Ultrasonic Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

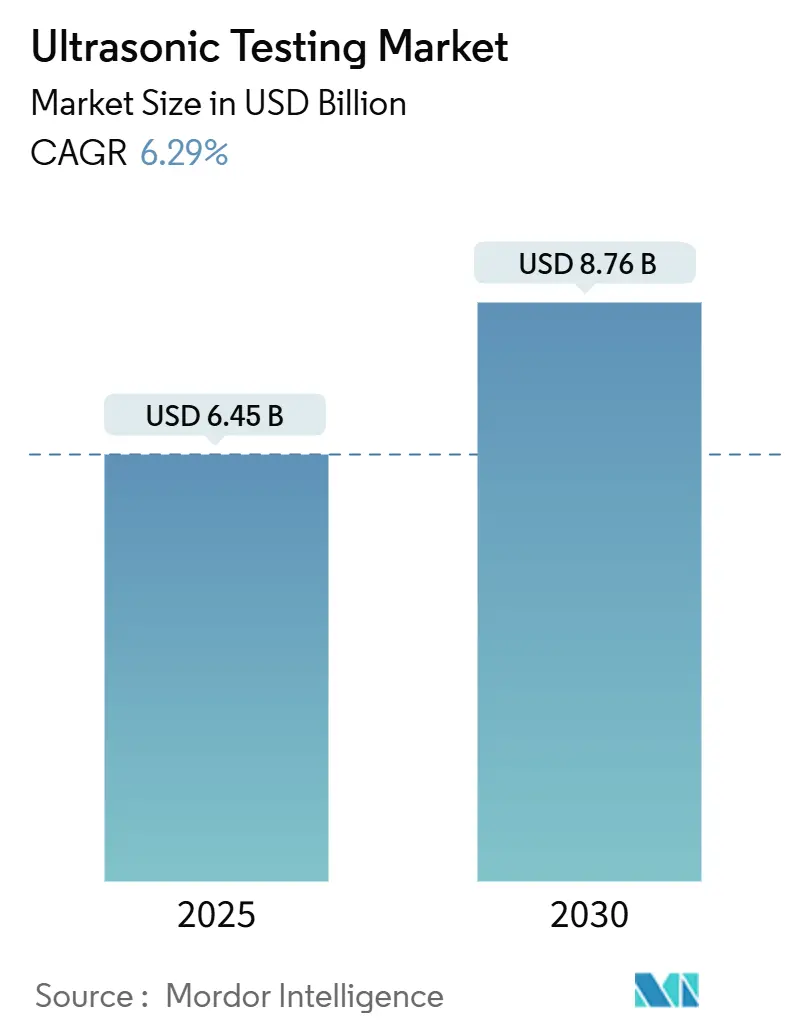

| Market Size (2025) | USD 6.45 Billion |

| Market Size (2030) | USD 8.76 Billion |

| Growth Rate (2025 - 2030) | 6.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

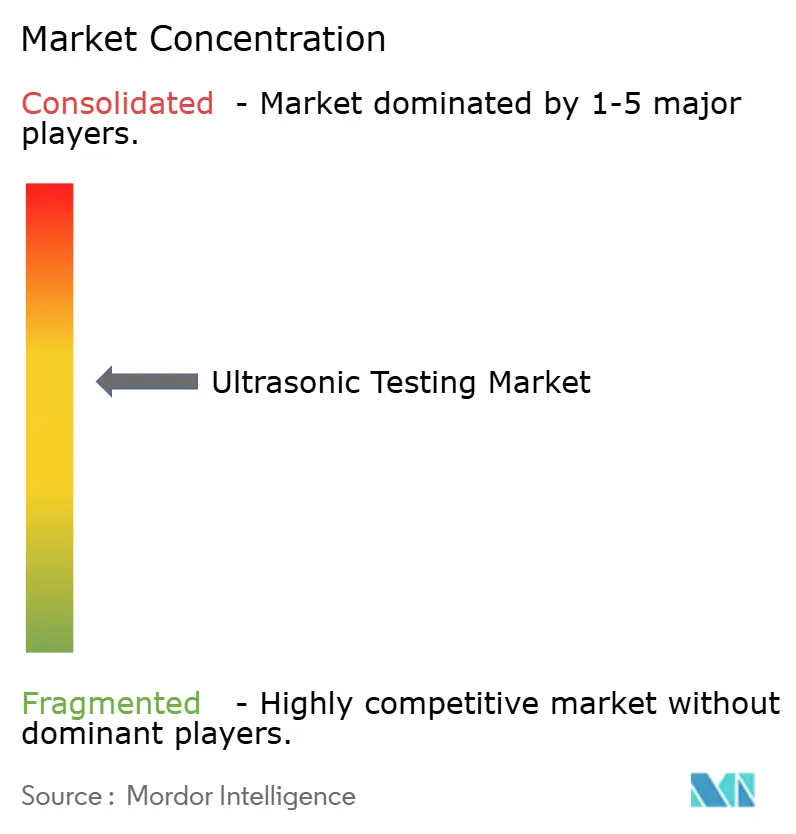

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasonic Testing Market Analysis by Mordor Intelligence

The ultrasonic testing market size reached USD 6.45 billion in 2025 and is forecast to advance to USD 8.76 billion by 2030, at a 6.29% CAGR, underscoring the method’s indispensable role in safeguarding critical assets across the energy, transportation, and advanced manufacturing sectors. Regulatory mandates that tighten inspection intervals, the rapid shift toward automated scanners, and the infusion of artificial intelligence for immediate defect recognition are converging to keep demand on a steady upswing. The Asia-Pacific region holds the lead position, thanks to large-scale infrastructure projects and the expanding production of aerospace structures, electric vehicles (EVs), and semiconductor devices. North America and Europe, while mature, continue to generate stable revenue because pipeline integrity rules and power-generation life-extension programs obligate owners to conduct recurring ultrasonic surveys.[1]Pipeline and Hazardous Materials Safety Administration, “Enhanced Pipeline Integrity Management Requirements,” phmsa.dot.gov As customers migrate from conventional single-element probes to phased-array and immersion systems, suppliers able to pair hardware with robust analytics suites are expected to capture incremental share. Near-term headwinds such as certified-technician shortages and procurement delays for high-end instruments are accelerating interest in turnkey robotic solutions and software-centric service models that minimize operator dependency.

Key Report Takeaways

- By portability, portable and handheld instruments accounted for a 46.7% share of the ultrasonic testing market in 2024, whereas automated and robotic systems are projected to expand at a 7.1% CAGR through 2030.

- By end-user, the oil and gas segment held 27.1% of the ultrasonic testing market share in 2024, while the automotive and transportation sectors are on track to deliver the fastest growth, at an 8.8% CAGR, through 2030.

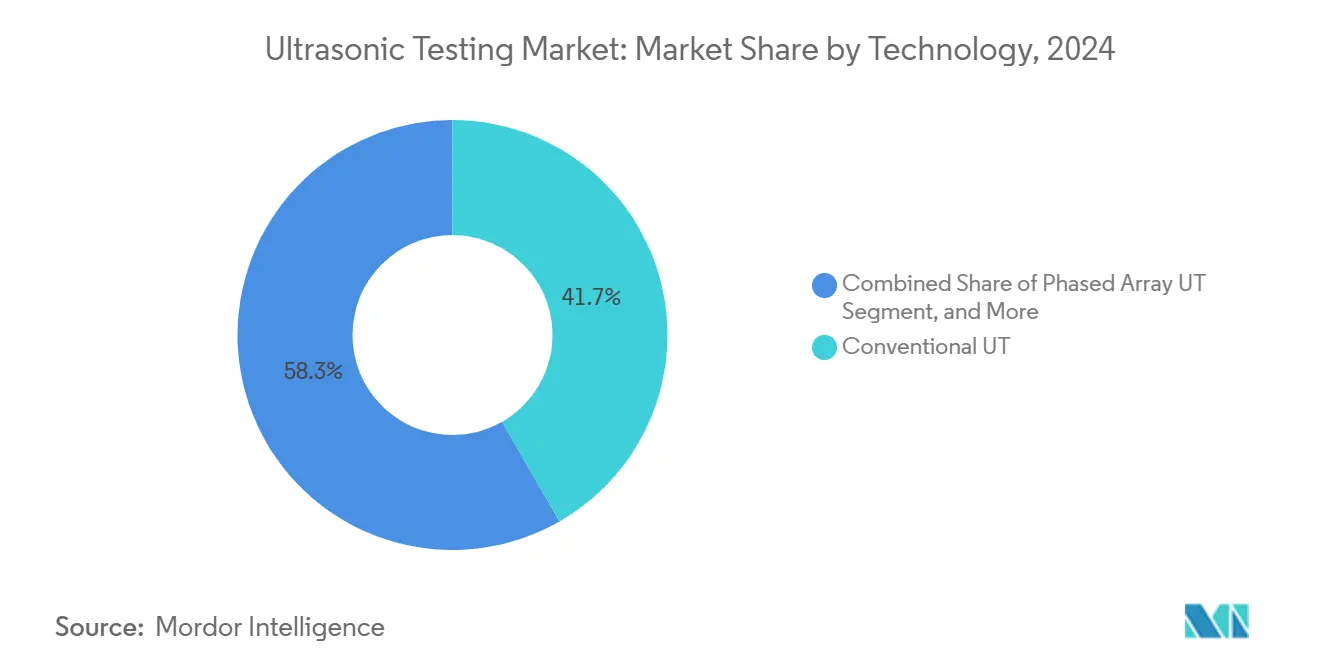

- By technology, conventional probes retained 41.7% of the ultrasonic testing market size in 2024; however, immersion ultrasonic testing is forecasted to grow at a 7.8% CAGR through 2030.

- By geography, the Asia-Pacific region led the ultrasonic testing market with 34.91% of revenue in 2024 and is projected to advance at a 7.5% CAGR through 2030.

Global Ultrasonic Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of phased array UT in aerospace composites | +1.2% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Stricter pipeline safety regulations driving inspection frequency in oil and gas | +0.8% | Global, with emphasis on North America and Middle East | Short term (≤ 2 years) |

| Expansion of automated UT in additive manufacturing quality control | +1.1% | North America and Europe, early adoption in Asia-Pacific | Medium term (2-4 years) |

| Rise of renewable energy installations requiring weld integrity testing in wind towers | +0.9% | Global, concentrated in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Increasing use of inline UT for EV battery manufacturing | +0.7% | Asia-Pacific core, expanding to North America and Europe | Medium term (2-4 years) |

| Integration of AI-driven defect recognition improving inspection throughput | +0.6% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Phased-Array UT in Aerospace Composites

Aircraft OEMs have transitioned from single-element probes to phased-array scanners, which generate real-time C-scan images of carbon-fiber parts, thereby significantly reducing rework costs while enhancing the probability of fault detection. The technology enables inspectors to resolve delaminations and fiber waviness down to the sub-millimeter scale, thereby satisfying safety-of-flight requirements for fuselage barrels and wing skins. More than 75 aircraft programs now specify phased-array ultrasonic testing as the default composite inspection method, and total focusing algorithms are further enhancing resolution for thick-section structures. Training cycles are shorter because software automatically steers beam-forming patterns, enabling operators certified at Level II to run complex inspections that were previously reserved for Level III personnel. With electric air taxi platforms adopting all-composite airframes, global demand for phased-array flaw detectors is expected to intensify throughout the decade.

Stricter Pipeline Safety Regulations Driving Inspection Frequency in Oil and Gas

The Pipeline and Hazardous Materials Safety Administration (PHMSA) mandated in 2024 that high-consequence areas receive ultrasonic inspection every seven years rather than every ten, spurring a rise in contract awards for guided-wave and electromagnetic acoustic transducer crawlers. API RP 1160, 3rd Edition, published in January 2025, reinforced these rules with performance-validation benchmarks that prioritize higher-resolution tools.[2]American Petroleum Institute, “API RP 1160 3rd Edition,” api.org Midstream operators are fast-tracking the procurement of multi-sensor inspection vehicles that can size stress-corrosion cracks in one pass, reducing field time by 30% compared to legacy pigs. Regional service providers are partnering with equipment OEMs to offer a single subscription that bundles inspection, analytics, and regulatory reporting services. Although the capital layout is substantial, fines for non-compliance and spill remediation far exceed equipment amortization, accelerating the regulatory pull-through effect.

Expansion of Automated UT in Additive Manufacturing Quality Control

Additive-manufacturing lines are embedding miniature ultrasonic transducers within recoater assemblies to spot pores and lack-of-fusion defects as small as 50 µm during the laser-melt process. By flagging anomalies layer by layer, operators can correct energy input on the fly and avoid post-build scrap, thereby trimming the total inspection cycle time by 60%. Siemens Energy validated the approach on gas-turbine blades, where every failed part previously cost upwards of USD 15,000 in wasted material and machining. Software dashboards convert high-volume acoustic data into simple traffic-light quality indicators, meaning fewer Level III inspectors must be physically present on the shop floor. The result is a measurable productivity uptick for powder-bed-fusion adopters now scaling to serial production.

Rise of Renewable-Energy Installations Requiring Weld-Integrity Testing in Wind Towers

IEC 61400-6 mandates 100% volumetric examination of wind-tower circumferential and longitudinal welds, prompting turbine OEMs to transition from X-ray film to phased-array ultrasonics for faster and safer compliance. Vestas reduced defect-escape rates by 75% and increased inspection throughput by 45% after migrating to automated crawler systems specifically designed for 80-meter tower sections. Given that installed wind capacity must triple by 2030 under European Green Deal targets, the volume of weld-integrity testing is set to increase, especially for offshore foundations, where structural failures carry outsized costs. The marriage of total-focusing algorithms and automatic probe-angle compensation now allows technicians to detect planar flaws parallel to fusion lines that X-ray often misses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced UT equipment | -0.9% | Global, particularly impacting emerging economies | Short term (≤ 2 years) |

| Shortage of certified UT technicians | -0.7% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Limited penetration in emerging economies due to low awareness | -0.5% | Africa, South America, parts of Asia-Pacific | Long term (≥ 4 years) |

| Data interoperability challenges with legacy inspection data | -0.4% | Global, concentrated in mature industrial regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced UT Equipment

Fully featured phased-array or time-of-flight diffraction rigs cost USD 150,000 to USD 500,000 per unit, a price that prompts many mid-sized fabricators to defer purchases in favor of cheaper but less sensitive penetrant or magnetic-particle techniques.[3]American Society for Nondestructive Testing, “UT Equipment Costs and Workforce Trends,” asnt.org Instrument costs alone account for as much as 45% of a typical inspection program budget once probes, wedges, and calibration blocks are included. Leasing models are starting to emerge; however, concerns about software update fees and replacement parts limit their adoption. Vendors able to offer subscription bundles with guaranteed trade-in values may remove the sting, but for now, capital budgets remain the primary gating factor in regions with less mature nondestructive-testing (NDT) ecosystems.

Shortage of Certified UT Technicians

An estimated 20% gap exists between open job requisitions and available Level II and Level III personnel in North America and Europe. Certification normally takes six to 24 months and costs USD 8,000-15,000 per candidate, discouraging small service firms from building internal benches. Moreover, emerging modalities such as guided-wave and total-focusing method examinations demand additional classroom and field hours. Recruiters report salary premiums of 18-22% for technicians proficient in phased-array data analysis. Automation and AI offer partial relief, yet site access rules still require a human ticket holder to sign off on final reports.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Portability: Automation Redefines Field and Factory Inspection

Portable and handheld devices retained a 46.7% revenue share in 2024, reflecting their role in in-situ weld surveys, remaining-life gauging, and corrosion mapping on pipelines and pressure vessels. Despite that dominance, uptake of robotic and automated scanners is forecast at a 7.1% CAGR as maintenance departments strive for consistent coupling pressure and scan overlaps that human operators struggle to replicate. Automated cells integrated into automotive stamping lines already run 24/7, feeding results to manufacturing-execution systems for closed-loop control. The ultrasonic testing market size for automated solutions is projected to exceed USD 2.4 billion by 2030, driven by these productivity gains. Evident’s OmniScan X4, released in April 2024, typifies next-generation portables that merge AI classifiers with rugged tablets, enabling less-skilled users to generate code-compliant reports in minutes.

The adoption of six-axis robot arms further enhances scan repeatability while reducing repetitive-strain injuries among technicians. In aerospace overhaul, collaborative robots now guide phased-array probes over complex nacelle contours, increasing coverage to 98% of the design surface area. As instrument makers standardize EtherCAT and Profinet interfaces, automated cells can be dropped into existing production lines with minimal rewiring.

By End-User Industry: Electrification Accelerates Automotive Uptake

The oil and gas segment accounted for 27.1% of 2024 revenue, but EV supply-chain expansion positions automotive and transportation as the fastest-growing segment at an 8.8% CAGR through 2030. Inline transducers verify electrode coating, separator placement, and cell stack alignment, safeguarding battery performance and safety. The ultrasonic testing market share for automotive applications is expected to move from 9.5% in 2024 to 13% by 2030 as pack volumes climb. Aerospace and defense maintain stable demand, thanks to the proliferation of composite airframes and life-extension programs for legacy fighters. Power-generation steam-pipe inspections remain mandatory, but the decarbonization pivot toward wind and hydrogen is redistributing spend toward renewable-project supply chains.

Heavy engineering firms integrate fully automated immersion tanks to inspect forged shafts and pressure vessel heads, allowing subsurface laminations to be detected before final machining. Chemical and petrochemical owners deploy permanently installed thickness-monitoring arrays on high-temperature reformer tubes, generating real-time corrosion rates without shutdown.

By Technology: Immersion Systems Achieve New Micron-Level Benchmarks

Conventional straight-beam probes still account for 41.7% of 2024 revenue, largely because they are sufficient for simple thickness checks. Yet immersion ultrasonic testing is growing at a 7.8% CAGR as semiconductor and electronics companies demand micron-level flaw resolution in silicon and advanced-substrate wafers. In high-frequency immersion baths, megahertz-class transducers coupled with synthetic-aperture focusing deliver lateral resolution approaching that of optical microscopy, uncovering defects invisible to eddy-current or X-ray imaging. The ultrasonic testing market size for immersion setups is forecast to touch USD 1.1 billion by 2030. Phased-array systems continue to penetrate the infrastructure and defense sectors, prized for their beam-steering flexibility and rapid area coverage. Time-of-flight diffraction (TOFD) holds a niche status for through-wall crack sizing in pressure vessels and girth welds but remains a valued cross-check for critical joints.

Total-focusing-method (TFM) algorithms are steadily gaining traction in mainstream phased-array platforms, sharpening volumetric images and reducing false positives. The convergence of immersion and phased-array modalities is anticipated as robotic arms dip multi-element probes into water columns for high-speed, automatic scanning of aero-engine disks and hypersonic-vehicle heat shields.

Geography Analysis

Asia-Pacific commanded 34.91% of global sales in 2024 and is expanding at a 7.5% CAGR, buoyed by Belt and Road pipeline builds, high-speed-rail construction, and leading-edge semiconductor fabs in China, Taiwan, South Korea, and Japan. China alone contributes roughly 40% of regional demand as state-owned EPCs specify phased-array inspections on massive LNG and hydrogen pipeline strings. India’s renewable push is spurring ultrasonic survey work on 2.5 GW of new wind-tower capacity, while Japanese automakers are installing inline inspection cells to validate battery modules destined for export EVs. Although technician shortages persist, government-funded workforce-development programs are expected to narrow the skills gap by 2028.

North America retains a mature yet robust base, anchored by PHMSA’s stricter seven-year inspection cycle and the aerospace sector’s ongoing transition to composite airframes. The United States provides fertile ground for AI-driven data analytics pilots, which are frequently funded through grants from the Department of Energy and NASA. Canada’s oil-sands pipelines and Mexico’s accelerating EV manufacturing add geographic diversification. Service providers note steady bookings for guided-wave crawlers that pinpoint corrosion under insulation on chemical plants along the Gulf Coast.

Europe ranks third in volume but leads in regulatory stringency. The European Commission’s Green Deal frameworks require comprehensive inspection documentation for offshore wind jackets, hydrogen pipelines, and EV gigafactories. Germany’s industrial Mittelstand purchases advanced immersion baths for turbine-blade root inspections, while the United Kingdom’s aerospace MRO hubs continue to adopt automated scanners to curb maintenance turn-time. In Southern Europe, nuclear steam generator inspections present stable revenue streams that offset softer shipbuilding demand. Emerging economies in Africa and South America are forecast to add incremental volume once awareness and financing barriers ease, especially where oil-and-gas infrastructure and mining facilities mature.

Competitive Landscape

The ultrasonic testing market exhibits moderate concentration, with the top five suppliers controlling approximately 55% of the global revenue. Evident Corporation, Waygate Technologies, and Sonatest lead the way in hardware innovation, each launching AI-enabled flaw detectors that significantly reduce interpretation times. Eddyfi Technologies’ 2024 purchase of Zetec illustrates the ongoing consolidation of electromagnetic and ultrasonic modalities under one roof, creating one-stop platforms for complex asset-integrity programs.[4]Eddyfi Technologies, “Zetec Acquisition Announcement,” eddyfi.com

Competition is intensifying around software ecosystems that ingest multi-modal NDT data. Waygate’s InspectionWorks and Evident’s Olympus Scientific Cloud now offer API hooks that enable asset-integrity teams to pipe ultrasonic readings into enterprise historians, facilitating predictive analytics. Licensing revenue from these platforms is outpacing hardware margins for early movers. Vendors positioning collaborative robots with plug-and-play ultrasonic end-effectors are winning contracts at EV battery plants where 24/7 line speed dictates zero downtime.

Regional service companies are differentiating through technician-training academies and digital report templates that accelerate regulatory submissions. Meanwhile, open-architecture startups are entering with cloud-native defect-classification engines, often white-labeling hardware sourced from OEM partners. The battle for share is expected to pivot further toward analytics and lifecycle software rather than probe-count arms races.

Ultrasonic Testing Industry Leaders

Evident Corporation

Waygate Technologies (Baker Hughes Business)

Sonatest Ltd.

Mistras Group Inc.

Zetec Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: XARION Laser Acoustics demonstrated its contact-free, laser-based ultrasonic testing system at the ASNT Annual Conference in Orlando, showcasing how the technology addresses inspection challenges on hot or fragile parts that cannot accommodate conventional probes.

- July 2025: Wabtec Corporation closed a USD 1.78 billion purchase of Evident Corporation’s Inspection Technologies Division, uniting Wabtec’s rail and industrial experience with Evident’s ultrasonic expertise to form one of the sector’s most extensive NDT equipment portfolios.

- July 2025: XARION Laser Acoustics outlined a U.S. expansion plan that will bring its patented optical-ultrasound tools closer to North American aerospace, semiconductor, and advanced-manufacturing customers who need non-contact inspection.

- June 2025: Verasonics has upgraded its Vantage NXT Research Ultrasound Platform with machine-learning defect classifiers and enhanced high-frequency signal processing, providing research labs and advanced manufacturers with a more flexible NDT solution.

Global Ultrasonic Testing Market Report Scope

The ultrasonic testing market typically comprises system integrators and security monitoring service providers who use these types of equipment to measure the hardness, flaws, and sometimes stress on the object. The study incorporates these in the scope of the market. These instruments provide mission-critical information to avoid failure due to fatigue or construction flaws in the structure.

The ultrasonic testing market is segmented by geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, Spain, rest of Europe], Asia Pacific [China, Japan, India, South Korea, rest of Asia-Pacific], Latin America [Brazil, Argentina, rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Portable / Handheld |

| Stationary / Benchtop |

| Automated / Robotic |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and Semiconductor |

| Mining |

| Medical Devices |

| Other End-user Industries |

| Conventional UT |

| Phased Array UT |

| Time-of-Flight Diffraction (TOFD) |

| Immersion UT |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Portability | Portable / Handheld | |

| Stationary / Benchtop | ||

| Automated / Robotic | ||

| By End-user Industry | Oil and Gas | |

| Power Generation | ||

| Aerospace | ||

| Defense | ||

| Automotive and Transportation | ||

| Manufacturing and Heavy Engineering | ||

| Construction and Infrastructure | ||

| Chemical and Petrochemical | ||

| Marine and Ship Building | ||

| Electronics and Semiconductor | ||

| Mining | ||

| Medical Devices | ||

| Other End-user Industries | ||

| By Technology | Conventional UT | |

| Phased Array UT | ||

| Time-of-Flight Diffraction (TOFD) | ||

| Immersion UT | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the ultrasonic testing market be by 2030?

It is projected to reach USD 8.76 billion, expanding at a 6.29% CAGR from 2025.

Which segment is growing fastest within ultrasonic testing?

Automated and robotic systems show the highest growth, moving at a 7.1% CAGR through 2030.

Why is Asia-Pacific the leading region?

Large infrastructure projects, strong manufacturing bases and government quality mandates give Asia-Pacific a 34.91% revenue share with 7.5% CAGR growth.

What is driving UT adoption in electric-vehicle production?

Inline ultrasonic gauges verify battery electrode uniformity and separator integrity, preventing defects that could lead to thermal events.

How are AI capabilities changing ultrasonic inspections?

Machine-learning classifiers embedded in modern flaw detectors reduce interpretation time by half and raise defect-hit rates to about 96%.

What challenges could slow market growth?

High upfront equipment costs and a global shortage of certified technicians remain the two most significant brakes on wider adoption.

Page last updated on: