Artificial Intelligence In Ultrasound Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

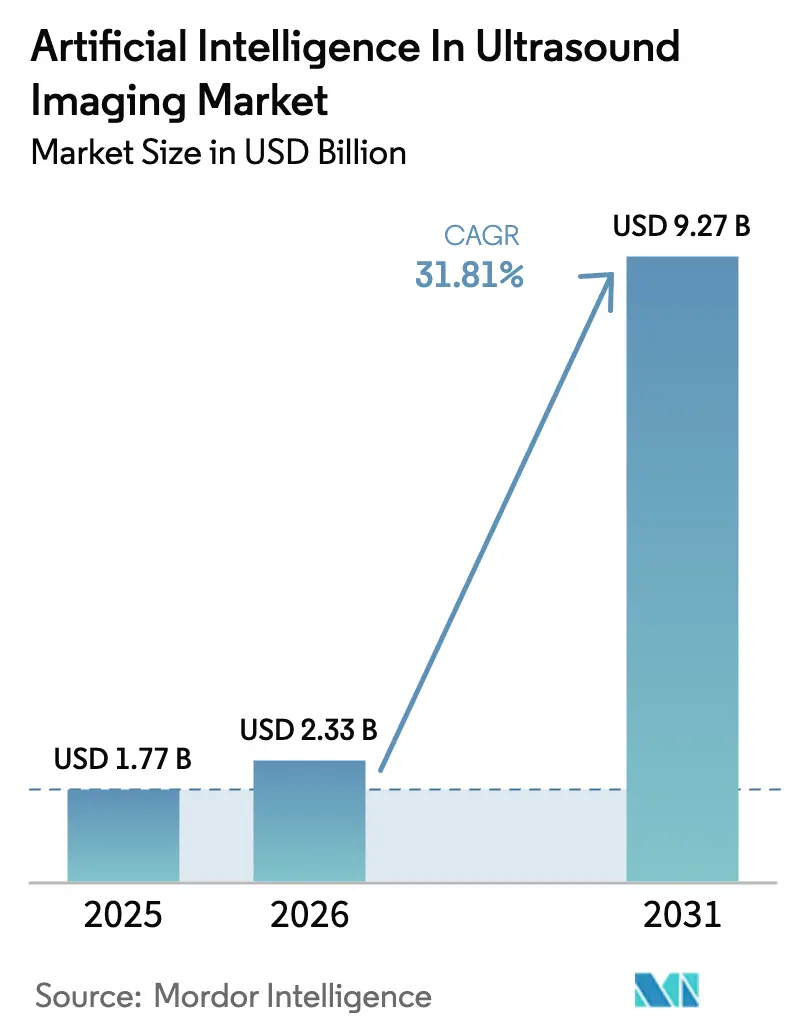

| Market Size (2026) | USD 2.33 Billion |

| Market Size (2031) | USD 9.27 Billion |

| Growth Rate (2026 - 2031) | 31.81% CAGR |

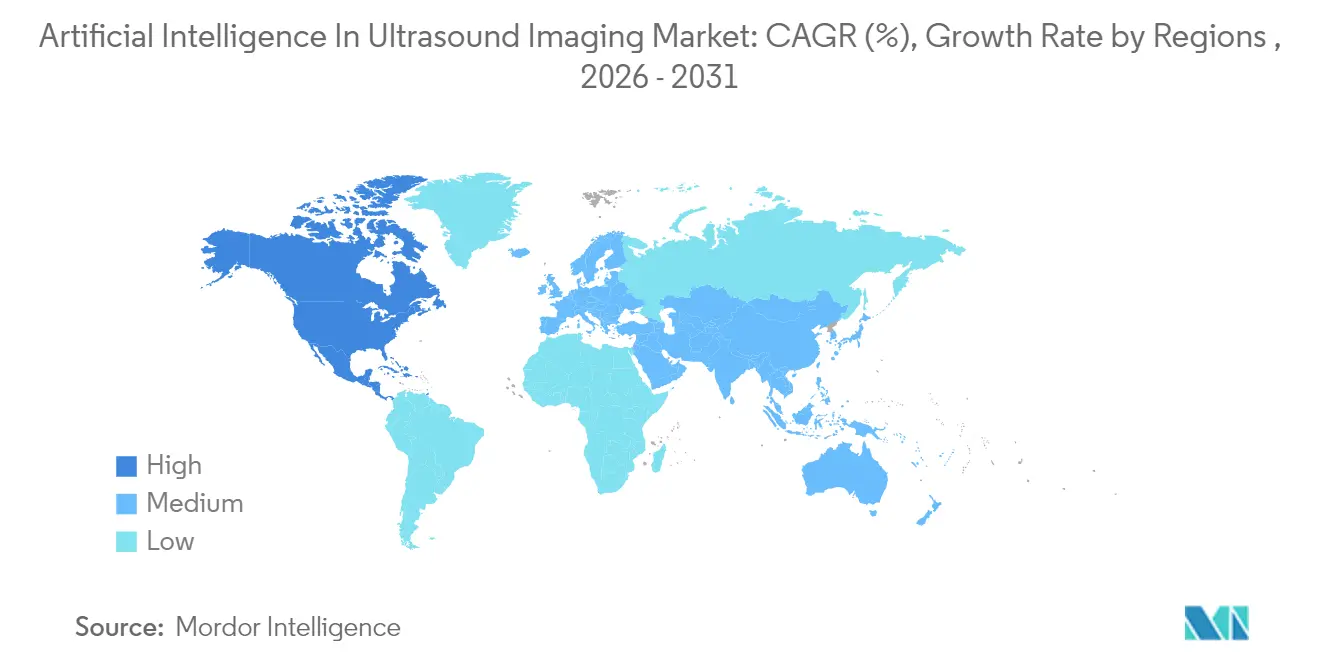

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

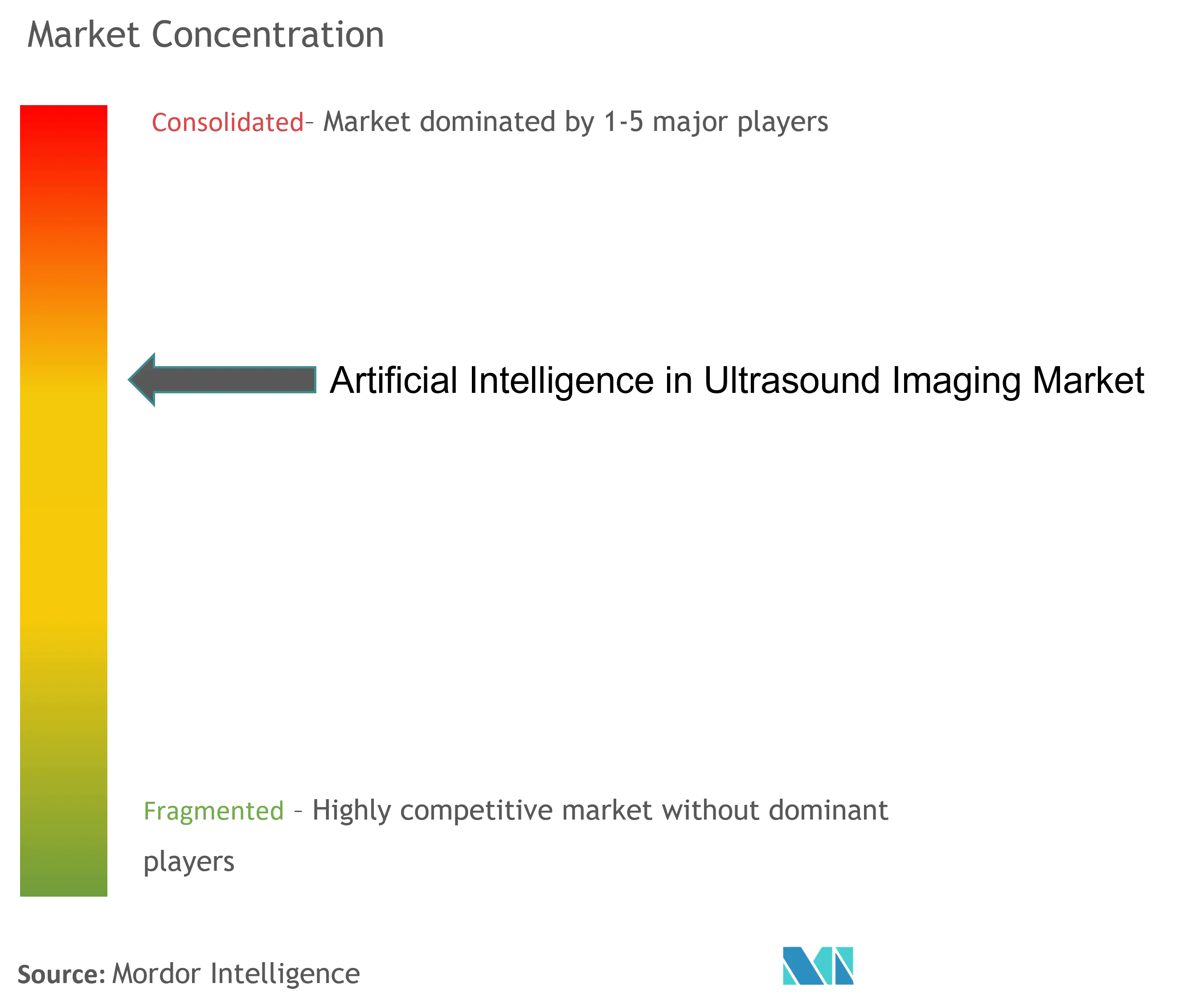

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence In Ultrasound Imaging Market Analysis by Mordor Intelligence

The AI in ultrasound imaging market size in 2026 is estimated at USD 2.33 billion, growing from 2025 value of USD 1.77 billion with 2031 projections showing USD 9.27 billion, growing at 31.81% CAGR over 2026-2031. Software-defined algorithms are rapidly replacing operator-dependent scanning, and reimbursement codes for AI-enabled echocardiography are accelerating enterprise adoption. Continuous miniaturization makes portable probes viable in primary care, while regulatory clarity from the FDA and Europe’s AI Act has shortened commercialization cycles. Strategic acquisitions by major device vendors signal an industry pivot toward full-stack AI platforms that link acquisition, interpretation, and reporting in a single workflow. In parallel, point-of-care ultrasound (POCUS) and wearable patches expand the addressable base, helping healthcare systems mitigate radiologist shortages and improve diagnostic consistency.

Key Report Takeaways

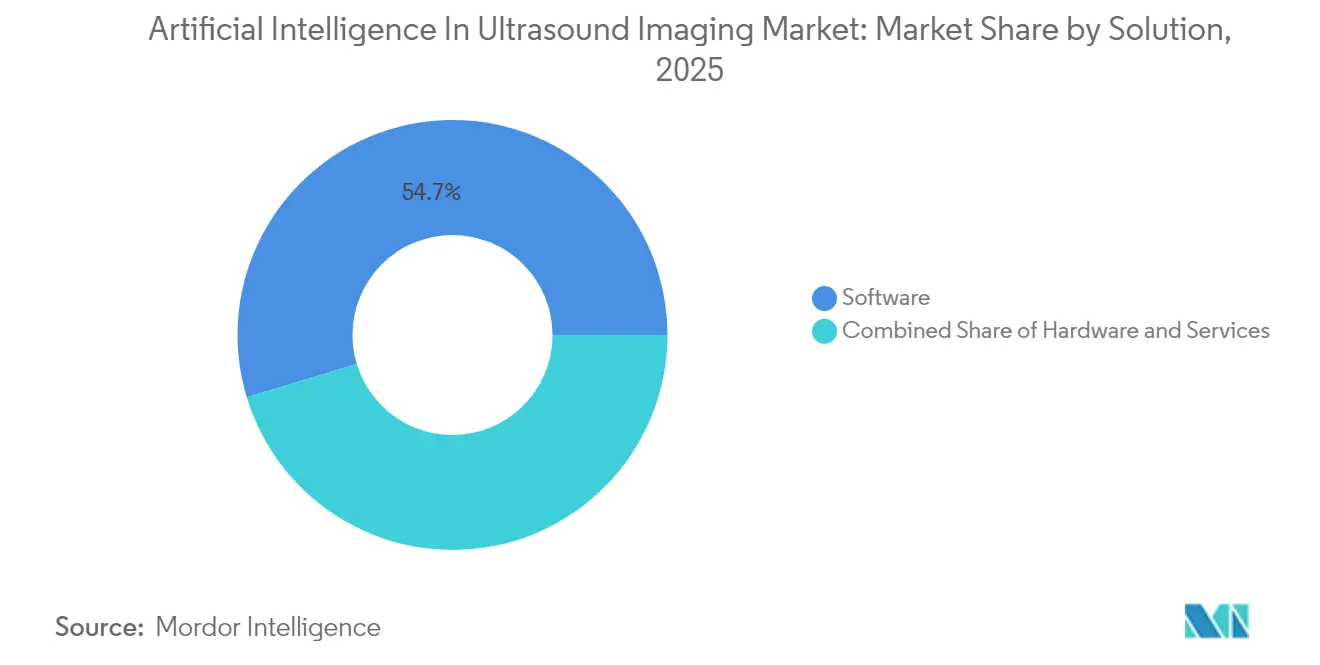

- By solution, software held 54.67% of the AI in ultrasound imaging market share in 2025, whereas services are projected to grow at 33.18% CAGR through 2031.

- By technology, machine learning led with 42.74% revenue share in 2025; context-aware computing is forecast to expand at 33.05% CAGR to 2031.

- By device type, handheld and probe-based systems captured 35.22% revenue in 2025; wearable and patch devices are set to rise at 33.29% CAGR through 2031.

- By imaging mode, 2-D retained 36.58% share in 2025, while volumetric imaging is poised for 33.64% CAGR to 2031.

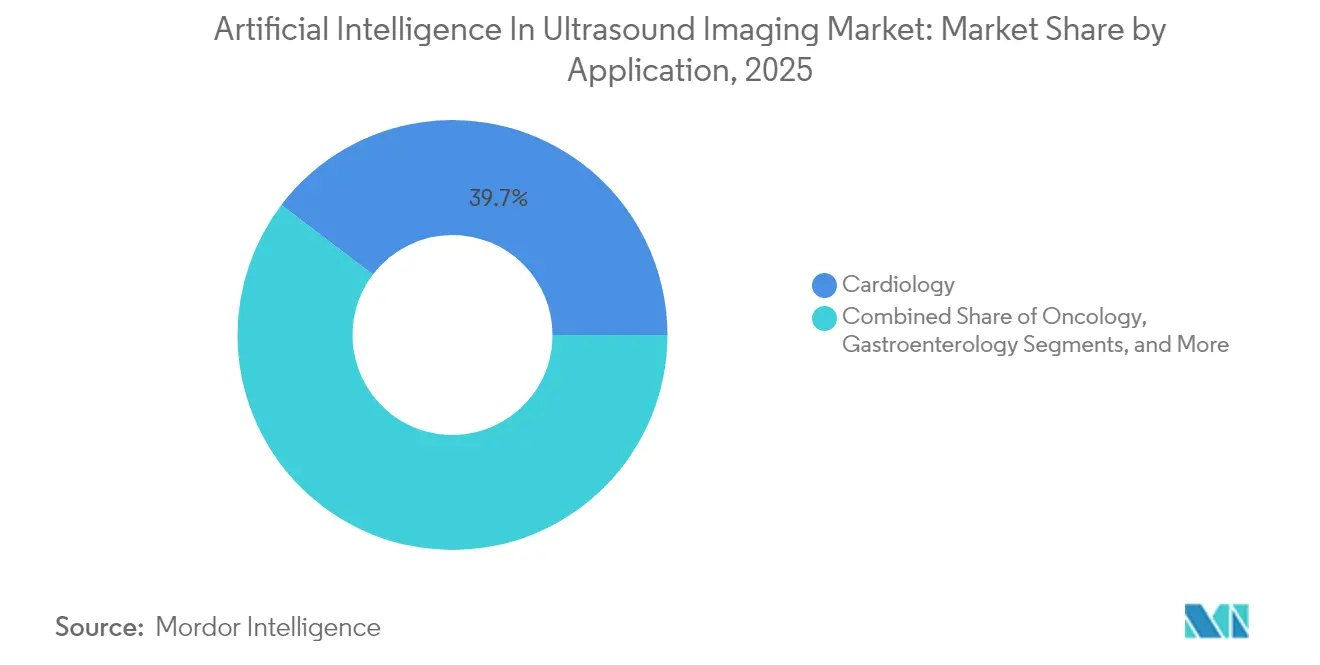

- By application, cardiology accounted for 39.66% of the AI in ultrasound imaging market size in 2025; obstetrics and gynecology will accelerate at 33.12% CAGR through 2031.

- By geography, North America dominated with 47.62% share in 2025; Asia-Pacific will grow fastest at 33.74% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Intelligence In Ultrasound Imaging Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in chronic diseases & aging population | +8.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Radiologist workload pressures & staffing shortages | +7.8% | Global, acute in North America & Western Europe | Medium term (2-4 years) |

| Government incentives & funding for AI health tech | +6.1% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Rapid POCUS adoption with integrated AI | +5.3% | Global, early gains in ambulatory settings | Short term (≤ 2 years) |

| CMS reimbursement codes for AI echocardiography software | + 2.9% | United States, potential expansion to Canada | Short term (≤ 2 years) |

| Cloud-native AI platforms enabling tele-ultrasound in LMICs | +2.8% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Chronic Diseases & Aging Population

Cardiovascular conditions remain the leading global cause of mortality, while diabetes prevalence is climbing in developing economies [1]World Health Organization, “Cardiovascular Diseases (CVDs),” who.int. These demographics create permanent demand for imaging that can be performed outside tertiary centers. AI-guided ultrasound lets non-specialists conduct diagnostic-grade scans, multiplying capacity without a proportional increase in radiologists. Chronic-disease pathways benefit because longitudinal monitoring becomes feasible at the bedside, improving adherence to value-based-care metrics and generating recurring software revenue for vendors.

Radiologist Workload Pressures & Staffing Shortages

Imaging volumes outstrip workforce growth. The American College of Radiology cites persistent staffing gaps across rural and urban hospitals [2]American College of Radiology, “Imaging Workforce Trends,” acr.org. Sonographers are retiring at 60.8 years on average, earlier than the general labor forc. AI reduces interpretation time by automating measurements and triaging normal studies, freeing experts for complex tasks. Emergency departments benefit first, where delays directly affect outcomes.

Government Incentives & Funding for AI Health Tech

The U.S. Department of Health and Human Services 2025 Strategic Plan prioritizes democratizing AI tools across underserved region. China, India, and South Korea have earmarked multi-year grants for ultrasound AI to bolster maternal and cardiac programs. Europe’s AI Act provides predictable approval pathways, encouraging cross-border commercialization [3]European Commission, “Proposal for a Regulation Laying Down Harmonised Rules on AI,” eur-lex.europa.eu. Grants often bundle staff training, smoothing implementation.

Rapid POCUS Adoption with Integrated AI

WONCA Europe endorses POCUS as a first-line diagnostic tool when augmented by AI guidance; clinicians report higher confidence and patient acceptability. Portable scanners save 21% versus legacy imaging workflows, and AI further trims operator training timelines. Portability unlocks home health, ambulance, and remote-clinic use cases, widening the AI in ultrasound imaging market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procurement & maintenance costs | -4.7% | Global, acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Mounting data-privacy and cybersecurity concerns | -3.2% | Global, stringent in EU & North America | Long term (≥ 4 years) |

| Clinician skepticism & training gaps | -2.8% | Global, pronounced in traditional healthcare systems | Medium term (2-4 years) |

| Regulatory ambiguity for AI-guided home ultrasound | -1.9% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procurement & Maintenance Costs

Budget constraints remain the top adoption barrier, particularly for independent clinics. Department heads cite funding gaps despite proven efficacy. Total cost of ownership spans cloud compute fees, license renewals, and staff training. Nonetheless, cross-modality platforms show 451% five-year ROI once scaled across CT, MRI, and ultrasound, and vendors now offer subscription or outcome-linked pricing to soften upfront hits.

Mounting Data-Privacy and Cybersecurity Concerns

FDA bulletins have flagged exploitable vulnerabilities in connected ultrasound gear. HIPAA compliance grows tougher when images transit multiple jurisdictions, demanding sophisticated governance. Privacy-preserving analytics—homomorphic encryption and federated learning—are emerging but add complexity. Procurement teams now mandate robust security audits before signing AI contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Software Dominance Drives Innovation

Software accounted for 54.67% of the AI in ultrasound imaging market share in 2025. Vendors focus on interoperable algorithms that sit on legacy probes, minimizing capital expenditure. The services line, growing at 33.18% CAGR, reflects rising demand for workflow integration, user training, and algorithm-performance optimization. Health systems seek proof that deployment improves throughput and revenue capture, shifting negotiations toward outcome-based contracts. Meanwhile, hardware makers embed on-device AI accelerators to reduce latency, yet buyers still gravitate to software-first stacks that remain brand-agnostic.

Over the forecast horizon, the AI in ultrasound imaging market will see layered platform ecosystems. Market leaders have opened software development kits that let third parties release specialty plug-ins. Butterfly Network’s Garden AI program exemplifies this move, encouraging cardiovascular, obstetric, and liver-disease modules on a single handheld chassis. Services revenue rises in parallel because each algorithm iteration requires continuous validation, reporting, and clinician retraining.

By Technology: Machine Learning Leads, Context-Aware Computing Surges

Machine-learning models held 42.74% revenue in 2025 thanks to proven gains in automated ejection-fraction measurement and nodule detection. Context-aware computing, projected to grow 33.05% CAGR, builds on this foundation by interpreting ambient data such as patient vitals and provider workflow, then tailoring real-time cues. Natural-language processing adds dictation and auto-reporting, reducing paperwork load, while advanced computer vision handles 3-D reconstructions in labor-intensive specialties.

Context-aware engines resonate strongly in emergency rooms where triage speed is critical. AI cues adapt to trauma protocols, highlighting free fluid in the abdomen during FAST exams. Such specificity pushes adoption deeper into critical-care pathways and expands the overall AI in ultrasound imaging market. Vendors combining multiple modalities—vision, NLP, and signal processing—create high switching costs, an essential moat as more entrants crowd the space.

By Device Type: Handheld Dominance, Wearable Innovation

Handheld probes contributed 35.22% revenue in 2025 as clinicians valued flexibility and lower price points. Enhanced with semiconductor-on-chip designs, new robes function for eight hours on a single charge, supporting rural rounds. Wearables, forecast to grow 33.29% CAGR, turn ultrasound into a continuous-monitoring modality. MIT researchers recently demonstrated a patch that performs automated breast exams, potentially shifting screening into the home.

Hospitals still rely on cart systems for high-resolution studies; however, hybrid laptop units are cannibalizing mid-range carts as departments standardize on multipurpose fleets. Vendors now position wearables as adjuncts rather than replacements, enabling nocturnal cardiac or renal monitoring without nursing intervention. As reimbursement structures adapt, continuous acquisition could redefine how the AI in ultrasound imaging market size is measured, shifting from capital sales to subscription analytics.

By Imaging Mode: 2-D Foundation, Volumetric Growth

2-D mode retained 36.58% share in 2025 because automation of diameter measurements and grayscale categorization yields immediate efficiency. The volumetric segment, with a 33.64% CAGR outlook, benefits from AI that aligns, reconstructs, and color-codes voxels in real time. Siemens Healthineers’ real-time 3-D shear-wave package has cut liver-fibrosis exam times by 48% during pilot programs.

Color-flow Doppler and elastography also accelerate, powered by AI that suppresses artefacts and quantifies stiffness more reliably than manual techniques. Contrast-enhanced ultrasound gains traction as algorithms predict optimum bolus timing, maximizing diagnostic yield without escalating dose. The AI in ultrasound imaging market thus shifts toward higher-complexity modes once thought niche, broadening the value proposition beyond routine scans.

By Application: Cardiology Leadership, Obstetrics Acceleration

Cardiology commanded 39.66% of the 2025 revenue base. Automated strain analysis and quantification of diastolic function underpin clear clinical utility in heart-failure management. Obstetrics and gynecology, set for 33.12% CAGR, relies on AI to flag structural anomalies and monitor growth curves. Samsung Medison’s newly integrated Sonio algorithms detect 165 fetal malformations and generate instant reports, trimming scan duration by 30%.

Gastroenterology sees momentum as AI improves liver steatosis scoring, while musculoskeletal practices adopt guided needle-placement tools. Oncology teams employ AI for tumor volumetry, feeding response data straight into treatment-planning systems. As subspecialty modules proliferate, the AI in ultrasound imaging market turns into a mosaic of micro-workflows, each contributing incremental volume and reinforcing platform stickiness.

By End User: Hospital Dominance, Ambulatory Expansion

Hospitals delivered 58.12% of revenue in 2025, leveraging enterprise PACS and analytics dashboards. Ambulatory clinics and urgent-care chains will post 33.48% CAGR because handheld AI probes let primary-care physicians rule out serious pathology on the spot. The University of Rochester Medical Center rolled out 862 devices across internal medicine, cardiology, and emergency services, boosting charge capture 116% in the first year.

Diagnostic imaging centers integrate AI to standardize reports across multi-site franchises, while home-care agencies pilot remote sonography with cloud-linked AI supervision. As aging populations prefer in-home services, payer policies continue to evolve, further enlarging the AI in ultrasound imaging market size for community-centric providers.

Geography Analysis

North America retained 47.62% share in 2025, bolstered by CMS reimbursement for AI echocardiography and a streamlined FDA approval framework. Leading health systems bundle AI ultrasound into cardiovascular centers of excellence, emphasizing outcome-based purchasing. Venture capital flows remain strong, but workforce shortages sustain the need for automation, thereby reinforcing future capital spending.

Asia-Pacific is the fastest-growing block with a 33.74% CAGR outlook. China’s Healthy China 2030 plan and India’s Ayushman Bharat initiative earmark funds for maternal-fetal diagnostics, while South Korea offers R&D tax credits for local AI developers. Cross-border partnerships, such as UltraSight’s alliance with SELVAS Healthcare to distribute cardiac AI throughout Southeast Asia, exemplify go-to-market tactics that marry international algorithms with local channel expertise.

Europe pursues measured expansion rooted in ethical governance. The AI Act’s risk-classification scheme compels vendors to document datasets and bias-mitigation efforts, but it also gives health systems confidence to procure at scale. Germany and the Nordic countries champion national ultrasound registries that feed back into AI model retraining, forming a virtuous cycle of quality assurance. Collectively, these trends consolidate the AI in ultrasound imaging market across advanced and emerging economies alike.

Competitive Landscape

The competitive field is moderately fragmented but tilting toward consolidation. Legacy vendors—GE HealthCare, Siemens Healthineers, Philips, and Samsung Medison—control distribution networks and are snapping up niche algorithm firms to close capability gaps. GE HealthCare’s USD 53 million buyout of Intelligent Ultrasound added real-time needle-tracking to its maternal-fetal line.

Pure-plays such as Butterfly Network and Exo employ semiconductor-on-chip designs that lower cost and move AI inference to the probe, enabling offline use. Exo’s purchase of Medo.ai deepened its musculoskeletal and abdominal libraries, while Butterfly’s USD 76 million financing round funds global expansion of its subscription model. In wearables, academic spin-offs partner with contract manufacturers to scale production, targeting oncology and nephrology tracking niches.

Competition increasingly centers on integration depth rather than isolated accuracy metrics. Health systems demand unified dashboards that feed billing codes directly into EHRs and prove quantifiable gains in throughput, diagnostic concordance, and patient outcomes. Vendors able to present longitudinal ROI evidence win multi-year enterprise contracts, tightening the moat around end-to-end ecosystems and propelling AI in ultrasound imaging market penetration.

Artificial Intelligence In Ultrasound Imaging Industry Leaders

Siemens Healthcare GmbH

Samsung

General Electric Company

DiA Imaging Analysis

Caption Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: RadNet acquired See-Mode Technologies to add AI thyroid-cancer screening to its portfolio, strengthening early-detection offerings.

- March 2025: GE HealthCare and NVIDIA formed a multi-year pact to co-develop autonomous imaging workflows for ultrasound and X-ray modalities, targeting productivity gains in acute settings.

- March 2025: Fujifilm partnered with Us2.ai to embed automated echocardiography analysis into its scanners, offering instant cardiac function reports to cardiologists.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the artificial-intelligence-in-ultrasound-imaging market as all hardware, embedded firmware, and cloud or on-premise software that autonomously assists image acquisition, interpretation, or workflow decisions for real-time B-mode, Doppler, and 3-D/4-D scans used across radiology, cardiology, obstetrics, critical care, and point-of-care settings.

Scope exclusion: Purely conventional ultrasound systems sold without any FDA or CE cleared AI feature sets are not counted.

Segmentation Overview

- By Solution

- Hardware

- Software

- Services

- By Technology

- Machine Learning

- Natural Language Processing

- Computer Vision

- Context-Aware Computing

- Other Technologies

- By Device Type

- Cart / Trolley-based

- Compact / Laptop

- Handheld / Probe-based

- Wearable & Patch Ultrasound

- By Imaging Mode

- 2-D

- Doppler & Color Flow

- 3-D / 4-D & Volumetric

- Elastography

- Contrast-Enhanced Ultrasound

- By Application

- Cardiology (Echocardiography)

- Obstetrics & Gynecology

- Gastroenterology / Hepatology

- Musculoskeletal & Sports Medicine

- Oncology

- Other Applications

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory & Physician Clinics

- Point-of-Care Settings (ICU, ED)

- Home-care Ecosystem

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview hospital imaging directors, emergency physicians, obstetric sonographers, device product managers, and AI algorithm start-ups across North America, Europe, and Asia-Pacific. These conversations test attach rate assumptions, typical selling prices, software renewal cycles, and regulatory gating, letting us plug critical gaps left by secondary information.

Desk Research

Mordor analysts first aggregate open data from tier-one sources such as the FDA 510(k) database, EMA device registrations, WHO Global Health Observatory, OECD Health Statistics, and national trade statistics that split ultrasound equipment and software exports. Industry insights are enriched with scientific papers indexed on PubMed, patent families from Questel, and company disclosures lodged on EDGAR and other investor portals.

Subscription repositories, such as Dow Jones Factiva for deal flow, D&B Hoovers for OEM financials, and Volza for shipment records, supply volume, price, and adoption clues that desk sources alone rarely align on. The sources named illustrate our approach; many additional datasets are tapped for corroboration and clarification.

Market-Sizing & Forecasting

A blended top-down and bottom-up loop underpins the model. We begin with national ultrasound unit install bases and annual shipment data, apply AI software attach rates validated through interviews, layer average license or firmware upgrade prices, and then reconcile outputs with sampled supplier roll-ups. Variables such as point-of-care ultrasound penetration, maternal health screening volumes, venture funding in imaging AI, device ASP erosion, regulatory approvals, and healthcare digitization indices feed a multivariate regression and ARIMA hybrid that projects demand to 2030. When bottom-up evidence is thin for an emerging region, weighted proxies (e.g., GDP-adjusted exam volumes) bridge the gap before final triangulation.

Data Validation & Update Cycle

Each draft undergoes senior analyst variance checks against historical patterns, competitor filings, and fresh news captured in Factiva. Material deviations trigger source re-checks or follow-up calls. Reports refresh yearly, with interim updates issued when major clearances, acquisitions, or reimbursement shifts occur. A last-mile review ensures clients receive the latest view.

Why Mordor's Artificial Intelligence In Ultrasound Imaging Baseline Commands Reliability

Published figures often diverge because firms pick different inclusion rules, discount rates, or device software bundling logic. Our disciplined scope, annual refresh, and dual-method modeling narrow those gaps and give decision-makers a traceable, middle-ground baseline.

Key gap drivers include: some publishers fold in AI-ready hardware still lacking deployed algorithms; others limit coverage to diagnostic uses and skip procedural guidance tools; price assumptions vary where perpetual licenses are converted to recurring revenue; update cadences differ, causing currency conversion swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.77 B (2025) | Mordor Intelligence | - |

| USD 2.35 B (2025) | Global Consultancy A | Counts AI-capable devices whether software is activated, inflating base value |

| USD 1.03 B (2024) | Industry Journal B | Restricts scope to radiology departments, excluding OB/GYN and emergency care uses |

| USD 1.15 B (2025) | Trade Digest C | Applies flat 8.6 % CAGR without modality-level drivers, understating high-growth segments |

In summary, Mordor's balanced mix of verified variables, frequent refreshes, and transparent logic provides a dependable starting point for investors, strategists, and product teams seeking clarity in this fast-evolving field.

Key Questions Answered in the Report

What is the current Artificial Intelligence In Ultrasound Imaging Market size?

The Artificial Intelligence In Ultrasound Imaging Market is projected to register a CAGR of 31.81% during the forecast period (2026-2031)

Who are the key players in Artificial Intelligence In Ultrasound Imaging Market?

Siemens Healthcare GmbH, Samsung, General Electric Company, DiA Imaging Analysis and Caption Health are the major companies operating in the Artificial Intelligence In Ultrasound Imaging Market.

Which is the fastest growing region in Artificial Intelligence In Ultrasound Imaging Market?

Asia-Pacific is the fastest-growing region, projected to expand at 33.74% CAGR through 2031.

Which region has the biggest share in Artificial Intelligence In Ultrasound Imaging Market?

In 2025, the North America accounts for the largest market share in Artificial Intelligence In Ultrasound Imaging Market.

Which solution type leads the AI in ultrasound imaging market?

Software solutions lead, holding 54.67% of AI in ultrasound imaging market share in 2025.

Page last updated on: