Unified Communications And Collaboration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

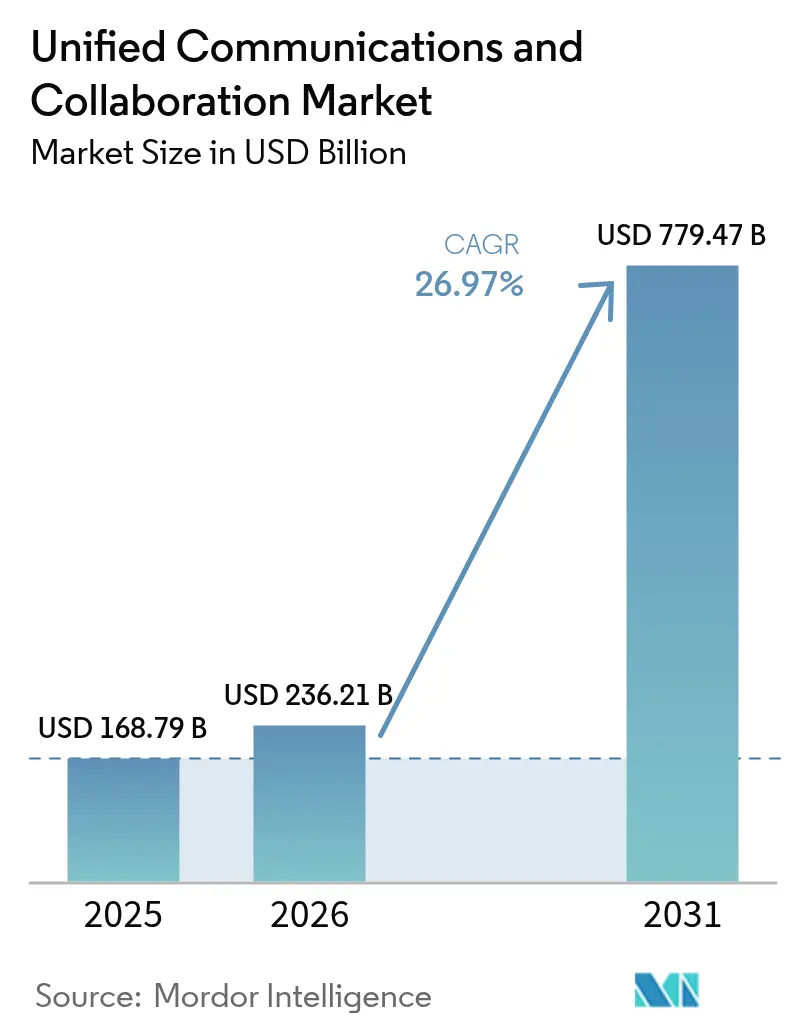

| Market Size (2026) | USD 236.21 Billion |

| Market Size (2031) | USD 779.47 Billion |

| Growth Rate (2026 - 2031) | 26.97% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unified Communications And Collaboration Market Analysis by Mordor Intelligence

The Unified Communications and Collaboration market size was valued at USD 168.79 billion in 2025 and estimated to grow from USD 236.21 billion in 2026 to reach USD 779.47 billion by 2031, at a CAGR of 26.97% during the forecast period (2026-2031). Rapid enterprise migration from legacy PBX systems to cloud-native platforms, the rollout of hybrid work policies, and the mainstreaming of generative AI within collaboration suites are reshaping spending priorities. Platform stickiness is rising because bundled suites reduce licensing complexity and enable unified governance across voice, video, messaging, and content sharing. Vendor roadmaps now center on vertical compliance certifications, deeper workflow integrations, and AI features that automate meeting tasks. Competitive activity is intensifying as hyperscale cloud providers bundle collaboration with infrastructure services, while specialized vendors defend share through domain-specific capabilities and ecosystem partnerships.

Key Report Takeaways

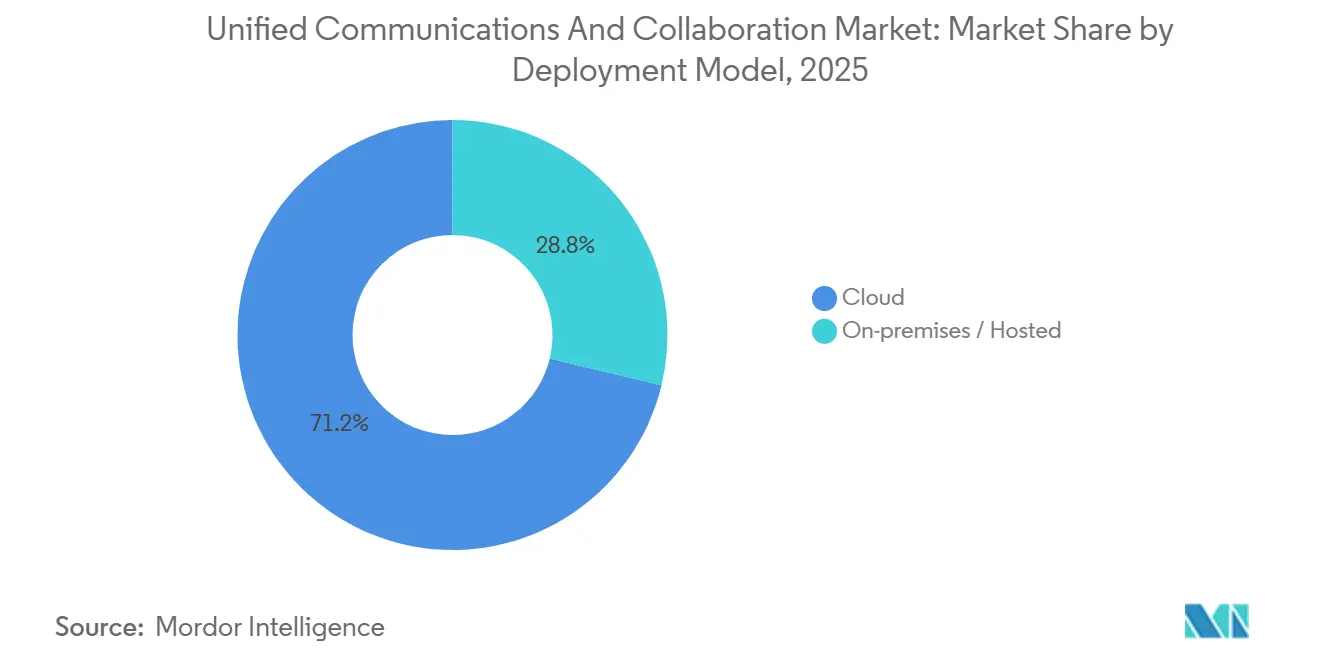

- By deployment model, cloud deployments held 71.23% of the Unified Communications and Collaboration market share in 2025 and are projected to advance at a 26.99% CAGR through 2031.

- By component, video conferencing led with 36.43% revenue share in 2025. Collaboration and content sharing tools are forecast to expand at a 27.84% CAGR to 2031.

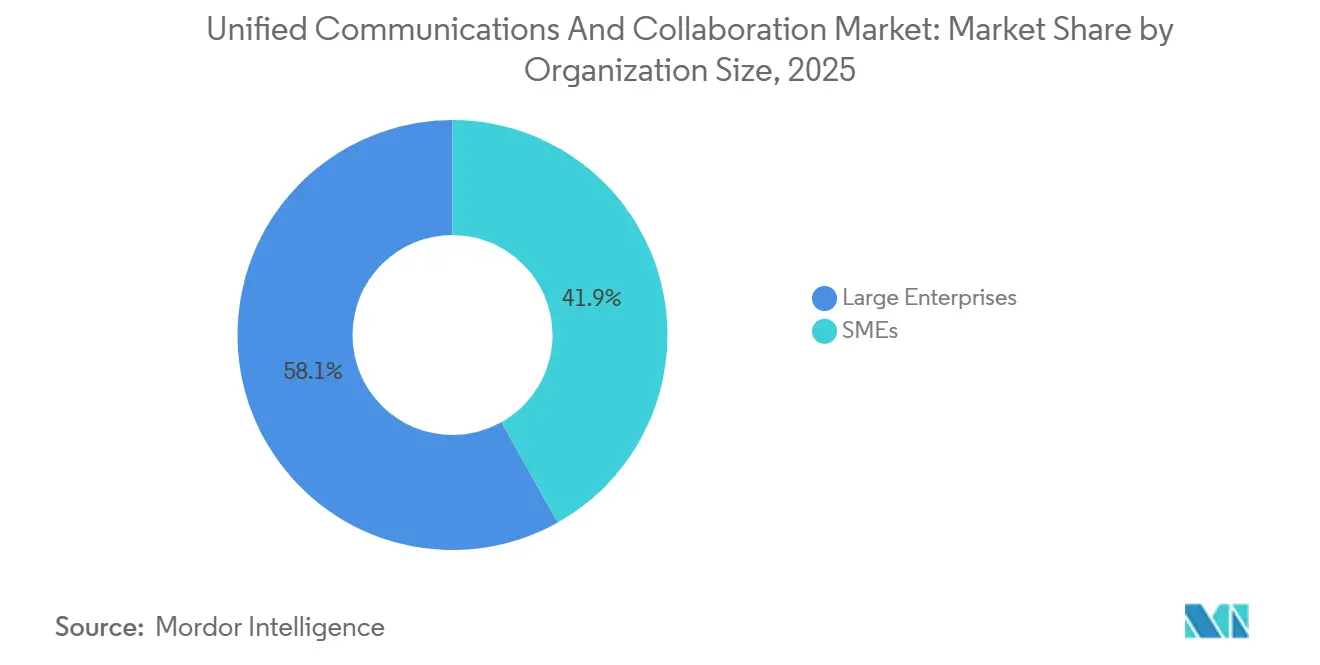

- By organization size, large enterprises accounted for 58.14% of 2025 spending. Small and medium-sized enterprises are expected to grow at a 27.15% CAGR over 2026-2031.

- By end-user industry, the IT and telecom segment commanded 24.76% revenue share in 2025. Healthcare and life sciences is projected to post the fastest 28.11% CAGR to 2031.

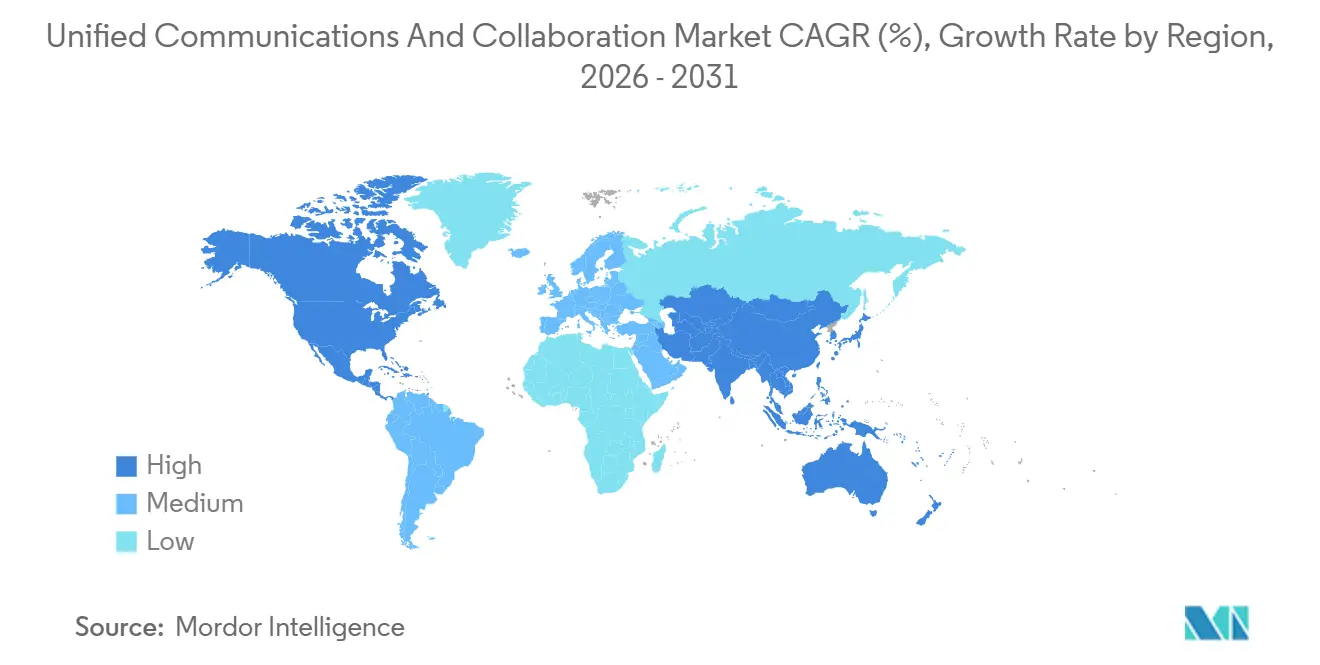

- By geography, North America retained 38.41% revenue share in 2025. Asia-Pacific is set to register the highest 27.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Unified Communications And Collaboration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid Work Demand Accelerates UCaaS Migration | +6.8% | Global, with concentration in North America, Western Europe, and Asia-Pacific urban centers | Short term (≤ 2 years) |

| AI-Augmented Meeting Productivity and Automation Tools | +5.9% | Global, early adoption in North America and Europe, rapid scaling in the Asia-Pacific | Medium term (2-4 years) |

| UC-CCaaS Convergence to Streamline Customer Experience | +4.7% | North America, Europe, and the Asia-Pacific financial services and retail hubs | Medium term (2-4 years) |

| 5G and Edge Computing Enable Low-Latency Immersive Collaboration | +4.2% | Asia-Pacific core (China, South Korea, Japan), spillover to the Middle East and North America | Long term (≥ 4 years) |

| Vertical-Specific Workflow Integration, e.g., Telehealth UC Kits | +3.6% | North America and Europe's healthcare systems, emerging in the Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Sustainability Mandates Favor Energy-Efficient Cloud UC Solutions | +2.5% | Europe (EU Green Deal), North America (corporate ESG commitments), and selective Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work Demand Accelerates UCaaS Migration

Permanent hybrid policies are pushing enterprises to retire on-premises telephony and adopt cloud platforms that deliver consistent experiences across office, home, and mobile endpoints. Gallup found 53% of global knowledge workers operated in hybrid arrangements during 2024. Microsoft Teams Phone surpassed 14 million seats by mid-2025, signaling consolidation of telephony and collaboration on a single platform. Professional services and financial firms are accelerating their moves to the cloud because real estate rationalization plans rely on robust remote communication infrastructure.

AI-Augmented Meeting Productivity and Automation Tools

Generative AI is turning collaboration suites into active productivity engines that draft meeting summaries, action items, and follow-up emails. Zoom’s AI Companion 3.0 reduced post-meeting administrative workload by 30% in early pilots.[1]Zoom Video Communications, “AI Companion 3.0 Product Release,” Zoom, zoom.com Microsoft Teams Intelligent Recap auto-creates timestamped chapters and task lists using Azure OpenAI. Google Meet now offers real-time translation across 69 languages, widening accessibility. As these capabilities become baseline, vendors without proprietary AI risk margin compression.

UC-CCaaS Convergence to Streamline Customer Experience

Enterprises are fusing employee collaboration with contact center platforms to eliminate data silos. RingCentral’s Customer Journey Analytics cut average handle time by 18% in financial-services pilots by embedding customer history into the agent workspace.[2]RingCentral, “Customer Journey Analytics Platform Launch,” RingCentral, ringcentral.com Five9’s deeper Teams integration allows live escalation to internal experts without transferring callers. Unified governance also helps firms satisfy SEC Rule 17a-4 and FINRA retention mandates, making converged suites attractive in regulated sectors.

5G and Edge Computing Enable Low-Latency Immersive Collaboration

Standalone 5G and edge-compute nodes are lowering round-trip latency to sub-20 milliseconds, unlocking real-time AR collaboration and 4K mobile video. T-Mobile’s Edge Control platform achieved a 60% reduction in latency compared to centralized clouds in 2025 field tests.[3]T-Mobile, “Edge Control Platform for Enterprise,” T-Mobile Business, t-mobile.com Verizon’s Private MEC offering pairs with Microsoft Teams and Cisco Webex to guarantee quality of service in hospitals and logistics hubs. These early deployments foreshadow widescale adoption in Asia-Pacific where dense populations make edge economics compelling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Security and Compliance Requirements Slow Adoption | -3.4% | Global, acute in North America and Europe (GDPR, HIPAA), emerging in Asia-Pacific (China Cybersecurity Law, India data localization) | Short term (≤ 2 years) |

| Legacy System Integration Complexity and High Switching Costs | -2.9% | North America and Europe incumbent enterprises, selective Asia-Pacific markets with aging infrastructure | Medium term (2-4 years) |

| Telecom-API Commoditization Squeezing Provider Margins | -1.8% | Global, most pronounced in North America and Europe competitive markets | Medium term (2-4 years) |

| Regional Data-Sovereignty Fragmentation Inflates Operating Costs | -1.6% | Europe (GDPR), China (Cybersecurity Law), India (data localization), Brazil (LGPD), Russia (Federal Law 242-FZ) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Security and Compliance Requirements Slow Adoption

Before launching telehealth services, healthcare providers are increasingly seeking HIPAA-certified platforms that offer detailed and robust privacy controls, thereby significantly narrowing their choice of vendors. These stringent requirements ensure compliance with healthcare regulations and safeguard sensitive patient data. Financial institutions, adhering to SEC Rule 17a-4, are required to maintain unchangeable and secure archives, a mandate that extends their procurement timelines by several months due to the complexity of implementation and verification processes. With the introduction of the new ISO/IEC 27701:2025 privacy controls, the stakes for compliance and data protection have been elevated further. As a result, vendor risk assessments for real-time communications now average nine months, a significant increase from the four months typically allocated for standard SaaS workloads. This extended timeline reflects the growing emphasis on privacy, security, and regulatory adherence in the evolving digital landscape.

Legacy System Integration Complexity and High Switching Costs

Enterprises managing extensive PBX systems frequently operate dual setups for over a year during transitions, leading to doubled expenses and heightened professional service fees. This prolonged period of parallel system operation significantly increases the overall costs associated with the migration process. Mitel noted that large deployments typically take an average of 14 months for cutovers, reflecting the complexity and scale of such transitions. Avaya highlighted that organizations with over 10,000 endpoints face average switching costs of USD 8.5 million, a figure that includes considerations for training, productivity lags, and other associated expenses. These substantial financial implications often delay migrations, particularly in capital-restrained settings where budgetary constraints limit the ability to undertake such extensive projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Dominance Reshapes Infrastructure Economics

Cloud deployments held 71.23% of the Unified Communications and Collaboration market share in 2025. The segment’s outperformance reflects consumption-based pricing, rapid feature velocity, and the elimination of capital expenditures for on-premises hardware. Large enterprises see predictable budgeting while small firms avoid the need for specialist IT staff. On-premises and hosted models retained 28.77% share, concentrated in defense and critical-infrastructure users with air-gapped networks. The Unified Communications and Collaboration market size for cloud solutions is projected to expand at a 26.99% CAGR through 2031, reinforcing long-term vendor focus on multitenant security and geo-redundancy.

Hyperscalers accelerate adoption by bundling collaboration with productivity suites. Microsoft converts Microsoft 365 customers into Teams users with minimal friction, pushing the Unified Communications and Collaboration market toward ecosystem lock-in. Google’s similar strategy with Workspace keeps switching costs low for Gmail-centric organizations. Hybrid architectures persist, however, where voice gateways remain on-site to satisfy local recording or survivability mandates, ensuring on-premises revenue does not shrink to zero.

By Component: Video Leads While Asynchronous Collaboration Gains Speed

Video conferencing captured 36.43% revenue share in 2025 as pandemic-era behaviors became structural. Yet asynchronous collaboration and content-sharing applications are the fastest element, forecast to grow at 27.84% CAGR. Businesses are balancing live video with tools that curb meeting fatigue, such as persistent chat, digital whiteboards, and co-authoring canvases. The Unified Communications and Collaboration market size for collaboration platforms is therefore expanding faster than for standalone video services.

Voice and IP telephony represented roughly 28% of revenue as enterprises replaced PBXs with cloud phones. Messaging and presence contributed about 22%. Vendor bundling blurs these boundaries as suites converge features under tiered subscriptions. Consequently, discrete component-level growth rates are harder to track, but demand for analytics and compliance add-ons is rising in regulated industries.

By Organization Size: SME Acceleration Narrows the Gap

Large enterprises still commanded 58.14% of 2025 spending, but many have already migrated core seats, so growth is moderating. The small and medium-sized enterprise segment is advancing at a 27.15% CAGR, closing the revenue gap. Freemium tiers and self-service provisioning encourage bottom-up adoption, often starting with external client calls before expanding internally.

Enterprise deals emphasize service-level agreements, custom compliance terms, and integration with ERP and CRM systems, which lengthens sales cycles. In contrast, SMEs value low entry costs and rapid deployment, making packaged bundles with standard security features attractive. As macro conditions tighten IT budgets, vendors that streamline onboarding and minimize professional-services requirements are poised to win share among resource-constrained firms.

By End-User Industry: Healthcare Outpaces Early Adopters

The IT and telecom segment led 2025 spending at 24.76% because technology-centric firms embraced collaboration early. Healthcare and life sciences, however, will be the fastest-growing vertical at 28.11% CAGR thanks to permanent telehealth reimbursement and demand for HIPAA-compliant video. The Unified Communications and Collaboration market size allocated to healthcare is underpinned by integrations with electronic health record systems and medical-grade peripherals.

Banking, financial services, and insurance contribute roughly 21% of revenue as institutions modernize contact centers under strict supervision rules. Retail and e-commerce drive about 16% through store communications and customer-service hubs. Government, education, manufacturing, and logistics collectively form a diversified tail, each seeking vertical add-ons such as shop-floor headsets or secure classroom portals.

Geography Analysis

North America retained 38.41% of global revenue in 2025, buoyed by mature cloud infrastructure and early hybrid work adoption. United States enterprises account for the bulk of spending, while Canada’s business cloud adoption exceeded 93% among firms with more than 50 employees in 2025. Growth in the region is tempering as penetration nears saturation, but rural broadband investments under the Broadband Equity, Access, and Deployment Program are widening the addressable base.

Asia-Pacific is forecast to expand at a 27.61% CAGR, the fastest regional pace. China surpassed 4.5 million 5G base stations in 2025, underpinning mobile-first adoption. India’s draft quality-of-service rules for cloud communications indicate regulatory support. Japan and South Korea subsidize small-business cloud uptake and have near-universal 5G coverage, fostering edge-enabled collaboration use cases.

Europe contributed roughly 28% of 2025 revenue. Data-sovereignty requirements under GDPR and the 2024 Data Act compel providers to build multicloud portability, adding complexity but also creating niches for regional players. The Middle East benefits from national digital agendas, with Saudi Arabia attracting USD 200 million in Cisco infrastructure investment in 2025. South America and Africa remain smaller but are seeing partnership-led expansions, particularly in Brazil, South Africa, Nigeria, and Egypt, where mobile operators bundle collaboration with connectivity.

Competitive Landscape

The top five vendors account for about 45% of revenue, indicating moderate concentration. Microsoft leverages Microsoft 365 bundling to maintain a 320 million-user installed base. Cisco, Zoom, RingCentral, and Google follow, each differentiating through compliance coverage, workflow integrations, or AI engines. Smaller firms such as 8x8, Avaya, Mitel, and Dialpad compete on vertical niches, voice quality, or developer friendliness.

The innovation race is shifting from basic feature parity to embedded AI, contact center convergence, and vertical workflow automation. Patent filings related to AI-driven meeting intelligence rose 23% year over year in 2025, highlighting sustained R&D momentum. Meanwhile, API commoditization pressures pure-play CPaaS providers; Twilio’s 2024 revenue fell 14% as margins eroded.

Strategic moves include Cisco’s 2026 acquisition of Lightico to integrate secure e-signature into Webex, RingCentral’s embedding of video in Salesforce Service Cloud, and 8x8’s purchase of Fuze to scale its enterprise footprint. Vendors are also racing for certifications such as FedRAMP, ISO/IEC 27001, and HIPAA to unlock regulated verticals.

Unified Communications And Collaboration Industry Leaders

Microsoft

Cisco Systems

Zoom Video Communications

RingCentral, Inc.

8x8, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Microsoft released Teams Premium AI features, bundling intelligent recaps and sentiment analysis at no extra cost for E5 customers.

- January 2026: Cisco closed the Lightico acquisition to add e-signature and document-collection to Webex Contact Center.

- December 2025: RingCentral and Salesforce embedded RingCentral Video inside Service Cloud for seamless video escalation.

- November 2025: Zoom introduced Zoom Workplace, combining video, chat, email, calendar, and AI productivity tools.

Global Unified Communications And Collaboration Market Report Scope

Unified Communications and Collaboration (UC&C) is a group of solutions organizations implement to ensure that nearly all their technology works smoothly and securely for near real-time collaboration. It is beneficial to integrate multiple enterprise communication tools such as voice calling, video conferencing, instant messaging (IM), presence, content sharing, etc.

The Unified Communications And Collaboration Market Report is Segmented by Deployment Model (On-Premises, and Cloud), Component (Voice/IP Telephony, Video Conferencing, and More), Organization Size (SMEs, and Large Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Public Sector and Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| On-Premises / Hosted |

| Cloud |

| Voice / IP Telephony |

| Video Conferencing |

| Messaging and Presence |

| Collaboration / Content Sharing |

| Other Components |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Public Sector and Education |

| IT and Telecom |

| Manufacturing and Logistics |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Deployment Model | On-Premises / Hosted | |

| Cloud | ||

| By Component | Voice / IP Telephony | |

| Video Conferencing | ||

| Messaging and Presence | ||

| Collaboration / Content Sharing | ||

| Other Components | ||

| By Organization Size | Small and Medium-Sized Enterprises | |

| Large Enterprises | ||

| By End-User Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Retail and E-Commerce | ||

| Public Sector and Education | ||

| IT and Telecom | ||

| Manufacturing and Logistics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Unified Communications and Collaboration market in 2031?

It is expected to reach USD 779.47 billion by 2031.

How fast is the cloud deployment segment growing?

Cloud deployments are projected to post a 26.99% CAGR between 2026 and 2031.

Which region will register the quickest growth through 2031?

Asia-Pacific is forecast to expand at a 27.61% CAGR, the fastest among all regions.

Why is healthcare adopting collaboration platforms so rapidly?

Permanent telehealth reimbursement and the need for HIPAA-compliant video are driving a 28.11% CAGR within healthcare.

How are vendors differentiating in an increasingly crowded field?

Leaders focus on embedded AI, contact center convergence, and vertical-specific compliance certifications to create switching costs.

What impact does 5G have on collaboration workloads?

Standalone 5G and edge computing cut latency below 20 ms, enabling immersive AR and 4K mobile video collaboration use cases.

Page last updated on: