Ultrafiltration Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 61.59 Billion |

| Market Size (2031) | USD 95.09 Billion |

| Growth Rate (2026 - 2031) | 9.07% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

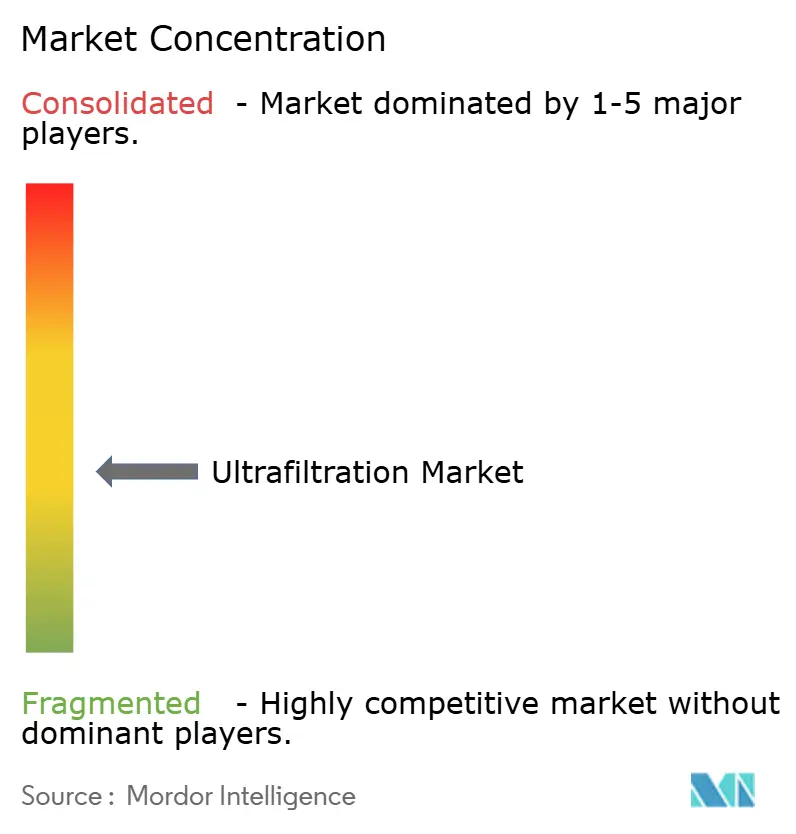

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrafiltration Market Analysis by Mordor Intelligence

The Ultrafiltration Market size is expected to grow from USD 56.63 billion in 2025 to USD 61.59 billion in 2026 and is forecast to reach USD 95.09 billion by 2031 at 9.07% CAGR over 2026-2031. A structural pivot toward membrane pretreatment in seawater desalination, rising adoption of decentralized smart-city water skids, and tightening microplastics and per- and polyfluoroalkyl substances (PFAS) regulations together underpin this expansion. Asia-Pacific remains the revenue anchor as Chinese and Singaporean utilities retrofit legacy plants, while the Middle-East and Africa post the fastest gains on the back of Saudi and Bahraini desalination pipelines. Product innovation continues to tilt toward ceramic and spiral-wound geometries that promise longer life and easier cleaning, and digital twins that trigger chemical-enhanced backwash only when fouling models dictate, lowering operating costs. Simultaneously, pharmaceutical buyers accelerate single-use tangential-flow filtration adoption to support messenger ribonucleic acid (RNA) and viral-vector capacity, adding a new layer of demand resilience.

Key Report Takeaways

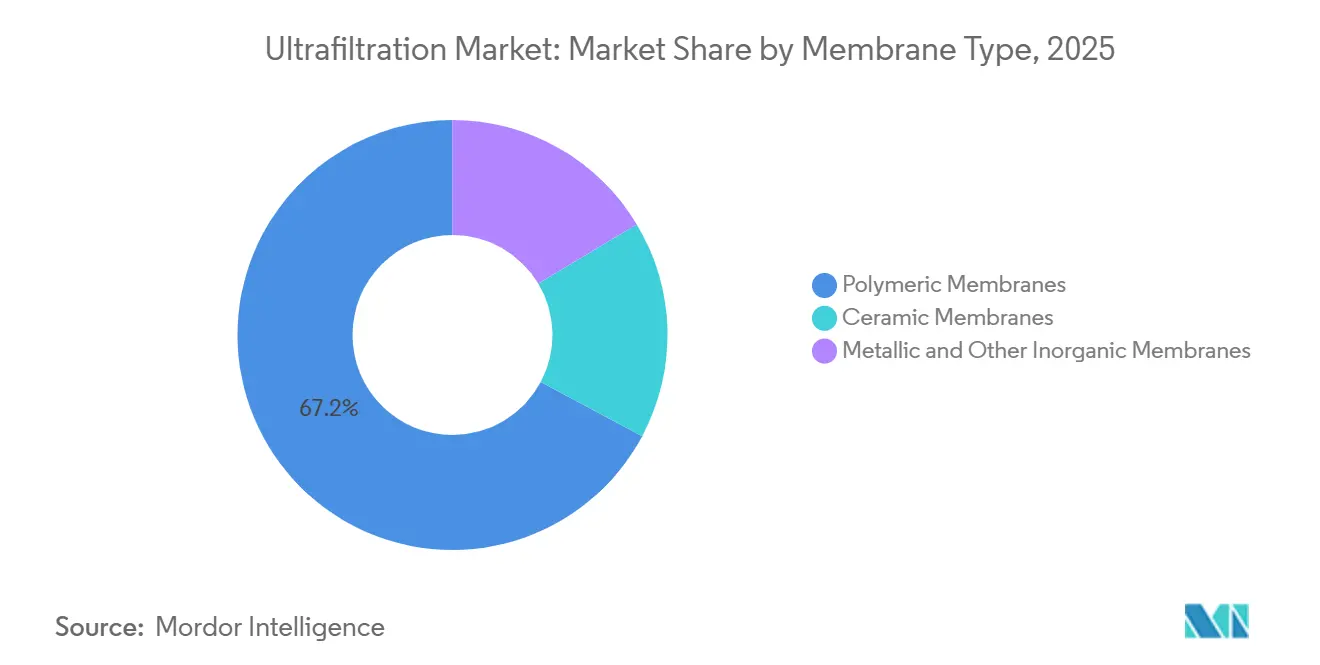

- By membrane type, polymeric variants led with 67.20% of the ultrafiltration market share in 2025, while ceramic membranes are projected to expand at a 10.56% CAGR from 2026 to 2031.

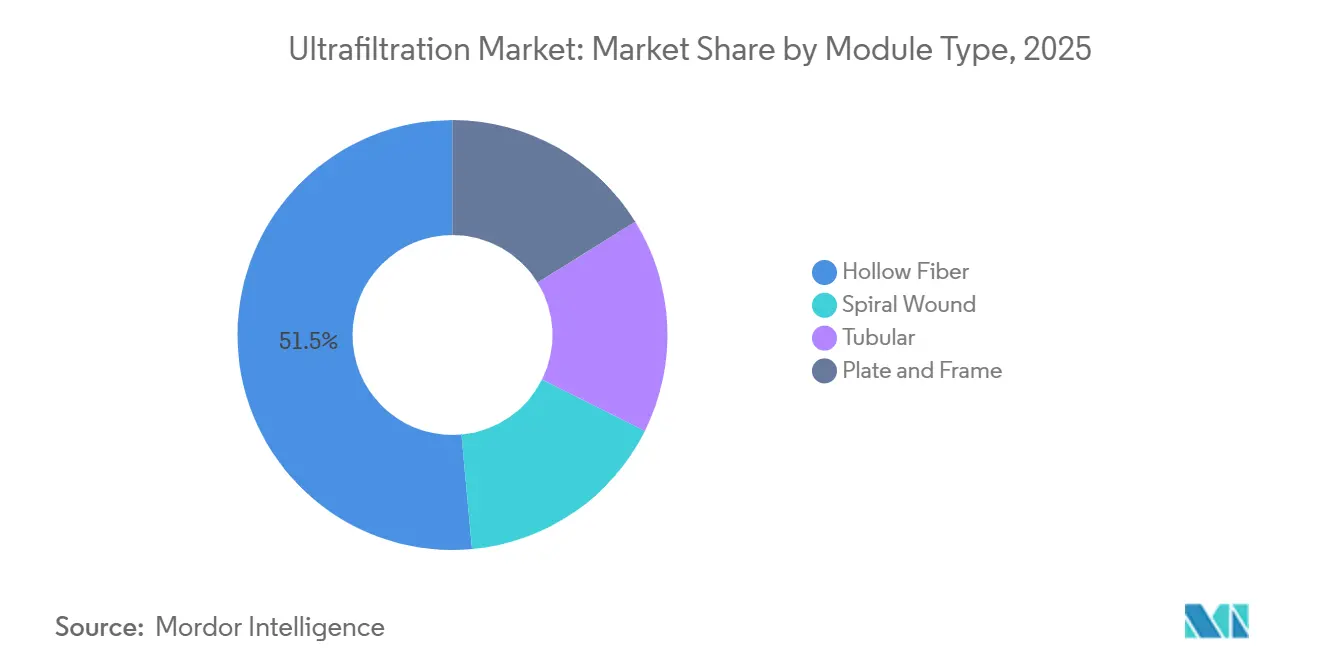

- By module type, hollow fiber captured 51.45% of the ultrafiltration market size in 2025, whereas tubular configurations are expected to advance at a 10.24% CAGR from 2026 to 2031.

- By application, water and wastewater treatment held 49.14% revenue in 2025, yet pharmaceuticals and biotechnology are expected to record the fastest 10.67% CAGR from 2026 to 2031.

- By end-user industry, municipal utilities accounted for 54.23% of demand in 2025, while healthcare buyers are expected to post a 10.61% CAGR from 2026 to 2031.

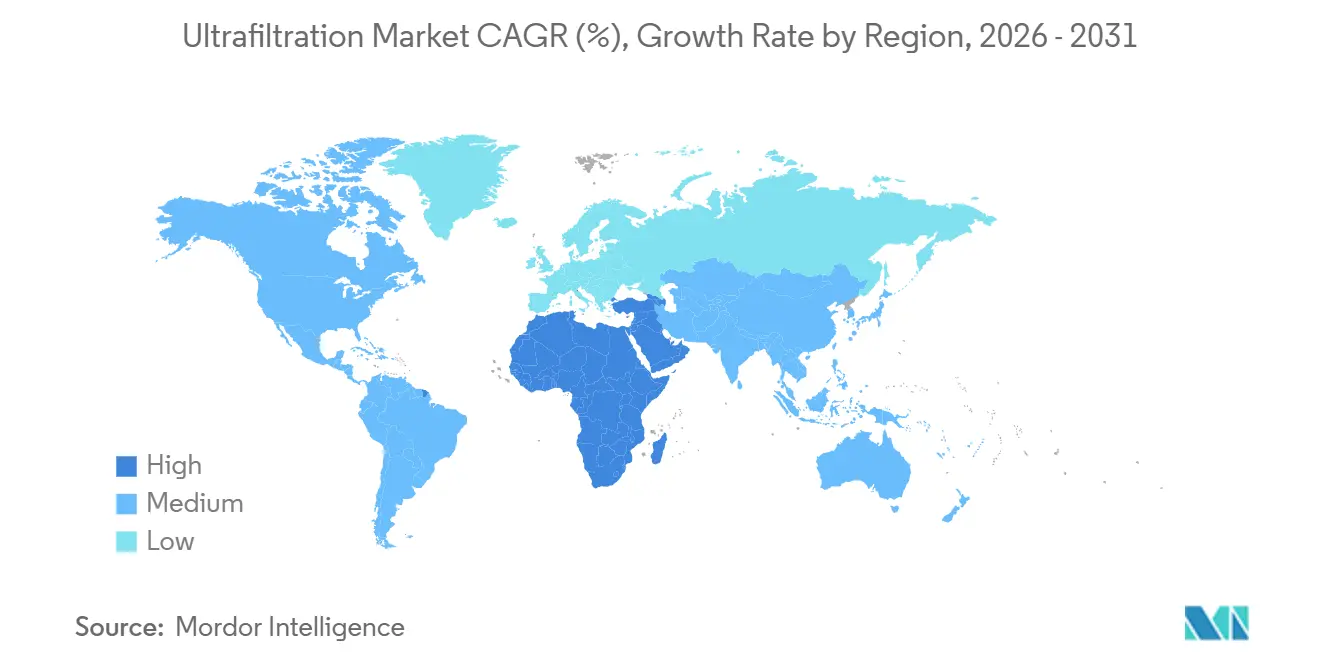

- By geography, Asia-Pacific commanded 38.31% of revenue in 2025, and the Middle-East and Africa region is forecast to grow at 10.74% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ultrafiltration Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for water and wastewater treatment | +2.10% | Global, concentrated in APAC and MEA | Long term (≥ 4 years) |

| Integration of ultrafiltration as pretreatment for reverse osmosis and desalination | +1.80% | MEA core, spillover to North America and APAC coastal regions | Medium term (2-4 years) |

| Rising adoption in food and beverage product-recovery loops | +1.30% | Europe, North America, and APAC | Medium term (2-4 years) |

| Decentralized ultrafiltration skids for smart-city and remote installations | +1.00% | Global, early gains in Singapore, the Netherlands, Scandinavia | Short term (≤ 2 years) |

| Regulatory push for microplastics removal in drinking water | +1.50% | Europe, North America, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Water and Wastewater Treatment

Utilities, facing challenges of water scarcity, are moving away from traditional sand filtration methods, opting instead for advanced membrane clarification. This transition not only enables them to adhere to strict turbidity standards but also sidesteps the significant expenses tied to reservoirs. In China, the Yiwu Third Water Plant is at the forefront, utilizing ceramic modules for extensive water processing. Their research indicates that, even accounting for fouling downtimes, ceramic systems are economically comparable to polymeric systems. Meanwhile, in Qingdao Dongjiakou, another facility is combining ultrafiltration with reverse osmosis, resulting in reduced maintenance needs and improved operational cost efficiency. The Middle-East is also advancing, with plans to expand desalination capacities in the coming years. Interestingly, a large portion of these tenders is leaning toward ultrafiltration pretreatment. This trend of ultrafiltration isn't confined to desalination; it's gaining traction in industrial reuse too. For example, Veolia's Vitória station in Brazil is supplying process water to major steel manufacturers. This achievement not only emphasizes the station's operational efficiency but also signifies a marked decrease in freshwater consumption for a region already grappling with drought challenges.

Integration of Ultrafiltration as Pretreatment for Reverse Osmosis and Desalination

Seawater plants now standardize dual-membrane trains, as reverse-osmosis warranties mandate ultrafiltration feedwater. Toray's 2025 high-removal hollow fiber cuts downstream fouling by a third and reduces carbon output from chemical cleaning by 30%. DuPont's 2026 ultra-high-pressure element, aiming for minimal liquid discharge, depends on ultrafiltration to avert irreversible compaction. Bahrain's USD 2 billion expansions at Sitra and Hidd set turbidity limits under 0.1 nephelometric turbidity units and a silt density index below 3.0, ensuring ultrafiltration is in place before major operations commence[1]Source: DigitalRefining, “Alfa Laval Wins Significant Order for Advanced Filtration Plant,” digitalrefining.com. Energy modeling reveals that implementing 0.5-2 bar ultrafiltration boosts reverse-osmosis flux by 10%-15%. This enhancement can prolong the lifespan of the elements by as much as two years, leading to a favorable net-present-value payback. As a testament to its efficacy, industry associations have incorporated these designs into their best-practice manuals, paving the way for a swift global adoption.

Rising Adoption in Food and Beverage Product-Recovery Loops

Producers in the dairy, brewing, and fermentation sectors are retrofitting ultrafiltration modules, transforming side-streams into marketable proteins, enzymes, and flavors. Alfa Laval secured a significant deal from the European Union for multiple containerized skids at an Asian amino-acid facility, achieving high purity in organic concentration. MANN+HUMMEL’s spiral membrane improves permeate flows in whey applications while ensuring protein retention. A pilot project by FrieslandCampina and VITO demonstrated ceramics' resilience in dairy cleaning cycles, achieving notable lactose retention and salt removal. Wafilin Systems plans to unveil its largest whey plant in the Netherlands in 2026, transitioning from centrifuges to continuous membrane fractionation. Furthermore, regulatory moves, such as Europe’s nutrient-recovery mandate, strengthen the economic feasibility of product-recovery processes.

Decentralized Ultrafiltration Skids for Smart-City and Remote Installations

In peri-urban areas, large conventional plants are being replaced by plug-and-play skids equipped with Long Range Wide Area Network (LoRaWAN) sensors and fouling algorithms. The smart-water grid segment is expected to experience significant growth by 2030, with ultrafiltration systems driving this expansion at a notable annual growth rate. Singapore’s NEWater lines, through predictive cleaning, activate only when flux declines to a certain level, resulting in considerable energy savings. Veolia’s trailer-mounted Mobile Ultrafiltration Unit Four by Eighty-Five Ton (MOUF 4×85T) can enhance potable capacity significantly, achieving this within a short timeframe after arriving on-site. Internet-of-Things optimization has led to a substantial reduction in chemical usage by aligning upstream coagulation with downstream disinfection. In smaller cities, a containerized system with a moderate daily capacity can be financed and installed within a relatively short period, avoiding the lengthy multiyear bond cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Membrane fouling and cleaning costs | -1.8% | Global, particularly acute in industrial applications across APAC (high-turbidity feedwater in China, India), Middle East and Africa (high-salinity environments), and aging municipal infrastructure in North America and Europe | Long term (≥4 years) |

| Competition from MBR and next-gen low-pressure membranes | -1.3% | Europe (municipal wastewater preference for MBR in Germany, UK), North America (integrated MBR systems), and emerging APAC markets (China, Japan) where hybrid systems gain traction | Medium term (2-4 years) |

| End-of-life polymer-membrane disposal uncertainty | -0.9% | Europe (stringent waste regulations under EU Circular Economy Action Plan), North America (landfill restrictions), with growing concern in APAC as regulatory frameworks mature | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Membrane Fouling and Cleaning Costs

Surface-water plants grappling with high turbidity and elevated dissolved organics face a significant financial drain due to fouling. Regular treatments using bleach, acid, and surface-active agents oxidize polymeric fibers, consequently shortening their effective lifespan[2]Source: VITO, “FrieslandCampina and VITO Pioneer Sustainable Dairy Processing,” vito.be . While ceramic modules can withstand rigorous cleaning, their elevated price confines them to upscale markets. Pall's Gradient Permeability Integrated Cartridge design, boasting graduated permeability, has notably cut down cleaning frequency in dairy trials, yet it is just now entering wider markets. Research on graphene-oxide coatings indicates potential in curbing flux decline in laboratory feeds; however, the absence of timely pilot data hampers field adoption. In the Middle East, operators are experimenting with ultraviolet pre-oxidation and dissolved-air flotation to lessen organic loads, though this comes with increased capital complexity.

Competition From Membrane Bioreactor and Next-Generation Low-Pressure Membranes

Membrane bioreactors combine biological and filtration processes, eliminating the need for secondary clarifiers and significantly reducing the required footprint. This efficiency is especially appealing to utilities with limited land availability. Moreover, with artificial intelligence integrated into their operations, these bioreactors can optimize energy consumption for aeration and prolong membrane lifespan. This technological leap brings their costs in line with standalone ultrafiltration systems. Membranes designed for loose nanofiltration and recycled ultrafiltration, sourced from oxidized reverse-osmosis elements, operate efficiently at low pressures. Yet, they achieve molecular-weight cutoffs comparable to traditional ultrafiltration, making them attractive to budget-conscious buyers. Europe and North America boast a significant number of membrane bioreactor plants, each potentially replacing a sale of ultrafiltration systems. Nonetheless, ultrafiltration remains dominant in decentralized areas or regions with limited power, where simpler hydraulics are preferred over more complex intensified processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Membrane Type: Ceramic Variants Gain Traction Despite Premium Pricing

In 2025, polymeric membranes secured 67.20% of the revenue, capitalizing on their cost advantages. However, ceramic alternatives are set to outpace the competition, boasting a projected CAGR of 10.56% in the ultrafiltration market from 2026 to 2031. Hollow fiber polymeric units are strategically priced to align with standard municipal budget depreciation schedules. On the other hand, food and pharmaceutical processors opt for the pricier ceramic units. This choice stems from ceramics' enhanced heat and chemical tolerance, which markedly prolongs their service life. Pall's new GP-IC ceramic has addressed previous yield loss concerns, now boasting a high recovery rate for dairy proteins. Furthermore, China's Yiwu plant illustrates that when factoring in long-term pricing for fouling downtime, ceramics can rival the economic viability of polymeric options.

Metallic and other inorganic membranes command a modest market share, predominantly catering to semiconductor ultrapure water loops. In this specialized arena, the capability to eliminate minuscule particles can markedly boost chip yield. Asahi Kasei's OAT series rises to meet these exacting standards, albeit for a select fabrication node. Concurrently, heightened scrutiny on per- and polyfluoroalkyl substances in Europe has pivoted the industry's attention towards ceramics devoid of these compounds. Emphasizing this shift, Nanostone's Ceramic Ultrafiltration Flow, boasting an augmented surface area per module, is swaying procurement choices towards ceramics, especially among utilities with rigorous compliance mandates.

By Module Type: Hollow Fiber Dominance Meets Tubular Renaissance

In 2025, hollow fiber modules dominated the landscape, accounting for 51.45% of deployments. These modules boasted the capability to pack up to 1,200 square meters of membrane per cubic meter and effectively managed solids through an outside-in flow. Meanwhile, spiral-wound designs transitioned from reverse osmosis to ultrafiltration, catering to sanitary needs in the food and pharmaceutical sectors. Notably, Alfa Laval’s DuroLac spiral, with its innovative envelope geometry tweaks, achieved a 15% boost in permeate. Tubular modules, favored for breweries and high-solids municipal retrofits due to their ability to scour foulants with shear, are projected to grow at a 10.24% CAGR from 2026 to 2031. A testament to this technology's prowess, Yiwu in China showcased a ceramic tubular installation achieving crossflow velocities of 3 meters per second, effectively warding off algae. In the realm of single-use biotech, plate-and-frame capsules are flourishing. Merck’s Cork plant, for instance, produces Pellicon devices that not only sidestep cleaning validation but also expedite batch turnover.

By Application: Pharmaceutical and Biotechnology Outpace Legacy Water Treatment

In 2025, water and wastewater held a 49.14% market share, but from 2026 to 2031, the pharmaceuticals and biotechnology sectors are projected to grow at a robust CAGR of 10.67% from 2026 to 2031. Companies are aggressively staking their claims in the ultrafiltration market. Merck has made a strategic pivot with its climate-neutral facility in Cork, Ireland, now rolling out virus filters and tangential-flow cassettes, emphasizing localized production. Meanwhile, Asahi Kasei is gearing up to unveil its Planova plant in Japan, targeting recombinant protein clearance, a move driven by the surging demand from biologics pipelines. In the food and beverage arena, there's a marked increase in membrane-enabled valorization of whey and fermentation broths, with Alfa Laval clinching a major contract in Asia as a testament. Although the demand for ultrapure water in microelectronics is relatively niche, its importance is highlighted by the critical role of ceramics in removing 10-nanometer particles.

By End-User Industry: Healthcare Buyers Accelerate Single-Use Adoption

In 2025, municipal utilities commanded a dominant 54.23% share of the ultrafiltration market. However, the healthcare sector is set to experience a robust growth spurt, with projections indicating a 10.61% CAGR from 2026 to 2031. The allure of single-use assemblies lies in their ability to minimize cleaning validation processes, coupled with stringent high-purity requirements that justify premium pricing. A testament to the industry's scale, Cytiva and Pall have rolled out a multibillion-dollar initiative spanning 13 plants. Meanwhile, Alioth Biotech is strategically positioning itself by localizing membranes to cater to China's burgeoning biosimilar market. Industrial sectors, ranging from petrochemicals to mining, are increasingly turning to membranes to meet zero-liquid-discharge goals or reuse mandates, with Veolia's flagship project in Brazil leading the charge. In agriculture, the adoption remains limited and niche, primarily focused on greenhouse fertigation loops and land-based aquaculture.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 38.31% of global revenue, fueled by China's desalination initiatives, Singapore's NEWater expansion, and India's vaccine manufacturing. Notably, an ultrafiltration pretreatment in Qingdao Dongjiakou has set a new standard for energy efficiency. Singapore's predictive cleaning techniques have yielded impressive energy savings, underscoring the power of data-driven operations. Additionally, pharmaceutical centers in Hyderabad and Bangalore are increasingly opting for imported single-use cassettes, signaling a market opportunity for domestic suppliers.

From 2026 to 2031, the Middle-East and Africa are poised to lead with a robust 10.74% CAGR. The Saudi National Water Company is spearheading a major initiative in Qassim, and Bahrain is heavily investing in its Sitra and Hidd projects. Notably, many recent desalination tenders in the region are now featuring ultrafiltration, highlighting its crucial role in water security. In South Africa, municipalities are exploring containerized skids as a budget-friendly solution to drought challenges.

While Europe and North America command a significant share of global revenue, their growth is tempered by a focus on retrofits and replacements. The European Union's Urban Wastewater Directive emphasizes the removal of nutrients and microplastics. Furthermore, with new per- and polyfluoroalkyl substance limits set to kick in by 2026, there is a surge in membrane technology advancements. Alfa Laval's Sarpsborg plant is on track to meet these regulatory standards by 2027. In North America, even as the capital cycle slows, there is a steady demand driven by bioprocessing expansions. A case in point is Meissner's new plant in Georgia, which not only produces single-use systems but also generates significant employment. Meanwhile, in South America, despite a smaller market presence, Veolia's Vitória station in Brazil underscores the region's potential for industrial water reuse.

Competitive Landscape

The Ultrafiltration Market is moderately fragmented. Innovations are buzzing: from graduated-permeability ceramics and sensor arrays predicting fouling, to groundbreaking recycling techniques that repurpose spent reverse-osmosis elements into ultrafiltration membranes with enhanced permeability. In the competitive landscape, Nanostone Water is championing its per- and polyfluoroalkyl substances-free continuous ultrafiltration flow, while Alioth Biotech rolls out filters specifically designed for China's domestic market. Merck's Cork facility is setting sustainability standards, achieving a remarkably high-purity water reuse rate, and running solely on renewable energy. Meanwhile, FrieslandCampina and VITO's collaboration on ceramic scale-up underscores a growing trend: end-users are keen to co-develop materials, aiming to break free from conventional suppliers.

Ultrafiltration Industry Leaders

DuPont

TORAY INDUSTRIES, INC.

Veolia

Pentair

Alfa Laval

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Nanostone has introduced CUF|Flow, its newest ceramic ultrafiltration (UF) module, delivering a notable improvement in capacity, efficiency, and sustainability for municipal and industrial water treatment applications.

- September 2025: Pall Corporation introduced the Membralox GP-IC system, which boosted filtration capacity by 45% and enabled a 95% product recovery rate, marking a significant innovation in filtration technology.

Global Ultrafiltration Market Report Scope

Ultrafiltration is a pressure-driven membrane filtration process that separates suspended solids, bacteria, viruses, and macromolecules from water or other fluids. Using membranes with pore sizes typically between 0.01 and 0.1 microns, it provides high-quality purification while retaining essential minerals. Ultrafiltration is widely applied in water and wastewater treatment, food and beverage processing, pharmaceuticals, and industrial operations, offering efficient, reliable, and environmentally friendly separation technology.

The Ultrafiltration Market is segmented by membrane type, module type, application, end-user industry, and geography. By membrane type, the market is segmented into polymeric membranes, ceramic membranes, metallic, and other inorganic membranes. By module type, the market is segmented into hollow fiber, spiral wound, tubular, and plate and frame. By application, the market is segmented into water and wastewater treatment, food and beverage processing, pharmaceuticals and biotechnology, chemicals and petrochemicals, and micro-electronics. By end-user industry, the market is segmented into municipal, industrial, healthcare, and agriculture. The report also covers the market size and forecasts for the Ultrafiltration Market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Polymeric Membranes |

| Ceramic Membranes |

| Metallic and Other Inorganic Membranes |

| Hollow Fiber |

| Spiral Wound |

| Tubular |

| Plate and Frame |

| Water and Wastewater Treatment |

| Food and Beverage Processing |

| Pharmaceuticals and Biotechnology |

| Chemicals and Petrochemicals |

| Micro-electronics |

| Municipal |

| Industrial |

| Healthcare |

| Agriculture |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Membrane Type | Polymeric Membranes | |

| Ceramic Membranes | ||

| Metallic and Other Inorganic Membranes | ||

| By Module Type | Hollow Fiber | |

| Spiral Wound | ||

| Tubular | ||

| Plate and Frame | ||

| By Application | Water and Wastewater Treatment | |

| Food and Beverage Processing | ||

| Pharmaceuticals and Biotechnology | ||

| Chemicals and Petrochemicals | ||

| Micro-electronics | ||

| By End-user Industry | Municipal | |

| Industrial | ||

| Healthcare | ||

| Agriculture | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the ultrafiltration market?

The ultrafiltration market stands at USD 61.59 billion and is forecast to reach USD 95.09 billion by 2031 at a 9.07% CAGR from 2026 to 2031.

Which region shows the fastest growth pace?

The Middle-East and Africa are projected to expand at about 10.74% CAGR from 2026 to 2031.

Which application area is set to outpace others?

Pharmaceuticals and biotechnology are expected to post the strongest 10.67% CAGR from 2026 to 2031.

Why are ceramic membranes gaining popularity?

Longer service life under harsh cleaning, per- and polyfluoroalkyl substances (PFAS)-free construction, and falling lifecycle costs drive adoption.

What key regulation is pushing adoption in the United States?

In November 2025, governors petitioned for microplastics monitoring under the Unregulated Contaminant Monitoring Rule 6, urging utilities to channel investments into ultrafiltration.

Page last updated on: