Bleached Eucalyptus Kraft Pulp Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

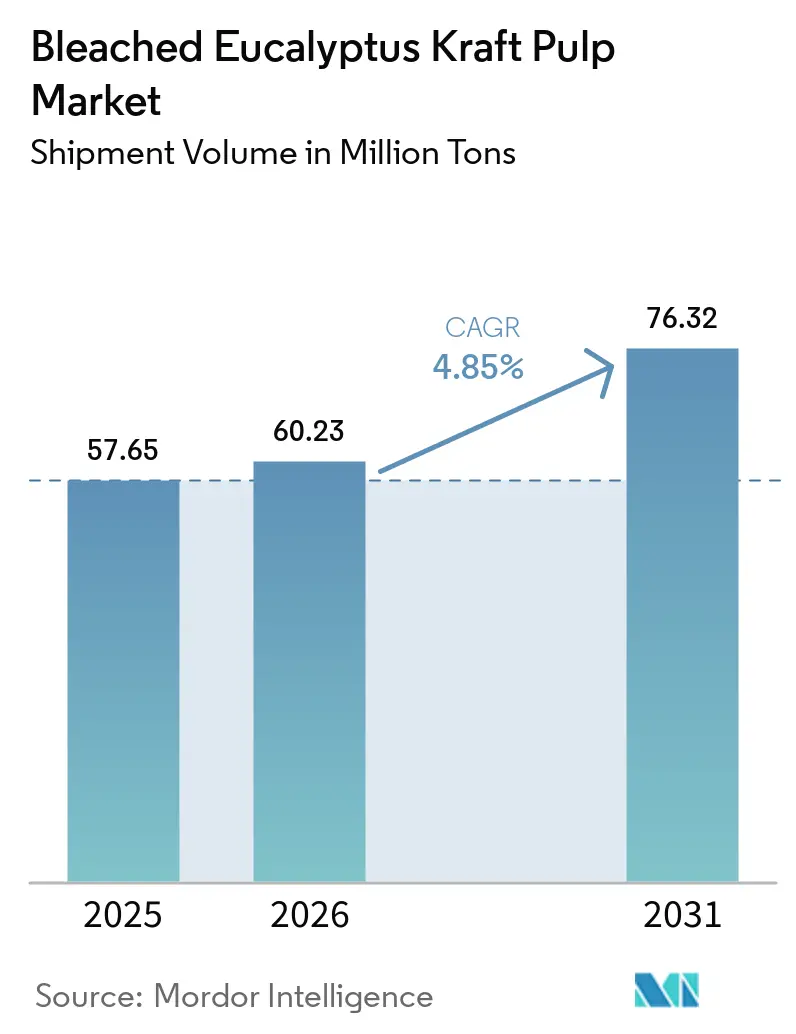

| Market Volume (2026) | 60.23 Million tons |

| Market Volume (2031) | 76.32 Million tons |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

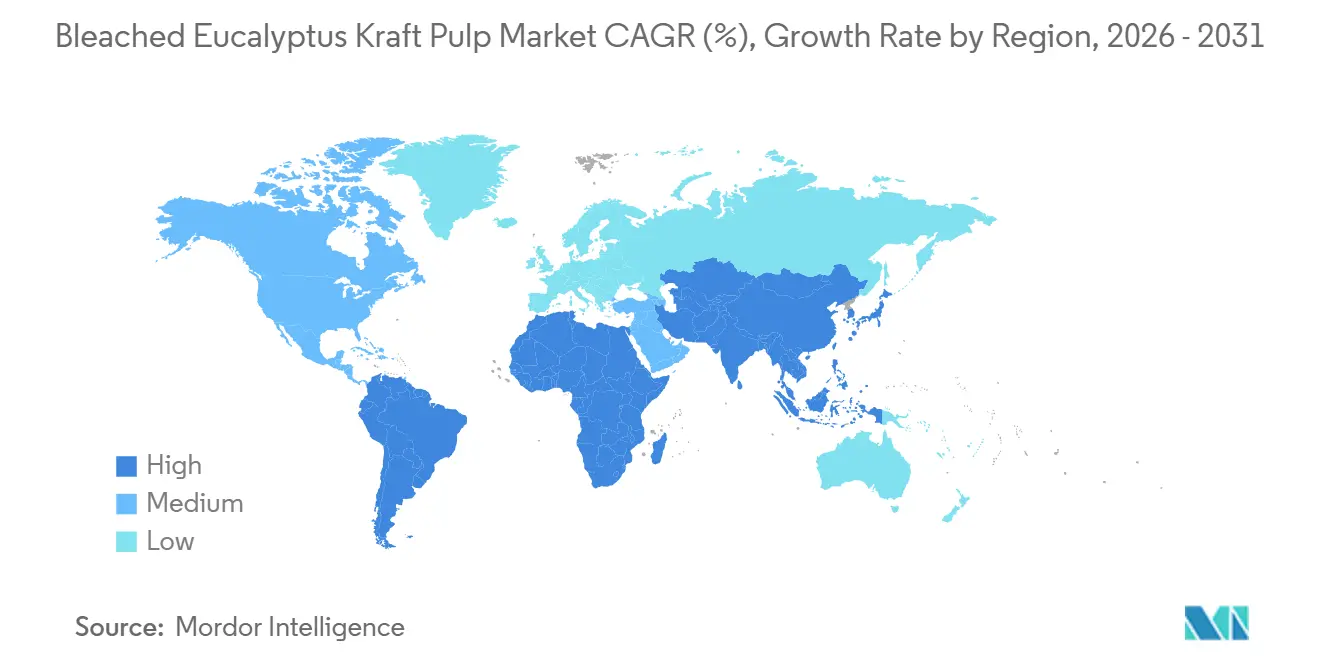

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bleached Eucalyptus Kraft Pulp Market Analysis by Mordor Intelligence

The Bleached Eucalyptus Kraft Pulp Market size in terms of shipment volume was valued at 57.65 Million tons in 2025 and is estimated to grow from 60.23 Million tons in 2026 to reach 76.32 Million tons by 2031, at a CAGR of 4.85% during the forecast period (2026-2031).

Structural demand from tissue and hygiene products, combined with rising e-commerce packaging needs, underpins medium-term growth even as 10 million tons of South American capacity prepare to enter the system. Inventories in China, the dominant import market, now dictate short-term price swings, while a widening price gap between Asian spot and European contract benchmarks preserves arbitrage opportunities for agile traders. Environmental scrutiny is accelerating upgrades to elemental chlorine free (ECF) sequences, yet totally chlorine free (TCF) adoption remains niche because of its higher operating cost. Supply-side risk centers on mega-mills in Brazil, Uruguay, and Chile ramping faster than demand, which would compress margins for higher-cost Nordic and Indonesian producers.

Key Report Takeaways

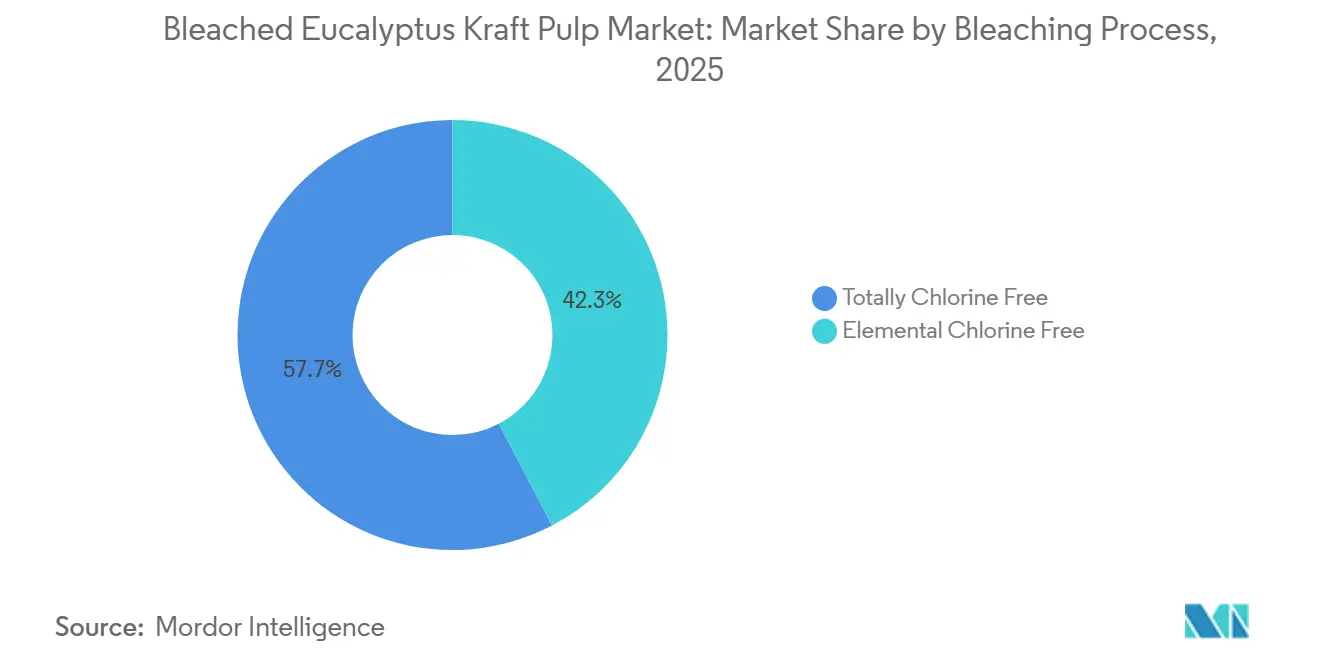

- By bleaching process, elemental chlorine free retained 42.34% of bleached eucalyptus kraft pulp market share in 2025, while totally chlorine free grades are projected to expand at a 4.97% CAGR through 2031.

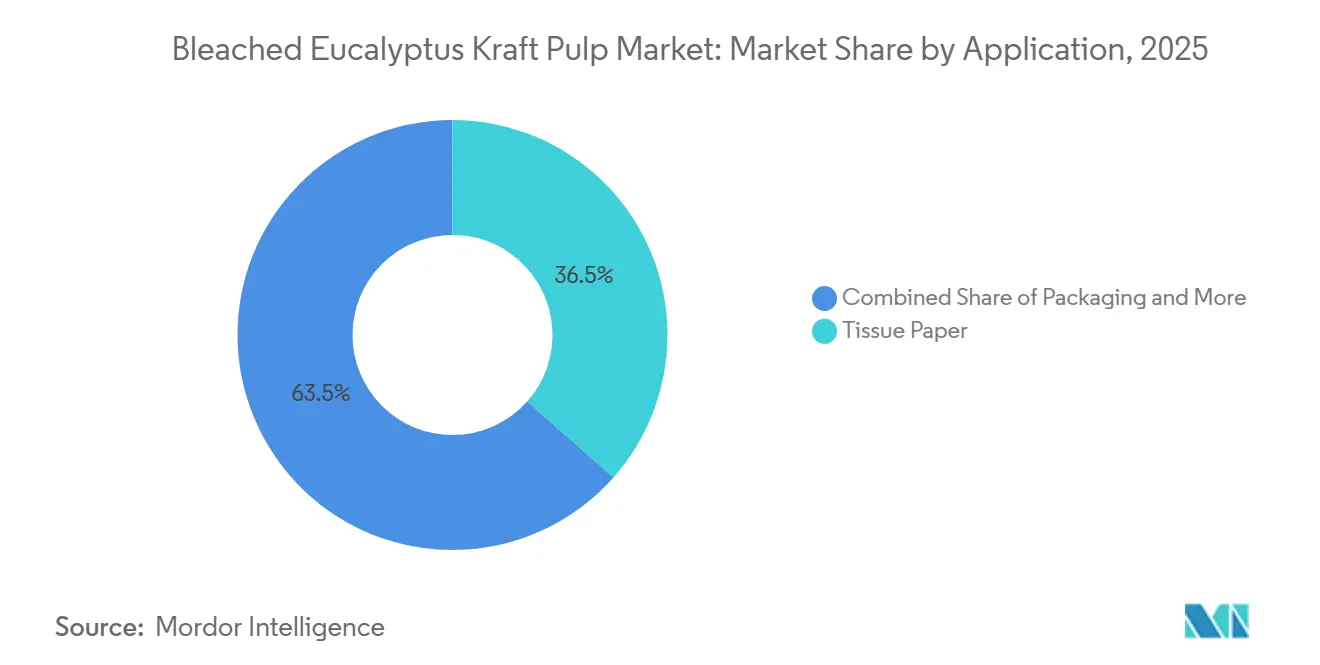

- By application, tissue paper led with 36.54% revenue share in 2025, whereas packaging is advancing at a 5.67% CAGR between 2026-2031.

- By geography, Asia-Pacific commanded 38.21% of volume in 2025 and is set to grow at a 4.67% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bleached Eucalyptus Kraft Pulp Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural Growth in Tissue and Hygiene Consumption | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Increasing Preference for Virgin Fiber in Premium Applications | +0.8% | Global, focus in North America and Europe | Medium term (2-4 years) |

| E-commerce Driving Packaging Demand | +1.1% | Global, led by North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Shift from Plastic to Fiber-Based Materials | +0.9% | Europe and North America regulatory push, Asia-Pacific following | Long term (≥ 4 years) |

| Rapid Growth in Emerging Markets | +0.7% | Asia-Pacific (India, Southeast Asia), Middle East and Africa | Long term (≥ 4 years) |

| Expansion of High-Yield Eucalyptus Plantations | +0.5% | South America (Brazil, Uruguay, Chile), Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Structural Growth In Tissue And Hygiene Consumption

Per-capita tissue use in emerging economies remains far below developed-market norms, giving the bleached eucalyptus kraft pulp market a long runway for conversion growth. India’s tissue demand is projected to reach 357,000 tons in 2026, up from 280,000 tons in 2024, yet domestic mills still import premium hardwood pulp because recycled fiber cannot meet brightness and softness thresholds.[1]Tissue World Magazine, “India Tissue Capacity Expansion,” tissueworldmagazine.com Regional quick-service restaurants and retail chains in Indonesia, Vietnam, and the Philippines are also standardizing away-from-home tissue grades that require virgin fiber. Global tissue sales climbed to USD 45.2 billion in 2025 and are forecast to hit USD 78.5 billion by 2034, reinforcing the underlying demand pull for virgin eucalyptus pulp. This secular trend cushions the market from substitution pressure in higher-margin formats even as recycled content rises in lower-grade towel and napkin products.

Increasing Preference For Virgin Fiber In Premium Applications

Converters producing facial tissue, diapers, and feminine hygiene products specify virgin eucalyptus pulp for softness, brightness, and wet strength that recycled alternatives cannot consistently deliver. Ence started Europe’s first eucalyptus-based fluff pulp line in Q4 2025 with 125,000 tons annual capacity aimed at hygiene applications, targeting premiums of 15-20% over commodity grades.[2]Ence Energía y Celulosa, “Investor Presentation Q4 2025,” ence.es Brand owners also leverage faster carbon sequestration rates of eucalyptus plantations to support sustainability messaging. Suzano’s Eucanatural unbleached pulp illustrates how suppliers are segmenting their portfolios to defend margins by meeting specialized functional demands rather than competing solely on price.

E-commerce Driving Packaging Demand

Surging parcel volumes require corrugated boxes, molded inserts, and wraps that combine printability and cushioning features that bleached eucalyptus kraft pulp delivers through uniform fiber formation. Global retailers have committed to eliminate single-use plastics by 2030, funneling fresh demand into virgin and recycled fiber. Suzano positions Eucanatural for this segment, offering a branded, lower-chemicals solution that maintains structural integrity during last-mile delivery. The packaging application is therefore the fastest rising slice of the bleached eucalyptus kraft pulp market, creating a buffer against secular decline in printing and writing grades.

Shift From Plastic To Fiber-Based Materials

Regulatory bans on plastic straws, cutlery, and polystyrene containers across the European Union have accelerated substitution toward molded pulp and coated board incorporating bleached eucalyptus kraft pulp. China’s tightened waste-import rules compound virgin pulp demand by curbing recycled feedstock supply. Short eucalyptus fibers provide excellent surface smoothness for high-resolution graphics, helping converters match the shelf appeal previously achieved with plastic laminates. These attributes, coupled with lower greenhouse-gas footprints when plantations are certified sustainable, sustain the positive demand trajectory even as alternative barriers, such as cost and recycling infrastructure, vary by region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Volatility (Cyclical Commodity Behavior) | -0.9% | Global, acute for spot-indexed buyers in Asia-Pacific | Short term (≤ 2 years) |

| Competition From Recycled Fiber | -0.7% | Europe and North America mature markets, emerging in Asia-Pacific | Medium term (2-4 years) |

| Environmental Scrutiny On Forestry Practices | -0.4% | Europe regulatory pressure, reputational risk in North America | Long term (≥ 4 years) |

| Dependence On China Demand | -0.5% | Global supply base, concentrated risk in South American exporters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price Volatility

Chinese spot prices rebounded from USD 495 per ton in July 2025 to USD 540 per ton by December 2025, a 9% swing that strained converters on quarterly contracts. Roughly one-quarter of the merchant pulp market operated cash-negative during the trough, pushing Bracell to reconfigure 600,000 tons of capacity into dissolving pulp, which trades USD 200-300 per ton higher. Such volatility complicates capital planning and encourages producers either to curtail output or accelerate capacity ramps, each option reinforcing price cycles.

Competition From Recycled Fiber

Recycled pulp totaled USD 4.96 billion in 2025 and is growing at 6.38% through 2032, aided by advanced de-inking technologies that narrow the quality gap for mid-grade tissue and packaging. The EU Circular Economy Action Plan targets 30-40% recycled content in institutional tissue by 2028, pressuring virgin pulp demand. Yet feedstock contamination and supply volatility keep premium tissue, fluff, and specialty papers squarely in the virgin-fiber domain, leaving bleached eucalyptus kraft pulp room to defend high-margin niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bleaching Process: Pragmatic Dominance Of Elemental Chlorine Free

Elemental chlorine free processes accounted for 42.34% of bleached eucalyptus kraft pulp market share in 2025, reflecting widespread acceptance of its cost-effective compliance profile. ECF sequences use 20-40 kg of chlorine dioxide per oven-dry ton, achieving 88-92% ISO brightness while meeting tight adsorbable organic halogen rules. The bleached eucalyptus kraft pulp market size for ECF grades will continue to rise as new South American lines default to this technology, particularly where power self-sufficiency from recovery boilers offsets chemical cost.

Totally chlorine free sequences are forecast to expand at a 4.97% CAGR, fueled by European brand mandates, yet they still make up a small slice because peroxide, oxygen, and ozone raise chemical spend 20-30% and often cap brightness near 90% ISO. Certification frameworks such as FSC Aligned and PEFC’s updated 2024 standard lower audit friction but stop short of favoring TCF, so adoption concentrates in niche hygiene and décor paper grades willing to pay a green premium.

By Application: Packaging Surges Past Tissue Growth

Tissue retained the largest absolute volume at 36.54% in 2025 thanks to expanding middle-class consumption across Asia-Pacific. However, packaging posted the strongest forward trajectory with a 5.67% CAGR, reflecting e-commerce proliferation and policy moves to phase out plastics. The bleached eucalyptus kraft pulp market size tied to packaging is projected to swell steadily as Amazon, Alibaba, and other platforms commit to fully recyclable solutions.

Converters value eucalyptus pulp’s fine fiber for coated board surfaces that support vivid graphics. Meanwhile, unbleached concepts such as Eucanatural cater to brand aesthetics that favor natural tones, illustrating how suppliers differentiate to capture additional margin. Legacy printing and writing demand continues to erode, yet specialty niches like filter media and label stock remain stable because of strict performance specifications.

Geography Analysis

Asia-Pacific represented 38.21% of global volume in 2025 and is on track for a 4.67% CAGR through 2031, underpinned by rising tissue penetration in India and Southeast Asia plus enduring Chinese import demand even as domestic integrated mills expand. India’s consumption upgrades as urban middle-class households trade up to softer facial tissue formats, while Indonesia, Vietnam, and the Philippines accelerate away-from-home towel rollouts in foodservice chains. Japan and Australia sustain niche requirements for specialty and fluff grades but show muted overall growth.

South America supplied 47% of global hardwood pulp in 2025, leveraging eucalyptus plantation yields averaging 27 Mg ha⁻¹ yr⁻¹ under optimal weather, an edge that producers elsewhere cannot match. Arauco’s 3.5 million-ton Sucuriú mill, slated for H2 2027, and CMPC’s 2.5 million-ton Natureza project in H2 2029 will reinforce the region’s export heft. Integrated rail-and-port investments slash delivered costs to China, where transit can now reach 30-35 days, tightening the freight differential with Indonesian suppliers.

North America and Europe show mature demand profiles focused on premium tissue, specialty, and regulatory-driven packaging shifts. European directives banning single-use plastics channel incremental tonnage into molded pulp and coated board, while Ence’s new fluff line in Spain captures hygiene-grade demand at a price premium.

Competitive Landscape

Suzano anchors the supply base with roughly 13.4 million tons of capacity and is vertically integrating downstream through a USD 3.4 billion tissue joint venture with Kimberly-Clark expected to close mid-2026, pending U.K. Competition and Markets Authority approval.[3]Suzano, “Joint Venture with Kimberly-Clark,” ri.suzano.com.br The deal folds 1 million tons of tissue output into Suzano’s orbit, ensuring baseload offtake for its bleached eucalyptus kraft pulp while giving Kimberly-Clark fiber security in premium categories.[4]Kimberly-Clark, “Strategic Partnership Announcement,” investor.kimberly-clark.com

Capacity expansion remains the core strategic lever. CMPC, Arauco, Bracell, and Klabin collectively plan to add more than 10 million tons by 2029, which could push the market into surplus if Chinese consumption slows. Bracell’s pivot of 600,000 tons toward higher-margin dissolving pulp underscores the optionality producers exercise when commodity pricing erodes. Technology deployments now prioritize digital process controls, closed-loop water circuits, and chemical-recovery optimizations that shave variable cost and meet tightening emission rules.

White-space openings are emerging in specialty niches. Ence’s 125,000-ton eucalyptus fluff launch demonstrates the advantage of adapting short-fiber characteristics to absorbent hygiene media. Suzano’s unbleached Eucanatural line courts eco-oriented packaging converters, while Nordic rivals target high-brightness digital printing substrates. Over the medium term, competitive intensity will sharpen as South American mega-mills come online, nudging smaller Asian and European players without plantation integration toward consolidation or shutdown.

Bleached Eucalyptus Kraft Pulp Industry Leaders

Suzano S.A.

Empresas CMPC

Klabin S.A.

Celulosa Arauco y Constitución S.A. (Arauco)

UPM-Kymmene Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Arauco advanced construction of the 3.5 million-ton Sucuriú mill in Brazil with USD 4.6 billion invested and BRL 2.4 billion allocated to rail plus BRL 2 billion to port facilities at Santos, targeting H2 2027 start-up.

- December 2025: Chinese bleached hardwood pulp spot rebounded to USD 540 per ton after mid-year lows of USD 495 per ton.

- November 2025: PEFC approved standard PEFC aligning with the EU Deforestation Regulation.

- October 2025: Ence launched a 125,000-ton eucalyptus fluff pulp line aimed at hygiene applications.

Global Bleached Eucalyptus Kraft Pulp Market Report Scope

The bleached eucalyptus kraft pulp market report is segmented by bleaching process (elemental chlorine free, totally chlorine free), application (tissue paper, printing and writing paper, specialty paper, packaging), and geography (North america, South america, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in terms of volume (tons).

| Elemental Chlorine Free |

| Totally Chlorine Free |

| Tissue Paper |

| Printing and Writing Paper |

| Specialty Paper |

| Packaging |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| Sweden | |

| Russia | |

| Finland | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Indonesia | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Middle East |

| Africa |

| By Bleaching Process | Elemental Chlorine Free | |

| Totally Chlorine Free | ||

| By Application | Tissue Paper | |

| Printing and Writing Paper | ||

| Specialty Paper | ||

| Packaging | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| Sweden | ||

| Russia | ||

| Finland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Indonesia | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | |

| Africa | ||

Key Questions Answered in the Report

What is the current bleached eucalyptus kraft pulp market size and how fast is it growing?

The bleached eucalyptus kraft pulp market size stands at 60.23 million tons in 2026 and is projected to reach 76.32 million tons by 2031, advancing at a 4.85% CAGR

Which region will drive the largest incremental demand through 2031?

Asia-Pacific will add the most volume, supported by rising per-capita tissue usage in India and Southeast Asia as well as sustained Chinese imports, delivering a 4.67% CAGR

Which application is expanding the fastest?

Packaging is the fastest-growing application segment, forecast to post a 5.67% CAGR through 2031 as e-commerce and plastic-replacement regulations boost fiber-based solutions.

What major capacity projects could pressure prices after 2027?

Arauco’s 3.5 million-ton Sucuriú mill (H2 2027) and CMPC’s 2.5 million-ton Natureza mill (H2 2029) together add 6 million tons, potentially driving prices toward USD 450-480 per ton if demand underperforms.

How are leading producers mitigating price volatility?

Suppliers such as Suzano pursue vertical integration into tissue, while others like Bracell convert commodity lines into higher-margin dissolving pulp, balancing exposure to cyclical swings.

Page last updated on: