Market Overview

| Study Period | 2020 - 2031 |

|---|---|

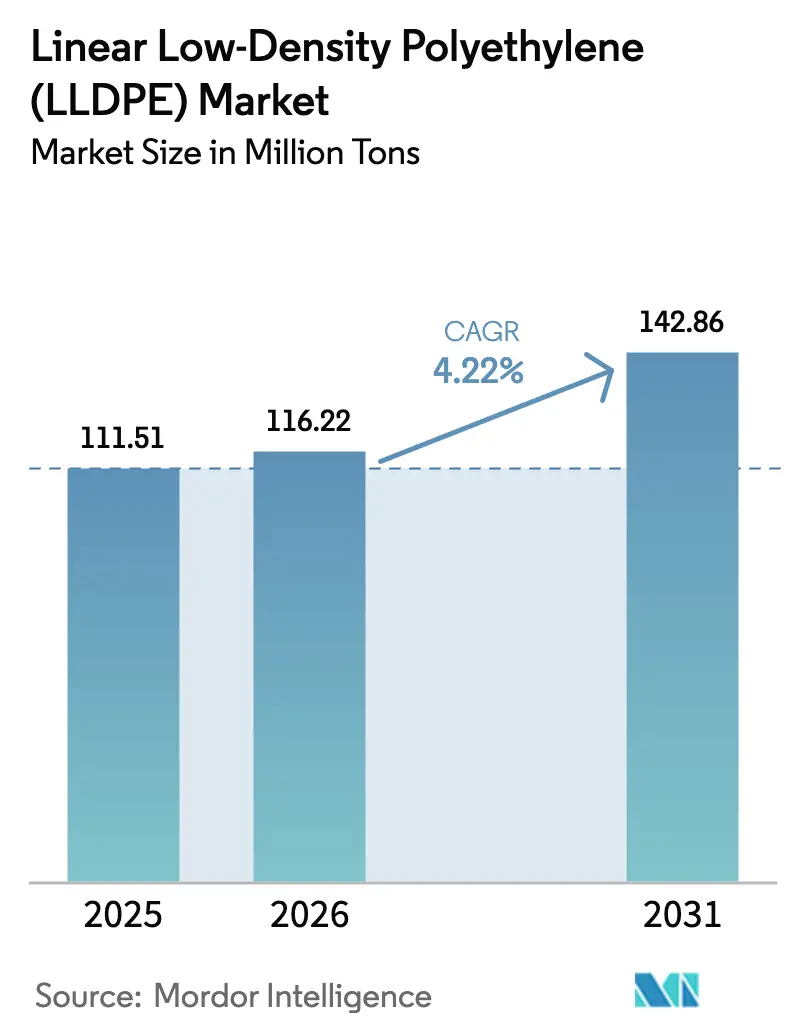

| Market Volume (2026) | 116.22 Million tons |

| Market Volume (2031) | 142.86 Million tons |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

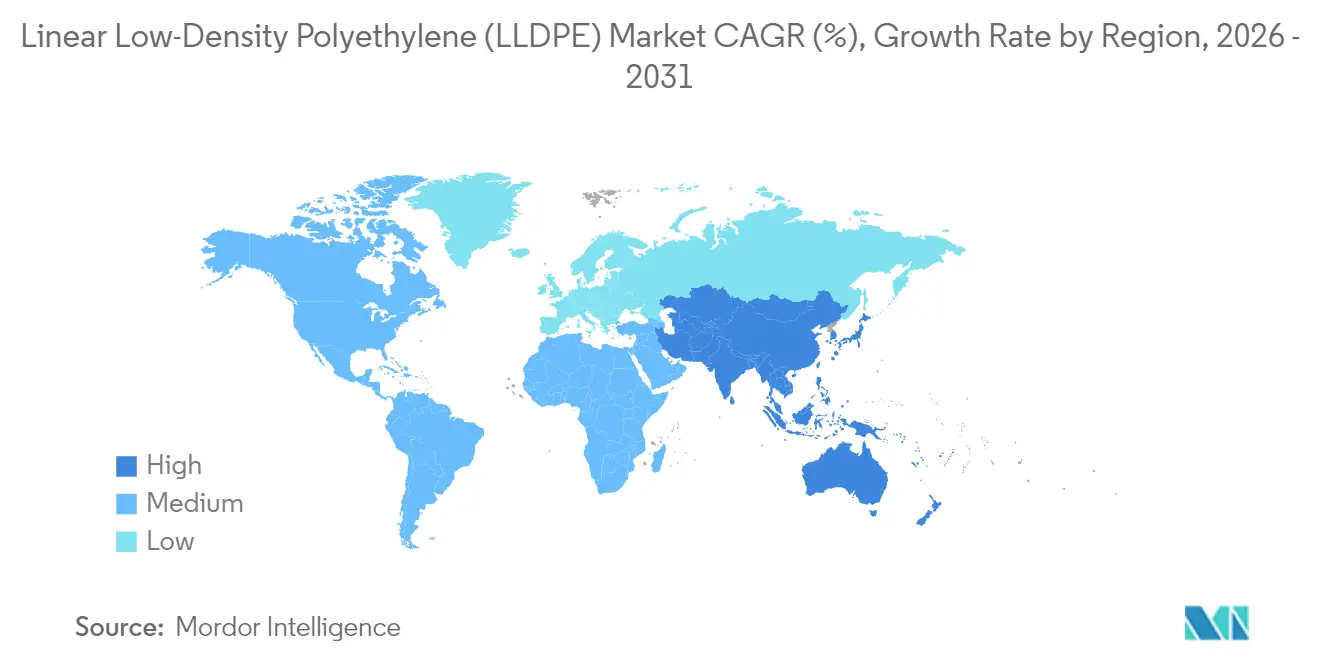

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Linear Low-Density Polyethylene (LLDPE) Market Analysis by Mordor Intelligence

The Linear Low-Density Polyethylene Market size was valued at 111.51 million tons in 2025 and estimated to grow from 116.22 million tons in 2026 to reach 142.86 million tons by 2031, at a CAGR of 4.22% during the forecast period (2026-2031). Packaging downgauging, e-commerce logistics, and capacity expansions in the Asia-Pacific region are the structural forces sustaining long-term demand. Even as North American and European utilization rates hover near 80%, Asia-Pacific producers continue to operate newer assets at rates above 90% and are redirecting surplus resin toward Southeast Asia and Africa, thereby reshaping trade patterns. Cost competition is intensifying because US ethane prices remain low, while Asian naphtha costs have risen, compressing margins for integrated crackers. Meanwhile, sustainability mandates are driving converters toward mono-material film structures that favor LLDPE and higher-recycle-content grades, prompting investment in advanced recycling assets. Volatility in feedstock pricing and regulatory divergence across regions create both risks and opportunities for players positioned with flexible feedstock slates and differentiated catalyst portfolios.

Key Report Takeaways

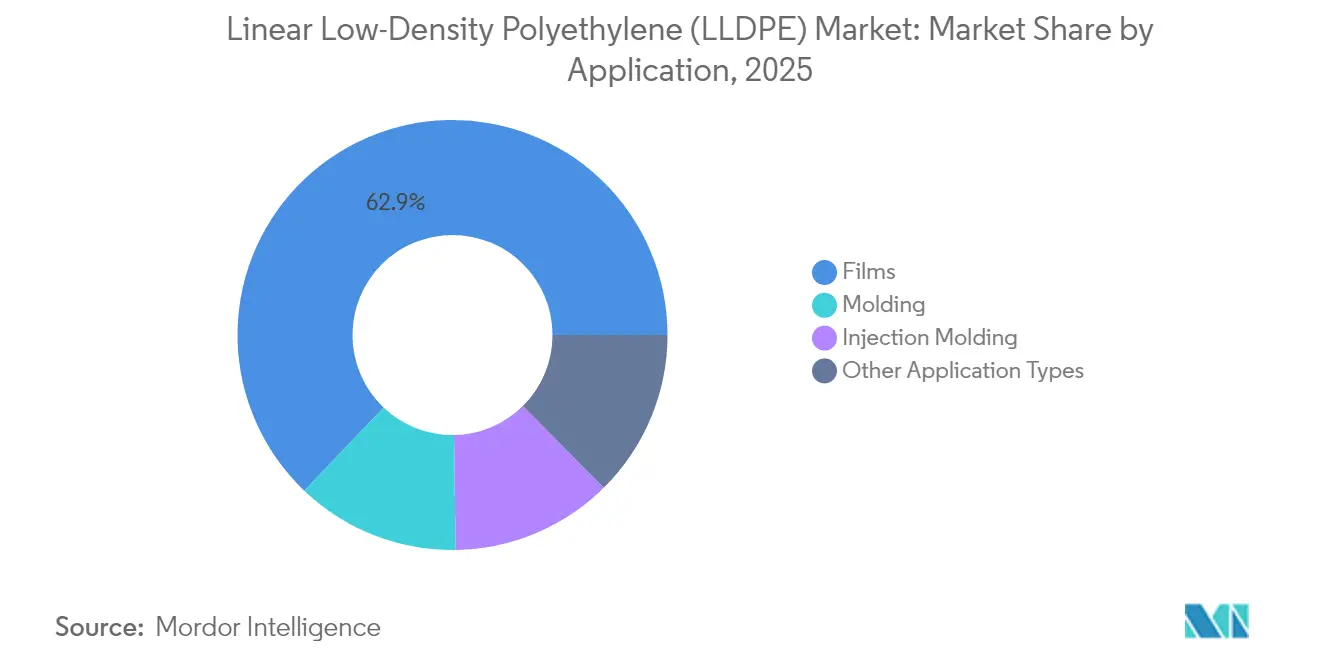

- By application, films commanded 62.89% of the Linear Low-Density Polyethylene market share in 2025, and other application types are forecast to register the fastest 5.68% CAGR between 2026 and 2031.

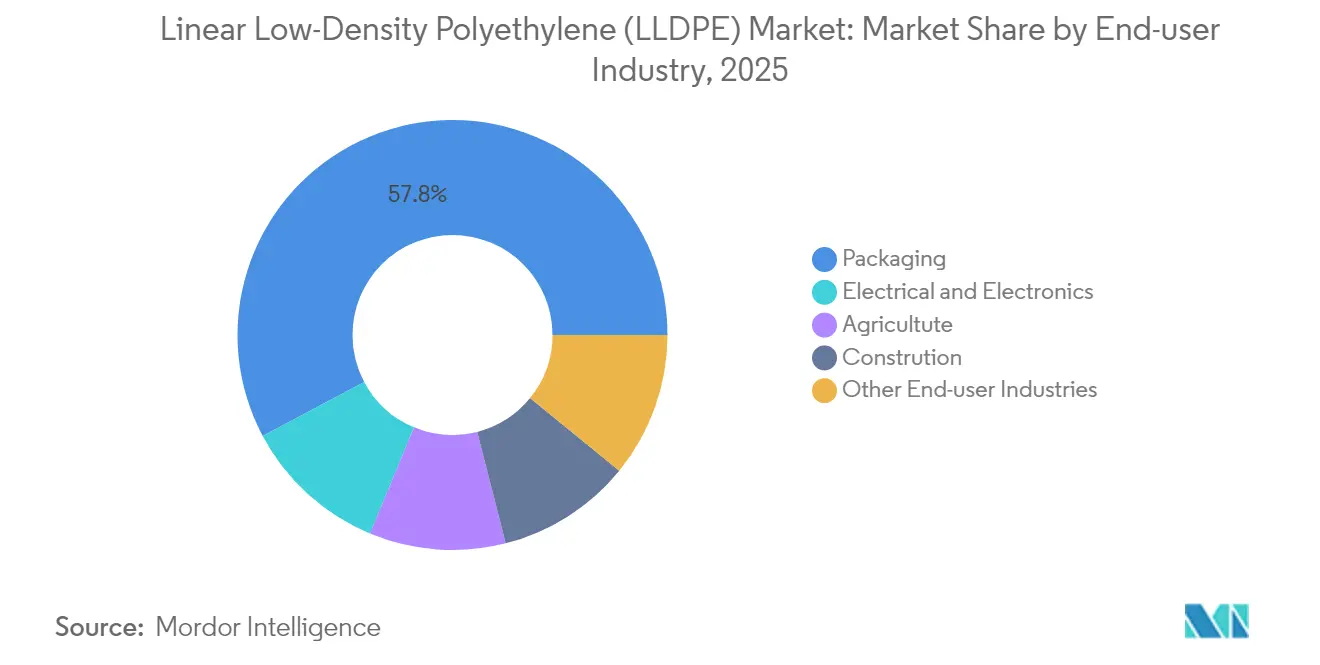

- By end-user industry, packaging accounted for 57.78% of the Linear Low-Density Polyethylene market size in 2025, while electrical and electronics is poised to grow the quickest at a 5.61% CAGR.

- By geography, the Asia-Pacific region led with 46.10% of the global volume in 2025. The Asia-Pacific region is anticipated to deliver the highest CAGR of 5.07% from 2021 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Linear Low-Density Polyethylene (LLDPE) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating packaged-food film demand | +0.9% | Global, led by Asia-Pacific and North America | Medium term (2–4 years) |

| E-commerce stretch-/shrink-film surge | +1.1% | Global, concentrated in Asia-Pacific, North America | Short term (≤ 2 years) |

| Solar-panel encapsulation film uptake | +0.3% | Asia-Pacific core, spill-over to Middle East-Africa | Long term (≥ 4 years) |

| Downgauging and circular-economy mandates | +0.8% | Europe, North America, early adoption in Asia-Pacific | Medium term (2–4 years) |

| Agricultural mulch and greenhouse films | +0.6% | Asia-Pacific, Middle East-Africa, South America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Packaged-Food Film Demand

Flexible snack and ready-meal packaging is shifting from rigid to lightweight pouches, trimming resin use by nearly 90% while preserving seal integrity through metallocene-enabled downgauging[1]LyondellBasell, “Flexible Packaging Film Trends,” lyondellbasell.com. ExxonMobil’s Exceed XP 7 grade introduced in 2024 delivers dart-impact values of 900 g and puncture energy reaching 2.3 J per mil at densities near 0.912 g/cc, allowing converters to thin film gauges by 15%–20% without sacrificing barrier performance. The performance leap is crucial in India, where polyethylene demand increased by 20% year-over-year in 2024 and landfill space is limited. Stand-up pouch adoption favors LLDPE over LDPE because short-chain branching supplies superior hot-tack strength for high-speed form-fill-seal lines. As middle-class food spending rises throughout Asia, brand owners view LLDPE’s downgauging capability as the primary lever for both cost and sustainability goals.

E-commerce Stretch-/Shrink-Film Surge

Global online retail continues to outpace GDP, driving the need for enhanced pallet-wrap and parcel-protection specifications. Stretch film incorporating metallocene LLDPE maximizes cling and puncture resistance, addressing load-stability demands that outweigh direct material costs. LyondellBasell’s 2023 venture with AFA Nord aims to produce 50,000 t/y of recycled LLDPE and LDPE flexible packaging by 2026, in line with extended producer responsibility rules. Although Northeast Asian cracker margins turned negative in late 2024, stretch-film consumption showed resilience due to its near-perfect correlation with parcel volumes. Retailers are also migrating from PVC to LLDPE blends for beverage and electronics shrink-bundling to eliminate chlorinated polymers and improve recycling yields.

Solar-Panel Encapsulation Film Uptake

Bifacial photovoltaic modules require white-pigmented backsheets to enhance albedo, and LLDPE offers the necessary moisture resistance and cost benefits for this emerging specification. A 1,500 GW utility-scale solar pipeline slated for commissioning between 2025 and 2030 across Asia-Pacific and the Middle East creates a multiyear runway for encapsulation films[2]International Energy Agency, “Oil 2024,” iea.org. LLDPE’s lower processing temperature compared with EVA curtails lamination energy, aligning with module makers’ carbon-reduction targets. However, strict IEC 61215 durability tests and entrenched supplier relationships temper near-term volume gains.

Downgauging and Circular-Economy Mandates

European single-use plastics rules, fully enforced since 2024, push converters toward mono-material LLDPE films that meet design-for-recycling criteria. Dow’s Path2Zero program pledges 2 million tons per year of low-carbon polyethylene and 3 million tons per year of recycled or renewable resins by 2030, underpinned by more than USD 1 billion in capital spending. PFAS-free processing aids launched in July 2024 enable gauge uniformity below 20 µm without melt fracture, resulting in up to 12% reduction in trimming resin use. Mechanical recycling studies show that LLDPE retains functionality through two cycles but loses 85% of its tear strength by the fourth cycle, underscoring the future importance of chemical depolymerization pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward m-LLDPE/HDPE for strength | -0.7% | Global, notably North America and Europe | Medium term (2–4 years) |

| Volatile naphtha/ethane feedstock cost | -0.9% | Asia-Pacific and Middle East-Africa (naphtha), North America (ethane) | Short term (≤ 2 years) |

| Global single-use-plastic restrictions | -0.5% | Europe, North America, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward m-LLDPE/HDPE for Strength

Metallocene LLDPE and HDPE command 10%–15% price premiums by delivering higher puncture resistance and stiffness, displacing conventional grades in heavy-duty sacks and industrial liners. ExxonMobil’s data show that C6-metallocene LLDPE provides narrower molecular-weight distributions, which lower seal-initiation temperatures and reduce trim waste on high-speed lines. HDPE’s superior environmental stress-crack resistance favors chemical containers and IBCs, drawing share away from LLDPE in North America and Europe where converters can reconfigure equipment. Emerging markets with legacy extruders remain cost-sensitive, slowing the substitution effect.

Volatile Naphtha/Ethane Feedstock Cost

Asian naphtha-based crackers faced a 15%–20% increase in feedstock costs in early 2025, forcing producers to curb operating rates and eroding petrochemical margins. In contrast, US ethane prices softened on associated-gas oversupply, widening a USD 200–USD 300/t cash-cost gap versus Northeast Asia. The divergence complicates long-term contracts and drives a shift toward shorter pricing cycles, straining working-capital efficiency for integrated producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Films Anchor Volume, Specialty Segments Accelerate

Films represented 62.89% of the global volume in 2025, as converters favored metallocene grades that enabled thinner gauges without compromising seal integrity. Metallocene catalyst systems provide enhanced hot-tack strength, enabling multilayer stand-up pouches to operate at higher line speeds and reduce total material consumption per package. Stretch-film producers are adopting pre-stretched rolls that reduce resin usage per pallet by up to 50%, further integrating LLDPE into supply-chain sustainability programs. Specialty shrink-film adoption in electronics bundling is advancing as PVC falls out of favor due to chlorine-related disposal liabilities.

Other application types are forecast to grow at a market-leading 5.68% CAGR through 2031. The Linear Low-Density Polyethylene market share of these specialty applications remains modest, yet the value proposition is rising. Rotomolded water tanks are gaining traction in off-grid African communities, leveraging LLDPE’s one-piece construction that eliminates leak points. Ultralight protective foams for consumer electronics packaging are another emerging outlet, supported by a method reported in Nature for producing ultrathin polyethylene sheets that preserve flexibility at micro-scale thicknesses. Semiconductor logistics are stimulating demand for antistatic films, a niche that benefits from LLDPE’s inherently low surface resistivity when compounded with conductive additives.

By End-User Industry: Packaging Dominates, Electronics Surges

Packaging accounted for 57.78% of global demand in 2025 and continues to dictate price cycles, as film converters typically carry limited inventory. Brand-owner commitments to cut virgin resin usage by 20%–25% by 2030 are spurring accelerated downgauging, which paradoxically maintains LLDPE volume by opening new applications that replace rigid formats. A visible shift from multi-material laminates toward mono-material polyethylene pouches improves mechanical recyclability, a change that favors LLDPE due to its melt-strength characteristics.

Electrical and electronics is the fastest-growing end-use at a 5.61% CAGR. Antistatic and moisture-barrier films protect high-value wafers during global transit, and any defect can destroy semiconductor lots valued at USD 10,000 or more, justifying the use of premium metallocene LLDPE grades. Agriculture remains an essential yet regionally varied outlet, relying on mulch and greenhouse films to amplify yields in water-scarce regions. Construction continues to employ LLDPE for vapor barriers and geomembranes, benefiting from its puncture resistance and ease of installation. Healthcare is an emerging specialty, where single-use medical pouches leveraging LLDPE’s toughness are gaining approval under ISO 13485 frameworks, especially in Southeast Asia’s fast-growing hospital markets.

Geography Analysis

The Asia-Pacific region accounted for 46.10% of the global 2025 volume and is expected to deliver a 5.07% CAGR through 2031. China’s commissioning of 5 million tonnes per year (t/y) of polyethylene capacity in 2025 and 6.5 million t/y in 2026 will narrow its import requirement to an average of 300,000 t/y, redirecting Middle Eastern and US cargoes toward Indonesia, Vietnam, and the Philippines. India is expected to bring 2.4 million tonnes per year online over the next three years, driven by 7% annual growth in petrochemical demand and an expanded virtual ethane pipeline that secures feedstock for Jamnagar. Japan and South Korea, while mature, are upgrading catalyst technology to serve agricultural-film niches and to hedge against naphtha volatility by integrating imported ethane.

North America remains a swing supplier thanks to ethane-based cost advantages. Borealis started up its 640,000 t/y Baystar unit and gained rapid access to Gulf export terminals. ExxonMobil continues to evaluate a USD 8.6 billion complex in Point Comfort, yet the company shuttered its 400,000 tonnes per year Gravenchon line in France, highlighting the continental divergence in feedstock economics. Mexico’s re-export role is expanding under USMCA, while Canada’s growth is capped by permitting hurdles for greenfield petrochemical sites in Alberta and Ontario. Europe is contracting capacity amid high energy costs and stringent environmental rules. SABIC closed its 400,000 t/y Geleen cracker, and LyondellBasell is exploring USD 7–9 billion in asset divestitures to focus on recycling and bio-based resins. Nonetheless, the region leads circular-economy innovation; LyondellBasell’s flexible-packaging recycling venture targets 50,000 t/y by 2026, positioning Europe as a technology hub for chemical recycling. South America and the Middle East-Africa represent growth frontiers. Braskem is negotiating gas supply to expand its Rio complex beyond 540,000 t/y, while Borealis’s 1.4 million t/y polyethylene project in Abu Dhabi is more than halfway to mechanical completion, assuring low-cost supply to Asian and African converters.

Competitive Landscape

The Linear Low-Density Polyethylene (LLDPE) Market is moderately concentrated. State-owned enterprises, such as SINOPEC and Reliance Industries, leverage integrated feedstock chains and local distribution to sustain high utilization rates. In contrast, privately held and publicly traded majors in North America and Europe face margin pressure as naphtha prices rise and as regulatory costs mount. Strategic bifurcation is evident: Middle Eastern and US Gulf Coast players are scaling ethane-based assets to capture export share, while European incumbents focus on recycled-content and bio-based portfolios to align with circular economy mandates.

Linear Low-Density Polyethylene (LLDPE) Industry Leaders

Dow

Exxon Mobil Corporation

LyondellBasell Industries Holdings B.V.

SABIC

INEOS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Directorate General of Trade Remedies, under the Ministry of Commerce and Industry, initiated an anti-dumping investigation into imports of Linear Low-Density Polyethylene (LLDPE) from six countries: Kuwait, Malaysia, Oman, Qatar, Saudi Arabia, and the United Arab Emirates.

- March 2025: Borealis GmbH unveiled Borcycle M CWT120CL, a recycled linear low-density polyethylene (rLLDPE) aimed at promoting circularity in non-food flexible packaging. It is crafted from 85% post-consumer recyclate (PCR) and a 15% LLDPE booster.

Global Linear Low-Density Polyethylene (LLDPE) Market Report Scope

Linear low-density polyethylene (LLDPE) is a thermoplastic polymer and is a class of polymers derived primarily from petrochemicals. Linear low-density polyethylene exhibits high tensile strength, flexibility, and puncture resistance compared to other similar chemical products. Linear low-density polyethylene (LLPDE) is a blended form of low-density polyethylene (LDPE). LLDPE is more robust than LDPE because of its side chains

The linear low-density polyethylene market is segmented by application, end-user industry, and geography. By application, the market is segmented into films, injection molding, molding, and other application types. By end-user industry, the market is segmented into agriculture, electrical and electronics, packaging, construction, and others. The report also covers the market size and forecasts for 16 countries across major regions. For each segment, market sizing and forecasts have been conducted based on volume (million tons).

By Application

| Films |

| Molding |

| Injection Molding |

| Other Application Types |

By End-user Industry

| Agricultute |

| Electrical and Electronics |

| Packaging |

| Constrution |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Films | |

| Molding | ||

| Injection Molding | ||

| Other Application Types | ||

| By End-user Industry | Agricultute | |

| Electrical and Electronics | ||

| Packaging | ||

| Constrution | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the Linear Low-Density Polyethylene market in 2026 and how fast is it growing?

The market stands at 116.22 million tons in 2026 and is set to expand to 142.86 million tons by 2031 at a 4.22% CAGR.

Which application holds the dominant share of global LLDPE demand?

Films command 62.89% of 2025 volume, driven by stretch, shrink, and food-packaging uses.

Which end-use sector is expected to grow the quickest through 2031?

Electrical and electronics is projected to grow at 5.61% CAGR thanks to demand for antistatic and moisture-barrier films.

Which region leads global consumption and why?

Asia-Pacific accounts for 46.10% of 2025 volume, supported by rapid capacity additions in China and robust demand growth in India and Southeast Asia.

What key factor is squeezing producer margins in 2025?

Divergent feedstock costs—rising naphtha prices in Asia versus weak ethane prices in North America—are compressing integrated-cracker margins.

Page last updated on: