Bleached Softwood Kraft Pulp Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.23 Billion |

| Market Size (2031) | USD 31.34 Billion |

| Growth Rate (2026 - 2031) | 4.43% CAGR |

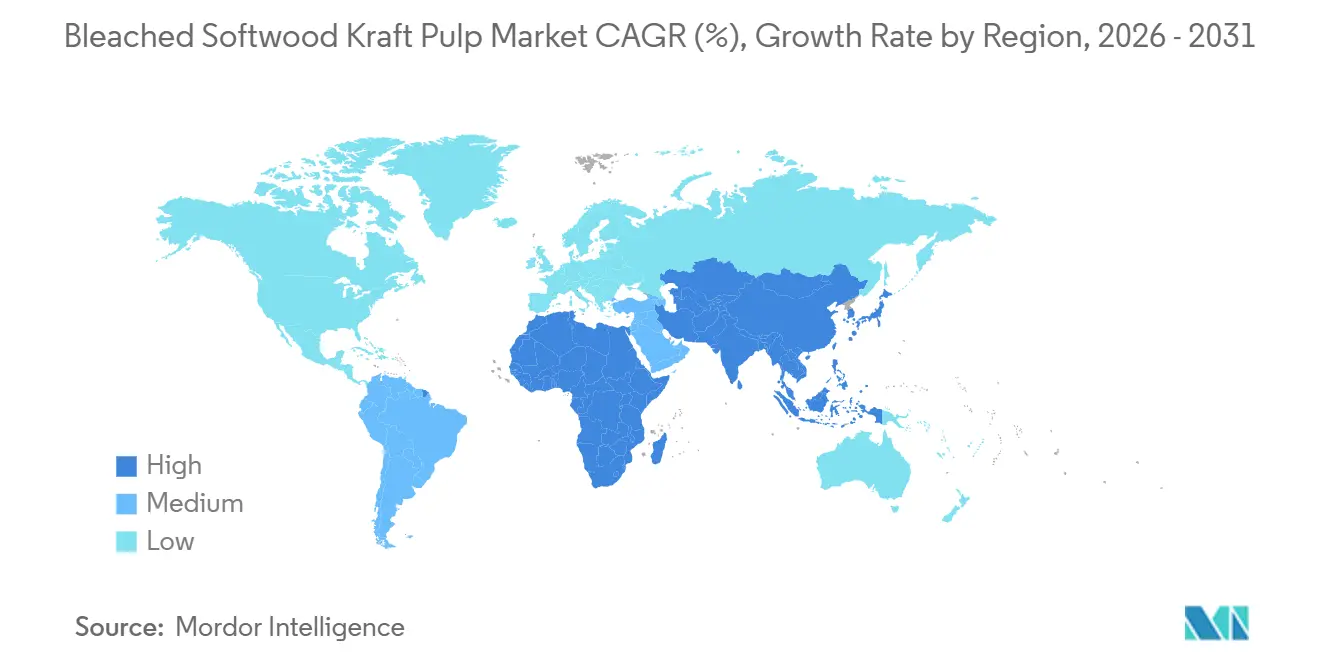

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

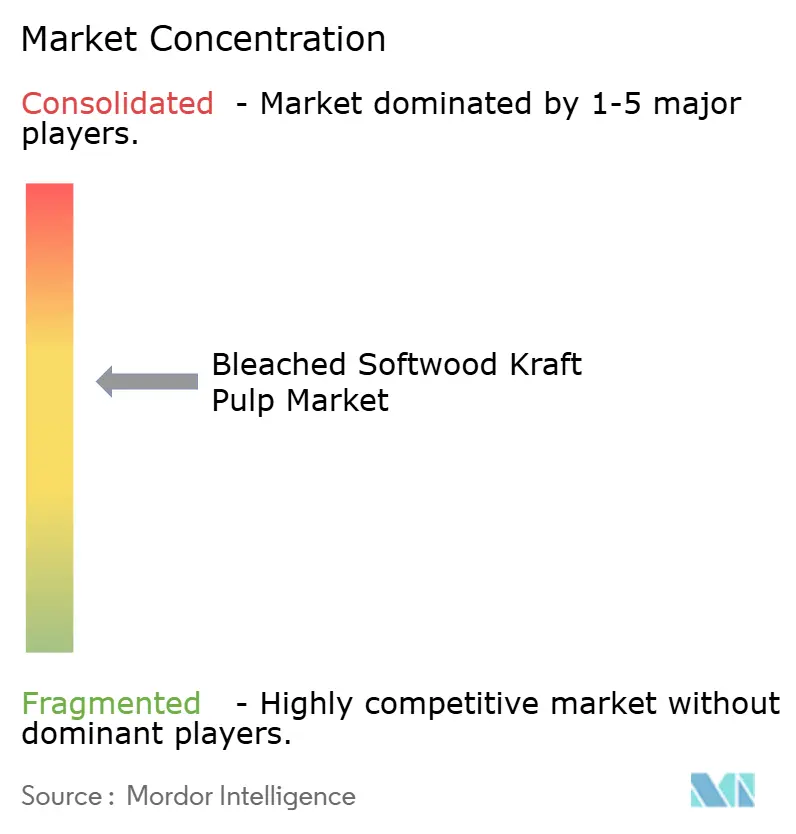

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bleached Softwood Kraft Pulp Market Analysis by Mordor Intelligence

The Bleached Softwood Kraft Pulp Market size is expected to increase from USD 24.56 billion in 2025 to USD 25.23 billion in 2026 and reach USD 31.34 billion by 2031, growing at a CAGR of 4.43% over 2026-2031.

The bleached softwood kraft pulp (BSKP) market remains supported by the role of long softwood fibers in applications that need tensile strength, wet-web integrity, and tear resistance, especially in tissue, fluff pulp, reinforced containerboard linerboard, and heavy-duty sack kraft. In 2026, the market is still working through the inventory overhang built during 2024 and 2025, but ongoing mill shutdowns and curtailments are shifting the rebalancing process toward supply discipline rather than a collapse in end demand. The market also reflects a split in demand conditions, with tissue and fluff pulp staying firm, packaging linked to industrial and e-commerce cycles, and printing and writing grades facing continued substitution pressure. Pricing behavior in 2026 continues to show a gap between NBSK and bleached hardwood kraft pulp, which has encouraged selective substitution in lower-performance paper grades but has not displaced softwood pulp in applications where performance thresholds remain strict. Over the medium term, the bleached softwood kraft pulp market is likely to be shaped by constrained boreal fiber supply, long forestry rotation cycles, and a gradual recovery window between 2026 and 2028 as excess inventories ease and higher-value applications keep demand anchored.

Key Report Takeaways

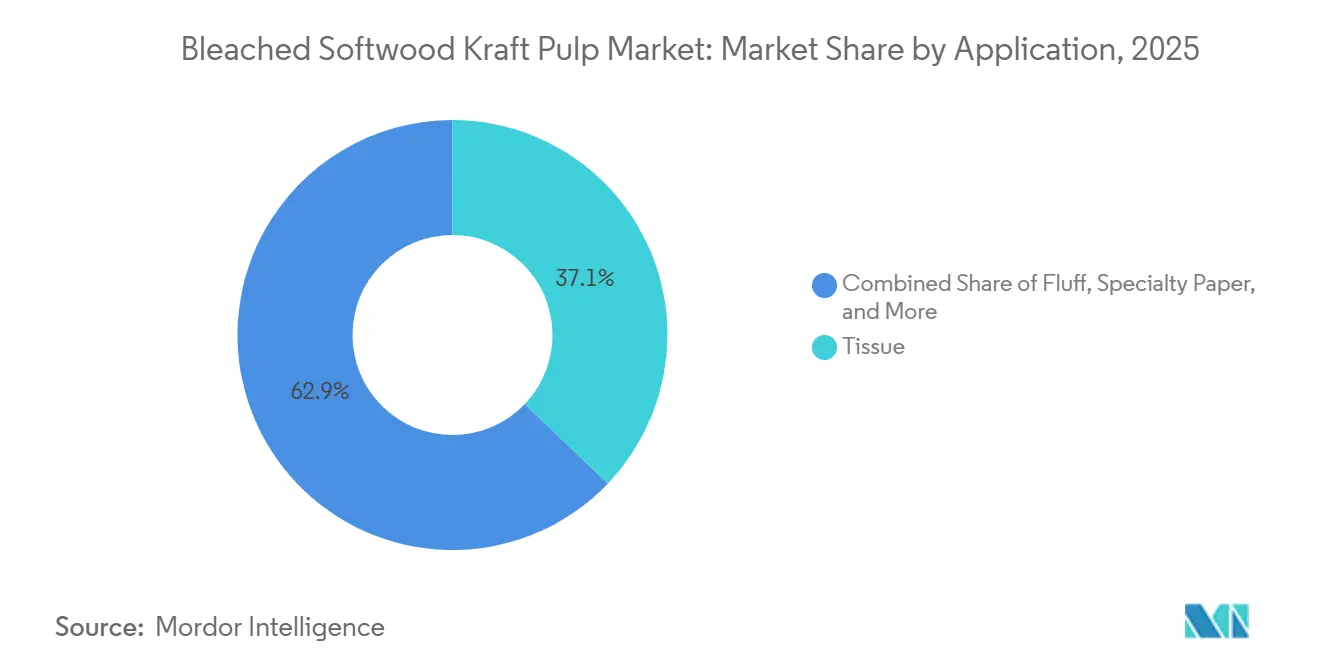

- By application, tissue held 37.13% of the bleached softwood kraft pulp market share in 2025 and is projected to expand at a 5.87% CAGR through 2031.

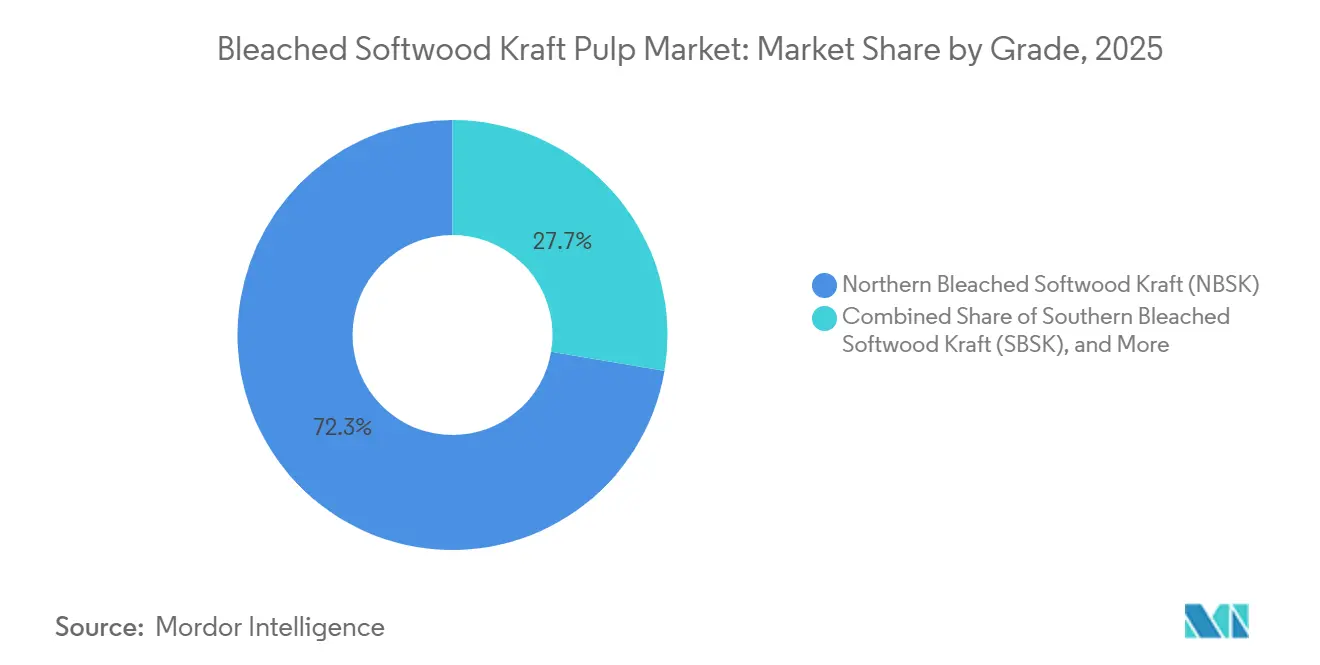

- By grade, Northern Bleached Softwood Kraft (NBSK) accounted for 72.34% share of the bleached softwood kraft pulp (BSKP) market size in 2025, while Southern Bleached Softwood Kraft (SBSK) is projected to expand at a 5.52% CAGR through 2031.

- By geography, Asia-Pacific held 38.76% of the bleached softwood kraft pulp market in 2025, while the Middle East and Africa is projected to record the fastest regional growth at a 6.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bleached Softwood Kraft Pulp Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Irreplaceable role of long fiber in strength applications | +1.5% | Global | Long term (≥ 4 years) |

| Growth in containerboard requiring reinforcement layers | +1.0% | North America and Asia-Pacific | Medium term (2-4 years) |

| E-commerce-induced packaging stress requirements | +0.7% | North America, Europe, China | Medium term (2-4 years) |

| Limited substitution possibility in high-performance grades | +0.4% | Global | Long term (≥ 4 years) |

| Expansion of industrial paper and heavy-duty bags | +0.3% | Asia-Pacific, Middle East and Africa, South America | Medium term (2-4 years) |

| Improved quality standards in packaging and hygiene products | +0.2% | Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Irreplaceable Role Of Long Fiber In Strength Applications

The bleached softwood kraft pulp market continues to depend on long fiber where strength performance cannot be compromised. Softwood kraft pulp fibers at 2.5–4.5 millimeters give paper makers the bonding network and sheet continuity needed in grades that rely on tensile, burst, and tear properties. Billerud’s Karlsborg NBSK specification shows that the grade meets FDA and EU food contact requirements while also delivering the strength profile expected in demanding furnish designs. SCA’s Östrand mill is supplying NBSK into tissue, packaging paper, and specialty paper, and the company is still planning capacity growth from a base already above 1 million tonnes per year. That combination of product requirements and supply commitment means the bleached softwood kraft pulp (BSKP) market keeps a resilient demand floor even when buyers try to optimize costs with more hardwood content.

Growth In Containerboard Requiring Reinforcement Layers

The bleached softwood kraft pulp market is also supported by the use of reinforcement fibers in containerboard liner and medium. AF&PA reported that total containerboard production in Q1 2026 fell 8% from Q1 2025, yet inventories at the end of Q1 2026 were still 3% lower than at the end of Q4 2025, which points to tighter operating balance after capacity reductions.[1]American Forest and Paper Association, “AF and PA Releases Q1 2026 Containerboard Quarterly Report,” TAPPI OnDemand Smurfit Westrock stated in its April 2026 earnings call that it had reached near sold-out status for nearly every fiber grade in Q1 2026 and had launched another round of price increases to address higher costs. Containerboard does not use bleached softwood pulp everywhere, but premium reinforcement layers still depend on softwood fiber where edge crush and burst targets are strict. As box demand improves from March through Q2 2026 and available linerboard supply remains disciplined, the bleached softwood kraft pulp (BSKP) market gains support from mills that need dependable reinforcement quality rather than the lowest-cost furnish.

E-Commerce-Induced Packaging Stress Requirements

The bleached softwood kraft pulp market benefits from the way e-commerce shipping raises the strength requirement of corrugated packaging. Direct-to-consumer shipments face repeated handling, stacking, and transport exposure, which increases the value of strong fiber in double-wall and heavy-duty single-wall constructions. Smurfit Westrock’s 2025 Form 10-K said e-commerce packaging demand contributed to new business wins entering 2026 and supported the company’s fiber grade portfolio. That matters because shipment growth in online channels changes not only the number of boxes used, but also the performance standard expected from each box. As logistics networks expand across North America, Europe, and China, the bleached softwood kraft pulp market keeps a role in the high-strength grades that protect goods with higher weight, higher value, or longer delivery paths.

Limited Substitution Possibility In High-Performance Grades

The bleached softwood kraft pulp market remains protected in part because substitution is limited in tissue, fluff pulp, and sack kraft. TAPPI Paper360 reported that tissue producers in Europe raised hardwood ratios where possible in late 2025, but wet burst and caliper targets in multi-ply bathroom tissue and kitchen towel still required a practical softwood floor of 25%–35% of the furnish. Stora Enso described fluff pulp as a structurally defensible business and committed to restructuring at Skutskär to increase fluff capacity after closing the softwood paper pulp fiberline. Fluff pulp has almost no hardwood substitute because absorption and rewet performance depend on the morphology of softwood cellulose. This gives the bleached softwood kraft pulp (BSKP) market a layer of demand visibility that extends beyond short-term pricing pressure and supports producer planning in the higher-value end uses.[2]TAPPI Paper360, “Uncertainty Dominates Tissue Markets,” TAPPI

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structurally higher cost vs hardwood alternatives | -0.8% | Global, acute in Europe and Asia | Long term (≥ 4 years) |

| Limited fiber availability due to long growth cycles | -0.6% | Canada, Nordic countries | Long term (≥ 4 years) |

| Dependence on sawmill output for wood chip supply | -0.4% | Canada, Nordic countries | Medium term (2-4 years) |

| Exposure to forestry disruptions from fires, pests, and climate impacts | -0.3% | Canada, western United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Structurally Higher Cost Vs Hardwood Alternatives

The bleached softwood kraft pulp market faces a clear cost challenge against bleached hardwood kraft pulp. Softwood pulp production requires more expensive fiber input, longer fiber preparation, and process conditions that preserve long-fiber integrity, so the cost base remains structurally above eucalyptus-based hardwood supply. Metsä Group stated in its full-year 2025 results that softwood market pulp demand remained muted in Europe and China and that partial replacement with hardwood pulp was reducing NBSK volumes in end products. Mercer International’s One Goal One Hundred program had reached USD 41 million in savings through Q1 2026 against a USD 100 million target, which shows how strongly producers are focused on internal cost reduction rather than assuming price recovery will solve the issue. Even with that response, the bleached softwood kraft pulp (BSKP) market is unlikely to close the core wood cost gap with plantation hardwood during the forecast period, so substitution pressure will continue in lower-performance grades.

Limited Fiber Availability Due To Long Growth Cycles

The bleached softwood kraft pulp market also faces a supply ceiling because boreal softwood fiber cannot be expanded quickly. Canadian and Scandinavian forests need 40–100 years to reach pulpwood maturity, and that long cycle sharply limits the pace of new capacity additions. Canfor Pulp said in May 2024 that the indefinite curtailment of one line at Northwood, equal to around 300,000 tonnes of annual NBSK capacity, was caused by a decline in the availability of economic fiber in northern British Columbia. UPM reported that pulpwood costs in Finland were lower year over year in Q1 2026, but that relief did not change the long-term scarcity of expansion-grade fiber in established boreal sourcing regions. As a result, the bleached softwood kraft pulp (BSKP) market is likely to remain structurally tight on the supply side even when demand cycles are uneven, because the underlying forestry constraint does not reset within a normal investment horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Tissue Remains The Core Demand Engine

Tissue accounted for 37.13% share of the bleached softwood kraft pulp market size in 2025, and it is also projected to expand at a 5.87% CAGR through 2031. That combination makes tissue the largest and fastest-growing application in the bleached softwood kraft pulp industry. The segment benefits from two parallel demand streams, stable premiumization in mature economies and faster per-capita adoption in Southeast Asia and South Asia. TAPPI Paper360 said private-label tissue could approach 40% of volume in developed markets, which is equal to the demand created by two tissue machine capacities each year. The performance requirement also matters, because multi-ply tissue outer plies still depend on long-fiber density to meet softness, caliper, and wet strength targets that hardwood-heavy furnishes struggle to achieve.

Fluff pulp remains the second most important application from a strategic standpoint because it is tied to adult incontinence, baby diaper, and feminine hygiene demand. Stora Enso’s 2025 capital markets material described fluff pulp as a defensible segment and linked its Skutskär restructuring directly to higher fluff output, which shows that producers are actively shifting toward more durable demand pockets. Packaging stays volume significant, but the use case is more selective because BSKP mainly reinforces multi-ply linerboard rather than setting the full furnish mix. Canfor’s product material highlights reinforcement strength and ease of refining for tissue, packaging, and filter grades, which explains why the grade retains value where paper makers need dependable runnability and strength rather than the lowest possible furnish cost. Printing and writing paper continues to decline, while specialty paper keeps a premium role for brightness and formation-sensitive uses, so the application mix in the bleached softwood kraft pulp (BSKP) market is gradually shifting toward hygiene, specialty, and performance packaging rather than legacy paper grades.

By Grade: NBSK Leads The Base While SBSK Gains Momentum

Northern Bleached Softwood Kraft (NBSK) held 72.34% of the bleached softwood kraft pulp market in 2025, which reflects the premium attached to slow-grown spruce, pine, and fir from Canada and the Nordic region. The grade remains dominant in the bleached softwood kraft pulp industry because cold-climate growth creates long, slender, and flexible fibers that paper makers value for tear strength and sheet integrity. Billerud describes its Karlsborg NBSK as long-fiber pulp from pine and spruce harvested in northern Sweden and notes certifications that support traceability and quality assurance for demanding end uses. SCA’s Östrand mill remains one of the world’s largest NBSK lines and is targeting expansion to 1.2 million tonnes per year using 100% green electricity, which strengthens the competitive position of Nordic NBSK in premium and lower-carbon supply chains. This leaves NBSK with a structural lead in premium tissue, specialty paper, and reinforcement applications where performance consistency carries more weight than simple cost comparison.

Southern Bleached Softwood Kraft (SBSK) is projected to expand at a 5.52% CAGR from 2026 to 2031, making it the faster-growing grade in the bleached softwood kraft pulp market. Its advantage comes from the US South, where pine rotations of 25–35 years provide more supply elasticity than the much longer boreal cycle in Canada and Scandinavia. Smurfit Westrock says its SBSK grade delivers strength, uniformity, and print brilliance for packaging, displays, and tissue, which aligns well with end markets that value both runnability and appearance. US South mills also have more room to shift between fluff and SBSK depending on pricing conditions, which gives operators a flexibility advantage that northern NBSK mills do not have to the same extent. Near-term price pressure in early 2026 does not change that broader position, because the medium-term outlook still rests on tissue, hygiene, and packaging demand that can absorb additional SBSK availability as the market normalizes.

Geography Analysis

Asia-Pacific held 38.76% of the bleached softwood kraft pulp market share in 2025, making it the largest regional demand center. China remains the key factor because it is the largest importer and the marginal price-setting buyer in the seaborne NBSK trade. The region’s tissue sector continues to draw imported BSKP into premium multi-ply tissue production, while paperboard and hygiene products create a broader demand base across the region. India and Indonesia are moving up in importance as rising incomes and modern retail formats increase per-capita paper consumption. Japan remains a mature but demanding outlet for high-brightness tissue and specialty grades, which helps preserve premium import demand in the region. Asia-Pacific also stays permanently import dependent because it lacks a large domestic boreal softwood resource base, so the bleached softwood kraft pulp (BSKP) market in the region remains highly sensitive to shipping costs, trade flows, and producer operating rates in exporting countries.

North America and Europe form the main production center of the bleached softwood kraft pulp market, with Canada supplying a major share of global NBSK output and Sweden and Finland forming the second major producer bloc. Europe’s consumption of bleached softwood kraft pulp fell by 10% in 2025 from 2024, reflecting hardwood substitution pressure in printing and writing papers even as tissue demand remained more resilient. The EUDR is adding compliance and traceability costs for exporters selling into Europe, and UPM said it was carrying out compliance work during the transition period to meet the full requirements. Production geography inside North America is also shifting because British Columbia has been losing capacity while eastern Canada is receiving strategic investment. Canada Infrastructure Bank said J.D. Irving’s Project NextGen in Saint John is a USD 1.5 billion modernization supported by a USD 660 million loan and is intended to lift production by more than 70% while cutting greenhouse gas emissions per tonne by half.[3]Canada Infrastructure Bank, “Irving New Brunswick Pulp Mill Undergoing Dramatic Transformation,” Canada Infrastructure Bank, cib-bic.ca.

The Middle East and Africa is projected to record the fastest regional growth at a 6.31% CAGR from 2026 to 2031 in the bleached softwood kraft pulp market. Demand is being supported by urbanization, broader food and consumer goods packaging needs, and tissue capacity growth in countries with little local fiber supply. Saudi Arabia’s Vision 2030 program is encouraging downstream packaging investment, while Egypt and Nigeria are building tissue demand from a growing urban middle class. Sub-Saharan Africa starts from a very low consumption base, which gives the region a long runway for growth even without a large local pulp industry. South America remains more important as a production and logistics region than as a demand center for BSKP, but growing packaging demand in Brazil and Argentina is still absorbing incremental volumes. Arauco’s broader infrastructure buildout for pulp exports in Brazil is centered on hardwood pulp, yet it still improves regional logistics that can indirectly support trade efficiency for the bleached softwood kraft pulp (BSKP) market across the South American export chain.

Competitive Landscape

The bleached softwood kraft pulp market is moderately concentrated, with a limited set of Nordic and North American producers holding much of global NBSK capacity. Metsä Group, UPM, SCA, and Stora Enso remain central in the Nordic supply base, while Mercer International, Canfor, West Fraser, and J.D. Irving shape the Canadian position, and Domtar, Smurfit Westrock, and Global Cellulose Fibers anchor SBSK production in the United States. The current competitive pattern is less about aggressive share capture and more about who can hold margins through cost control, fiber access, and operating flexibility. That is why the bleached softwood kraft pulp market in 2026 shows a divide between efficient incumbents that are still investing and higher-cost assets that are being curtailed, reconfigured, or closed.

Mercer International’s One Goal One Hundred program is a clear example of this response, with the company targeting USD 100 million in annualized improvements by the end of 2026 and reaching USD 41 million in savings through Q1 2026. SCA represents another approach, because it is pushing capacity growth at Östrand and using a large-scale asset with green electricity as a benchmark position in lower-carbon NBSK supply. Stora Enso is reshaping its mix by closing softwood fiberline 3 at Skutskär and shifting the mill toward fluff pulp, which shows a deliberate move toward applications with better margins and stronger demand durability. Canfor and other Canadian operators are also managing around fiber scarcity in British Columbia, so capacity decisions are tied as much to raw material economics as to pulp prices. These strategic moves show why the bleached softwood kraft pulp market is being shaped by portfolio quality, fiber security, and operational resilience more than by short-lived price spikes.

Technology and process design are becoming stronger competitive tools in the bleached softwood kraft pulp market. Metsä Fibre selected ANDRITZ’s LoSolids single-vessel continuous cooking technology for the Kemi bioproduct mill modernization, with startup scheduled for Q4 2026 and the ability to process both softwood and hardwood within a 1.5 million tonne annual capacity system.[4]ANDRITZ AG, “Metsä Fibre Selects ANDRITZ for Major Cooking System Modernization at Kemi Mill,” ANDRITZ, andritz.com. That kind of flexibility helps leading mills improve yield, widen raw material options, and reduce operational risk when fiber markets tighten. The market also offers room for low-carbon and fully certified supply, where established forestry management systems and chain-of-custody credentials give companies such as Billerud and SCA a stronger position with premium tissue and specialty paper buyers. Alternative fibers are still not a credible threat in these high-performance applications, so established producers continue to control the technical edge in the competitive structure.

Bleached Softwood Kraft Pulp Industry Leaders

Metsä Group

UPM-Kymmene Corporation

Mercer International Inc.

Celulosa Arauco y Constitución S.A.

Svenska Cellulosa Aktiebolaget SCA (publ)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Metsä Fibre, part of Metsä Group, selected ANDRITZ to modernize the cooking system at its Kemi bioproduct mill in Finland. The conversion to ANDRITZ LoSolids single-vessel continuous cooking technology, with startup scheduled for Q4 2026, will enable the mill to process both softwood and hardwood, supporting a total annual production capacity of 1.5 million tonnes and significantly reducing odorous gas emissions.

- May 2026: Stora Enso announced plans to permanently close softwood pulp fiberline 3 (L3) at its Skutskär mill in Sweden during Q3-Q4 2026, citing declining European softwood pulp demand since 2023, falling prices, and rising wood costs resulting in negative margins for L3. The restructuring will refocus Skutskär's remaining capacity on fluff pulp to improve long-term competitiveness, the total mill capacity stands at 515,000 tonnes per year.

- May 2026: Metsä Fibre initiated a market-driven shutdown at its Joutseno pulp mill in Finland at the end of Q1 2026, citing ongoing demand weakness in European and Chinese markets and adjusting output to current conditions. The Joutseno shutdown followed a similar halt from June to December 2025.

Global Bleached Softwood Kraft Pulp Market Report Scope

Bleached Softwood Kraft Pulp (BSKP) is a high-strength chemical pulp manufactured from softwood species principally spruce, pine, and fir through the kraft (sulfate) process, followed by bleaching to remove residual lignin and attain high brightness. Distinguished by long, durable fibers that impart superior tensile strength, tear resistance, and reinforcing capability, BSKP is a critical furnish across tissue, fluff, printing and writing, specialty paper, and packaging grades.

The bleached softwood kraft pulp market report is segmented by application (tissue, fluff, printing and writing, specialty paper, packaging), grade (northern bleached softwood kraft (NBSK), southern bleached softwood kraft (SBSK), other grades), and geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Tissue |

| Fluff |

| Printing and Writing |

| Specialty Paper |

| Packaging |

| Northern Bleached Softwood Kraft (NBSK) |

| Southern Bleached Softwood Kraft (SBSK) |

| Other Grades |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Nordics | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Middle East |

| Africa |

| By Application | Tissue | |

| Fluff | ||

| Printing and Writing | ||

| Specialty Paper | ||

| Packaging | ||

| By Grade | Northern Bleached Softwood Kraft (NBSK) | |

| Southern Bleached Softwood Kraft (SBSK) | ||

| Other Grades | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | |

| Africa | ||

Key Questions Answered in the Report

How large was the bleached softwood kraft pulp market in 2025 and what is the outlook to 2031?

The market was valued at USD 24.56 billion in 2025 and is forecast to reach USD 31.34 billion by 2031 at a 4.43% CAGR from 2026 to 2031.

Which application drives the most demand for bleached softwood kraft pulp?

Tissue is the largest application, with 37.13% of consumption in 2025, and it is also the fastest-growing application at a 5.87% CAGR through 2031.

Why is softwood kraft pulp difficult to replace in many paper grades?

Long softwood fibers provide tensile strength, tear resistance, and wet-web integrity that hardwood pulp cannot fully match in premium tissue, fluff pulp, and sack kraft applications.

Which grade is dominant and which one is growing faster?

NBSK led with a 72.34% share in 2025, while SBSK is projected to grow faster at a 5.52% CAGR through 2031.

Which region leads demand and which region is expanding fastest?

Asia-Pacific held the largest regional share at 38.76% in 2025, while the Middle East and Africa is projected to post the fastest growth at a 6.31% CAGR through 2031.

What is the main risk to supply over the forecast period?

The biggest supply risk is limited fiber availability, because boreal forests require long growth cycles and several producing regions are already facing tighter harvest conditions and curtailments.

Page last updated on: