Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

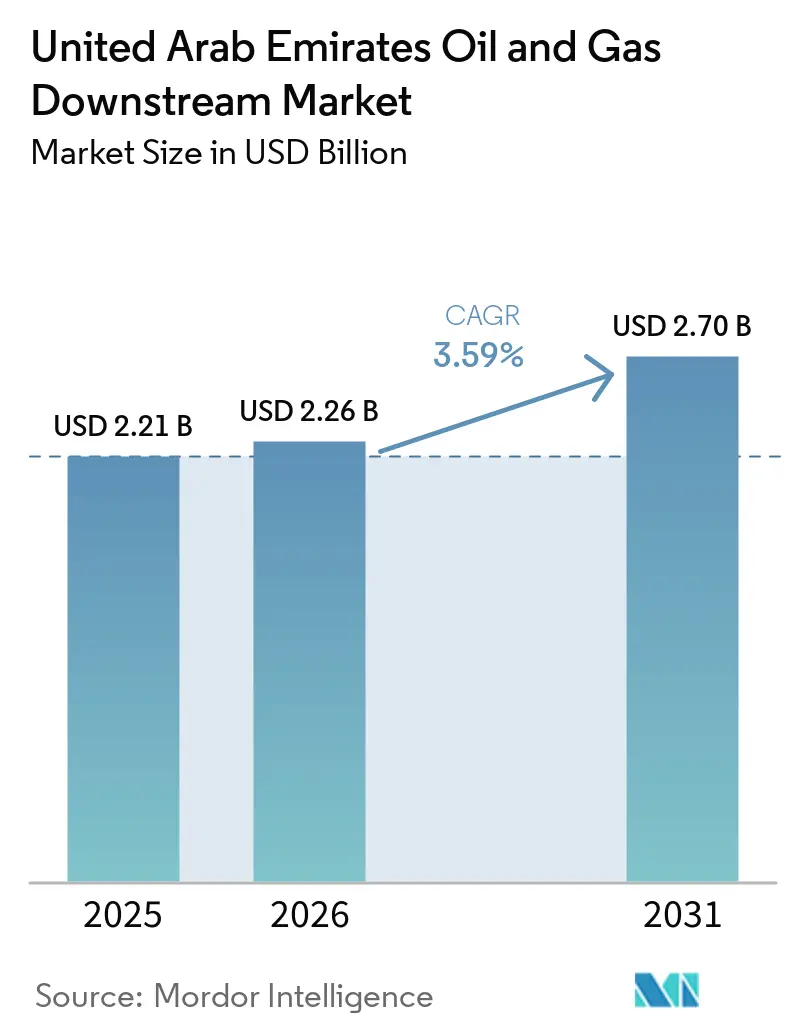

| Base Year Market Size (2025) | USD 2.21 Billion |

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 2.70 Billion |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

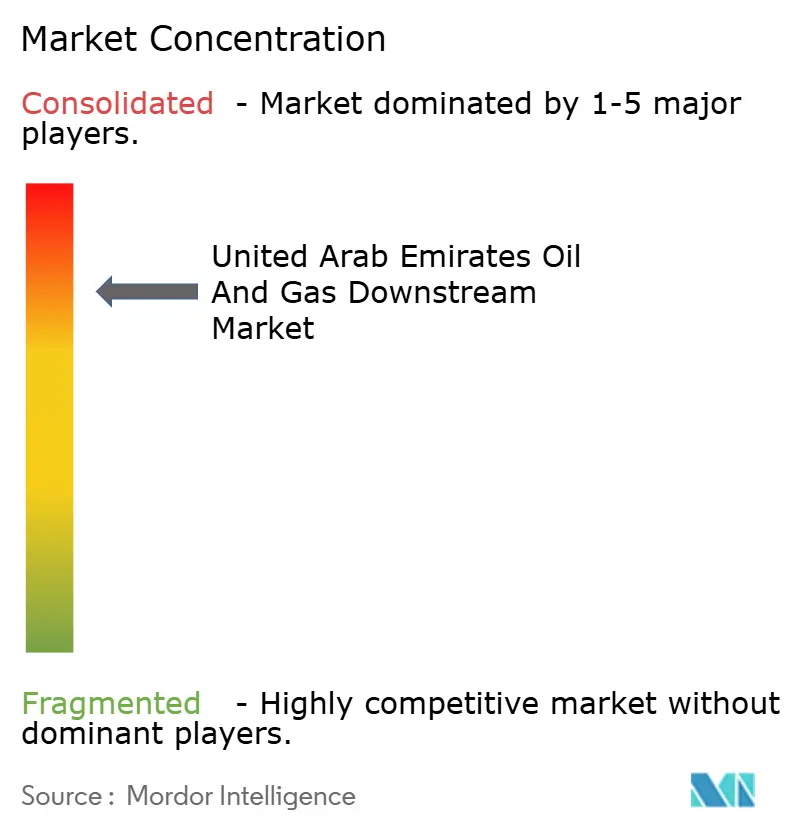

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Oil And Gas Downstream Market Analysis by Mordor Intelligence

The United Arab Emirates Oil And Gas Downstream Market size is expected to increase from USD 2.21 billion in 2025 to USD 2.26 billion in 2026 and reach USD 2.70 billion by 2031, growing at a CAGR of 3.59% over 2026-2031.

The headline growth rate understates a deliberate pivot from legacy refining to higher-margin petrochemicals, anchored by ADNOC’s USD 45 billion downstream and chemicals program that channels capital toward crackers, specialty polymers, and digital integration. Asian demand continues to pull Gulf cargoes, lifting UAE refined-product exports to 5.51 million barrels per day in 2024, yet new mega-refineries in India and China are eroding cost advantages in commodity fuels, pushing local operators to defend margins through crude-flexibility upgrades, logistics investments in Fujairah, and real-time optimization technologies. Policy shifts add further complexity: the EU Carbon Border Adjustment Mechanism, active since January 2026, now forces exporters to document emissions intensity or absorb default mark-ups that can shave USD 3-8 per tonne off European netbacks. Financing conditions also influence strategy; with global downstream investment at a ten-year low in 2025, projects backed by sovereign balance sheets enjoy privileged access to capital, while independent refiners face higher hurdles for carbon-abatement spending.

Key Report Takeaways

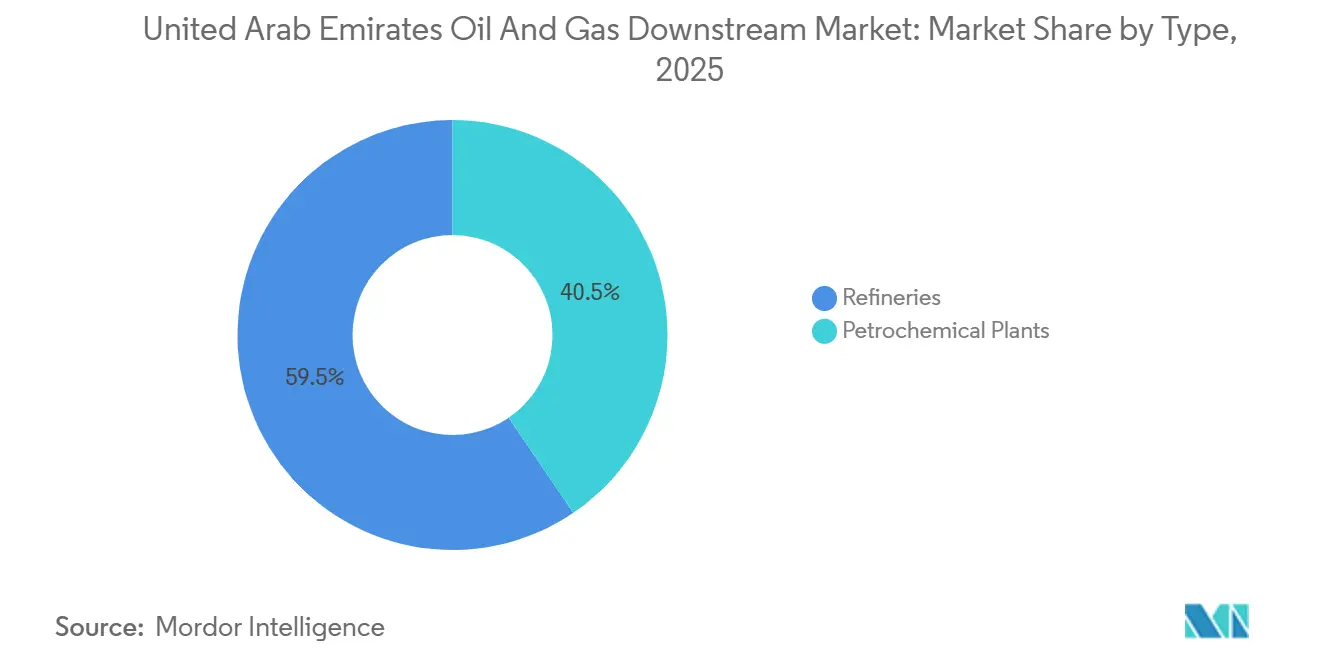

- By type, refineries led with 59.5% of the United Arab Emirates oil and gas downstream market share in 2025, while petrochemical plants are expected to grow at a 5.1% CAGR through 2031.

- By product type, refined petroleum products accounted for 52.3% of the United Arab Emirates oil and gas downstream market size in 2025, whereas petrochemicals are projected to expand at a 5.9% CAGR to 2031.

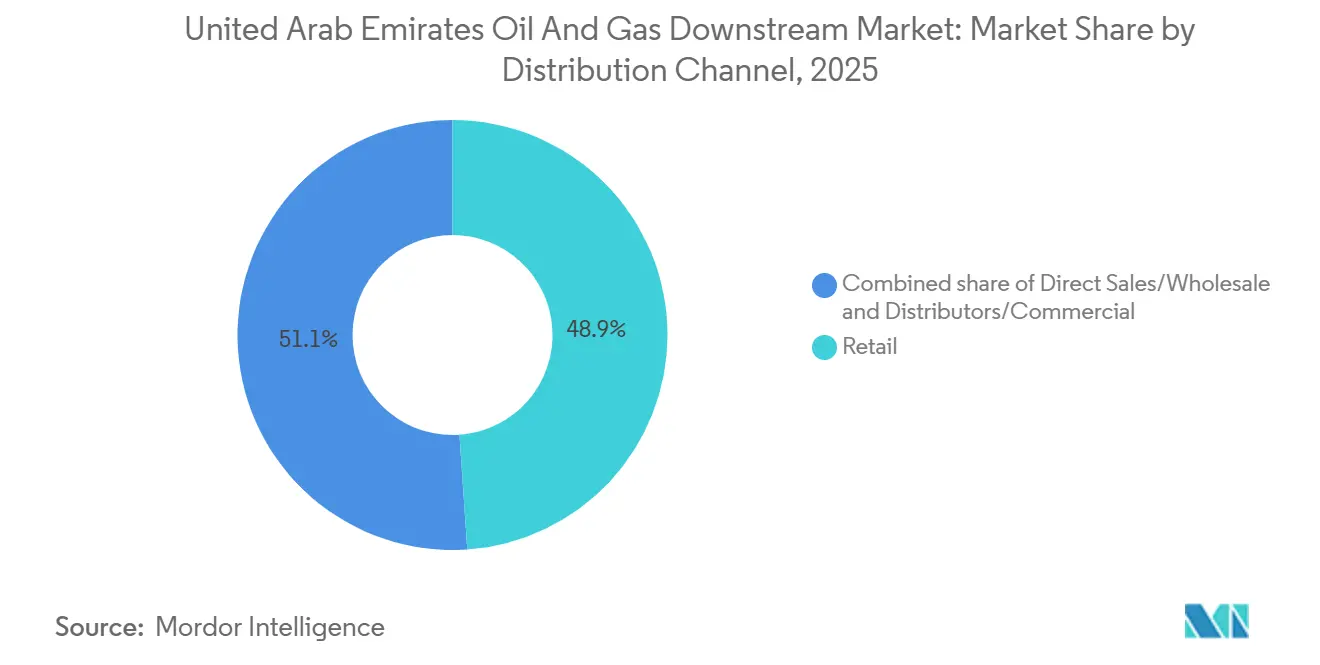

- By distribution channel, the retail segment held 48.9% of the United Arab Emirates oil and gas downstream market size in 2025, but distributors and commercial channels are expected to grow at a 6.2% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Oil And Gas Downstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADNOC USD 45 billion downstream & petrochemicals investment program | 1.2% | UAE national, with spillover to GCC export corridors | Long term (≥ 4 years) |

| Rising Asian demand pulling UAE refined-product exports | 0.9% | Global, concentrated in India, China, Southeast Asia | Medium term (2-4 years) |

| Fujairah's emergence as regional bunkering & storage hub | 0.5% | UAE (Fujairah), regional maritime routes (Arabian Sea, Gulf of Aden) | Medium term (2-4 years) |

| Ruwais crude-flexibility & refinery-petchem integration upgrades | 0.7% | UAE national (Abu Dhabi, Ruwais industrial zone) | Short term (≤ 2 years) |

| Hydrogen-ready multi-energy retail network roll-out | 0.4% | UAE national, early deployment in Abu Dhabi and Dubai | Long term (≥ 4 years) |

| AI / digital-twin deployment boosting refinery margins | 0.6% | UAE national, with demonstration effects across GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ADNOC USD 45 Billion Downstream & Petrochemicals Investment Program

ADNOC’s USD 45 billion allocation through 2030 redirects capital from incremental distillation toward high-margin derivatives that yield 30-50% larger spreads than diesel or gasoline.[1]ADNOC, “Investor Presentation 2025,” adnoc.ae TA’ZIZ Phase 1, a USD 5 billion complex targeting 4.7 million t/year of chemicals by 2028, is structured around joint ventures with Reliance Industries, ADQ, and BASF, all focused on specialty chains rather than commodity fuels.[2]TA’ZIZ, “Phase 1 Project Factsheet,” taziz.ae The USD 6.2 billion Borouge 4 cracker, commissioned in late 2025, tilts the United Arab Emirates oil and gas downstream market toward polyethylene and polypropylene exports for Asian packaging and automotive demand.[3]Borouge, “Borouge 4 Commissioning Update,” borouge.com Execution hinges on feedstock flexibility achieved via Ruwais’s USD 3.5 billion crude-flexibility upgrade that enables 420 000 b/d of heavy-crude processing, cutting input costs by USD 2-4 per barrel.

Rising Asian Demand Pulling UAE Refined-Product Exports

Gulf exporters shipped a record 5.51 million b/d of refined products in 2024, 7% above 2023, with India remaining structurally short of diesel and jet fuel despite 5.3 million b/d of installed capacity. Fujairah’s 14 million m³ of storage lets traders arbitrage naphtha, condensate, and LPG flows responding to price swings between term and spot contracts in Asia.[4]Port of Fujairah, “Annual Traffic Report 2025,” fujairahport.ae Momentum is bifurcating: India and Southeast Asia still import middle distillates for transport and power, while China’s overcapacity is pushing low-margin diesel exports that undercut UAE barrels by USD 1-2 per barrel. The EU carbon mechanism compounds risk for shipments to Europe unless exporters verify lower life-cycle emissions.

Fujairah’s Emergence as Regional Bunkering & Storage Hub

Handling 7.6 million m³ of marine fuel in 2024, Fujairah is now the world’s third-largest bunkering center, supported by Vopak Horizon’s 1 million m³ tanks and recent capacity additions by Brooge Energy and Apex Terminals. A USD 204 million port deepening and digital-tracking project aims to accommodate larger LNG and container vessels by 2027, improving turnaround and inventory visibility. Red Sea security disruptions since late 2023 are diverting ships around Africa, lengthening voyages by 10-14 days and elevating Fujairah’s role as a refueling midpoint. Independent operators import blended fuels from Saudi, Indian, and Russian suppliers, capturing spreads without owning refining assets.

Ruwais Crude-Flexibility & Refinery-Petchem Integration Upgrades

Completed in late 2023, Ruwais’s USD 3.5 billion retrofit enables 420 000 b/d of heavy, sulfur-rich crude processing that lowers feedstock costs while preserving ultra-low-sulfur diesel and jet yields. Off-gas streams feed adjacent ethylene crackers, adding 15-20% value per barrel compared with standalone refineries. AIQ’s SMARTi monitoring, deployed in 2024, analyzes over 1 billion images daily, cutting unplanned shutdowns by 50% and extending maintenance windows by 20%. Fertiglobe’s ammonia and urea lines recycle hydrogen and carbon dioxide byproducts, trimming emissions intensity by up to 12% relative to isolated assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising project financing barriers from carbon-intensity scrutiny | -0.6% | Global, acute in UAE for independent refiners seeking international capital | Medium term (2-4 years) |

| Competition from new mega-refineries in India & China | -0.4% | Global, concentrated impact on UAE export margins to Asia | Long term (≥ 4 years) |

| Gulf/Red-Sea maritime security disruptions elevating logistics risk | -0.3% | Regional, affecting Red Sea, Bab el Mandeb, Gulf of Aden, Arabian Sea, Persian Gulf | Short term (≤ 2 years) |

| EU Carbon Border Adjustment Mechanism (CBAM) on fuel imports | -0.3% | UAE exports to EU, with indirect effects on global pricing benchmarks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Project Financing Barriers from Carbon-Intensity Scrutiny

Downstream FIDs dropped to decadal lows in 2025, and 64% of energy investors now rank policy alignment as decisive for profitability. ICMA’s 2025 transition-bond guidelines oblige fossil projects to show credible decarbonization pathways; yet, only 10% of Middle East refineries have sanctioned CCUS installations. EU and Japanese importers mandate emissions-intensity disclosure, pushing UAE plants to install continuous monitors costing USD 5-15 million per site or face default carbon factors that trim export netbacks. Fertiglobe’s blue-ammonia joint venture, with 90% carbon capture, highlights how state-linked entities secure financing for low-carbon derivatives that fetch potential USD 50-100/t premiums in Europe and Asia.

Competition from New Mega-Refineries in India & China

Reliance’s 1.4 million b/d Jamnagar complex sports a Nelson complexity of 21.1 and processes ultra-heavy crude into fuels and feedstocks 10-15% cheaper than Gulf peers. China’s 400 000 b/d Shandong Yulong plant, online since 2024, feeds an oversupplied domestic market, pushing competitively priced diesel into Southeast Asia. Kuwait’s 615 000 b/d Al-Zour and Oman’s 230 000 b/d Duqm refineries add further pressure, trimming Asian cracks by USD 2-4 per barrel. UAE refiners mitigate with integration and AI-enabled cost controls, yet older Ruwais units commissioned in the 1980s-1990s still require expensive retrofits to match Indian and Chinese complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Petrochemical Integration Reshapes Asset Mix

Petrochemical plants are advancing at a 5.1% CAGR through 2031, whereas refineries commanded 59.5% of the United Arab Emirates' oil and gas downstream market share in 2025. The United Arab Emirates oil and gas downstream market size, attached to Borouge 4's 1.5 million t/year cracker, and TA'ZIZ's 4.7 million t/year chemicals slate highlights the scale shift toward polymers and specialty derivatives.

Refineries remain vital thanks to Ruwais's 922 000 b/d capacity and ENOC's 140 000 b/d Dubai plant, yet most new spending targets hydrocracking and isomerization that maximize petrochemical feedstock yields. Digital-twin deployments at Ruwais and the Sour Gas facility are extracting 5-10% more value per barrel, underpinning competitiveness in the United Arab Emirates oil and gas downstream market.

By Product Type: Petrochemicals Gain Share

Refined petroleum products held 52.3% of the United Arab Emirates' oil and gas downstream market size in 2025, but petrochemicals are projected to expand at a 5.9% CAGR between 2026 and 2031. Lubricants remain a niche anchored by ENOC's premium aviation and marine grades.

Petrochemical momentum reflects higher margins for polyethylene, polypropylene, and chlor-alkali streams produced by Borouge and TA'ZIZ joint ventures. Gasoline and diesel face headwinds from electric-vehicle uptake in China and Europe, and aviation fuel demand, though rebounding, still trails 2019 levels in key Asian hubs. Polymer demand in India and Southeast Asia is rising 6-7% annually, reinforcing the growth differential within the United Arab Emirates oil and gas downstream market.

By Distribution Channel: Commercial Gains on Aviation Recovery

Retail stations captured 48.9% of 2025 revenue, yet distributors and commercial channels are forecast to rise at a 6.2% CAGR to 2031 as aviation fuel sales rebound and industrial clients lock in term contracts.

ADNOC Distribution’s plan for 1 150 service stations by 2028 and 500-750 EV charging points signals diversification, but commercial volumes tied to Fujairah bunkering and Dubai International Airport are growing faster. This shift underscores a gradual realignment in the United Arab Emirates oil and gas downstream market toward bulk contracts, credit-flexible terms, and multi-energy offerings.

Geography Analysis

Abu Dhabi dominates the United Arab Emirates' oil and gas downstream market, hosting the 922 000 b/d Ruwais refinery and the emergent TA’ZIZ chemicals cluster that together anchor most new capacity. Fujairah supplements this core with 14 million m³ of storage and the world’s third-largest bunkering trade, moving 7.6 million m³ of marine fuel in 2024. Dubai operates the 140 000 b/d ENOC refinery and a dense retail network oriented toward aviation and tourism demand.

Ruwais expansions, Borouge 4’s cracker, and TA’ZIZ’s USD 5 billion Phase 1, target polymers for Asian consumers, aligning asset footprints with demand centers that already import USD 35.52 billion of UAE hydrocarbons annually. Fujairah’s independent tanks added 650 000 m³ in 2024-2025, enabling traders to arbitrage between Indian, Chinese, and African markets even as Red Sea security issues extend voyage times by two weeks and inflate insurance premiums.

Regional competition intensifies pressure on the United Arab Emirates' oil and gas downstream market: Saudi Aramco’s digitally optimized Yanbu complex reports 35% higher profitability and 14% lower emissions, Kuwait’s 615 000 b/d Al-Zour plant targets the same Asian offtakers, and Oman’s Duqm facility adds 230 000 b/d of export-oriented supply. UAE operators reply with AIQ’s SMARTi suite, Neuron 5 analytics, and blue-ammonia ventures positioned to capture European low-carbon premiums that competitors have yet to commercialize.

Competitive Landscape

The United Arab Emirates oil and gas downstream market is consolidated: ADNOC entities control refining, petrochemicals, gas processing, and retail, while ENOC, Emarat, Vopak Horizon, Brooge Energy, and Apex Terminals compete across storage, bunkering, and distribution niches. ADNOC’s integrated model and USD 45 billion capital plan reinforce scale advantages, but independent Fujairah operators gain ground by offering flexible contract terms and faster cargo handling.

Technology deployment is the chief differentiator. Neuron 5 AI, rolled out in 2024, lowered unplanned downtime by 50% and created USD 500 million in additional value, while AIQ’s SMARTi platform scans more than 1 billion images a day to detect corrosion and leaks at >90% accuracy. Borouge’s autonomous operations pilot, launched in January 2026, delivered up to 20% operating-cost savings and is slated for full-scale adoption by 2027.

Strategic optionality centers on low-carbon derivatives. Fertiglobe’s 1 million t/year blue-ammonia project, expected online in 2028, targets premium customers exposed to EU and Japanese carbon regimes. Storage players such as Brooge Energy and Vopak Horizon continue to expand tanks and jetties, allowing traders to import discounted Russian or Saudi cargoes for blending, a practice that inserts competitive tension into an otherwise vertically integrated market.

United Arab Emirates Oil And Gas Downstream Industry Leaders

Emirates National Oil Co

Abu Dhabi National Oil Co

Total SA

Royal Dutch Shell Plc

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: BPCL signed a strategic crude purchase agreement with TotalEnergies for UAE-sourced oil. This agreement enhances demand for UAE crude and reinforces its downstream significance by ensuring consistent export channels, supporting refinery utilization, and strengthening its global market position.

- January 2026: Galp and Moeve agreed to merge their downstream operations, creating a significant Iberian refining and retail network. Although primarily focused on Europe, this consolidation enhances global downstream competitiveness. It indirectly impacts UAE downstream players by altering trade flows and refining capacity dynamics.

- May 2025: Borouge announced capacity expansions at Al Ruwais, including the EU2 ethane cracker upgrade, which will add 230,000 tonnes per year of ethylene capacity, and expansions of the PE4/PE5 plants to 700,000 tonnes per year each.

- September 2025: EGA introduced a UAE National housing support program in collaboration with the Abu Dhabi Housing Authority. This initiative, aimed at high-performing employees, enhances Emirati workforce retention. While not directly related to downstream operations, it bolsters the UAE’s industrial labor ecosystem, contributing to long-term stability for national energy companies, including those in the downstream sector.

- August 2025: ADNOC Gas entered into a 10-year LNG supply agreement with India’s HPCL. Although LNG falls under the midstream category, this deal indirectly supports the downstream sector by ensuring stable gas flows. It also strengthens the UAE’s energy trade profile and increases demand for downstream-linked infrastructure.

United Arab Emirates Oil And Gas Downstream Market Report Scope

In the downstream sector, crude oil is refined, natural gas is processed and purified, and products derived from crude oil and natural gas are marketed and distributed.

The United Arab Emirates oil and gas downstream market is segmented by type, product type, and distribution channel. By type, the market is segmented into refineries and petrochemical plants. By product type, the market is segmented into refined petroleum products, petrochemicals, and lubricants. By distribution channel, the market is divided among direct sales/wholesale, distributors/commercial, and retail. For each segment, the market sizing and forecasts have been done based on value (USD).

By Type

| Refineries |

| Petrochemical Plants |

By Product Type

| Refined Petroleum Products |

| Petrochemicals |

| Lubricants |

By Distribution Channel

| Direct Sales/Wholesale |

| Distributors/Commercial |

| Retail |

| By Type | Refineries |

| Petrochemical Plants | |

| By Product Type | Refined Petroleum Products |

| Petrochemicals | |

| Lubricants | |

| By Distribution Channel | Direct Sales/Wholesale |

| Distributors/Commercial | |

| Retail |

Key Questions Answered in the Report

What is the current value of the United Arab Emirates oil and gas downstream market?

The United Arab Emirates oil and gas downstream market size stands at USD 2.26 billion in 2026 and is projected to reach USD 2.70 billion by 2031.

Which segment is expanding fastest within UAE downstream operations?

Petrochemical plants are the fastest-growing type, advancing at a 5.1% CAGR on the back of projects like Borouge 4 and TA'ZIZ Phase 1.

How is Fujairah strengthening its position in regional bunkering?

Fujairah handled 7.6 million m³ of marine fuel in 2024 and is expanding storage, berth depth, and digital tracking to attract vessels rerouting around Red Sea disruptions.

What role does technology play in UAE downstream competitiveness?

ADNOC's Neuron 5 AI and AIQ's SMARTi monitoring cut unplanned downtime by up to 50% and unlock hundreds of millions of dollars in annual savings, cushioning margins against rising competition.

How will the EU Carbon Border Adjustment Mechanism affect UAE exports?

From January 2026, fuel cargoes into Europe face default emissions charges unless operators provide verified intensity data, potentially reducing netbacks by USD 3-8 per tonne.

Are distributors or retail filling stations growing faster in the UAE?

Distributors and commercial channels are projected to outpace retail, growing at a 6.2% CAGR through 2031 as aviation and industrial buyers favor term contracts and bulk deliveries.

Page last updated on: