Unbleached Kraft Pulp Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

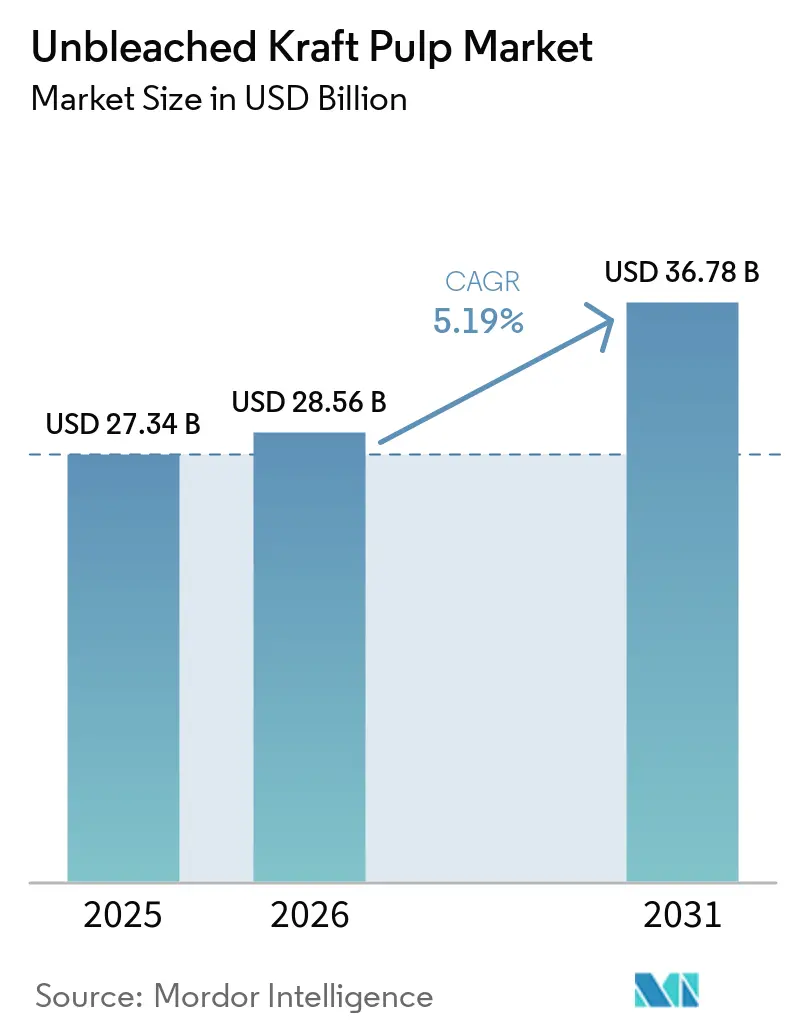

| Market Size (2026) | USD 28.56 Billion |

| Market Size (2031) | USD 36.78 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unbleached Kraft Pulp Market Analysis by Mordor Intelligence

The Unbleached Kraft Pulp Market size is expected to grow from USD 27.34 billion in 2025 to USD 28.56 billion in 2026 and is forecast to reach USD 36.78 billion by 2031 at 5.19% CAGR over 2026-2031.

The unbleached kraft pulp market is being supported by steady demand from containerboard manufacturing, where strength, runnability, and reliability remain central to mill purchasing decisions. The unbleached kraft pulp (UKP) market is also gaining support from the wider move toward fiber-based packaging, especially in applications where bleached and recycled grades do not offer the same structural performance. Regional demand remains strongest in Asia-Pacific, where paperboard production, e-commerce logistics, and FMCG packaging expansion continue to lift procurement needs across the packaging chain. Competitive behavior is increasingly shaped by backward integration, capacity discipline, and portfolio shifts toward higher-performance kraft grades, while the market continues to face pressure from recycled fiber substitution, wood cost volatility, and changing trade flows among major export producers. South American cost advantages and rising integrated pulp capacity in China are also changing the pricing and trade setting for the UKP market over the forecast period.

Key Report Takeaways

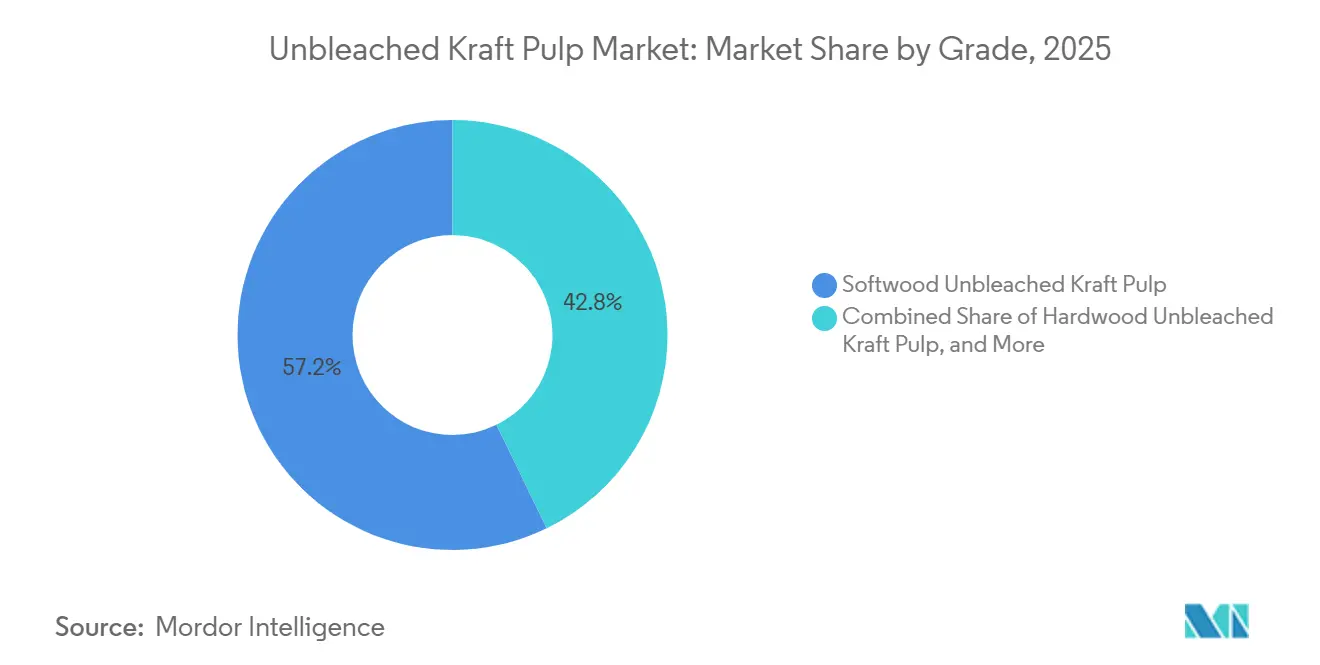

- By grade, softwood held 57.23% of the unbleached kraft pulp market share in 2025, while hardwood is projected to expand at a 5.73% CAGR through 2031.

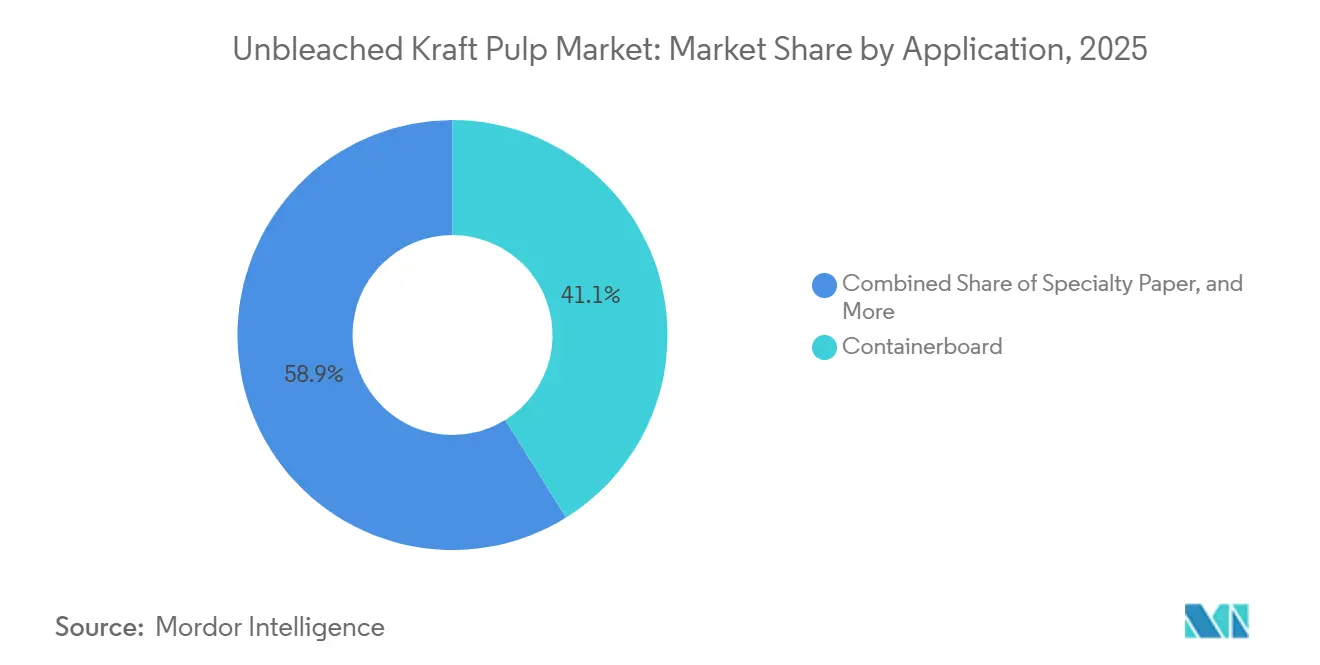

- By application, containerboard accounted for 41.14% share of the unbleached kraft pulp (UKP) market size in 2025, while specialty paper is expected to record the fastest growth at 6.11% CAGR through 2031.

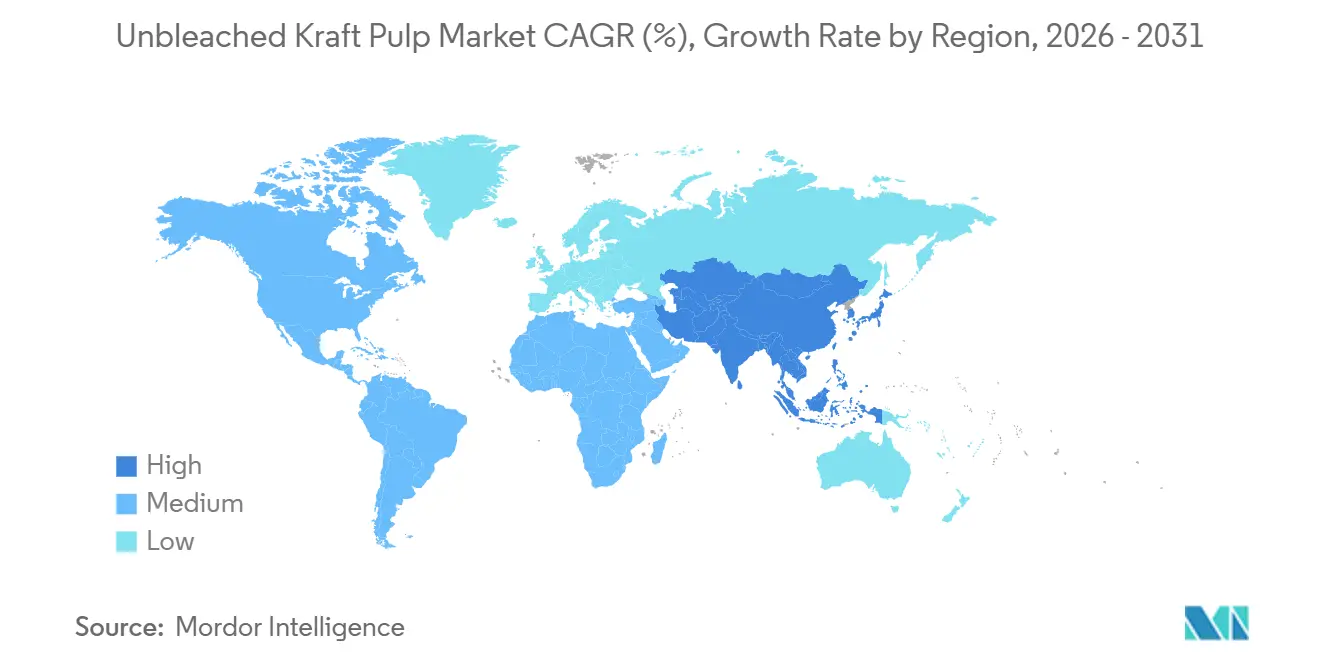

- UKP market with a 39.45% share in 2025 and is also projected to remain the fastest-growing regional segment at a 5.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Unbleached Kraft Pulp Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Corrugated Packaging Demand Driven by E-Commerce | +1.8% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Shift Toward Sustainable, Unbleached Packaging Materials | +1.3% | Global, EU-led with Asia-Pacific follow-through | Medium term (2-4 years) |

| Plastic Substitution in Retail and Transport Packaging | +0.9% | EU, North America, spill-over to Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Growth in Heavy-Duty Packaging | +0.6% | Global, industrial and construction market clusters | Short term (≤ 2 years) |

| Lower Chemical Processing Enhancing Environmental Acceptance | +0.3% | Europe, North America, Asia-Pacific regulatory markets | Long term (≥ 4 years) |

| Integration Strategies by Packaging Companies | +0.2% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth In Corrugated Packaging Demand Driven By E-Commerce

E-commerce logistics remained the clearest near-term demand signal for the unbleached kraft pulp market because each shipped unit typically requires more corrugated protection than store-based replenishment formats. The unbleached kraft pulp (UKP) market continued to benefit from strong operating conditions in U.S. containerboard, where mills kept utilization high even after capacity reductions across the sector.[1]American Forest and Paper Association, “AFandPA Releases 66th Annual Paper Industry Capacity and Fiber Consumption Survey,” AFandPA, afandpa.org AF&PA reported that containerboard operating rates held at 91.9% in 2025, even as installed capacity declined by 5.1%, which showed that end demand absorbed the structural footprint cuts. The same survey showed that containerboard represented more than 50% of total U.S. paper and paperboard capacity in 2025, reinforcing its central role in the packaging system. This supports a stable outlet for virgin strength fiber, especially where mills need dependable furnish for kraft linerboard and corrugating medium. As a result, the UKP market continues to track corrugated packaging demand closely, with e-commerce shipment growth providing a durable floor for consumption.

Shift Toward Sustainable, Unbleached Packaging Materials

The unbleached kraft pulp market is also benefiting from the shift toward packaging formats that are easier to recycle and simpler to specify under tightening sustainability rules. Regulation (EU) 2025/40 entered into force in February 2025 and sets a path under which all packaging placed on the EU market must be recyclable by 2030, with the regulation applying from August 2026.[2]European Union, “Regulation (EU) 2025/40 of the European Parliament and of the Council on Packaging and Packaging Waste,” Official Journal of the European Union, eur-lex.europa.eu This direction favors mono-material and fiber-based packaging structures, which has increased the appeal of uncoated and unbleached paper formats in transport and heavy-duty uses.[3]European Commission, “Packaging and Packaging Waste Regulation,” European Commission, environment.ec.europa.eu Germany provided a clear demand signal in 2025, when packaging paper output reached 12.5 million tonnes and represented 67% of total paper production, up 1.8% from 2024.[4]Verband Deutscher Papierfabriken, “Paper Facts and Figures 2025,” Verband Deutscher Papierfabriken, papierindustrie.de The unbleached kraft pulp (UKP) market also benefits from procurement teams placing more weight on process chemistry and discharge profiles when evaluating fiber options for packaging specifications. That gives unbleached grades an advantage in programs that seek stronger environmental positioning without giving up mechanical performance in demanding applications.

Plastic Substitution In Retail And Transport Packaging

The unbleached kraft pulp market is gaining from the gradual replacement of plastic in retail and transport packaging, especially where paper-based formats can now meet performance needs that once favored polymer films. The EU packaging regulation and the ongoing effect of the Single-Use Plastics Directive are pushing brand owners and retailers to redesign packaging formats around recyclable material choices. Mondi opened a new paper bags plant in Pittsburgh in April 2026 with annual capacity of 300 million bags, aimed at e-commerce and industrial customers, which showed that large-scale plastic-to-paper conversion is already being built into production networks. UPM, Michelman, and BOBST also introduced a bio-based paper packaging concept in May 2026 that was aligned with EU packaging rules and designed to improve barrier functionality in recyclable paper structures. These moves matter for the unbleached kraft pulp (UKP) market because parcel mailers, industrial bags, and paper-based transport formats consume strength fiber where packaging failure costs are high. The UKP market therefore stands to benefit as paper solutions become more capable in moisture resistance, sealing, and transport durability.

Growth In Heavy-Duty Packaging

Heavy-duty packaging remains an important outlet for the unbleached kraft pulp market because industrial sacks and transport packaging still depend on long-fiber strength that recycled furnish cannot fully match. Construction materials, fertilizers, chemicals, and agricultural products continue to require sacks and papers with strong tensile and burst performance under handling stress. Georgia-Pacific began its USD 800 million capital investment program at the Alabama River Cellulose mill in Q4 2025, and the project is expected to lift capacity by around 300 tonnes per day by 2027. The company said the site is expected to become the largest and one of the most technologically advanced softwood pulp mills in the United States, which signals confidence in long-term demand for strength-grade virgin fiber. This is relevant to the unbleached kraft pulp (UKP) market because heavy-duty packaging is less exposed to substitution than standard brown packaging applications. It also supports premium positioning for softwood-based grades where end users value load-bearing reliability more than lowest-cost furnish.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Competition From Recycled Fiber (OCC-Based Production) | -1.0% | North America, Europe | Short term (≤ 2 years) |

| Limited Use In High-Quality Applications | -0.7% | Global | Long term (≥ 4 years) |

| Raw Material Cost Volatility (Wood Supply Impact) | -0.5% | North America, Europe, Nordics | Short term (≤ 2 years) |

| Environmental Pressure On Forestry And Land Use | -0.3% | Europe, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Competition From Recycled Fiber (OCC-Based Production)

The unbleached kraft pulp market faces its most direct competitive pressure from recycled fiber in containerboard applications where cost discipline matters more than peak strength. Large packaging groups continue to build systems that combine virgin and recycled furnish, which reduces the addressable share available to independent market pulp sellers. Smurfit Westrock reported annual recycled fiber consumption of 13 million tonnes across its operating footprint, showing the scale at which major producers are managing mixed fiber strategies. International Paper also agreed in April 2026 to acquire NORPAC, adding containerboard and recycled lightweight containerboard capability that improves system flexibility. This matters for the UKP market because each increase in integrated recycled capacity can reduce merchant demand for virgin brown fiber in cost-sensitive grades. The restraint is strongest in North America and Europe, where mature collection systems and integrated packaging groups have greater ability to shift furnish according to economics.

Limited Use In High-Quality Applications

The unbleached kraft pulp market also remains limited by the natural performance boundaries of the fiber itself in applications that require high brightness, whiteness, or specific visual standards. Unbleached grades deliver strong mechanical properties, but their brown color and residual lignin content restrict direct use in printing, writing, tissue, and premium white packaging categories. This means the unbleached kraft pulp (UKP) market remains concentrated in brown packaging, industrial paper, sacks, and a defined set of specialty uses rather than the full paper and board universe. Billerud’s 2025 and 2026 product positioning showed that specialty paper opportunities exist where medical, barrier, and packaging functions matter more than visual brightness, but these remain narrower than the addressable base for bleached fiber products. The practical result is that producers cannot enter premium white packaging or high-brightness paper markets without additional conversion, coating, or blending steps that raise complexity. That structural limit caps how far the UKP market can expand into higher-value adjacent grades even when sustainability preferences are favorable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Softwood Dominance Anchors Fiber Strength Standards

Softwood held 57.23% of global demand by grade in 2025, which kept it at the center of the unbleached kraft pulp market across linerboard and heavy-duty paper uses. The segment’s lead reflects the long-fiber advantage of spruce, pine, and fir furnish, which remains essential for tensile and burst strength in demanding packaging applications. Buyers in Europe and North America also continue to place weight on certified sourcing, with FSC and PEFC frameworks shaping procurement eligibility for softwood supply. This supports grade stability in the unbleached kraft pulp (UKP) market because certification and strength performance work together in customer specifications. Chile’s production of unbleached radiata pine pulp reached 326,200 tonnes in 2024, down from 503,000 tonnes in 2022, which showed that portfolio discipline among suppliers can also tighten softwood availability in export channels. That supply adjustment reinforced the premium role of softwood furnish in applications where mills cannot compromise on strength benchmarks.

Hardwood is projected to expand at a 5.73% CAGR, which makes it the fastest-growing grade in the unbleached kraft pulp (UKP) market size by segment through 2031. Growth is being supported by wider use of eucalyptus-based furnish in Asian mills, where cost-performance balance often matters more than peak fiber strength. Brazil remained the key structural enabler because national pulp production reached 29.4 million tonnes in 2025 and exports climbed to 20.7 million tonnes, up 11.6% from 2024. Mixed fiber grades are also gaining commercial value in the unbleached kraft pulp industry because mills in Southeast Asia and India are blending hardwood and softwood to optimize input cost and board performance. This keeps grade competition active, but it does not change the fact that softwood remains the reference point for strength-critical specifications in the unbleached kraft pulp market.

By Application: E-Commerce Lifts Containerboard Demand

Containerboard held 41.14% of demand in 2025, which made it the largest application in the unbleached kraft pulp market size by end use. Its lead position comes from the central role of linerboard and corrugating medium in shipping, industrial distribution, and fast-moving consumer goods packaging. U.S. containerboard mills operated at 91.9% in 2025 even after capacity cuts, which showed that demand stayed firm across the packaging base. Smurfit Westrock also reported stronger industry operating conditions in 2026, which supported the outlook for packaging system demand tied to kraft fiber consumption. This keeps containerboard as the main volume anchor for the unbleached kraft pulp market, particularly where performance needs limit the share of recycled substitution. It also means the unbleached kraft pulp industry remains closely tied to shipment intensity, logistics activity, and mill operating discipline in corrugated packaging.

Specialty paper is projected to grow at a 6.11% CAGR, which makes it the fastest-rising application in the unbleached kraft pulp market size through 2031. Demand is being lifted by medical packaging, industrial barrier paper, and natural-look food service formats where recyclability and fiber purity have commercial value. Billerud introduced MediKraft SealBase to address medical and pharmaceutical packaging needs, which showed that targeted unbleached paper solutions are moving into higher-specification packaging niches. Kraft paper also retained an important role in the unbleached kraft pulp market, especially in flexible packaging, e-commerce bags, and industrial uses where converting lines favor strong brown fiber formats. Other applications, including tissue and molded fiber products, remain smaller because many of those categories continue to prefer bleached furnish for appearance and softness requirements.

Geography Analysis

Asia-Pacific held 39.45% of the unbleached kraft pulp market share in 2025 and is projected to expand at a 5.92% CAGR through 2031, which keeps it as both the largest and fastest-growing regional segment. China remains the main regional demand center because it is the world’s largest paperboard producer and continues to require virgin fiber grades for quality-sensitive corrugated packaging output. India is the strongest demand-growth vector within the region, supported by organized retail expansion, pharmaceutical packaging exports, and rising e-commerce fulfillment activity. Japan and South Korea continue to support the unbleached kraft pulp market through technically demanding specialty paper uses, especially in industrial and electronics-linked packaging chains. UPM stated in its Q1 2026 CEO presentation that specialty paper markets in Asia remained stable, even as conditions were softer in Europe and North America.

Europe showed a more regulation-led demand profile in the unbleached kraft pulp market during 2025 and 2026. Regulation (EU) 2025/40 and its August 2026 application timeline pushed packaging buyers to move earlier on recyclable fiber-based formats. Germany’s packaging paper production reached 12.5 million tonnes in 2025 and accounted for 67% of national paper output, which showed how deeply packaging has come to dominate paper demand in the country. Billerud continued to upgrade capabilities across its system, including work at Skärblacka in Q1 2026, as part of its focus on premium packaging materials. Mondi also advanced long-term infrastructure through its biomass power project in Ružomberok, which is expected to raise energy self-sufficiency at the integrated mill from 75% to 90%.

North America remained a major consumption and production hub for the unbleached kraft pulp market, supported by its large integrated containerboard base and continued investment in packaging assets. Packaging paper production in the United States grew 1.7% in 2025, while containerboard operating rates remained at 91.9%, which showed that demand adjusted well to lower capacity. South America continued to function mainly as a supply region for the unbleached kraft pulp market, with Arauco’s Sucuriú project reaching 42.6% physical progress by Q4 2025 and remaining on schedule for start-up in the second half of 2027. CMPC’s Natureza project also remained a major future capacity addition, with planned output of up to 2.5 million tonnes per year and a dedicated export terminal strategy that will influence global trade flows through 2030.

Competitive Landscape

The unbleached kraft pulp market operates within a moderately concentrated structure that is shaped less by pure merchant pulp scale and more by integration across pulp, paper, and packaging systems. Large producers manage fiber strategy through captive supply, which limits open-market demand and raises the importance of regional positions. Smurfit Westrock illustrates this scale well, with more than 500 facilities in over 40 countries, 23 million tonnes of paper capacity, and 13 million tonnes of annual recycled fiber consumption. That footprint gives the company broad flexibility to balance virgin and recycled fiber across end markets in the unbleached kraft pulp market. International Paper added to the consolidation pattern in April 2026 when it agreed to acquire NORPAC for USD 360 million, adding around 1 million tonnes of annual containerboard capacity in Longview, Washington.

South American producers continue to shape the cost curve of the unbleached kraft pulp market through plantation productivity, export scale, and new project pipelines. Arauco’s corporate presentation showed continued progress on the Sucuriú mill, which will add 3.5 million tonnes of annual capacity when it starts up in 2027. CMPC’s 2024 Integrated Report also confirmed progress on the Natureza project and on supporting export infrastructure in Brazil. These moves matter because they will expand South America’s role as a global supply base and increase competitive pressure on higher-cost producers. In parallel, the unbleached kraft pulp market continues to see strategic differentiation from Nordic players that compete more on traceability, grade quality, and customer proximity than on lowest delivered fiber cost.

Billerud is a good example of this premium strategy within the unbleached kraft pulp market. The company reported equipment upgrades and portfolio actions in 2026 that were designed to improve capability in premium packaging materials across its mill network. Smurfit Westrock also outlined a five-year growth framework in February 2026 that covered North America, EMEA and Asia-Pacific, and South America, while confirming ongoing capacity rationalization and geographic expansion. The competitive pattern in the unbleached kraft pulp market therefore combines integration, selective expansion, and product upgrading rather than simple volume growth alone. This keeps competition active across regions, but it also preserves room for differentiated suppliers that can meet performance, certification, and service requirements consistently.

Unbleached Kraft Pulp Industry Leaders

Stora Enso Oyj

International Paper Company

Mondi plc

CMPC Celulosa S.A.

Canfor Pulp Products Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: UPM, Michelman and BOBST introduced a bio-based paper packaging concept aligned with EU packaging rules, expanding the commercial case for recyclable high-performance paper structures.

- May 2026: International Paper broke ground on a USD 225 million greenfield sustainable packaging facility in Rankin County, Mississippi. The facility was designed to enhance manufacturing capabilities and serve growing demand in key packaging segments. Operations are anticipated to begin in Q4 2027.

- April 2026: International Paper entered into an agreement to acquire North Pacific Paper Company, a Longview, Washington containerboard and paper mill producing approximately 1 million tonnes annually, for USD 360 million. The acquisition added system flexibility and recycled lightweight containerboard capability, subject to regulatory approval.

Global Unbleached Kraft Pulp Market Report Scope

Unbleached Kraft Pulp (UKP) is a high-strength chemical pulp produced from softwood and hardwood species through the kraft (sulfate) process, retaining its natural brown color as the lignin-removing bleaching stage is omitted. This preserves fiber integrity, delivering exceptional tensile and tear strength at lower production cost and environmental impact. Valued for these properties, UKP is a primary source for containerboard, kraft paper, and specialty grades. The market spans softwood, hardwood, and mixed-fiber grades across both integrated production and merchant trade, serving packaging and industrial applications worldwide.

The unbleached kraft pulp market report is segmented by grade (softwood, hardwood, and mixed fiber), application (containerboard, kraft paper, specialty paper, and other applications), and geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Softwood Unbleached Kraft Pulp |

| Hardwood Unbleached Kraft Pulp |

| Mixed Fiber Unbleached Kraft Pulp |

| Containerboard |

| Kraft Paper |

| Specialty Paper |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Nordics | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Middle East |

| Africa |

| By Grade | Softwood Unbleached Kraft Pulp | |

| Hardwood Unbleached Kraft Pulp | ||

| Mixed Fiber Unbleached Kraft Pulp | ||

| By Application | Containerboard | |

| Kraft Paper | ||

| Specialty Paper | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | |

| Africa | ||

Key Questions Answered in the Report

What is the current size and future outlook for unbleached kraft pulp?

The sector was valued at USD 27.34 billion in 2025, was estimated at USD 28.56 billion in 2026, and is forecast to reach USD 36.78 billion by 2031 at a 5.19% CAGR.

Which grade leads demand for unbleached kraft pulp?

Softwood led demand in 2025 with 57.23% share because long-fiber furnish remains critical for tensile and burst strength in linerboard and heavy-duty packaging.

Which application is growing the fastest for unbleached kraft pulp?

Specialty paper is projected to grow the fastest, with a 6.11% CAGR through 2031, supported by medical packaging, barrier papers, and natural-look food service formats.

Why is Asia-Pacific the leading regional hub for this business?

Asia-Pacific held 39.45% share in 2025 and is projected to grow at 5.92% CAGR, driven by China’s paperboard scale and India’s expanding e-commerce, retail, and packaging demand.

What is the biggest near-term growth driver for producers and suppliers?

Corrugated packaging demand linked to e-commerce remains the strongest near-term growth driver because it supports steady containerboard output and sustained need for strength-grade virgin fiber.

What is the main threat to future growth in this space?

Recycled fiber is the main competitive restraint, especially in North America and Europe, where integrated packaging groups can shift furnish mix in cost-sensitive containerboard grades.

Page last updated on: