

- July 2025: TEX YEAR INDUSTRIES INC. launched Asia’s first biodegradable hot melt adhesive dedicated production line, along with the newly established innovation building, a dedicated R&D and production facility. These bio-based adhesive products are widely used in various industries, including packaging, hygiene products, DIY, and label tapes.

- January 2025: The H.B. Fuller Company launched Full-Care 6550 SecureFix, a hygiene adhesive designed to provide a strong bond in high-moisture environments. Its unique formulation ensures that products like pantyliners stay securely in place, even when exposed to moisture or movement.

Global Hygiene Adhesives Market Report Scope

Hygiene adhesives are non-woven construction adhesive systems used for applications such as bonding applications in baby diapers, adult incontinence, feminine care, medical protective wear, and tissue and towel applications.

The market for hygiene adhesives is segmented by resin type, product type, application, and geography. By resin type, the market is segmented into ethylene-vinyl acetate (EVA), styrene-ethylene-butadiene-styrene (SEBS), styrene-isoprene-styrene (SIS), styrene-butadiene-styrene (SBS), and other resin types. By product type, the market is segmented into woven and non-woven. By application, the market is segmented into baby care, adult care, feminine care, and other applications. The report offers market size and forecasts for the anti-reflective coatings market in 17 countries across major regions. For each segment, market size and forecasts for the anti-reflective coatings market in revenue (USD million).

Segmentation Overview

| Ethylene-vinyl acetate (EVA) |

| Styrene-ethylene-butadiene-styrene (SEBS) |

| Styrene-isoprene-styrene (SIS) |

| Styrene-butadiene-styrene (SBS) |

| Other Resin Types |

| Woven |

| Non-woven |

| Baby Care |

| Adult Care |

| Feminine Care |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Ethylene-vinyl acetate (EVA) | |

| Styrene-ethylene-butadiene-styrene (SEBS) | ||

| Styrene-isoprene-styrene (SIS) | ||

| Styrene-butadiene-styrene (SBS) | ||

| Other Resin Types | ||

| By Product Type | Woven | |

| Non-woven | ||

| By End-use Product | Baby Care | |

| Adult Care | ||

| Feminine Care | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is demand for adhesives in feminine hygiene products growing?

Feminine products are projected to record a 6.04% CAGR between 2026 and 2031, the quickest among all end-use segments.

Which region provides the largest sales base for hygiene adhesives?

Asia-Pacific led with 46.10% share in 2025, anchored by China’s sizable diaper and pad production volumes.

What resin is gaining popularity for premium diapers and adult briefs?

SEBS is scaling the fastest because its heat resistance and elastic recovery outperform EVA and SIS in extended-wear applications.

Why are converters considering ultrasonic bonding?

Ultrasonic welding can remove elastic-attachment adhesives entirely and cut material expense by up to 90%, though high capex limits uptake.

What sustainability trends affect formulation choices?

Regulators are lowering VOC thresholds, prompting a move toward bio-based polyurethane hot-melts that meet ISO 14855 degradability criteria.

What is the current market size of hygiene adhesives market?

The Hygiene Adhesives Market size is estimated at USD 3.51 billion in 2026, and is expected to reach USD 4.39 billion by 2031, at a CAGR of 4.55% during the forecast period (2026-2031).

Page last updated on: