Ultra Low Temperature Freezer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

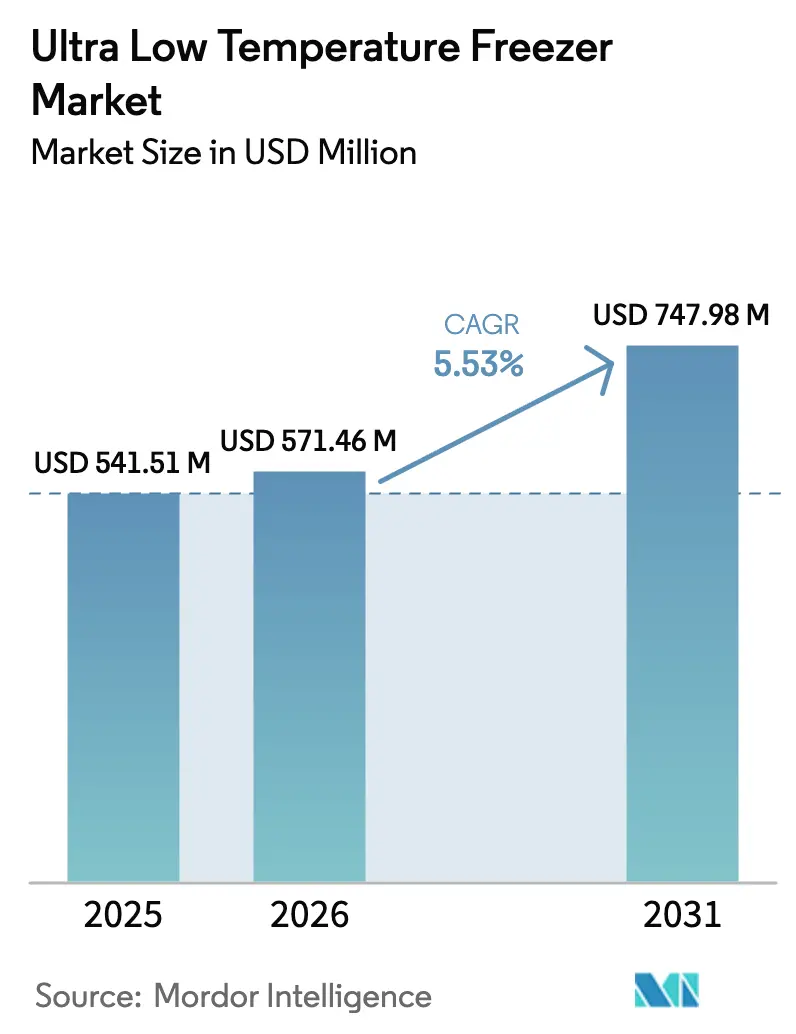

| Market Size (2026) | USD 571.46 Million |

| Market Size (2031) | USD 747.98 Million |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

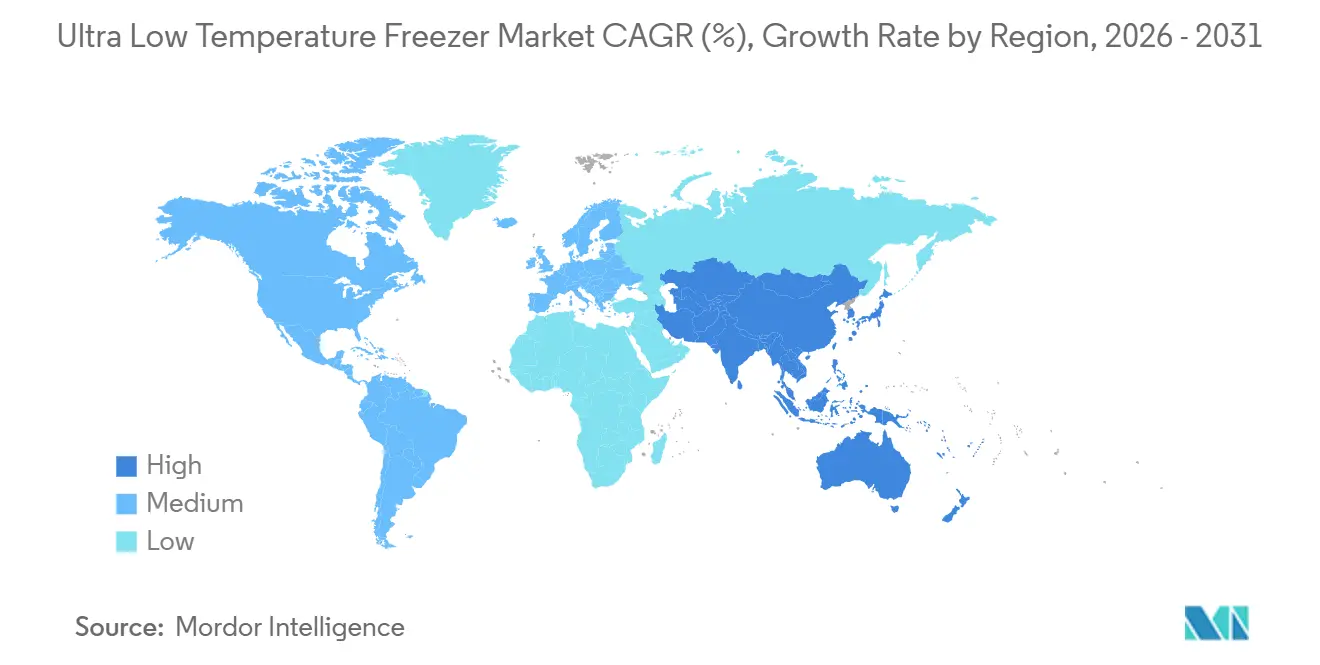

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ultra Low Temperature Freezer Market Analysis by Mordor Intelligence

The ultra-low temperature freezer market size was valued at USD 541.51 million in 2025 and is estimated to grow from USD 571.46 million in 2026 to reach USD 747.98 million by 2031, at a CAGR of 5.53% during the forecast period (2026-2031). Energy-efficient freezers that rely on natural refrigerants are displacing older cascade systems, while freezer-as-a-service contracts let laboratories shift large capital purchases to operating expenses. Upright units continue to dominate purchases because they optimize floor space and sample access, yet chest models are gaining favor in long-term biobanking due to tighter temperature uniformity. Pharmaceutical and biotechnology companies remain the largest buyers, but demand is rising fastest in hospitals and blood centers as decentralized clinical trials and point-of-care testing spread. Regionally, North America leads on the back of dense biobank networks and mandatory ENERGY STAR Version 2.0 limits, whereas Asia-Pacific will expand the quickest as China, Japan and India pour funds into genomics and regenerative-medicine infrastructure. [1]U.S. Environmental Protection Agency, “ENERGY STAR Product Specification for Laboratory Grade Refrigerators and Freezers, Version 2.0,” energystar.gov

Key Report Takeaways

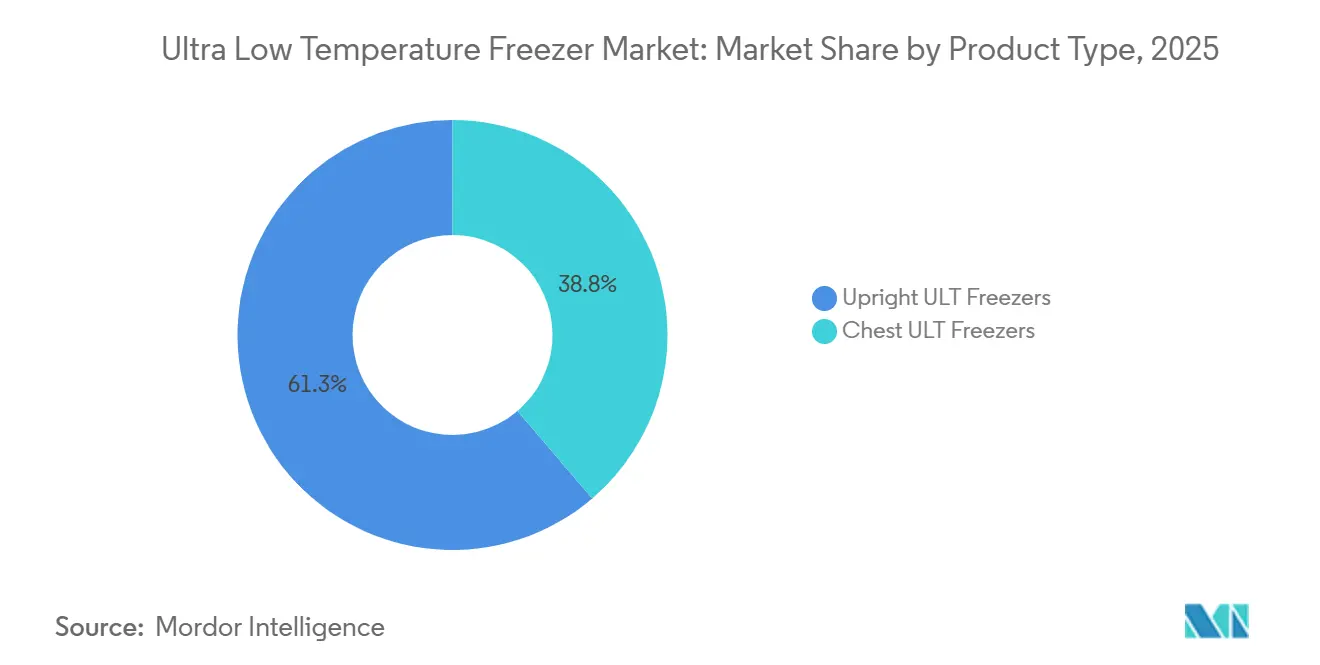

- By product type, upright configurations captured 61.25% of the ultra low temperature freezer market share in 2025; chest freezers are projected to grow at a 6.61% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies commanded a 44.23% share of the ultra low temperature freezer market size in 2025, while hospitals and blood centers are set to register the highest 6.34% CAGR to 2031.

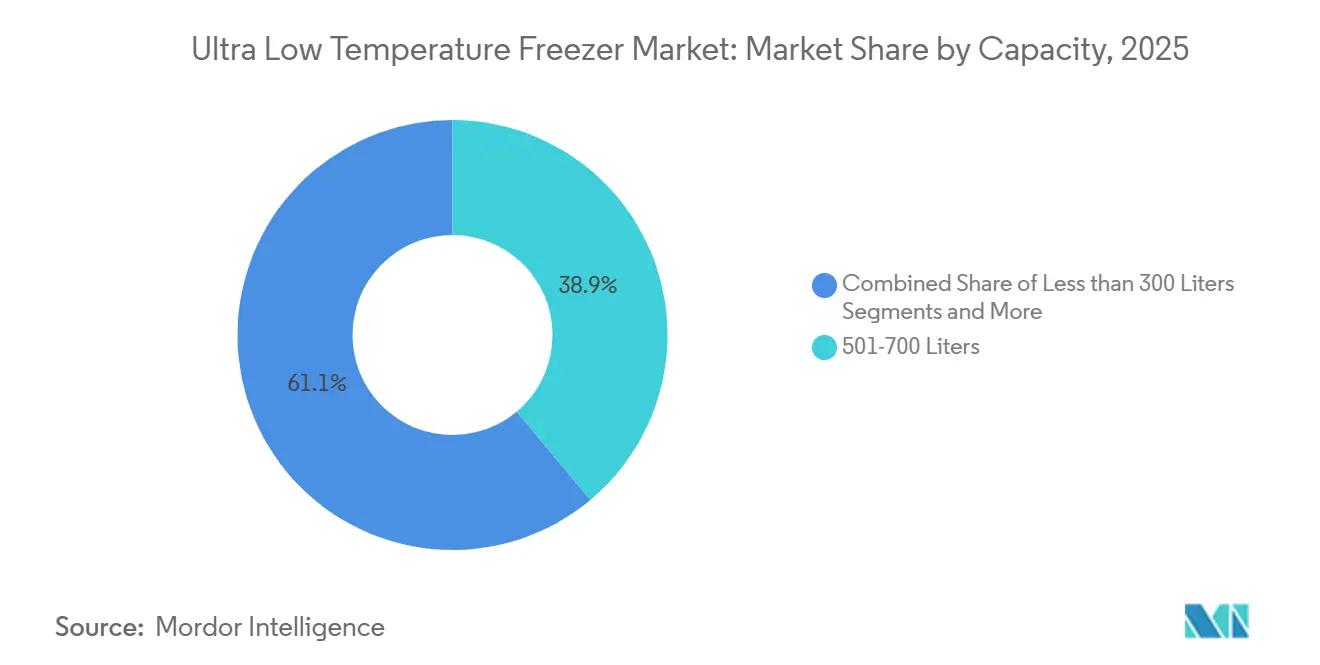

- By capacity, the 501-700 liter segment led with 38.91% of the ultra low temperature freezer market share in 2025; units below 300 liters are forecast to expand at a 6.73% CAGR between 2026-2031.

- By geography, North America held 42.45% revenue in 2025, and Asia-Pacific is anticipated to advance at the strongest 6.81% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ultra Low Temperature Freezer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding biobank networks worldwide | +1.2% | Global, with concentration in North America, Europe, and China | Long term (≥ 4 years) |

| Post-COVID vaccine cold-chain build-out | +0.8% | Global, particularly Asia-Pacific and Middle East | Medium term (2-4 years) |

| Rapid adoption of energy-efficient natural-refrigerant ULT models | +1.0% | North America & EU leading; APAC following | Medium term (2-4 years) |

| Growth of cell & gene therapy pipelines | +1.3% | North America, Europe, Japan | Long term (≥ 4 years) |

| ENERGY STAR compliance-driven replacement demand | +0.7% | North America, with spillover to Australia | Short term (≤ 2 years) |

| Emergence of freezer-as-a-service rental models | +0.4% | North America, Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Biobank Networks World-Wide

National genomic initiatives are scaling sample repositories beyond academic settings, lifting long-term demand for validated ultra low temperature storage. China’s National GeneBank added capacity for 50 million samples, and Japan’s Genome and Data Infrastructure Project funds biobanking tied to AI-led drug discovery, both of which specify freezers that meet ISO 13485 quality controls. [2]China National GeneBank, “Facility Overview and Capacity Expansion,” cngb.org India’s BioE3 Policy pairs biomanufacturing hubs with a 10,000-genome target, pressuring laboratories facing frequent power disruptions to order energy-efficient, battery-ready units. Azenta Life Sciences’ 2025 BioArc Ultra deal with UK Biocentre, which delivers 70% energy savings, shows sustainability now ranks alongside specimen security in tender criteria.

Post-COVID Vaccine Cold-Chain Build-Out

Infrastructure built for mRNA vaccines is being repurposed for monoclonal antibodies and next-gen therapeutics. DHL earmarked EUR 500 million for Asia-Pacific healthcare logistics and UPS invested USD 250 million in similar freezer farms, ensuring -80 °C capacity for biosimilars. Saudi Arabia’s biotechnology roadmap requires localized ULT storage for clinical-trial materials, and Japan keeps an emergency-approval pathway that encourages pharmaceutical firms to maintain surge capacity. Updated WHO guidelines strengthen validation rules, favoring manufacturers that bundle IoT monitoring and cloud archival services. [3]World Health Organization, “Cold Chain Equipment for COVID-19 Vaccines: Guidance,” who.int

Rapid Adoption of Energy-Efficient Natural-Refrigerant ULT Models

Escalating electricity tariffs and stricter F-gas curbs are accelerating a switch from HFC cascade systems to propane and ethane designs. EU Regulation 2024/573 tightens phasedown schedules, spurring vendors to redesign compressors around R290 and R170. Thermo Fisher’s TSX Universal Series cuts energy draw by 33% through variable-frequency drives, and PHC Holdings’ dual-voltage VIP ECO SMART consumes 5.4 kWh per day, meeting ENERGY STAR Version 2.0 thresholds.

Growth of Cell & Gene Therapy Pipelines

CAR-T therapies, gene-editing platforms and iPSC programs demand cryopreservation across manufacturing and clinical stages. Japan’s regenerative-medicine market is projected to exceed USD 22 billion by 2030, bringing 19 approved products that require −80 °C logistics. Europe’s EBiSC installed fully automated cryo-tanks with smart cryotubes for GDPR-compliant traceability, and Mitsubishi Logistics runs a ULT hub in Kawasaki dedicated to cell-therapy cargo.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & operating costs | -0.6% | Global, acute in emerging markets and small laboratories | Medium term (2-4 years) |

| Complex multi-jurisdictional regulatory compliance | -0.4% | Global, especially North America, EU, and Japan | Long term (≥ 4 years) |

| Grid-instability risks in emerging markets | -0.5% | Sub-Saharan Africa, South Asia, parts of Middle East | Long term (≥ 4 years) |

| Liquid-nitrogen cryogenic alternatives in niche segments | -0.3% | Global, concentrated in stem-cell and reproductive-medicine applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Costs

Purchase prices range from USD 8,000 for compact models to USD 25,000 for high-capacity dual-compressor units, and annual running costs add USD 1,000-3,000. Nigeria’s heavy generator reliance lifts total costs by up to 60%, while even efficient units carry 20-30% price premiums that stress public-sector budgets.

Complex Multi-Jurisdictional Regulatory Compliance

FDA 21 CFR Part 11, EU MDR and ISO 13485 each impose separate validation, cybersecurity and post-market surveillance rules, extending launch timelines by six to twelve months. Japan’s PMDA and China’s NMPA demand local testing even for CE-marked products, fragmenting model lines and inflating distributor inventories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Upright Dominance Meets Chest Resurgence

Upright units comprised 61.25% of 2025 revenue for the ultra low temperature freezer market thanks to efficient racking and faster lid-to-specimen retrieval. Energy savings, IoT monitoring and ENERGY STAR labels now dictate procurement checklists. Conversely, chest freezers’ superior thermal retention underpins a 6.61% forecast CAGR through 2031. Binder, Liebherr and Meling capitalize on thicker wall insulation to house vacuum-insulation panels without shrinking usable volume. As biobanks store irreplaceable genomic archives for decades, chest designs find renewed relevance despite slower sample access.

Competitive innovation is reshaping both categories. Uprights integrate cloud dashboards that log alarms for FDA-compliant audits, and chest designs add side-access ports for robotic pick-and-place modules. Portable micro-freezers are also emerging, carving out a sub-segment that supports mobile vaccination clinics, yet they still roll up under the broader ultra low temperature freezer market for reporting purposes.

By End User: Pharma Incumbency Versus Hospital Acceleration

Pharmaceutical and biotech firms held a 44.23% slice of the ultra low temperature freezer market size in 2025, driven by master-cell banks and global stability studies. Hospitals and blood centers, currently smaller in absolute revenue, will log the strongest 6.34% CAGR on the back of decentralized clinical trials and expanded blood fractionation services. CROs increasingly lease capacity through freezer-as-a-service programs to align cold store counts with project pipelines, while academic labs consolidate legacy fleets into shared core facilities to minimize redundant maintenance contracts.

Saudi Arabia’s Vision 2030 biotechnology targets and India’s cell-therapy focus are blurring lines among these user groups. Shared campuses like Japan’s Greater Tokyo Biocommunity house start-ups next to contract manufacturers and universities, pooling cold infrastructure and further accelerating unit refresh cycles across the ultra low temperature freezer market.

By Capacity: Mid-Range Incumbency Challenged by Compact Growth

Freezers sized 501-700 liters produced 38.91% of 2025 sales, a sweet spot balancing rack density and doorway clearance. Nevertheless, sub-300 liter models will post the fastest 6.73% CAGR as mobile clinics and satellite labs seek grid-independent, battery-ready solutions. Compact units now ship with the same dual-compressor redundancy and IoT telemetry historically reserved for larger volumes, flattening performance gaps.

Non-linear energy scaling encourages labs to right-size purchases: a 700-liter freezer typically uses only 20% more power than a 500-liter unit. Vendors such as B Medical Systems and Haier Biomedical respond with modular arrays of smaller freezers governed by centralized alarm servers, encouraging laboratories to build redundancy through distributed capacity rather than monolithic cabinets.

Geography Analysis

North America generated 42.45% of 2025 revenue in the ultra low temperature freezer market. Over 600 biobanks and the NIH All of Us program create steady replacement demand as older units fail ENERGY STAR Version 2.0 thresholds that began in June 2025. Canada’s Toronto-Montreal corridor expands regenerative-medicine manufacturing that relies on validated ULT storage, and nearshoring pushes contract manufacturing into Mexico to serve Latin American trial sites.

Asia-Pacific is set for the fastest 6.81% CAGR. China’s National GeneBank, Japan’s USD 3.3 billion Greater Tokyo Biocommunity and India’s BioE3 Policy collectively pump billions into biorepositories, accelerating orders for hydrocarbon-refrigerant units compliant with CE and GB standards. Australia’s TGA alignment with FDA and EMA eases market entry but high logistics costs favor Singapore-Hong Kong distribution hubs.

Europe’s strict F-gas phasedown propels replacement demand, while Saudi Arabia and Brazil spearhead growth in the Middle East and South America through vaccine self-sufficiency drives. Conversely, Sub-Saharan Africa’s 600 million residents without reliable power limit mechanical freezer uptake, steering some facilities toward LN₂ dewars or solar/battery hybrid kits until grid reliability improves.

Regulatory Landscape

Ultra-low temperature freezers used for regulated medical storage sit within medical-device and quality-system regimes in major markets. In the United States, medical-storage ULT freezers are classified as Class II devices under 21 CFR 864.9700, and laboratories using electronic records align freezer alarm and temperature-log systems with requirements such as FDA 21 CFR Part 11. ISO 13485:2016 is a common baseline for quality management across design and manufacturing.

Internationally, ISO 13485:2016 is a baseline for quality management across design and manufacturing, and it is frequently referenced in procurement for genomics and biobanking programs. For immunization and public-health procurement, WHO PQS performance specification E003/ULT01.1 anchors tests for holdover time, cooldown behavior, and operation across defined climate zones, influencing how manufacturers validate robustness for decentralized sites and grid-variable environments. In parallel, environmental and efficiency policies accelerate migration away from legacy HFC cascade systems, including EU Regulation 2024/573 tightening F-gas phasedown schedules and ENERGY STAR Version 2.0 thresholds in North America that drive replacement of higher-draw fleets.

Value Chain Analysis

The ULT freezer value chain starts with core inputs and subassemblies such as refrigeration components (compressors and related assemblies), vacuum insulation panels, cabinet fabrication materials, and electronic control and monitoring hardware. OEMs and major brands integrate these into final products in regional manufacturing and assembly hubs across North America, Europe, and China, then move units through direct sales teams, laboratory distributors, and service partners. For regulated end users, the chain extends beyond delivery into installation and qualification, where IQ/OQ/PQ activities in GxP environments (aligned with frameworks such as GMP Annex 15 and USP <1079>) add material time and cost and make local service coverage a practical differentiator.

Component availability and lead times remain a pivotal constraint and a driver of supplier strategy. Import dependence for specialized compressors, insulation technologies, and controllers exposes manufacturers and buyers to variability, and extended lead times for compressors and electronic controllers in 2024-2025 have elevated the value of inventory buffering and multi-sourcing. Downstream, the shift toward freezer-as-a-service and connected monitoring pushes additional value toward remote telemetry platforms, calibration, preventive maintenance, and compliance-ready documentation, making after-sales support and validated monitoring ecosystems an increasingly important part of competitive positioning.

Competitive Landscape

Thermo Fisher Scientific, PHC Holdings, Eppendorf and Haier Biomedical control an estimated 52% of global 2025 revenue, leveraging in-house compressor lines and vacuum-panel insulation to defend margins. M&A remains active: Global Cooling bought Stirling Ultracold in April 2024, while Azenta snapped up B Medical Systems and Barkey in 2022, bundling hardware with automated sample-management software and cryogenic logistics. Emerging challenger MIRAI Intex markets air-cycle refrigeration that eliminates HFCs altogether, attractive where F-gas levies rise annually.

White-space lies in modular biobanking arrays, predictive-maintenance algorithms and leasing programs that convert lump-sum capex into opex. Excedr and CryoSolutions AG offer multi-year rental platforms, while consumables vendors embed freezers in reagent-supply bundles, shifting negotiating leverage away from traditional hardware-only sellers. Cyber-secure IoT telemetry is also becoming a differentiator as FDA audits now scrutinize electronic logs under 21 CFR Part 11.

Ultra Low Temperature Freezer Industry Leaders

-

PHC Holdings Corporation

-

Thermo Fisher Scientific Inc.

-

Haier Smart Home Co., Ltd (Haier Biomedical)

-

Eppendorf SE

-

BioLife Solutions, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Replacement demand and specification-driven procurement create clear whitespace for energy-efficient, natural-refrigerant ULT platforms that reduce operating cost and simplify compliance reporting. In North America, ENERGY STAR Version 2.0 thresholds (with the market referencing an 8 kWh/day cap for qualifying models) have become an explicit decision gate for fleet refresh programs, and manufacturers are responding with redesigned refrigeration architectures and connected monitoring. In Europe, the tighter phasedown path under EU Regulation 2024/573 has moved natural refrigerants such as R290 and R170 from a premium feature to a design imperative for new bids, particularly where institutional buyers also score tenders on sustainability criteria.

Public-health and biobanking build-outs expand addressable demand for vaccine-grade performance, validated documentation, and resilient operation outside top-tier research campuses. WHO PQS E003/ULT01.1 and its verification protocol provide a concrete benchmark for procurement tied to immunization programs, favoring suppliers that can certify holdover performance, climate-zone operation, and reliable alarm logging. On the demand side, national genomics and regenerative-medicine initiatives that specify ISO 13485 quality controls, and logistics players building -80 C capacity for biologics, support opportunities for modular arrays, battery-ready configurations for grid-unstable settings, and service-led offerings that bundle monitoring, qualification, and preventive maintenance into predictable operating spend.

Recent Industry Developments

- April 2026: Esco Lifesciences launched the Esco Lexicon Dual System Ultra-Low Temperature Freezer, emphasizing enhanced insulation and backup refrigeration architecture. The launch expands competitive pressure around redundancy and sample protection features, which are increasingly specified in biobanking and regulated laboratory procurement.

- January 2026: PHC Corporation of North America announced the TwinGuard ECO 703VXH ULT freezer with dual independent refrigeration systems, natural refrigerants, and inverter-controlled compressors. The product positioning targets both sustainability metrics and risk mitigation for high-value samples, reinforcing the shift away from legacy cascade designs.

- April 2024: Liebherr expanded its ultra-low temperature freezer lineup by adding a compact 350-liter variant. The addition supports laboratories with constrained floor space and helps suppliers address demand growth in satellite labs and decentralized testing environments that favor smaller footprints without sacrificing ULT capability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue earned from selling ultra-low temperature freezers used to store sensitive biological and medical materials at very low temperatures, typically in the -45 C to -86 C operating range. The sizing reflects equipment sales value across major end-use settings and regions.

Scope exclusions: We exclude sample handling services, consumables, and facility HVAC or cold-room buildouts that sit outside standalone ULT freezer equipment.

Segmentation Overview

-

By Product Type

- Upright ULT Freezers

- Chest ULT Freezers

-

By End User

- Bio-Banks

- Pharmaceutical & Biotechnology Companies

- Academic & Research Laboratories

- Contract Research Organizations (CROs)

- Hospitals & Blood Centers

-

By Capacity

- Less than 300 Liters

- 301-500 Liters

- 501-700 Liters

- 701-900 Liters

- More than 900 Liters

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a demand map for ULT storage, and then aligning it with how equipment is bought and replaced in labs, biobanks, and healthcare settings. We rely on public references such as CDC and NIH guidance for lab and biospecimen handling context, FDA databases for regulated life science activity signals, and WHO publications for broader health system trends that influence cold storage needs.

We also use sources such as USITC trade statistics and UN Comtrade to understand cross-border equipment flows, and peer-reviewed journals to validate adoption trends like energy efficiency and natural refrigerants. Company annual reports, investor presentations, and press coverage help confirm product mix shifts like upright versus chest formats and typical purchasing cycles. For difficult-to-collect points, we use paid subscriptions for company financials and patent databases to cross-check technology direction and revenue exposure. These are illustrative sources only, and many other references were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys are used to sanity-check the desk model and close gaps around pricing, replacement timing, and real-world procurement behavior. We speak with manufacturers, distributors, service partners, lab managers, biobank operators, and procurement stakeholders across APAC, EMEA, and the Americas, so assumptions can be tested against what is actually being purchased and installed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 18% | APAC: 47% |

| Mid tier: 50% | Functional/Unit leaders: 32% | EMEA: 30% |

| Smaller Players: 19% | Managers: 50% | Americas: 23% |

Market-Sizing & Forecasting

The core sizing is built using a top-down approach where lab and biostorage activity indicators are converted into an addressable equipment demand pool, and then translated into annual unit needs by factoring in replacement cycles and new lab capacity additions. Once that structure is set, selective bottom-up checks are used, such as sampling average selling prices (ASP) by freezer type, checking unit shipment signals through trade flows, and validating the implied revenues against supplier and channel feedback.

Key inputs in the model include the installed base replacement rhythm for ULT freezers, the mix shift between upright and chest formats, typical capacity preferences tied to storage volume needs, energy efficiency-related upgrade decisions, and regional procurement patterns for research labs and biobanks. Where bottom-up checks are incomplete, gaps are handled by using conservative ranges for ASP and volume assumptions, which are then tightened through interview feedback.

For forecasting, scenario analysis is used first to reflect different funding and lab expansion environments, and then time series smoothing is applied to avoid unrealistic year-to-year jumps. Forecast paths are kept consistent with the same demand drivers used in the base year so the final numbers stay explainable and repeatable.

Data Validation & Update Cycle

Validation is done by comparing the model outputs with independent signals like import and export movements, observed procurement cycles, and the implied ASP range that buyers report paying. If results look misaligned for a region or year, assumptions are revisited, outliers are challenged, and targeted follow-up calls are triggered to confirm whether the change is real or a data artifact.

Before sign-off, the work is reviewed in multiple steps so the logic, math, and scope boundaries are consistent across regions and years. Reports are refreshed annually, and interim updates are made when major events occur, such as changes in funding patterns, large technology shifts, or meaningful pricing moves. Right before delivery, a final freshness check is done so clients receive the most current view available.

Mordor Intelligence's Ultra Low Temperature Freezers Market Sizing Compared With Other Published Estimates

It is normal to see different market values for ultra-low temperature freezers because the year chosen, the currency conversion timing, and the way pricing is averaged can change the total. Differences also come from whether the study anchors on equipment demand signals (installed base and replacement) or uses broader healthcare equipment spending as a starting point.

When ASP is updated frequently and corrected for regional mix, and when the final totals are checked against trade flow direction and interview-backed procurement behavior, the size estimate stays closer to what buyers actually face, which is why the 2026 figure shown here lands where it does in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 571.46 M (2026) | |

| Global Research House A | USD 780.80 M (2024) | Uses an earlier base year and appears to keep a broader ASP and scope set, which can pull in adjacent cold storage equipment or different temperature-range interpretations and make cross-year comparison uneven without re-basing. |

| Industry Publisher B | USD 862.00 M (2023) | Starts from a wider 2023 revenue pool and may include wider temperature-range and capacity brackets without separating only ULT-focused demand drivers, which typically lifts the total when mixed with broader freezer classes. |

Reading the three figures together, the spread is mainly explained by year alignment and how tightly the study separates ULT freezer equipment from nearby cold storage categories. By keeping the pricing logic tied to buyer-reported bands and then re-checking the totals against independent volume signals, the final number stays traceable to clear inputs and can be updated cleanly as conditions change.

Key Questions Answered in the Report

What CAGR is expected for ultra low temperature freezer sales between 2026 and 2031?

The market is projected to grow at a 5.53% CAGR over the forecast period.

Which region will add capacity the fastest?

Asia-Pacific is forecast to register the strongest 6.81% CAGR, spurred by major genomics and regenerative-medicine investments in China, Japan and India.

How do ENERGY STAR Version 2.0 rules affect purchasing decisions?

The 2025 rules cap daily energy draw at 8 kWh, prompting labs to retire non-compliant freezers and favor new hydrocarbon-based models with lower operating costs.

Why are hospitals increasing ultra-low freezer purchases?

Decentralized clinical trials, point-of-care testing and expanded blood-component processing drive hospitals to install validated −80 °C storage on-site.

What alternatives exist in regions with unstable electricity?

Facilities often pair mechanical ULT freezers with solar-battery backup or adopt liquid-nitrogen dewars that provide −196 °C storage without grid dependence.

Page last updated on: