Ultrasound Image Analysis Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

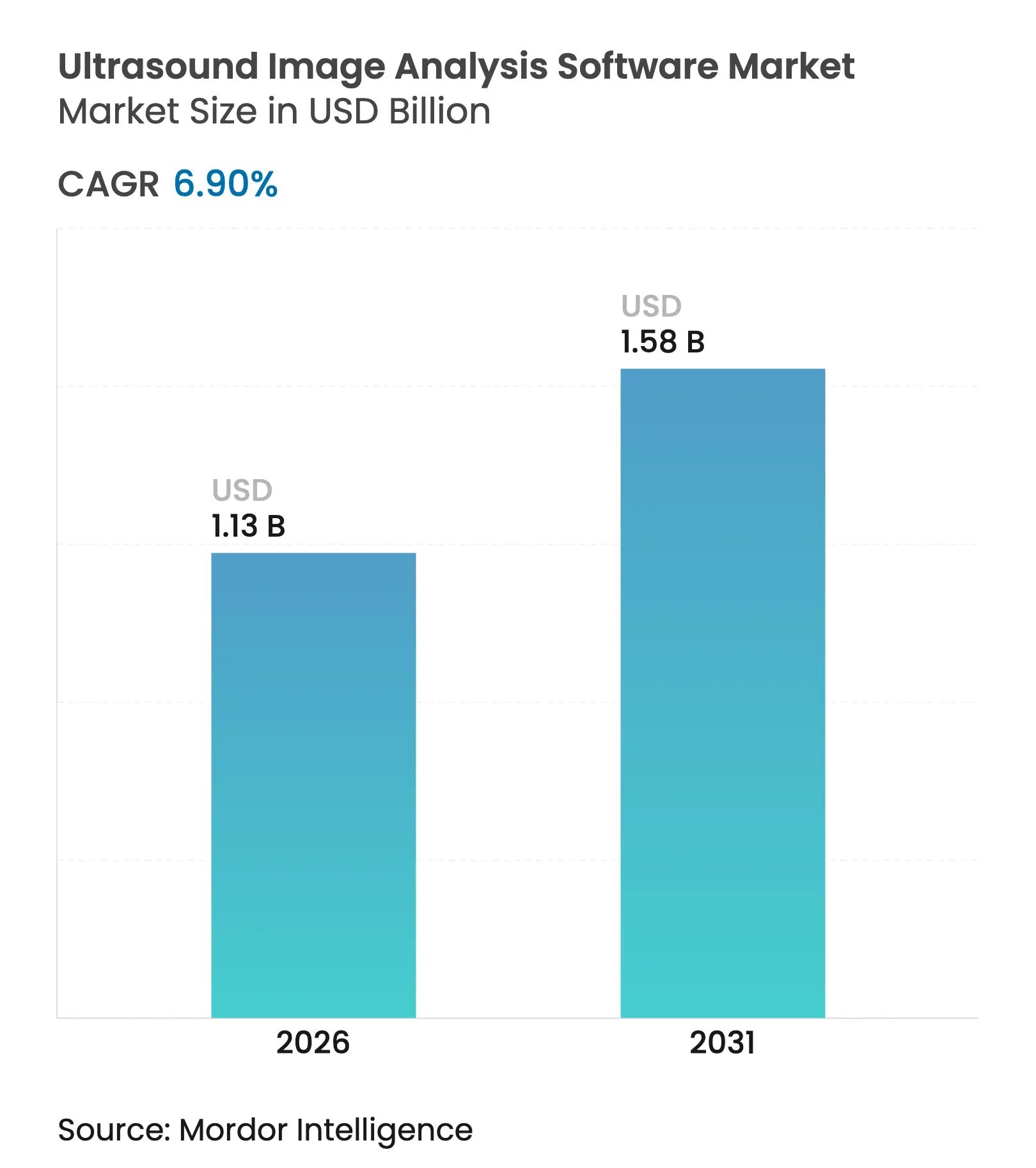

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 6.90 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ultrasound Image Analysis Software Market Analysis by Mordor Intelligence

The ultrasound image analysis software market size is expected to grow from USD 1.06 billion in 2025 to USD 1.13 billion in 2026 and is forecast to reach USD 1.58 billion by 2031 at 6.90% CAGR over 2026-2031. This outlook positions the ultrasound image analysis software market as a vital digital health segment, benefiting from AI-driven automation that shortens reading times, boosts diagnostic confidence, and alleviates workforce shortages. Integrated AI modules that automate routine measurements, standardize reporting, and flag anomalies in real time are migrating from research pilots into everyday clinical practice. Point-of-care ultrasound (POCUS) and handheld devices, which grew sharply during pandemic-era bedside care protocols, now anchor the next growth wave. Hospitals demand software that plugs seamlessly into PACS/HIS stacks to unlock cross-departmental image exchange, while oncology, cardiology, and maternal-fetal medicine rely on advanced radiomics to personalize therapy selection. Cost pressures and an aging sonographer cohort continue to accelerate adoption of autonomous scanning and cloud-native collaboration tools, securing a solid long-term runway for the ultrasound image analysis software market.

Key Report Takeaways

- By software type, integrated solutions commanded 60.08% of ultrasound image analysis software market share in 2025; standalone software is projected to post a 9.07% CAGR to 2031.

- By product, 3D/4D systems captured 38.12% of the ultrasound image analysis software market size in 2025, while Doppler technology is forecast to expand at 10.66% CAGR to 2031.

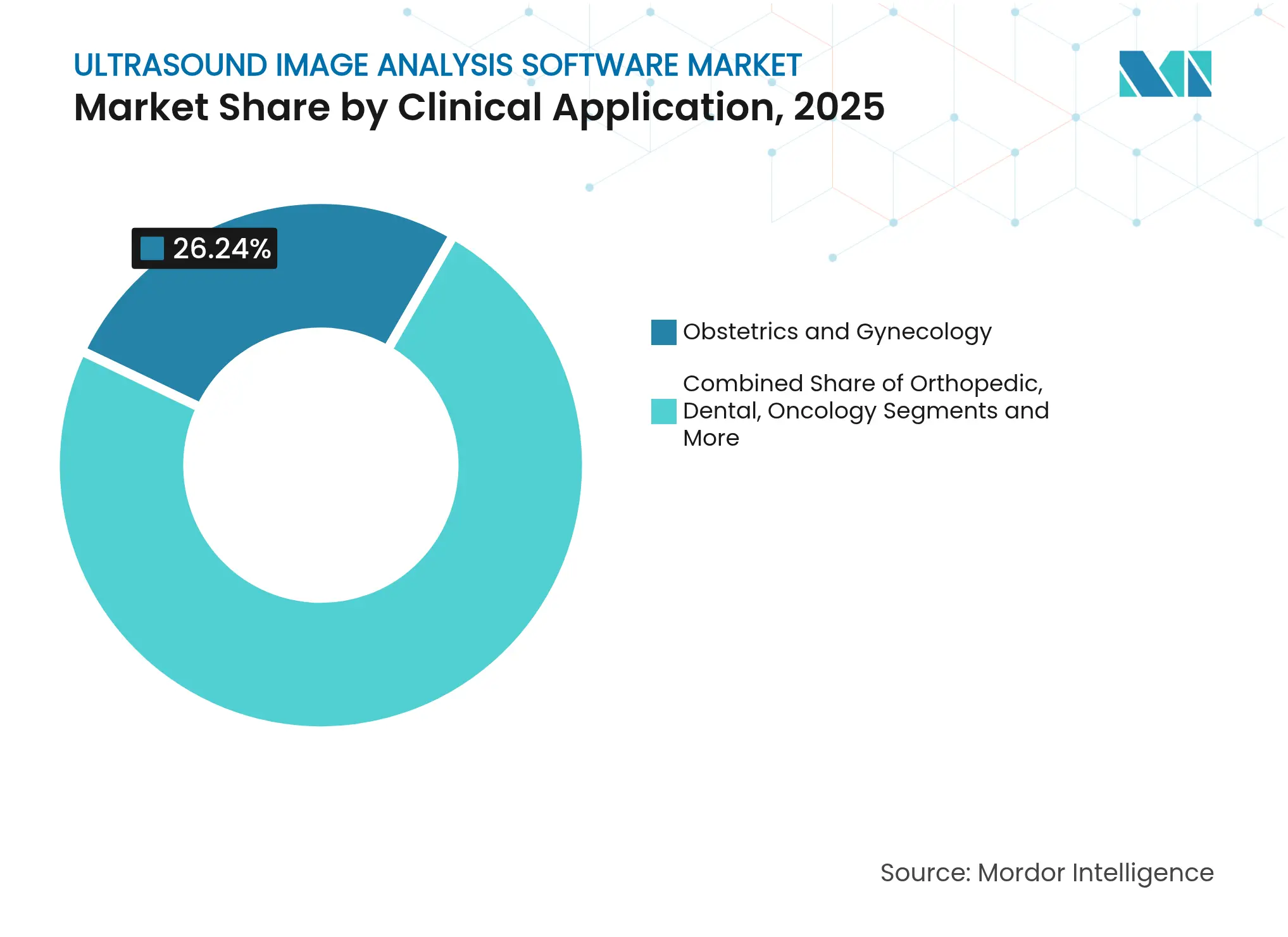

- By clinical application, obstetrics and gynecology led with 26.24% ultrasound image analysis software market share in 2025; oncology applications will advance at 10.69% CAGR through 2031.

- By end user, hospitals and ambulatory surgery centers held 48.11% of the ultrasound image analysis software market size in 2025, whereas diagnostic imaging centers are set for 8.98% CAGR growth through 2031.

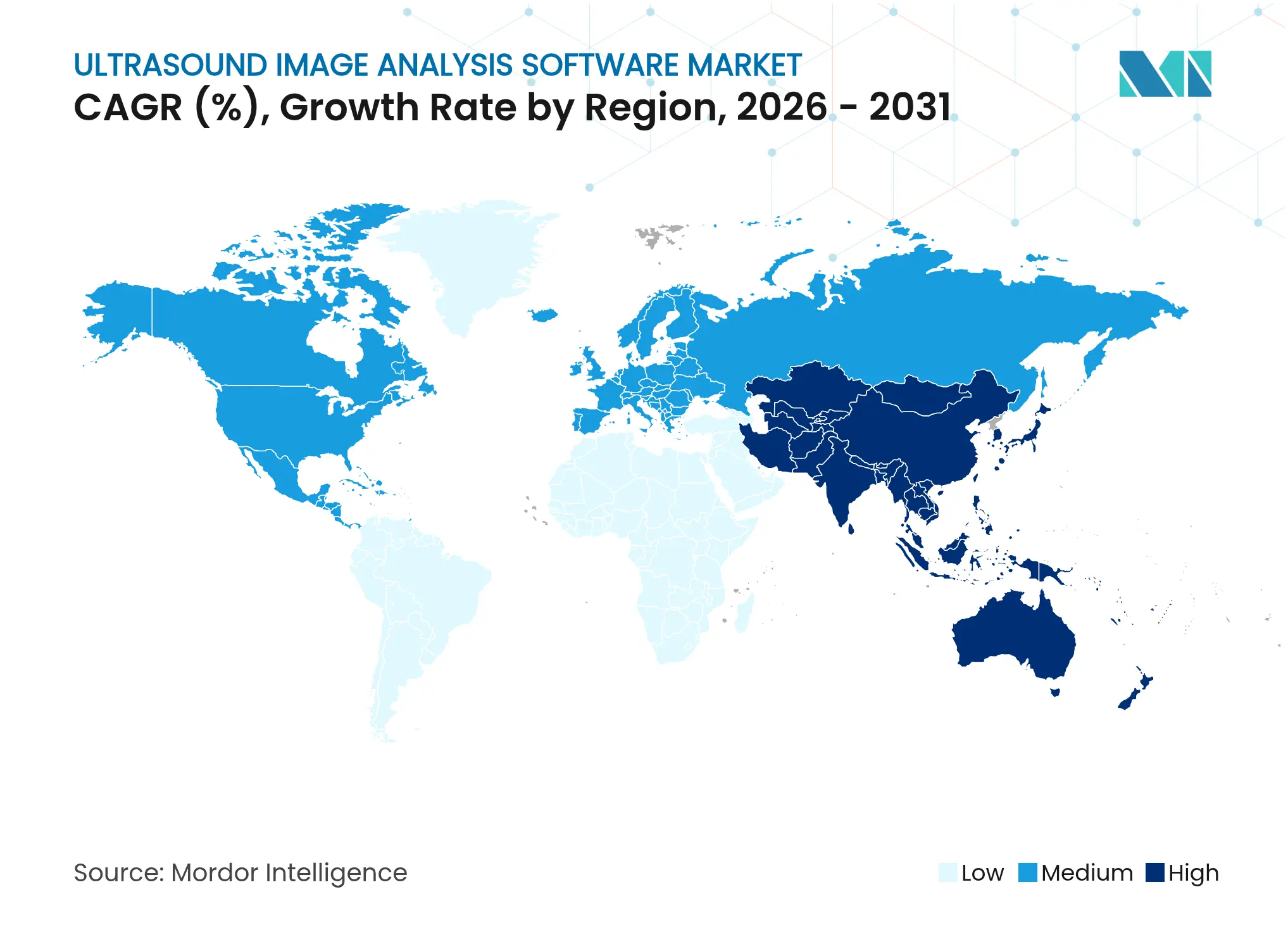

- By geography, North America contributed 40.95% revenue in 2025, yet Asia-Pacific is projected to see the fastest 9.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultrasound Image Analysis Software Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing burden of chronic diseases

Increasing burden of chronic diseases

| +1.8% | Global – most pronounced in North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.8%

| Geographic Relevance:

Global – most pronounced in North America & Europe

| Impact Timeline:

Long term (≥ 4 years)

|

Rapid AI + ML innovation in ultrasound

Rapid AI + ML innovation in ultrasound

| +2.1% | Global – led by North America & Asia-Pacific | Medium term (2-4 years) | |||

Surging demand for point-of-care/handheld

Surging demand for point-of-care/handheld

| +1.5% | Global – strongest in Asia-Pacific & MEA | Short term (≤ 2 years) | |||

Hospital workflow digitalisation mandates

Hospital workflow digitalisation mandates

| +1.2% | North America & EU, expanding in Asia-Pacific | Medium term (2-4 years) | |||

Cloud-native tele-sonography platforms

Cloud-native tele-sonography platforms

| +0.9% | Early adoption in developed markets | Medium term (2-4 years) | |||

Ultrasound radiomics uptake in oncology

Ultrasound radiomics uptake in oncology

| +0.7% | North America & EU, emerging in Asia-Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Burden Of Chronic Diseases

Escalating cardiovascular, diabetic, and oncologic caseloads are driving a 7% annual increase in ultrasound studies, especially in obstetric and gastroenterology clinics. Insufficient radiologist hours and limited sonographer supply intensify the need for automated post-processing that triages abnormal exams and reduces repeat scanning. Point-of-care ultrasound outperforms chest X-ray in pneumonia detection and lowers episode-of-care costs, validating software investment for value-based care providers. Emerging economies view ultrasound as the most affordable imaging entry point, so vendors that optimize algorithms for mid-tier hardware and intermittent connectivity unlock sizable addressable demand.

Rapid AI + ML Innovation In Ultrasound Analytics

Deep-learning pipelines now deliver real-time speckle reduction, automated biometry, and probability-based lesion categorization that guide novice operators. FDA clearances for Caption Guidance and similar tools indicate regulatory openness to AI ultrasound, yet only 59 of 950 cleared AI devices target sonography, highlighting scope for new submissions. Radiomics models built from head-and-neck ultrasound achieve >90% treatment-response prediction accuracy, illustrating clinical gains beyond workflow acceleration. Partnerships, such as GE HealthCare and NVIDIA, leverage parallel computing to pursue autonomous scanning, aiming to shift reliance from scarce human expertise to software.

Surging Demand For Point-Of-Care / Handheld Ultrasound

Smartphone-tethered probes and tablet-based consoles shrink acquisition costs and bring imaging to primary-care clinics, home visits, and austere settings. Pandemic protocols validated bedside lung and vascular scans, entrenching POCUS in standard triage. Comparative studies report image quality parity between six leading handheld devices and traditional systems for core abdominal views. AI guidance overlays that coach users on probe positioning lower training barriers and feed more consistent datasets for back-end analytics, sustaining momentum of the ultrasound image analysis software market.

Hospital Workflow Digitalisation & Data-Interoperability Mandates

Policy and payer quality programs reward closed-loop reporting and image exchange, prompting hospitals to phase out siloed carts. Implementations of AI-enabled workflow suites have cut documentation time by 45% and saved USD 428 per encounter[1]Kristin Pingili, “How Workflow Optimization Improves Patient Care,” International Journal of Research in Computer Applications and Information Technology, iaeme.com. Full DICOM-IHE compliance is now table stakes; however, legacy PACS environments complicate rollouts, reinforcing demand for vendor support and open APIs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shortage of trained sonographers & high price

Shortage of trained sonographers & high price

| -1.4% | Global – most acute in North America & EU | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-1.4%

| Geographic Relevance:

Global – most acute in North America & EU

| Impact Timeline:

Short term (≤ 2 years)

|

Interoperability gaps with legacy PACS/HIS

Interoperability gaps with legacy PACS/HIS

| -0.8% | North America & EU, emerging in Asia-Pacific | Medium term (2-4 years) | |||

AI bias & regulatory scrutiny on ethnic variance

AI bias & regulatory scrutiny on ethnic variance

| -0.6% | Global – strictest in North America & EU | Long term (≥ 4 years) | |||

Cyber-security risks in connected endpoints

Cyber-security risks in connected endpoints

| -0.5% | Highest in developed markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Shortage Of Trained Sonographers & High Software Price

Sonographer retirements average age 60.8, four years earlier than national averages, while 90% report musculoskeletal disorders from repetitive scanning[2]Jim Baun, “Early Retirement in the Sonography Community: What’s Next?” Journal of Diagnostic Medical Sonography, journals.sagepub.com. Vacancies force overtime and reduce mentoring capacity, constraining new graduate pipelines. AI modules that automate acquisitions can ease workloads but often carry premium license fees beyond small-clinic budgets, limiting uptake where staff shortfalls are most pronounced.

Interoperability Gaps With Legacy PACS/HIS

Hospitals still running ACR-NEMA-era archives face 4- to 12-month integration projects, delaying software benefits. Color-flow mis-registrations and metadata corruption degrade Doppler reads, demanding middleware and IT resourcing that many community sites lack.

Segment Analysis

By Software Type: Integrated Solutions Drive Market Consolidation

Integrated platforms generated 60.08% ultrasound image analysis software market share in 2025 as providers sought a single pane for acquisition, review, and archival. Bundled ecosystems cut training time and capitalize on existing hardware footprints, giving conglomerates like Philips and Siemens Healthineers cross-selling leverage. Standalone suites, though smaller, will outpace at 9.07% CAGR by 2031, propelled by niche AI analytics that plug into multi-vendor fleets. Oncology radiomics start-ups illustrate this tailwind, offering cloud APIs that overlay legacy scanners without forklift upgrades, positioning the ultrasound image analysis software market for a hybrid growth architecture.

Integrated dominance mirrors hospital sourcing that bundles service contracts and cybersecurity certifications into multi-year deals. Yet radiology groups and outpatient centers prize vendor-neutral engines that shield them from lock-in and enable rapid algorithm swaps. As reimbursement shifts toward value-based care, demand rises for outcome-tracking dashboards that aggregate longitudinal imaging data, an edge currently delivered faster by agile standalone vendors.

Note: Segment shares of all individual segments available upon report purchase

By Product: 3D/4D Technology Leads While Doppler Shows Strongest Growth

The 3D/4D category captured 38.12% of ultrasound image analysis software market size in 2025 thanks to volumetric fetal, cardiac, and oncologic imaging. Real-time rendering boosts patient engagement and improves anatomical delineation for surgical planning. Doppler variants, set to rise at 10.66% CAGR, ride global cardiovascular screening programs and AI flow-quantification that lifts sensitivity for stenosis detection.

AI-super-resolution algorithms now reconstruct clearer hemodynamic maps from standard Doppler data, extending utility to resource-limited clinics lacking high-end probes. Meanwhile, iterative deep-learning noise suppression revitalizes 2D platform sales, underscoring that incremental software advances can reinvigorate mature hardware lines.

By Clinical Application: Obstetrics Leadership Faces Oncology Challenge

Obstetrics held 26.24% ultrasound image analysis software market share in 2025 driven by mandated prenatal scans and AI-enabled anomaly screening. Automated measurement suites trim exam time and ensure guideline adherence, critical amid sonographer scarcity. Oncology, predicted at 10.69% CAGR, benefits from radiomics that stratify breast and liver tumors by histology, aiding therapy planning without invasive biopsy.

Cardiology software gains from AI echocardiography tools that quantify ejection fraction and wall-motion scores, while nephrology modules monitor chronic kidney disease progression. Specialty-centric algorithm libraries open premium SaaS revenue layers beyond base licenses, further diversifying the ultrasound image analysis software market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospital Dominance Challenged by Diagnostic Centers

Hospitals and ASCs contributed 48.11% of ultrasound image analysis software market size in 2025 owing to multi-disciplinary imaging demand and bundled EMR purchases. Yet regulatory cost pressure and outpatient migration propel imaging-center uptake at 8.98% CAGR. Independent centers deploy cloud PACS and AI triage to manage throughput with lean staff, positioning themselves as rapid-turnaround partners for accountable-care networks.

Academic institutes, while smaller in revenue, shape product roadmaps through early-phase validation of AI decision support and tele-mentoring frameworks. Their datasets reinforce FDA submissions and offer vendors critical feedback loops for algorithm bias mitigation.

Geography Analysis

North America retained 40.95% revenue leadership in 2025, underpinned by robust reimbursement policies and early adoption of AI-enabled imaging. Integrated software upgrades align with government initiatives that incentivize interoperable EHRs, creating fertile ground for the ultrasound image analysis software market. Workforce shortages—more than 1,400 open radiology posts—heighten reliance on automated measurement and reporting to maintain service levels. The region also pioneers cybersecurity governance, with new FDA mandates that extend Secure-Development-Lifecycle requirements to medical AI.

Asia-Pacific is forecast at 9.05% CAGR through 2031, reflecting hospital infrastructure build-outs and government policies that favor local manufacturing. China’s 85% local-content rules spur domestic software houses to embed AI within cost-optimized ultrasound consoles, accelerating technology diffusion. Southeast Asia’s USD 6.3 billion digital-health fund-raising underscores investor appetite for tele-imaging and cloud PACS start-ups, powering the ultrasound image analysis software market toward wider rural penetration.

Europe exhibits steady adoption shaped by GDPR-aligned data-sharing frameworks and cross-border research consortia that validate AI radiomics. Emerging economies in Africa and Latin America remain nascent but promising, with eHealth pilots showing potential 15% efficiency gains through tele-ultrasound triage and cloud archives. Success hinges on mobile-first designs that tolerate intermittent bandwidth and deliver low-power edge inference.

Competitive Landscape

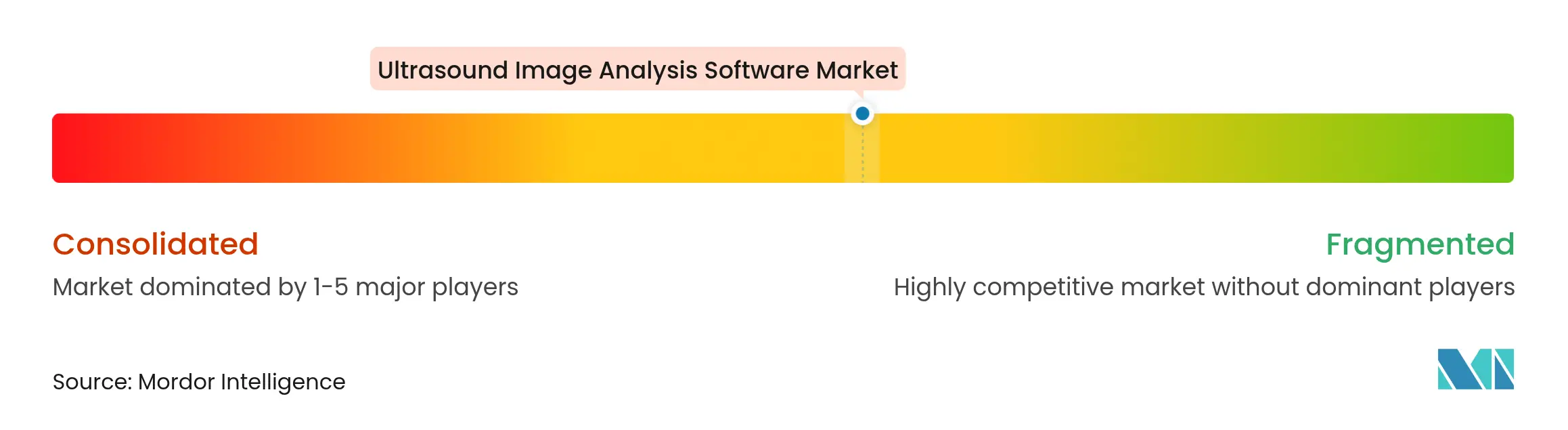

Market Concentration

Competition remains moderately fragmented as legacy equipment giants contend with agile AI vendors. GE HealthCare acquired Intelligent Ultrasound's clinical AI arm for USD 53 million, fortifying its installed base and enriching breast and vascular analytics modules. Samsung spent USD 92 million on fetal AI specialist Sonio, signaling a strategic pivot toward software-centric differentiation.

Start-ups target white-space niches, with Us2.ai and Fujifilm collaborating on automated echo quantification, and UltraSight and Mayo Clinic developing AI for novice-led cardiac POCUS. RadNet's 2025 acquisition of See-Mode Technologies expands screening algorithms for thyroid nodules and underscores diagnostic-center influence on product roadmaps.

Cyber-security and fairness oversight intensify competitive stakes. Vendors invest in diverse training cohorts and secure software bill-of-materials disclosures to comply with evolving rules, while patent filings for deep-learning reconstruction and autonomous scanning continue to climb. Market success increasingly hinges on demonstrating clinically validated AI that integrates into heterogeneous hospital IT ecosystems without locking buyers into proprietary silos.

Ultrasound Image Analysis Software Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: RadNet acquired See-Mode Technologies to enhance AI ultrasound screening for thyroid cancer.

- March 2025: GE HealthCare launched Invenia ABUS Premium, a 3D breast ultrasound with Verisound AI assistant.

Table of Contents for Ultrasound Image Analysis Software Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing Burden Of Chronic Diseases

- 4.2.2Rapid AI + ML Innovation In Ultrasound Analytics

- 4.2.3Surging Demand For Point-Of-Care / Handheld Ultrasound

- 4.2.4Hospital Workflow Digitalisation & Data-Interoperability Mandates

- 4.2.5Cloud-Native Tele-Sonography Platforms

- 4.2.6Ultrasound Radiomics Adoption In Oncology Trials

- 4.3Market Restraints

- 4.3.1Shortage Of Trained Sonographers & High Software Price

- 4.3.2Interoperability Gaps With Legacy PACS/HIS

- 4.3.3AI-Bias & Regulatory Scrutiny On Ethnic Performance

- 4.3.4Cyber-Security Risks In Connected Ultrasound Endpoints

- 4.4Technological Outlook

- 4.5Porter's Five Forces

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Software Type

- 5.1.1Integrated Software

- 5.1.2Standalone Software

- 5.2By Product

- 5.2.12D Ultrasound

- 5.2.23D / 4D Ultrasound

- 5.2.3Doppler Ultrasound

- 5.3By Clinical Application

- 5.3.1Orthopedic

- 5.3.2Dental

- 5.3.3Oncology

- 5.3.4Obstetrics & Gynecology

- 5.3.5Nephrology & Urology

- 5.3.6Radiology

- 5.3.7Cardiology

- 5.4By End User

- 5.4.1Hospitals & ASCs

- 5.4.2Diagnostic Imaging Centers

- 5.4.3Research & Academic Institutes

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Agfa HealthCare

- 6.3.2Canon Inc. (Canon Medical Systems)

- 6.3.3Esaote SpA

- 6.3.4GE HealthCare

- 6.3.5Image Analysis Group

- 6.3.6Infervision

- 6.3.7Koninklijke Philips N.V.

- 6.3.8Merative

- 6.3.9MIM Software

- 6.3.10Neusoft Corp.

- 6.3.11Siemens Healthineers

- 6.3.12Talan Group (Coexya)

- 6.3.13FUJIFILM Sonosite

- 6.3.14Butterfly Network

- 6.3.15Clarius Mobile Health

- 6.3.16Mindray Medical

- 6.3.17Hitachi Healthcare

- 6.3.18Hologic

- 6.3.19Terason

- 6.3.20ContextVision

- 6.3.21Median Technologies

- 6.3.22EchoNous

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Ultrasound Image Analysis Software Market Report Scope

Image analysis software, also known as image recognition or computer vision, processes images to extract details using artificial intelligence.

The market for ultrasound image analysis software is segmented by software type, product, clinical application, end user, and geography. By software type, the market is segmented into integrated software and standalone software. By product, the market is segmented into 2D ultrasound, 3D/4D ultrasound, and Doppler ultrasound. The clinical application segment is further segmented into orthopedic, dental, oncology, obstetrics and gynecology, nephrology and urology, radiology, and cardiology. By end user, the market is segmented into hospitals and ASCs, diagnostic imaging centers, and research and academic institutes. The geography segment is further segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major global regions. The report provides the value (in USD) for all the above segments.