Size and Share of Unified Communications-as-a-Service Market in Healthcare

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

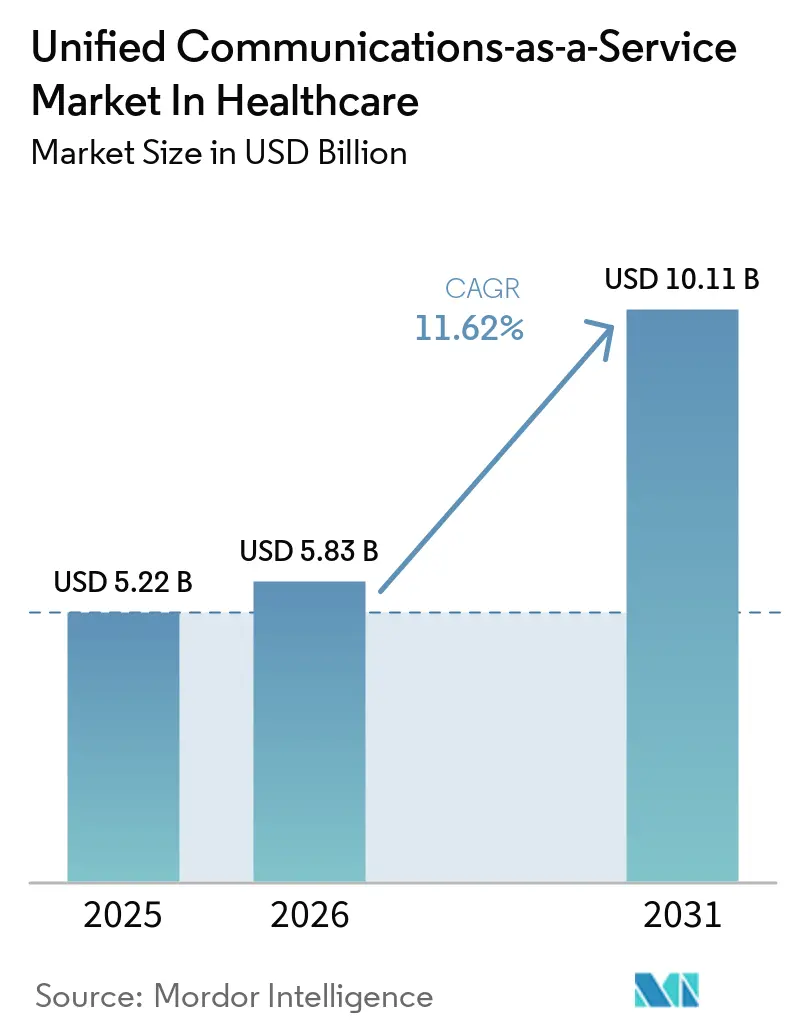

| Market Size (2026) | USD 5.83 Billion |

| Market Size (2031) | USD 10.11 Billion |

| Growth Rate (2026 - 2031) | 11.62% CAGR |

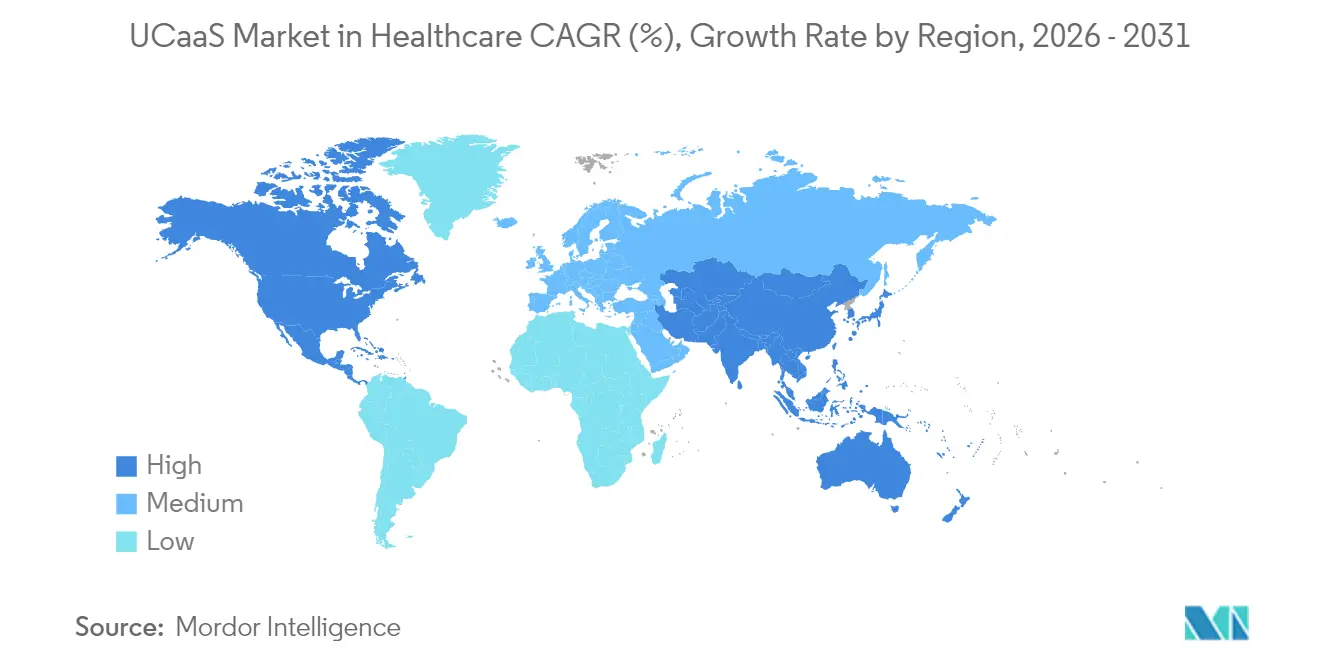

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

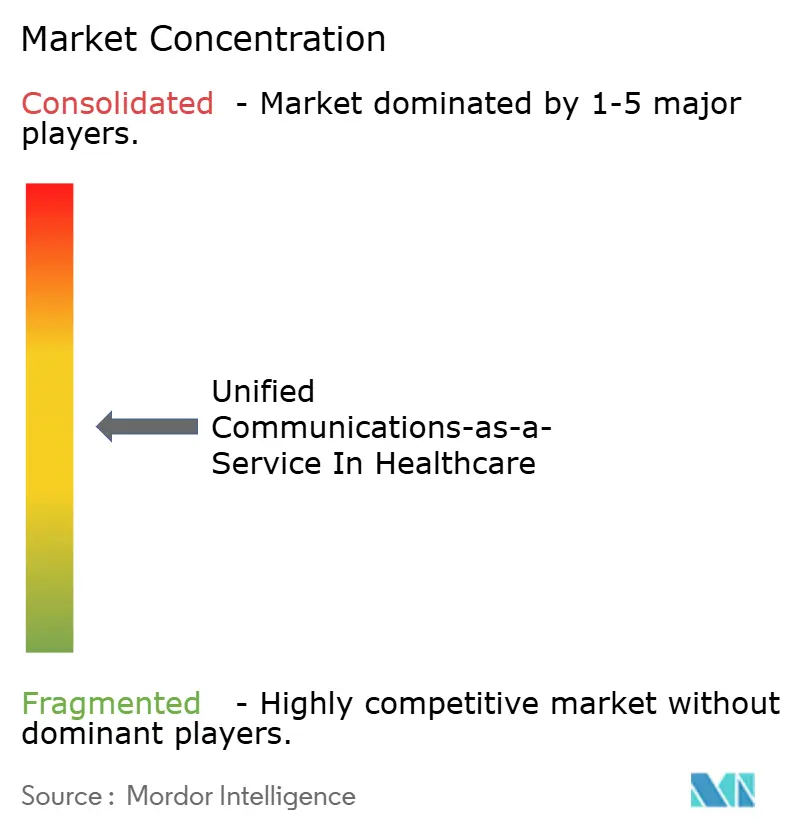

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Unified Communications-as-a-Service Market in Healthcare by Mordor Intelligence

Unified Communications-as-a-Service in Healthcare market size in 2026 is estimated at USD 5.83 billion, growing from 2025 value of USD 5.22 billion with 2031 projections showing USD 10.11 billion, growing at 11.62% CAGR over 2026-2031. The expansion reflects hospitals, clinics, and home-care agencies replacing on-premises PBX equipment with cloud platforms that unify voice, video, messaging, and collaboration in HIPAA-compliant environments. Measurable benefits such as a 211% three-year ROI and a 45% fall in average call-handling time have validated the business case, encouraging rapid budget reallocations toward cloud communications.[1]RingCentral, “Forrester Study: 211% ROI,” ringcentral.com Momentum is further reinforced by 5G-enabled edge use cases, AI-assisted clinical documentation, and a steady rise in hybrid care models that rely on always-on connectivity. North America leads adoption through mature EHR integration, whereas Asia-Pacific records the fastest growth as public-sector digitization initiatives subsidize telehealth infrastructure. Cyber-security, compliance complexity, and legacy PBX inertia remain headwinds, yet the overall trajectory continues upward as platforms demonstrate clear productivity gains and patient-safety improvements.

Key Report Takeaways

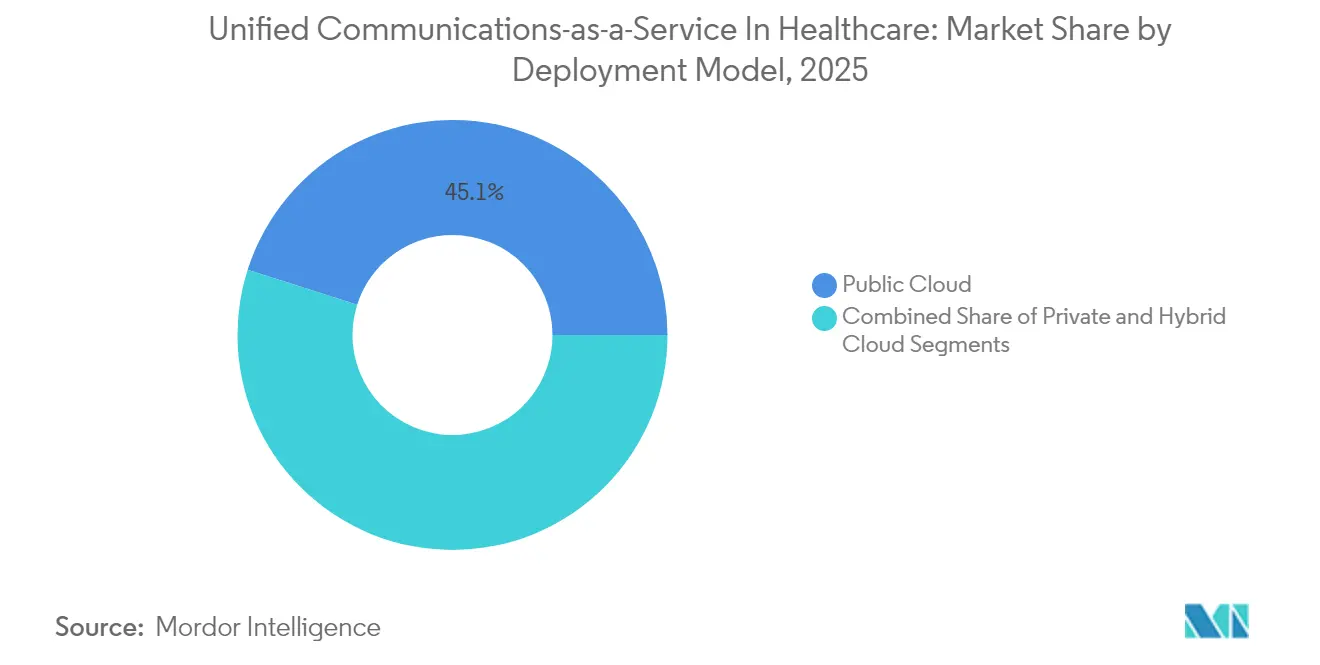

- By deployment model, the Public Cloud segment led with 45.10% of Unified Communications-as-a-Service in Healthcare market share in 2025; the Hybrid Cloud segment is projected to expand at a 16.70% CAGR through 2031.

- By component, Telephony/Voice captured 26.60% revenue share in 2025, while Collaboration Tools post the highest projected CAGR at 17.90% through 2031.

- By application, Clinical Communications and Collaboration accounted for a 33.40% share of the Unified Communications-as-a-Service in Healthcare market size in 2025; Tele-health & Virtual Care is advancing at a 20.90% CAGR to 2031.

- By organization size, large enterprises held a 69.40% share of the Unified Communications-as-a-Service in Healthcare market in 2025, whereas SMEs are forecast to grow at a 14.90% CAGR during 2026-2031.

- By end-user, Hospitals commanded 40.70% share of the Unified Communications-as-a-Service in Healthcare market in 2025; Home Healthcare Agencies register the fastest growth at 18.80% CAGR through 2031.

- By geography, North America led with 35.90% share in 2025, while Asia-Pacific records the highest regional CAGR at 13.40% over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Unified Communications-as-a-Service Market in Healthcare

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tele-health expansion post-COVID-19 | +3.2% | Global (North America, Europe lead) | Medium term (2-4 years) |

| Cost-saving OPEX model of UCaaS | +2.8% | Global, cost-sensitive markets | Short term (≤ 2 years) |

| Integration with EHR and clinical workflows | +2.5% | North America, Europe | Medium term (2-4 years) |

| 5G edge-enabled AR surgical collaboration | +1.8% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Compliance-as-a-Service bundles for HIPAA | +1.5% | North America, expanding to Europe | Short term (≤ 2 years) |

| AI-driven clinical documentation & workflow automation | +1.6% | North America, Europe, early adopters in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tele-health Expansion Post-COVID-19

Elevated telehealth volumes have stabilized, pushing providers to consolidate voice, video, and remote-monitoring traffic onto single platforms. Average cost per encounter in virtual care is falling by up to 17%, and caregivers report higher job satisfaction when workflows remain inside one secure environment.[2]HomeCare Magazine, “Telehealth Adoption Benefits,” homecaremag.com Providers now contract “virtualist” physicians who practice exclusively online, requiring continuous, HIPAA-grade connectivity for hand-offs and escalations. Integration of predictive analytics and AI-driven triage elevates tele-consultations from episodic events to longitudinal care pathways. Demand for contextual messaging within electronic health records (EHRs) grows in parallel, underpinning fresh opportunities for UCaaS vendors that can certify interoperability.

Cost-Saving OPEX Model of UCaaS

Switching from capital-intensive PBX hardware to subscription-based UCaaS frees cash for patient-centric investments. A 40-site community health network saved USD 350,000 annually after migrating 2,000 employees to RingCentral, an outcome echoed across multi-facility systems looking to trim support overhead. The operating-expense structure removes large refresh cycles, aligning expenses with fluctuating patient volumes. CFOs under pressure from value-based reimbursement find predictable monthly fees preferable to lumpy capital outlays. Smaller practices benefit most because cloud providers assume maintenance, security patching, and disaster recovery, lowering the personnel barrier to enterprise-class communications.

Integration with EHR & Clinical Workflows

Context-aware messaging embedded in EHR interfaces eliminates duplicate data entry and reduces miscommunication. A tertiary hospital cut consult time from 50 minutes to as little as 3 minutes after embedding calling, secure chat, and file-share links directly in its Cerner deployment. APIs expose patient metadata inside call pop-ups, enabling rapid triage and fewer transcription errors. Automated routing of lab results and care-team notifications decreases readmission risk, while audit trails satisfy HIPAA logging mandates. Demand is shifting toward vendors shipping pre-built connectors for Epic, Cerner, and Meditech rather than selling generic APIs that require custom coding.

5G Edge-Enabled AR Surgical Collaboration

Pilot procedures have proven the feasibility of remote, real-time surgical mentoring via 5G networks. In one case, surgeons performed a thyroidectomy with remote guidance over 5G links featuring sub-50 millisecond latency. Edge nodes process imaging locally, while augmented-reality overlays travel upstream for remote specialists. Rural hospitals leverage this architecture to avoid patient transfers and to expand service lines without hiring on-site subspecialists. Growth in Asia-Pacific is pronounced as public-private consortia finance 5G smart-hospital corridors. Long-term impact will surface once payers ratify reimbursement schedules for remote surgical support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security & HIPAA concerns | -2.1% | North America primarily, expanding globally | Short term (≤ 2 years) |

| Legacy PBX & low digital readiness | -1.8% | Global, smaller facilities | Medium term (2-4 years) |

| Budget squeeze from value-based care | -1.4% | North America, Europe | Medium term (2-4 years) |

| Vendor lock-in with vertical UC stacks | -1.2% | Global, multi-facility systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Security and HIPAA Concerns Create Adoption Barriers

Encrypting data at rest and in transit, enforcing granular access controls, and signing business-associate agreements add cost and delay. Smaller clinics report six-to-twelve-month project slippage while security teams validate cloud architectures and map data flows. Breach penalties can exceed USD 1.5 million per incident, elevating risk perception and driving preference for incumbents with long compliance track records. Multi-tenant clouds intensify worries about co-mingling patient records, spurring interest in hybrid and dedicated instances despite higher price points.

Legacy PBX and Low Digital Readiness Constrain Migration

Fax machines and analog phones remain embedded in clinical workflows, with 75% of pre-pandemic communication still traveling over fax. Converting these paths demands cultural as well as technical change. Providers must protect business-critical contact channels during cut-over periods, which often requires dual-running old and new systems. Rural hospitals lacking in-house IT staff outsource migration, inflating cost and hindering pace. Custom protocol adaptors needed for pager, nurse-call, and alarm systems further complicate total-cost assessments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Cloud Balances Scalability and Control

Public Cloud dominated 2025 with 45.10% share of the Unified Communications-as-a-Service in Healthcare market, reflecting preference for on-demand scalability and automatic software updates. Large integrated-delivery networks tap global data centers to support geographically dispersed care teams, while start-ups exploit pay-as-you-go pricing to sidestep capital outlays. Hybrid Cloud trajectories are set to compound at 16.70% CAGR, the fastest within the deployment category, as privacy policies and data-sovereignty laws force providers to retain clinical databases in local vaults. The Unified Communications-as-a-Service in Healthcare market size for Hybrid Cloud is projected to reach USD 6.62 billion by 2031. Providers typically host call-detail records and recordings on-premises while offloading real-time workloads to the cloud. The arrangement mitigates latency for on-site emergency codes and integrates with elevators, alarms, and medical-device gateways that remain behind hospital firewalls.

Demand for Private Cloud remains niche, concentrated in academic medical centers conducting high-risk clinical trials or operating under national defense constraints. These deployments attract higher total cost due to dedicated hardware and carrier circuits. Nonetheless, managed-service options that bundle security appliances and 24×7 monitoring are lowering entry barriers. Some providers adopt a phased approach: migrate non-clinical departments such as HR and billing to Public Cloud first, then shift patient-facing workloads once governance models mature.

By Component: Collaboration Tools Surpass Voice in Growth Momentum

Telephony/Voice retained 26.60% share in 2025, underlining voice’s enduring role for code calls, consults, and switchboard operations. However, Collaboration Tools hold the growth spotlight with an 17.90% CAGR. Across multidisciplinary team huddles, clinicians now prefer persistent chat rooms, file-share spaces, and video huddle portals embedded inside their EHR cockpit. The Unified Communications-as-a-Service in Healthcare market share for Collaboration Tools is forecast to exceed 31.80% by 2031. Vendors differentiate by embedding note-taking AI, automatic language translation, and virtual whiteboards that map directly to patient records.

Unified Messaging converges voicemail, email, and SMS into one queue, easing information scatter. Conferencing solutions integrate high-definition camera carts and stethoscope peripherals for virtual rounding. Contact-Center Integration remains pivotal to omni-channel patient engagement, routing lab results, appointment reminders, and pharmacy queries through a unified queue. Momentum here climbs as providers emphasize consumer-grade experience to retain patients under value-based reimbursement.

By Application: Tele-health and Virtual Care Surges Ahead

Clinical Communications and Collaboration led 2025 with a 33.40% slice, serving urgent messaging, secure file exchange, and role-based alerting inside hospitals. Tele-health and Virtual Care applications march forward at a 20.90% CAGR, lifting the Unified Communications-as-a-Service (UCaaS) in Healthcare market size for this sub-segment to USD 4.05 billion by 2031. Drivers include chronic-care management programs that rely on video follow-ups and remote-patient-monitoring dashboards, as well as payer reimbursement parity for virtual visits in major markets.

Administrative and Billing workflows use UCaaS to automate insurance verification, co-pay collection, and claims follow-up, lowering days in accounts receivable. Emergency Response Coordination leverages mass-notification modules to mobilize code teams and publish disaster advisories. Patient Outreach and Engagement automates vaccination reminders, medication adherence nudges, and lifestyle coaching, demonstrating improved satisfaction metrics in CAHPS surveys.

By Organization Size: Small Practices Accelerate Cloud Migration

Large Enterprises (≥1,000 beds) wield 69.40% share through complex vendor frameworks that embed UCaaS within multi-site call flows. These institutions prioritize uptime SLAs, geo-redundant failover, and advanced analytics. In contrast, SMEs post the swiftest expansion at 14.90% CAGR as subscription bundles democratize enterprise functions. The Unified Communications-as-a-Service in Healthcare market share among Small Practices is on track to surpass 21.70% by 2031.

Cloud auto-provisioning scripts now let a two-physician clinic activate softphones, SMS, and telehealth extensions in minutes. Smaller providers use these tools to compete with larger systems through quicker appointment scheduling and broader after-hours coverage. Medium Enterprises occupy the middle ground, adopting phased migrations to maintain budget discipline while modernizing auxiliary facilities such as imaging centers.

By End-User: Home Healthcare Agencies Transform Delivery Models

Hospitals retained 40.70% share in 2025 ahead of any other end-user group. They require enterprise-grade security, redundant trunks, and nurse call integrations. Home Healthcare Agencies grow fastest at 18.80% CAGR, propelled by aging demographics, payer incentives for home-based care, and the need for continuous triage from field nurses. The Unified Communications-as-a-Service in Healthcare market size allocated to home care is projected to triple by 2031 as agencies expand coverage areas without adding brick-and-mortar branches.

Clinics and Physician Offices exploit auto-attendant features to triage incoming calls. Ambulatory Surgical Centers integrate high-definition video with peri-operative dashboards for same-day discharge coordination. Long-Term Care Facilities prioritize fall-detection alerts, while Diagnostic and Imaging Centers embed appointment confirmations and results delivery via secure messaging.

Geography Analysis

North America contributed 35.90% of 2025 revenue, driven by entrenched HIPAA mandates, EHR ubiquity, and aggressive AI pilots. Microsoft’s DAX Copilot is live in 400+ provider networks, generating 9.5 million encounter notes and validating clinical-grade speech recognition at scale. Providers leverage mature broadband and 5G coverage for in-unit teleconsults and cross-facility resource pooling. Federal flexibilities for telehealth reimbursement, extended through 2026, further entrench cloud reliance.

Asia-Pacific leads in growth momentum at 13.40% CAGR. Public-sector smart-hospital pilots in Thailand, South Korea, and China exemplify 5G-enabled ambulance telemetry and AI-based triage that slash imaging turnaround from 15 minutes to 25 seconds. Regionally diverse privacy laws cultivate demand for configurable data-residency settings and bring-your-own-carrier options inside UCaaS stacks. Local system integrators bundle compliance consultancy, making adoption less daunting for mid-tier clinics.

Europe holds steady mid-single-digit growth underpinned by eHealth initiatives and cross-border data-sharing goals in the European Health Data Space. France’s tele-consult legislation expanded remote-work eligibility for clinicians, fueling demand for secure video channels. GDPR obligations push interest in hybrid deployments, where communication payloads remain inside regional data centers. Vendor roadmaps increasingly reference “Schrems-II ready” architectures to court public hospitals.

Competitive Landscape

The market is moderately fragmented, with enterprise communication giants and niche specialists vying for healthcare wallet share. Microsoft, Cisco, and RingCentral leverage broad cloud fabrics and AI pipelines to target large health systems, bundling voice, meetings, and machine-learning transcription. Cisco’s USD 28 billion Splunk acquisition injected observability and threat-detection DNA into its platform, elevating its appeal to risk-averse hospital IT teams. TigerConnect retains leadership in pure-play clinical communication, serving more than 7,000 facilities with workflow-optimized interfaces.

Strategic partnerships drive differentiation. RingCentral couples with Zayo for resilient fiber underlays while co-developing HIPAA-ready workforce-engagement betas with Verint. 8x8’s tie-up with SpinSci embeds AI chatbots into Epic and Cerner modules, shaving 43 seconds from each patient-verification call and yielding six hours of staff time savings daily. Market entrants tout AI-generated discharge summaries and automated prior-authorization calls as white-space innovations.

Price pressure intensifies amid vendor convergence on feature parity. Providers weigh migration costs, integration depth, and roadmap transparency over raw licensing price. Reference architectures that showcase tangible productivity gains such as note-taking AI or edge-optimized video quality wield outsized influence on purchase decisions. As consolidation continues, top-tier vendors are expected to acquire niche cloud-security or workflow-automation specialists to round out offerings.

Leaders of Unified Communications-as-a-Service Market in Healthcare

Ring Central Inc.

8X8 Inc.

Verizon Communications Inc.

Comcast Corporation

Vonage Holdings Inc. (Ericsson)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: 8x8 launched AI Orchestrator to blend decision flows across multiple AI bots, bolstering patient-engagement automation in Epic workflows.

- March 2025: 8x8 earned a 5-Star rating in the CRN 2025 Partner Program Guide, underscoring its channel-first expansion in healthcare.

- February 2025: 8x8 partnered with SpinSci to inject EHR-aware patient-assist automation into its contact-center suite, saving providers six hours of daily staff time.

- February 2025: Zoom invested in Suki to enrich clinician documentation with voice AI, expanding its healthcare footprint.

Scope of Report on Unified Communications-as-a-Service Market in Healthcare

The Unified Communications-As-A-Service in Healthcare Report is Segmented by Deployment Model (Public Cloud, Private, Cloud, and Hybrid Cloud), Component (Telephony / Voice, Unified Messaging, Conferencing, Collaboration Tools, and Contact-Center Integration), Application (Clinical Communications and Collaboration, Tele-Health and Virtual Care, Administrative and Billing, Emergency Response Coordination, and Patient Outreach and Engagement), Organization Size (Large Enterprises, and Small and Medium Enterprises ), End-User (Hospitals, Clinics and Physician Offices, Ambulatory Surgical Centers, Long-Term Care Facilities, Diagnostic and Imaging Centers, and Home Healthcare Agencies), and Geography (North America, Europe, South America, Asia Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Telephony / Voice |

| Unified Messaging |

| Conferencing |

| Collaboration Tools |

| Contact-Center Integration |

| Clinical Communications and Collaboration |

| Tele-health and Virtual Care |

| Administrative and Billing |

| Emergency Response Coordination |

| Patient Outreach and Engagement |

| Large Enterprises |

| Small and Medium Enterprises |

| Hospitals |

| Clinics and Physician Offices |

| Ambulatory Surgical Centers |

| Long-Term Care Facilities |

| Diagnostic and Imaging Centers |

| Home Healthcare Agencies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Component | Telephony / Voice | ||

| Unified Messaging | |||

| Conferencing | |||

| Collaboration Tools | |||

| Contact-Center Integration | |||

| By Application | Clinical Communications and Collaboration | ||

| Tele-health and Virtual Care | |||

| Administrative and Billing | |||

| Emergency Response Coordination | |||

| Patient Outreach and Engagement | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-User | Hospitals | ||

| Clinics and Physician Offices | |||

| Ambulatory Surgical Centers | |||

| Long-Term Care Facilities | |||

| Diagnostic and Imaging Centers | |||

| Home Healthcare Agencies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current Unified Communications-as-a-Service in Healthcare market size?

The market is valued at USD 5.83 billion in 2026.

How fast will the Unified Communications-as-a-Service in Healthcare market grow through 2031?

It is forecast to expand at an 11.62% CAGR, reaching USD 10.11 billion by 2031.

Which deployment model shows the highest growth?

Hybrid Cloud records the fastest trajectory at a 16.70% CAGR.

Which application area is expanding quickest?

Tele-health and Virtual Care leads with a 20.90% CAGR as virtual care becomes mainstream.

Page last updated on: