Unified Communications (UC) Hardware Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

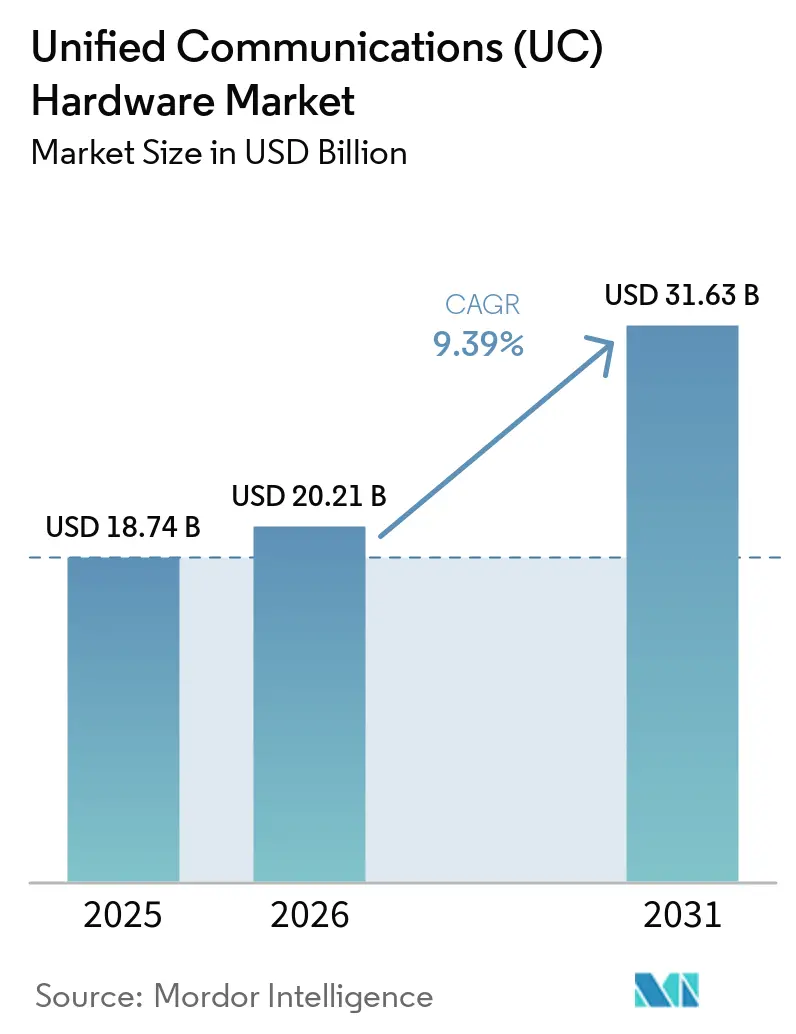

| Market Size (2026) | USD 20.21 Billion |

| Market Size (2031) | USD 31.63 Billion |

| Growth Rate (2026 - 2031) | 9.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unified Communications (UC) Hardware Market Analysis by Mordor Intelligence

The Unified Communications (UC) Hardware market size was valued at USD 18.74 billion in 2025 and estimated to grow from USD 20.21 billion in 2026 to reach USD 31.63 billion by 2031, at a CAGR of 9.39% during the forecast period (2026-2031). Strong policy support for all-IP migration in the United States and the United Kingdom, permanent hybrid-work practices, and rapid advances in AI-enabled peripherals are the primary growth engines. Enterprises that invested in stop-gap webcams and headsets in 2020-2021 are now standardizing certified endpoints that can be provisioned and secured at scale. Meanwhile, AI-powered cameras with automatic framing and multilingual transcription are transforming collaboration rooms from cost centers into productivity hubs. Heightened security scrutiny is steering risk-averse sectors toward devices with hardware-based encryption, even as intense price competition from Asian vendors continues to compress margins on legacy desk phones.

Key Report Takeaways

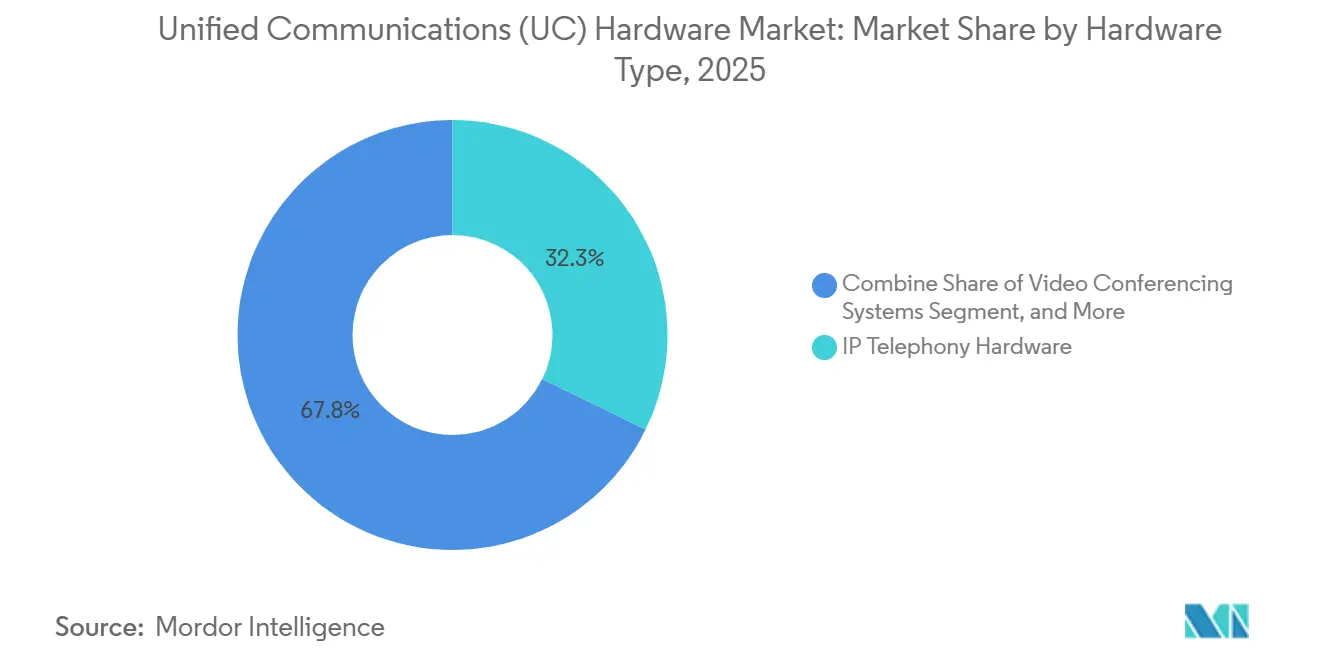

- By hardware type, video conferencing systems led with 11.24% growth, while IP telephony hardware accounted for 32.25% of the Unified Communications (UC) Hardware market share in 2025.

- By distribution model, offline channels retained 68.27% revenue share in 2025, whereas online channels are projected to expand at a 12.08% CAGR through 2031.

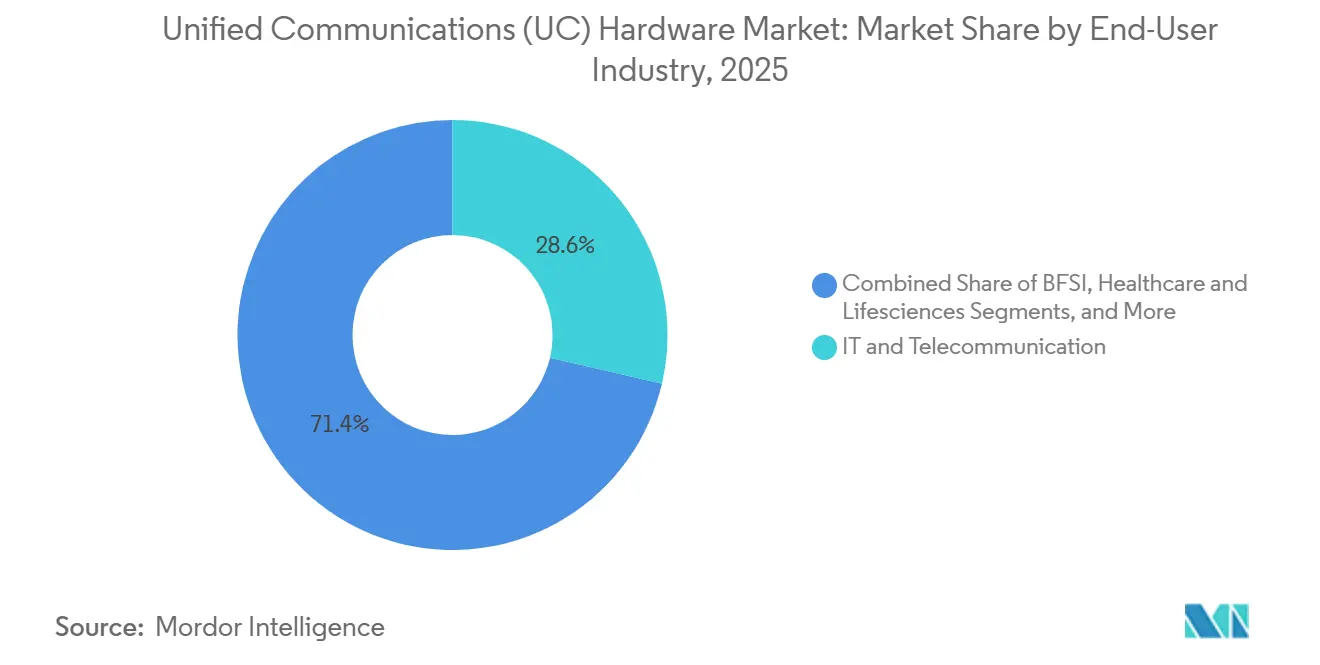

- By end-user industry, IT and telecommunications accounted for 28.64% of 2025 revenues, while the healthcare and life sciences industry is forecast to grow at a 10.72% CAGR through 2031.

- By organization size, large enterprises commanded 71.53% of the Unified Communications (UC) Hardware market size in 2025, yet small and medium-sized enterprises are advancing at an 11.67% CAGR through 2031.

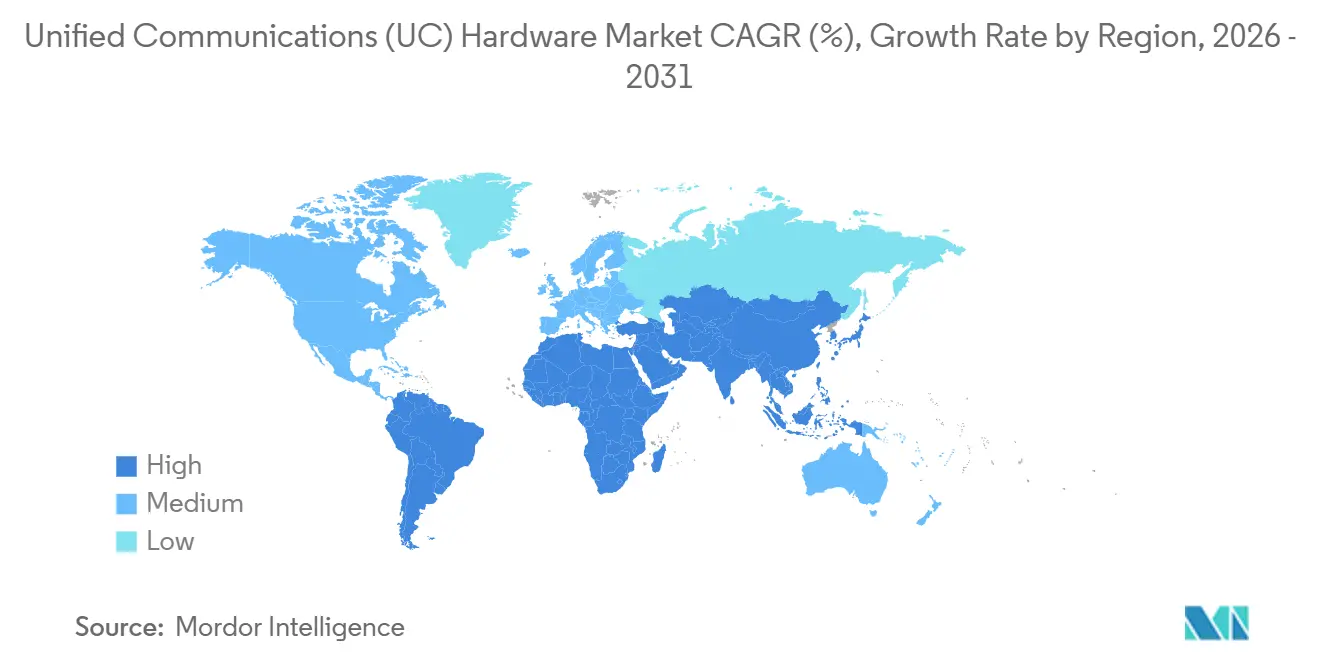

- By geography, North America held 34.82% revenue share in 2025, and Asia-Pacific is poised for the fastest regional growth with an 11.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Unified Communications (UC) Hardware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Hybrid Work Environments | +2.8% | Global, concentration in North America and Europe | Medium term (2–4 years) |

| Surge in Enterprise-Wide Video Collaboration Demand | +2.3% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Migration from PSTN to IP-Based Telephony Systems | +1.9% | Europe and North America | Short term (≤ 2 years) |

| Cost Efficiencies Achieved Through Equipment Consolidation | +1.2% | Global, strongest in SME segment | Medium term (2–4 years) |

| Rise of Hardware-Optimized UCaaS Gateways in Emerging Markets | +0.8% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Growing Integration of AI-Enabled Audio Peripherals | +0.6% | North America and Europe early adopters | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Hybrid Work Environments

Permanent hybrid schedules are compelling organizations to replace ad-hoc consumer devices with enterprise-certified endpoints that can be centrally managed and secured. Gartner has noted that poor device quality contributes to digital friction for roughly two-thirds of employees, prompting refresh cycles to shrink to three-to-four years. Vendors such as Cisco have responded with collaboration boards that embed AI compute, eliminating the need for external peripherals and simplifying remote provisioning.[1]Cisco Systems, “Cisco Announces New Multifunctional Collaboration Devices for Hybrid Work,” cisco.com Standardizing device portfolios by role and room type reduces support costs and improves the user experience, positioning high-performance UC hardware as a strategic enabler of talent retention and operational resilience.

Surge in Enterprise-Wide Video Collaboration Demand

Video usage has expanded from executive suites to every desk and huddle room, driving demand for scalable systems that support modular upgrades. Jabra’s 2026 PanaCast Room Kits, offered in one-, three-, and five-camera variants, allow IT teams to right-size investments while preserving future expansion paths.[2]Jabra, “Jabra and Lenovo collaborate on the next generation PanaCast 50 Room System,” jabra.com Logitech’s Rally AI Camera Pro introduces dual-camera intelligence at the USD 2,999 price point, addressing visibility gaps in large spaces. Integration of scheduling panels ensures that expensive meeting spaces are utilized efficiently, reducing “ghost meetings” and optimizing real estate.

Migration from PSTN to IP-Based Telephony Systems

Regulatory deadlines are accelerating the sunset of copper networks. The United Kingdom’s January 2027 PSTN switch-off requires migrating roughly 19.5 million lines, prompting BT Group to allocate GBP 416 million (USD 520 million) to customer equipment upgrades. In the United States, the FCC’s 2026 proposal to finalize bill-and-keep rules provides predictability for enterprises investing in SIP gateways and VoIP-ready endpoints. These mandates are creating concentrated procurement waves for session border controllers, battery back-up units, and telecare-certified devices.

Cost Efficiencies Achieved Through Equipment Consolidation

Budgets are shifting from stand-alone PBX servers to multi-function devices that bundle video, audio, and control into one appliance. Avaya’s partnership with Zoom lets customers layer AI features onto existing Avaya hardware, extending asset life and deferring replacement spending. Jabra’s second-generation PanaCast 50 Room System pairs a video bar with Lenovo compute, claiming up to 40% lower power consumption and reduced cabling complexity. Subscription models that bundle hardware with cloud software convert capital expenditure into predictable operating expenses, a particularly attractive proposition for SMEs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Average Selling Prices of Legacy UC Endpoints | -1.4% | Global, acute in Asia-Pacific SMEs | Short term (≤ 2 years) |

| Security Concerns Around SIP and VoIP Gateways | -0.9% | Global, heightened in regulated industries | Medium term (2–4 years) |

| Persistent Supply-Chain Chips Shortage in Networking ASICs | -0.6% | Global | Short term (≤ 2 years) |

| Environmental Regulations Limiting Single-Use Plastics in Headsets | -0.3% | Europe primary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Average Selling Prices of Legacy UC Endpoints

Asian vendors such as Yealink now offer Microsoft Teams-certified desk phones at prices up to 40% below Western incumbents, eroding margins on commodity hardware.[3]Yealink, “Yealink and Microsoft Elevate Strategic Partnership,” yealink.com The commoditization trend enables buyers to source endpoints from multiple suppliers, forcing legacy providers to bundle value-added software or shift focus to premium AI-enhanced categories. Vendors have responded with subscription offerings like Jabra Engage AI Complete, which fuses tone analytics and transcription into a per-user fee, creating recurring revenue to offset lower hardware margins.

Security Concerns Around SIP and VoIP Gateways

The December 2025 disclosure of CVE-2025-68274, a nil-pointer dereference in the widely used sipgo library, underscored the vulnerability of voice gateways to denial-of-service attacks. Highly regulated verticals now demand hardware root of trust, encryption at rest and in transit, and compliance with ISO 27001 and SOC 2 standards. These requirements lengthen procurement cycles and increase the total cost of ownership, tempering near-term uptake despite clear functionality benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hardware Type: Video Conferencing Systems Sustain the Innovation Runway

IP telephony hardware still generated the highest category revenue, holding a 32.25% Unified Communications Hardware market share in 2025, yet its growth rate is moderating as voice becomes an embedded feature within broader collaboration suites. Video conferencing systems recorded the fastest growth, advancing at an 11.24% CAGR between 2026 and 2031. They remain the focal point of new feature investment as enterprises seek inclusive meeting experiences across hybrid teams.

Advances in edge-AI silicon now allow cameras to perform real-time speaker tracking and language transcription without relying on cloud compute, reducing latency and meeting privacy mandates. Collaboration bars that integrate a camera, microphone, speaker, and codec into a single device lower installation complexity and have become a preferred form factor for rapid rollout programs. Vendors with strong software roadmaps and certified cross-platform compatibility continue to displace pure-play hardware competitors.

By Distribution Model: Online Channels Move from Fringe to Mainstream

Offline distribution model continued to dominate the distribution landscape in 2025, accounting for 68.27% of total revenue, largely due to the need for complex room integrations and on-site support in large enterprises and mission-critical environments. Despite this, online channels are rapidly transitioning from a niche option to a mainstream purchasing route, growing at a CAGR of 12.08%. Their adoption is particularly strong for standardized, plug-and-play products such as USB headsets and personal webcams, where deployment complexity is minimal.

To capitalize on this shift, manufacturers are expanding investments in direct e-commerce platforms and cloud-based marketplaces that allow customers to configure and purchase certified bundles quickly and efficiently. Small and medium-sized enterprises (SMEs) are particularly inclined toward these platforms due to transparent pricing and streamlined procurement processes. At the same time, initiatives like Cisco’s evolving partner strategy reflect a broader industry transition, where traditional resellers are being repositioned toward higher-value services as transactional sales increasingly migrate to digital channels.

By End-User Industry: Healthcare Accelerates Beyond Early-Adopter Status

IT and telecommunications companies accounted for the largest share of spending in 2025, contributing 28.64% of the market, driven by the need to support always-on customer service centers and deliver managed unified communications (UC) services. Meanwhile, the healthcare and life sciences sector is emerging as the fastest-growing segment, projected to expand at a CAGR of 10.72%. This growth is fueled by the stabilization of telehealth reimbursement frameworks and stricter compliance requirements, such as HIPAA, which are pushing healthcare providers to adopt secure, encrypted, and standards-based video communication solutions.

In other sectors, BFSI institutions are prioritizing investments in security-hardened devices equipped with audit trails to meet regulatory and compliance needs. Retail organizations are increasingly deploying video kiosks to facilitate virtual customer interactions and consultations. At the same time, the education sector continues to invest in hybrid learning environments that seamlessly integrate in-person and remote participation. This sustained demand is driving the adoption of all-in-one interactive boards and AI-powered cameras that simplify lecture capture and reduce technical complexity.

By Organization Size: SMEs Take Center Stage for Future Expansion

Large enterprises accounted for 71.53% of the Unified Communications (UC) hardware market in 2025, supported by their extensive office footprints, complex communication needs, and strict compliance requirements. In contrast, small and medium-sized enterprises (SMEs) are expected to grow faster, with a projected CAGR of 11.67% through 2031, indicating a gradual shift in demand toward smaller organizations.

This growth among SMEs is driven by the increasing adoption of subscription-based UCaaS bundles that include pre-configured headsets and video bars, reducing the need for high upfront capital investment. Jabra exemplifies this trend with its Evolve3 headset line, launched globally in March 2026, which offers advanced features such as boomless AI microphones and replaceable batteries at accessible price points for smaller businesses.[4]Jabra, “Jabra Expands Meeting Room Portfolio with the Launch of Jabra Scheduler,” jabra.com Combined with faster procurement cycles and more flexible purchasing approaches, SMEs are expected to become the primary volume drivers in the UC hardware market over the next five years.

Geography Analysis

North America captured 34.82% revenue share in 2025, buoyed by robust enterprise refresh cycles and the FCC’s all-IP modernization agenda. United States enterprises continue to prioritize AI-infused devices that meet stringent security guidelines, while Canada’s strong public-sector demand complements corporate spending. Mexico benefits from cross-border supply-chain integration and USMCA incentives that encourage nearshoring of assembly operations.

Asia-Pacific is projected to record the fastest regional growth at an 11.92% CAGR between 2026-2031. China’s sovereign AI push and city-level smart-office mandates favor domestic champions such as Huawei and ZTE. India’s tier-2 cities are emerging hotspots as government-led digitization programs extend fiber connectivity to municipal buildings and schools. Japan and South Korea leverage mature 5G networks to roll out mobile-centric collaboration solutions, while Australia relies on ruggedized, satellite-ready gear to support mining and energy installations spread across vast distances.

Europe’s outlook is uniquely shaped by the United Kingdom’s January 2027 PSTN switch-off, which is generating staggered procurement spikes as enterprises replace copper-dependent devices. Germany and France are next in scale, although strict GDPR requirements tilt demand toward hybrid or on-premises architectures. South American growth is clustered in Brazil and Argentina, where improved broadband is allowing SMEs to leapfrog directly to cloud-native UC. In the Middle East, Saudi Arabia’s national AI plan and Expo-driven infrastructure upgrades create lumpy but lucrative tenders, while Africa remains an early-stage opportunity concentrated in South Africa, Nigeria, and Kenya.

Competitive Landscape

The Unified Communications Hardware market shows moderate concentration. Cisco Systems, Avaya, Poly (HP Inc.), and Logitech anchor the premium tier through wide portfolios and deep platform partnerships. Their combined share approaches two-thirds of global revenue, yet cost-advantaged players such as Yealink and Huawei consistently undercut pricing by 30-40% on desk phones and video bars.

Defensive strategies now prioritize software differentiation and recurring revenue. Cisco’s November 2025 acquisition of EzDubs brings real-time translation into the Webex ecosystem, transforming language inclusivity into a hardware-agnostic service.[5]Cisco, “Cisco completes EzDubs acquisition,” cisco.com Avaya’s Nexus platform, scheduled for Q4 2026, targets mission-critical verticals with carrier-grade redundancy and encrypted media paths. Logitech focuses on AI-camera innovation to protect its stronghold in conference rooms, while Jabra expands room systems that dovetail with its headset dominance.

Interoperability certifications have become table stakes. Vendors chase Microsoft Teams Rooms and Zoom Rooms badges to assure buyers that a single hardware SKU can survive platform shifts. At the edge, partnerships with NVIDIA and AMD for on-device AI acceleration are rewriting hardware roadmaps. The competitive gap therefore hinges less on megapixels or SIP ports and more on embedded silicon, cloud APIs, and lifecycle management software that transforms static devices into analytics-rich endpoints.

Unified Communications (UC) Hardware Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

HP, Inc.

Mitel Networks Corporation

NEC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Avaya announced the Avaya Nexus mission-critical voice platform for regulated industries, featuring always-on architecture and encrypted deployments, with general availability slated for Q4 2026.

- February 2026: Yealink deepened its Microsoft alliance via the Device Ecosystem Platform to advance hybrid-work hardware optimized for Teams environments.

- February 2026: Jabra unveiled PanaCast Room Kits with scalable camera configurations and AI-driven multi-camera tracking, shipping in Q2 2026.

- January 2026: Logitech introduced Rally AI Camera and Rally AI Camera Pro with 15x hybrid zoom and adaptive framing, launching in spring and summer 2026.

Global Unified Communications (UC) Hardware Market Report Scope

The Unified Communications (UC) Hardware Market comprises physical devices and infrastructure components that enable integrated enterprise communication across voice, video, messaging, and collaboration platforms. This includes endpoints such as IP phones, video conferencing systems, headsets, collaboration bars, and room kits, as well as supporting hardware such as UC gateways and networking infrastructure that facilitate seamless communication across IP networks.

The Unified Communications (UC) Hardware Market Report is Segmented by Hardware Type (IP Telephony Hardware, Video Conferencing Systems, UC Gateways and Infrastructure Hardware, Headsets and Audio Devices, Collaboration Bars/Room Kits, and Other Hardware Types), Distribution Model (Offline, and Online), End-user Industry (IT and Telecommunication, BFSI, Healthcare and Life Sciences, Retail and Consumer Goods, Education, Government and Public Sector, Manufacturing, Media and Entertainment, and Other Industry Verticals), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| IP Telephony Hardware |

| Video Conferencing Systems |

| UC Gateways and Infrastructure Hardware |

| Headsets and Audio Devices |

| Collaboration Bars/Room Kits |

| Other Hardware Types |

| Offline |

| Online |

| IT and Telecommunication |

| BFSI |

| Healthcare and Lifesciences |

| Retail and Consumer Goods |

| Education |

| Government and Public Sector |

| Manufacturing |

| Media and Entertainment |

| Other Industry Verticals |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Hardware Type | IP Telephony Hardware | |

| Video Conferencing Systems | ||

| UC Gateways and Infrastructure Hardware | ||

| Headsets and Audio Devices | ||

| Collaboration Bars/Room Kits | ||

| Other Hardware Types | ||

| By Distribution Model | Offline | |

| Online | ||

| By End-user Industry | IT and Telecommunication | |

| BFSI | ||

| Healthcare and Lifesciences | ||

| Retail and Consumer Goods | ||

| Education | ||

| Government and Public Sector | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Other Industry Verticals | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Unified Communications (UC) Hardware market?

It stands at USD 20.21 billion in 2026, advancing toward USD 31.63 billion by 2031.

How fast is video conferencing hardware growing?

Video conferencing systems are projected to register an 11.24% CAGR from 2026-2031.

Which region is expanding the quickest?

Asia-Pacific is forecast to lead with an 11.92% CAGR through 2031 thanks to large-scale digitization programs.

Why are SMEs important to future demand?

Subscription bundles that eliminate upfront capital make it easier for SMEs to adopt enterprise-grade devices, driving an 11.67% CAGR in that segment.

What security measures are enterprises demanding in UC hardware?

Buyers now require hardware-root-of-trust, end-to-end encryption, and compliance with ISO 27001 and SOC 2 following high-profile SIP vulnerabilities.

Page last updated on: