Metallocene Polyethylene (mPE) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

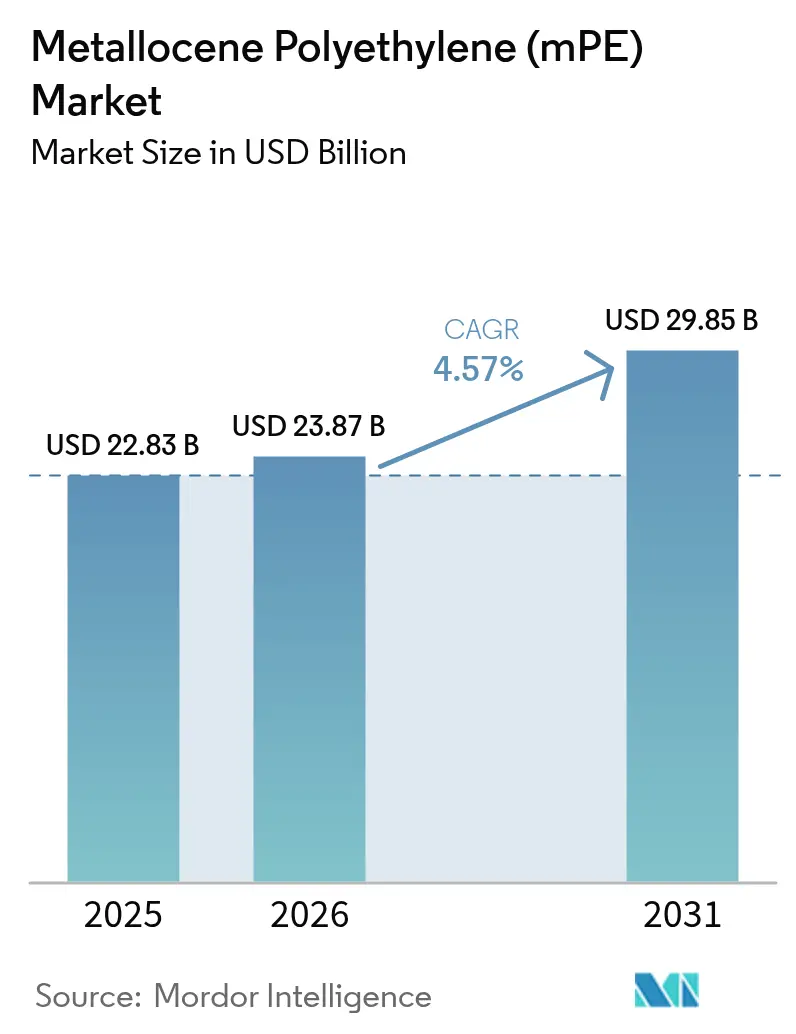

| Market Size (2026) | USD 23.87 Billion |

| Market Size (2031) | USD 29.85 Billion |

| Growth Rate (2026 - 2031) | 4.57% CAGR |

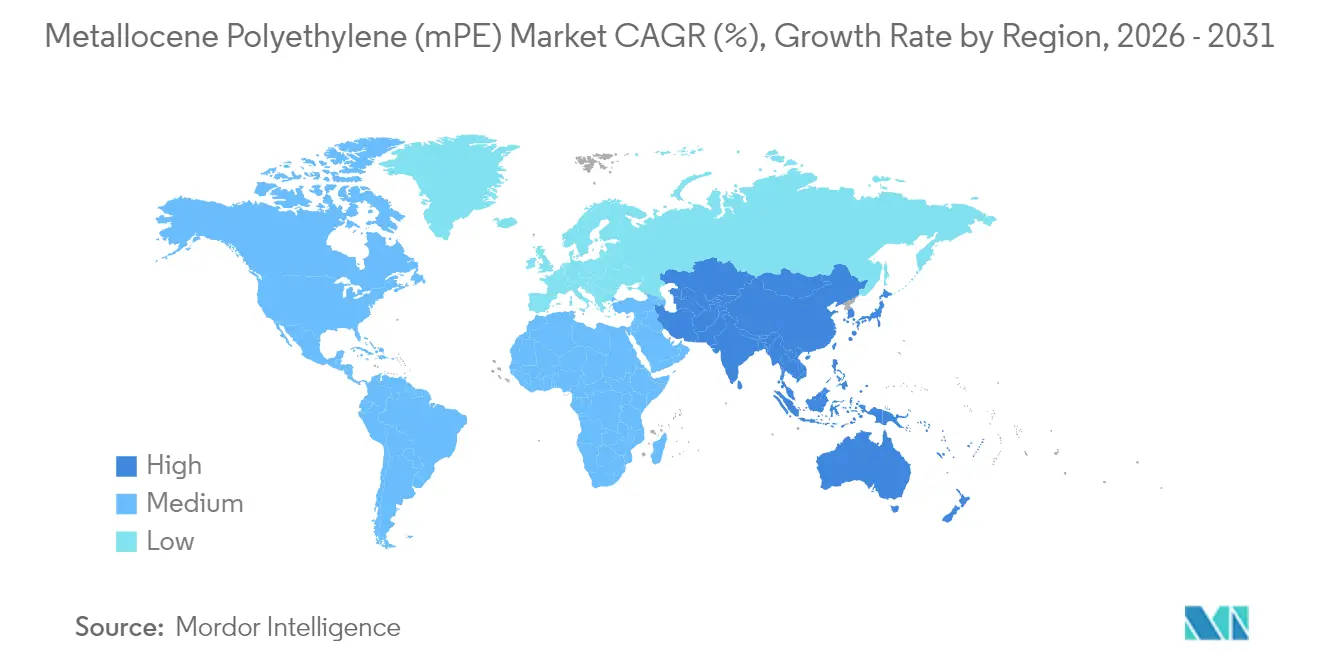

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

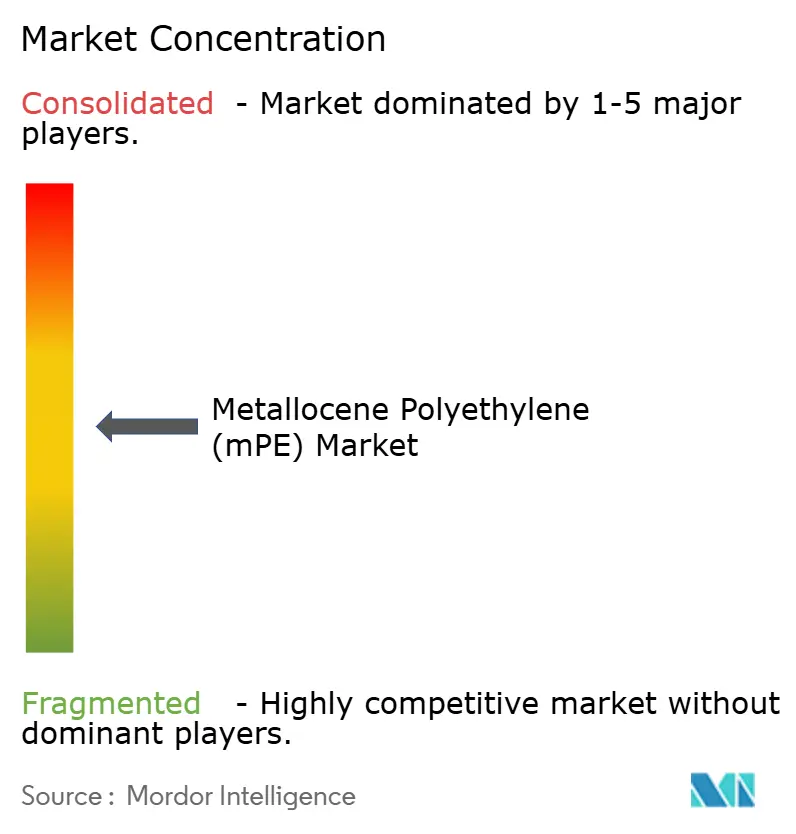

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metallocene Polyethylene (mPE) Market Analysis by Mordor Intelligence

The Metallocene Polyethylene Market size was valued at USD 22.83 billion in 2025 and estimated to grow from USD 23.87 billion in 2026 to reach USD 29.85 billion by 2031, at a CAGR of 4.57% during the forecast period (2026-2031). Robust demand for high-clarity down-gauged films, the scale-up of solar panel encapsulant lines, and modernization in agriculture sustain this growth path. Producers benefit from single-site catalyst technology that yields narrow molecular weight distribution, enabling consistent mechanical strength and superior optical properties at lower gauges. China’s ethylene capacity additions, India’s e-commerce boom, and capacity investments in the Middle East together reinforce upstream supply security, while ongoing shifts toward circular plastics keep strategic focus on advanced recycling and bio-based feedstocks. The Metallocene polyethylene market therefore marries performance gains with sustainability objectives and positions itself as a core enabler of next-generation flexible packaging solutions.

Key Report Takeaways

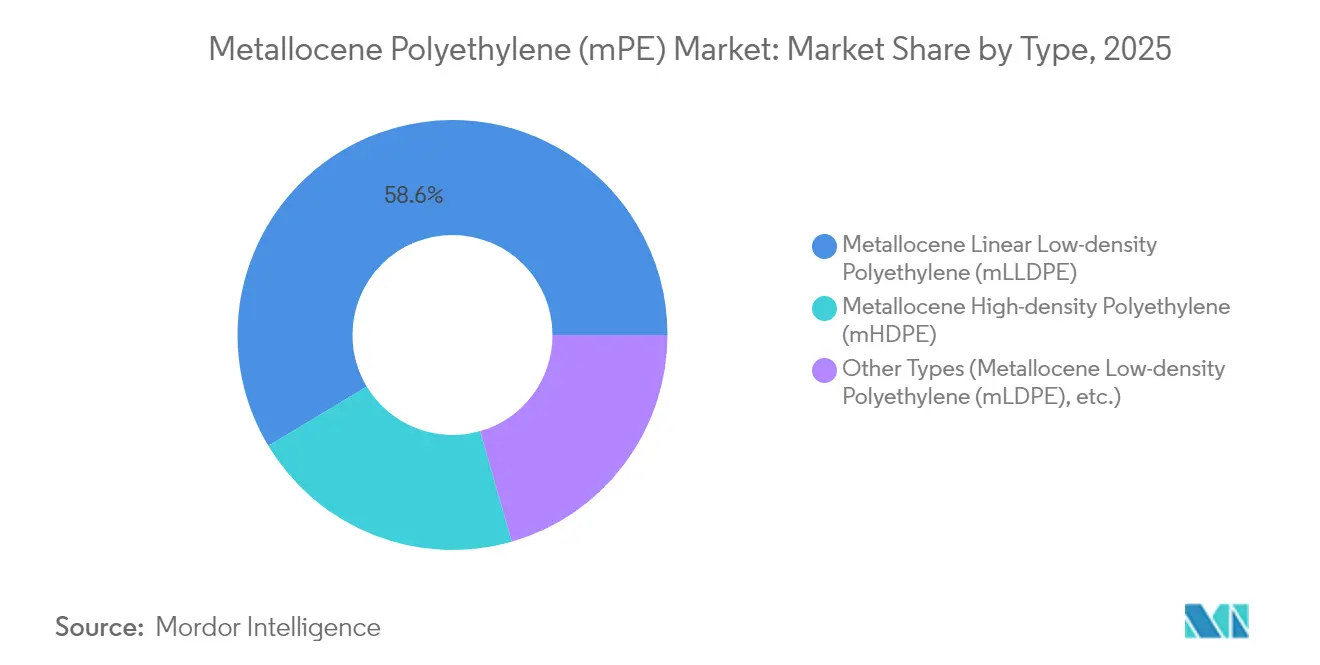

- By type, mLLDPE held 58.62% revenue share within the Metallocene polyethylene market in 2025, while mHDPE is anticipated to expand at 6.52% CAGR to 2031.

- By catalyst type, zirconocene catalysts captured 62.15% of Metallocene polyethylene market share in 2025. Further, Hafnocene catalysts are projected to post the fastest 5.14% CAGR through 2031.

- By application, films captured 70.97% of the Metallocene polyethylene market size in 2025; “other applications” including extrusion coatings and solar encapsulants will post the steepest 6.37% CAGR over the forecast horizon.

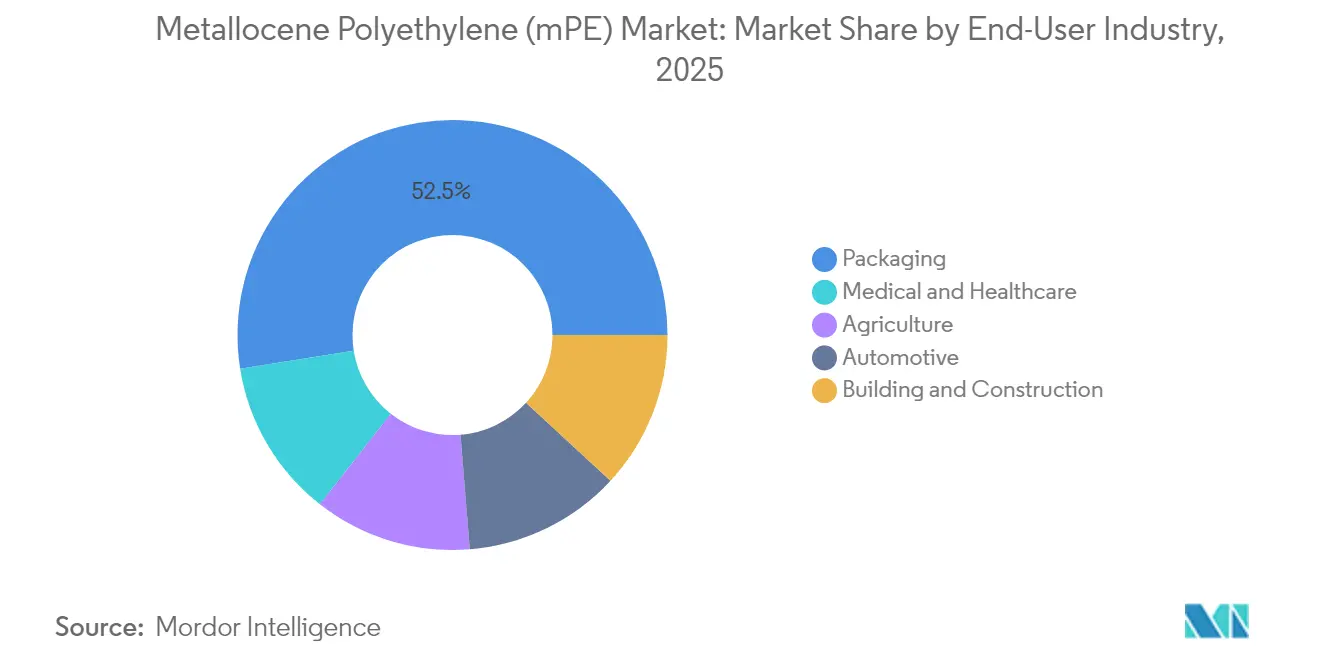

- By end-user industry, packaging accounted for 52.50% share of the Metallocene polyethylene market size in 2025; medical and healthcare is projected to register a 6.17% CAGR through 2031.

- By geography, Asia-Pacific commanded 45.83% of Metallocene polyethylene market share in 2025; North America is forecast to deliver the fastest regional CAGR at 5.63% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metallocene Polyethylene (mPE) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-clarity, down-gauged packaging films | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Surge in adoption of films and sheets in packaging industry | +1.0% | Global, led by Asia-Pacific emerging markets | Short term (≤ 2 years) |

| Growth of multilayer agricultural films and geomembranes | +0.8% | Asia-Pacific core, spill-over to Latin America and MEA | Long term (≥ 4 years) |

| Solar-panel encapsulant shift to mPE-based tie layers | +0.6% | Global, with early adoption in Europe and Asia-Pacific | Medium term (2-4 years) |

| Catalyst-switch flexible crackers enabling custom grades | +0.4% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Clarity, Down-Gauged Packaging Films

Converters continue to migrate toward thinner films that preserve mechanical integrity, and single-site catalysts facilitate uniform comonomer distribution that yields clarity alongside dart impact strength. Typical gauge reductions of 15-20% lower material use and carbon intensity, directly supporting brand-owner sustainability pledges. Narrow molecular weight distribution also cuts edge-trim waste on blown-film lines and improves bag-making throughput, which increases operating margins for convertors. Premium metallocene grades such as Exceed XP provide year-round toughness suited to cold-chain logistics, while the rapid rise of omnichannel retail elevates parcel-handling stresses that require stronger but lighter films[1]“Exceed™ XP High-Performance PE,” ExxonMobil Product Solutions, corporate.exxonmobil.com .

Surge in Adoption of Films and Sheets in Packaging Industry

Flexible formats replace rigid containers across food, home-care, and personal-care sectors as retailers prioritize shelf efficiency and lower logistics costs. Metallocene polyethylene delivers stronger hot-tack and wider sealing windows, reducing leakers on high-speed vertical form-fill-seal equipment. Trade bans on PVC in contact applications accelerate transition toward recyclable polyethylene blends, illustrated by PreservaWrap lines that replicate PVC clarity without chloride content[2]“Single-Use Plastics Directive Updates,” Progressive Grocer, progressivegrocer.com . Medical device makers also pivot from PVC to metallocene polyethylene for biocompatibility, which reinforces healthcare demand and widens segment reach.

Growth of Multilayer Agricultural Films and Geomembranes

Greenhouse operators adopt metallocene polyethylene films with tailored UV packages that extend service life by 30-40%, offsetting initial premium costs. Comonomer uniformity permits incorporation of light-diffusion and anti-drip additives without embrittlement. Geomembrane manufacturers favor stress-crack-resistant resins for landfill liners and water reservoirs used in arid regions. In China, rural revitalization programs grant subsidies for higher-specification greenhouse and irrigation films, stimulating incremental tonnage in the Metallocene polyethylene market.

Solar-Panel Encapsulant Shift to mPE-Based Tie Layers

Photovoltaic module makers increasingly select polyolefin encapsulants to eliminate acetic acid corrosion associated with EVA. Metallocene tie layers deliver volume resistivity improvements that mitigate potential-induced degradation, enabling 25-year warranty requirements. Vinyl-functionalized metallocene polyolefins cure 14-times faster during lamination while maintaining 91% light transmission, which shortens module cycle times and raises line productivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile ethylene feedstock costs | -0.8% | Global, with acute impact in regions dependent on imported feedstock | Short term (≤ 2 years) |

| Stringent single-use film regulations | -0.6% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Post-patent IP disputes on single-site catalysts | -0.3% | Global, with concentration in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Ethylene Feedstock Costs

Swing crude and natural-gas prices cascade into ethylene swings, compressing margins for specialty resin producers who pay a 15-20% catalyst premium. Electrified crackers and carbon-capture retrofits inflate capital cost, adding pressure during feedstock spikes. Vertically integrated Middle Eastern producers retain cost leadership while Asian converters reliant on imports see steeper volatility. Bio-ethylene routes partly hedge volatility yet call for parallel infrastructure build-out, raising upfront cash needs.

Stringent Single-Use Film Regulations

Policy makers in Europe and parts of North America target single-use plastics, adding compliance layers for packaging films even when they are recyclable. Fragmented rules force multinational converters to juggle material reforms for each jurisdiction, raising SKU complexity. California’s PVC ban in food packaging drives substitution toward polyethylene but broader plastic curbs could curb absolute volume growth for certain thin-wall items.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: mLLDPE Dominance Drives Market Evolution

mLLDPE commanded 58.62% Metallocene polyethylene market share in 2025. The segment retains leadership thanks to superior puncture resistance and dart impact strength that allow 15-20% down-gauging without packaging failure. Many beverage pouch producers shifted entirely to mLLDPE structures in 2024. In pipe coatings, mLLDPE’s flexibility reduces cracking risk during coil-on-reel handling.

mHDPE is forecast to log a 6.52% CAGR through 2031, boosted by pressure pipe and chemical drum demand in developing economies. Stress-crack-resistant grades also penetrate fuel tank blow-molding and under-hood parts. Niche mLDPE lines serve specialty cast-film uses where melt strength is crucial. UHMWPE advances broaden reach into artificial joints and protective gear markets, fortifying value pools for the Metallocene polyethylene market.

By Catalyst Type: Zirconocene Leadership Faces Hafnocene Challenge

Zirconocene catalysts held 62.15% share in 2025. Producers favor their proven operability across gas-phase and solution reactors. Strong track records shorten qualification times, essential for food-contact certifications.

Hafnocene systems, expanding at 5.14% CAGR, excel in high-temperature polymerization that enables faster gas-phase throughput. Recent ligand innovations temper activity drop-off above 90 °C, widening the commercial window. Dual-site and hybrid designs merge narrow and broad molecular fractions in one step, unlocking tailored melt rheology. These innovations further diversify offerings within the Metallocene polyethylene market.

By Application: Films Segment Leverages Superior Properties

Films dominated with 70.97% share in 2025. High seal strength at lower thickness allows brand owners to cut plastic intensity per package without compromising product safety. Growth in chilled ready-meal pouches, stand-up spouted caps, and heavy-duty sacks keeps films consumption buoyant.

Other applications, slated to expand 6.37% CAGR, encompass solar encapsulants, extrusion coatings, and medical device parts. Polyolefin encapsulant replacements for EVA reduce corrosion risk in new heterojunction solar modules, while medical blister packs benefit from wider seal windows that secure sterilization integrity.

By End-User Industry: Packaging Dominance Amid Healthcare Surge

Packaging captured 52.50% of Metallocene polyethylene market size in 2025 and remains buoyant as omnichannel retail demands puncture-resistant mailers. E-grocery adoption pushes frozen-chain demands where mLLDPE’s toughness is paramount.

Medical and healthcare show a 6.17% CAGR outlook as hospitals move away from plasticized PVC tubing. Metallocene polyethylene’s inherent flexibility without plasticizers removes leachability concerns. Agriculture also picks up share through advanced mulch and greenhouse films that withstand UV and mechanical fatigue across multiple crop cycles.

Geography Analysis

Asia-Pacific led with 45.83% share in 2025, anchored by China’s new 1.8 million t ethylene units and India’s packaging upturn. These investments ensure feedstock security and shorten delivery time for regional converters. Packaging, construction membranes, and automotive fuel tanks together lifted regional off-take and are expected to keep the Metallocene polyethylene market on a 4.57% CAGR trajectory.

North America relies on shale-linked ethane cost advantages and catalyst innovation leadership. Dow’s forthcoming net-zero cracker in Alberta is poised to support premium resin output with low embedded emissions. Mexico secures back-integration gains by importing feedstock from US Gulf complexes and converting into value-added films for domestic consumption and export.

Europe’s strict plastic rules challenge demand yet simultaneously open space for recyclable flexible packaging. Germany’s auto sector values weight reduction, and Nordic retailers champion mono-material structures that simplify mechanical recycling. TotalEnergies’ Amiral complex, though Middle Eastern, channels volumes into Europe, supplementing short domestic supply. South America and the Middle East & Africa remain emerging yet fast-growing clusters. Brazil’s greenhouse sector and Qatar’s polymer complex expansion add incremental pull on the Metallocene polyethylene market.

Regulatory Landscape

Regulation affecting metallocene polyethylene (mPE) is tightening around food-contact plastics, recycled-content governance, and microplastics definitions that can affect additives, powders, and downstream uses. In the European Union, Regulation (EU) 2025/351 amends Regulation (EU) No 10/2011 for plastic materials intended for food contact, strengthening quality control and manufacturing expectations around recycled plastics used in food-contact applications. This increases documentation and supplier-qualification requirements for mPE grades used in packaging.

For chemicals management, the EU continues to operationalize the REACH restriction on synthetic polymer microparticles (Annex XVII, Entry 78). Commission Regulation (EU) 2026/1168 (published June 2026) amends and clarifies aspects of the microplastics restriction, including provisions relevant to R&D and certain application categories. Resin and compound suppliers must verify whether particular product forms or use cases trigger obligations or fall under derogations, such as permanent incorporation into a solid matrix. In the United States, food-contact compliance remains anchored in the FDA Food Contact Notification (FCN) framework, with ongoing updates including notices of FCNs that are no longer effective, reinforcing the need for converters and resin suppliers to track substance status for food packaging applications.

Value Chain Analysis

The mPE value chain starts with hydrocarbon feedstocks (naphtha/ethane) converted to ethylene, followed by polymerization in gas-phase or solution processes using single-site catalyst systems. This produces mLLDPE, mHDPE, and specialty grades. A critical upstream layer is catalyst and process technology, including metallocene and post-metallocene systems and licensed platforms used to produce metallocene-enabled PE families, which shapes achievable resin property windows such as narrow molecular weight distribution, sealing performance, and downgauging capability.

Polymer producers, often integrated with ethylene crackers, sell to converters that dominate downstream tonnage. These include blown and cast film producers, sheet and extrusion coaters, and compounders serving packaging, agriculture, medical, and industrial applications. Value capture concentrates in resin production and conversion, where catalyst premiums, qualification cycles (notably for food-contact and medical uses), and ethylene cost volatility affect margins. Distribution is typically via direct contracts and regional warehousing to maintain supply continuity for high-throughput film lines, while circularity initiatives add another node through mechanical recycling and advanced-recycling feedstock streams that must be quality-controlled to preserve mPE performance in downgauged structures.

Competitive Landscape

The metallocene polyethylene (mPE) market is moderately fragmented in nature. Leading producers hold proprietary single-site catalyst platforms and upstream integration. Dow markets INSITE technology and is trialing electrified cracking to cut Scope 1 emissions. SABIC leverages joint ventures in China to place capacity near growth nodes. LyondellBasell applies its Hostalen ACP process for bimodal mHDPE grades used in pressure pipe. ExxonMobil’s cross-licensing with Chevron Phillips resolved long-running IP disputes, lowering legal risk and enabling broader grade portfolios.

Technology differentiation remains central. Univation’s XCAT delivers gas-phase mLLDPE with narrow dispersion for collation shrink. Borealis applies Borstar tandem reactors to blend metallocene and traditional fractions for rigid packaging. ADNOC-OMV-Nova’s merger pools 13.6 million t global polyolefin capacity, bolstering feedstock optionality.

Metallocene Polyethylene (mPE) Industry Leaders

SABIC

Chevron Phillips Chemical Company LLC.

Dow

Exxon Mobil Corporation

LyondellBasell Industries Holdings B.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity centers on new integrated capacity and specialty-unit commissioning that expands availability of metallocene-enabled grades in high-growth packaging and industrial film hubs. In China, the Sinopec-SABIC Gulei Petrochemical project reported mechanical completion (April 2026) of a 600,000 tons/year metallocene specialty polyethylene unit within a 1.5 million ton ethylene complex, with commissioning activity referenced for the second half of 2026. This expands local supply of metallocene-grade PE for downgauged films and helps converters shorten qualification and lead-time cycles versus imported specialty resins.

In the Middle East, upstream expansions that increase regional olefins availability support resin portfolio growth and improve feedstock optionality for metallocene-enabled polyethylene production. Tasnee completed a USD 500 million ethylene expansion at the Saudi Ethylene and Polyethylene Company (SEPC) cracker in Al Jubail Industrial City (July 2026), increasing olefins capacity and reinforcing the region's role as a cost-advantaged supply base for polyethylene value chains. Beyond these supply-side moves, application whitespace aligns with already visible demand, including high-clarity downgauged packaging films, polyolefin solar encapsulant and tie-layer structures replacing EVA in modules, and medical and healthcare conversions away from plasticized PVC, where mPE grades can provide flexibility without added plasticizers and support wider sealing windows in packaging formats.

Recent Industry Developments

- July 2026: Tasnee completed a USD 500 million ethylene expansion project at the Saudi Ethylene and Polyethylene Company (SEPC) cracker in Al Jubail Industrial City, increasing olefins production capacity by 18%. The additional ethylene availability supports polyethylene chain utilization and strengthens feedstock security for specialty polyethylene slates that include metallocene-enabled grades in the region.

- May 2025: Univation Technologies announced a world-scale 800,000 tonnes/year design capacity offering for its UNIPOL PE Process technology, which includes manufacturing capability for metallocene PE alongside unimodal and bimodal HDPE and LLDPE. The larger reference scale improves the economics and attractiveness of new PE projects for licensors and producers, and it supports flexible grade production targeted at downgauged film and other performance-driven applications.

- October 2024: TotalEnergies expanded its metallocene polyethylene product portfolio by introducing a new grade with very low linear density. The addition targets film converters seeking improved sealing and downgauging performance, and it increases competitive pressure among suppliers differentiating through specialty-grade breadth rather than commodity volume.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the metallocene polyethylene market covers revenues from mPE resin sold into downstream converters and compounders, across major end uses such as packaging films, rigid packaging, pipes, and other molded or coated applications, reported in USD.

Scope exclusions: metallocene catalyst sales and conventional polyethylene grades not produced using metallocene catalysis are excluded from the market value.

Segmentation Overview

- By Type

- Metallocene Linear Low-density Polyethylene (mLLDPE)

- Metallocene High-density Polyethylene (mHDPE)

- Other Types (Metallocene Low-density Polyethylene (mLDPE), etc.)

- By Catalyst Type

- Single-site Zirconocene

- Hafnocene and post-metallocene

- Dual-site and hybrid systems

- By Application

- Films

- Sheets

- Other Applications (Extrusion Coatings, etc.)

- By End-User Industry

- Packaging

- Agriculture

- Automotive

- Building and Construction

- Medical and Healthcare

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Turkey

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- South Africa

- Nigeria

- Egypt

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building the demand context for polyethylene and film applications using public sources such as U.S. Energy Information Administration (EIA) feedstock indicators, U.S. International Trade Commission (USITC) trade statistics, UN Comtrade shipment trends, and the World Bank macro and industrial output series. For product and definition consistency, we also referenced association and standards bodies that publish plastics and polymer context, including PlasticsEurope and ASTM documentation, plus peer-reviewed polymer science articles.

On the supply side, we used public company filings, investor presentations, plant announcements in reputed press, and customs and tariff notes to understand capacity additions and regional trade flows. A paid subscription focused on company financials and a shipment-level import export database were used selectively to cross-check producer exposure and country movement patterns when public data was not granular enough. The sources listed here are illustrative, and many other public documents were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test key assumptions through structured interviews and short surveys with resin producers, polymer distributors, converters (especially film and packaging), and knowledgeable participants from the processing ecosystem. Since this is a global market, inputs were balanced across APAC, EMEA, and the Americas so regional pricing, availability, and substitution patterns could be checked before final numbers were signed off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | APAC: 49% |

| Mid tier: 51% | Functional/Unit leaders: 25% | EMEA: 30% |

| Smaller Players: 22% | Managers: 59% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where polyethylene demand pools are reconstructed using polymer consumption indicators, packaging film output signals, and regional trade and production context, then the mPE share is applied using adoption rates discussed by industry participants. Once this structure was in place, totals were checked using selective bottom-up approximations, such as sampling resin pricing ranges and typical contract movement, and then scaling with region-level volume cues to confirm the implied revenue envelope.

Key inputs used in the model include crude and ethylene feedstock trends, polyethylene and film demand growth in packaging, announced capacity changes and utilization direction, regional import export intensity for polyethylene materials, and the observed mPE premium versus conventional PE in common applications. Forecasting uses scenario analysis supported by short multivariate regression tests, where demand growth, feedstock-linked pricing direction, and adoption shifts are varied together based on the consensus from primary respondents. When a country or application lacked usable conversion-level cues, the gap was handled with proxy penetration rates from comparable markets and then re-validated using trade signals and interview feedback.

Data Validation & Update Cycle

Outputs are validated through several checks so the final number is not dependent on any single assumption. Model results are compared against independent signals like trade direction, capacity changes, and price trend logic, and then variance items are reviewed and resolved before sign-off.

A second analyst review is done to re-check unit consistency, currency conversions, and any unusual year-on-year jumps, followed by targeted re-contact of experts when a number falls outside expected ranges. The report is refreshed annually, and interim updates are made when material events occur, such as major capacity startups, policy changes affecting plastics, or sharp feedstock moves. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Metallocene Polyethylene Market Size Compared With Other Published Estimates

Published market sizes for metallocene polyethylene can vary widely, even when the market name looks the same, because the scope and valuation steps behind the number are not identical. Differences usually come from what is counted as mPE, which end uses are included, and whether pricing and demand are tied back to observable market signals.

Trade-flow direction, announced capacity additions, and the implied mPE price premium seen in packaging film checks are the evidence points that anchor Mordor Intelligence s 2026 market value, because mPE revenue is counted only where adoption is validated by these signals and supported by converter-side feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 23.87 B (2026) | |

| Industry Data Publisher A | USD 8.23 B (2024) | Uses an earlier base year and appears to capture a narrower set of mPE revenue streams, so the total stays closer to selected product types and channels and reflects lower pricing levels than later-year valuation. |

| Global Research Publisher B | USD 8.33 B (2024) | Publishes a lower 2024 starting point that likely undercounts mPE supplied into film and packaging conversion in some regions, and it does not clearly show how adoption and premiums were cross-checked against capacity additions and trade signals. |

The spread in the table is mainly explained by the year used for valuation and by how tightly the scope is limited to verified mPE demand pools, followed by how regional premiums are applied. Our build stays repeatable by linking the demand base, penetration, and price movement to visible indicators, and then confirming the implied totals with targeted cross-checks before forecasting forward.

Key Questions Answered in the Report

What is the current market value of metallocene polyethylene?

The Metallocene polyethylene market size stands at USD 23.87 billion in 2026 and is forecast to reach USD 29.85 billion by 2031.

Which region leads global consumption?

Asia-Pacific dominates with 45.83% share, while North America is projected to grow the fastest at a 5.63% CAGR through 2031 thanks to ethylene capacity builds and packaging demand.

Why is mLLDPE the largest product type?

MLLDPE offers high puncture resistance and clarity, enabling 15-20% gauge reduction which drives a 58.62% share of global volume.

How are sustainability trends influencing the market?

Brand owners demand recyclable, down-gauged films and advanced recycling. Technologies like Exxtend molecular recycling convert waste back into feedstock suitable for food-grade polyethylene.

Page last updated on: