Market Overview

| Study Period | 2021 - 2031 |

|---|---|

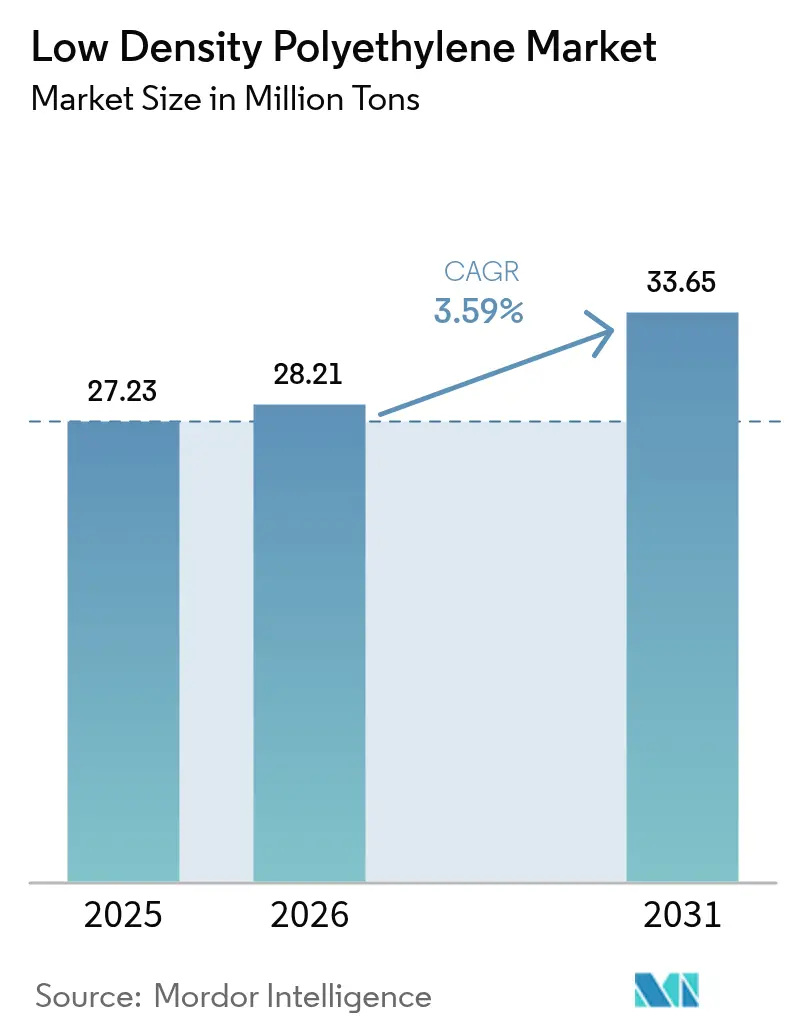

| Market Volume (2026) | 28.21 Million tons |

| Market Volume (2031) | 33.65 Million tons |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Density Polyethylene Market Analysis by Mordor Intelligence

The Low Density Polyethylene Market size is projected to expand from 27.23 million tons in 2025 and 28.21 million tons in 2026 to 33.65 million tons by 2031, registering a CAGR of 3.59% between 2026 to 2031. Robust demand from e-commerce mailers, sterile healthcare vials, and renewable-energy cable insulation is counterbalanced by linear low-density polyethylene (LLDPE) substitution in stretch film and tightening European rules on mono-layer flexible packaging. Producers are prioritizing backward integration into advantaged ethane or bio-naphtha feedstocks as well as advanced mechanical and chemical recycling pathways that allow premium-priced circular grades. Film applications still dominate, but wire and cable insulation now capture investors’ attention because 5G backhaul, electric-vehicle charging, and utility-scale solar farms require LDPE’s dielectric strength above 20 kV/mm. Regionally, Asia-Pacific retains a structural cost edge thanks to new high-pressure reactors in China, while North American crackers benefit from low-cost shale ethane, and Europe faces permanent capacity rationalization.

Key Report Takeaways

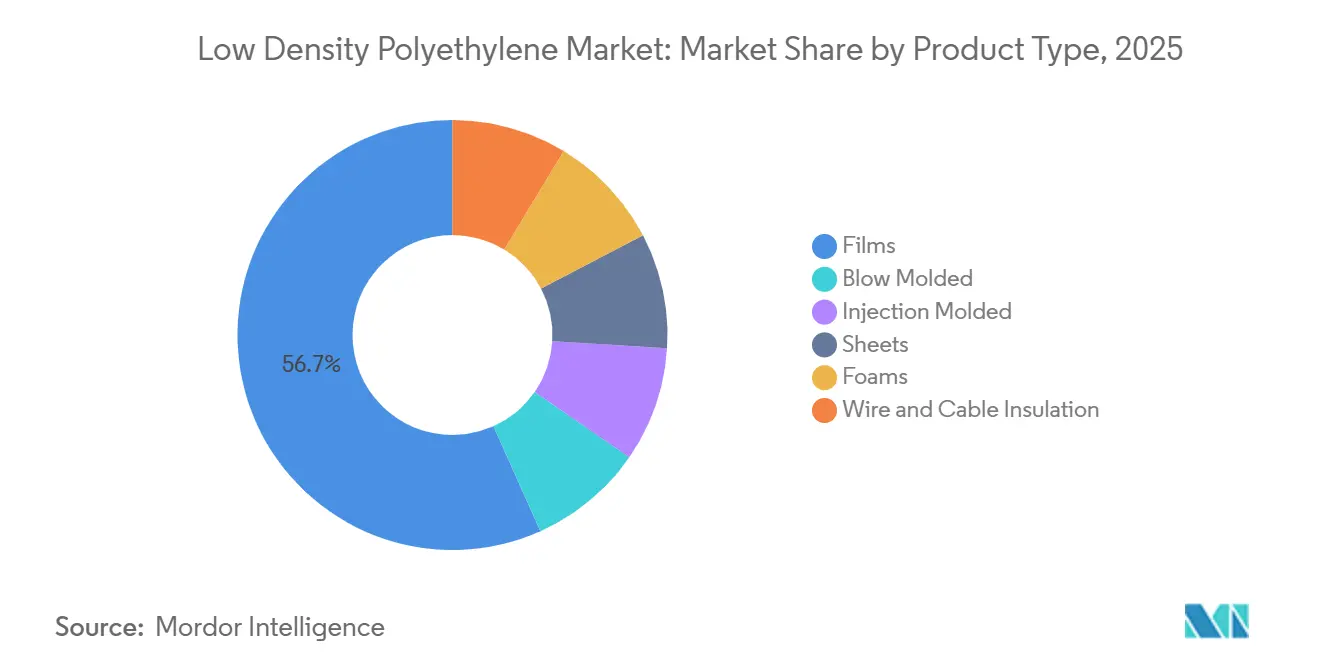

- By product type, films led with 56.71% of low density polyethylene market share in 2025. Wire and cable insulation is projected to expand at a 4.14% CAGR through 2031, the fastest product-type growth.

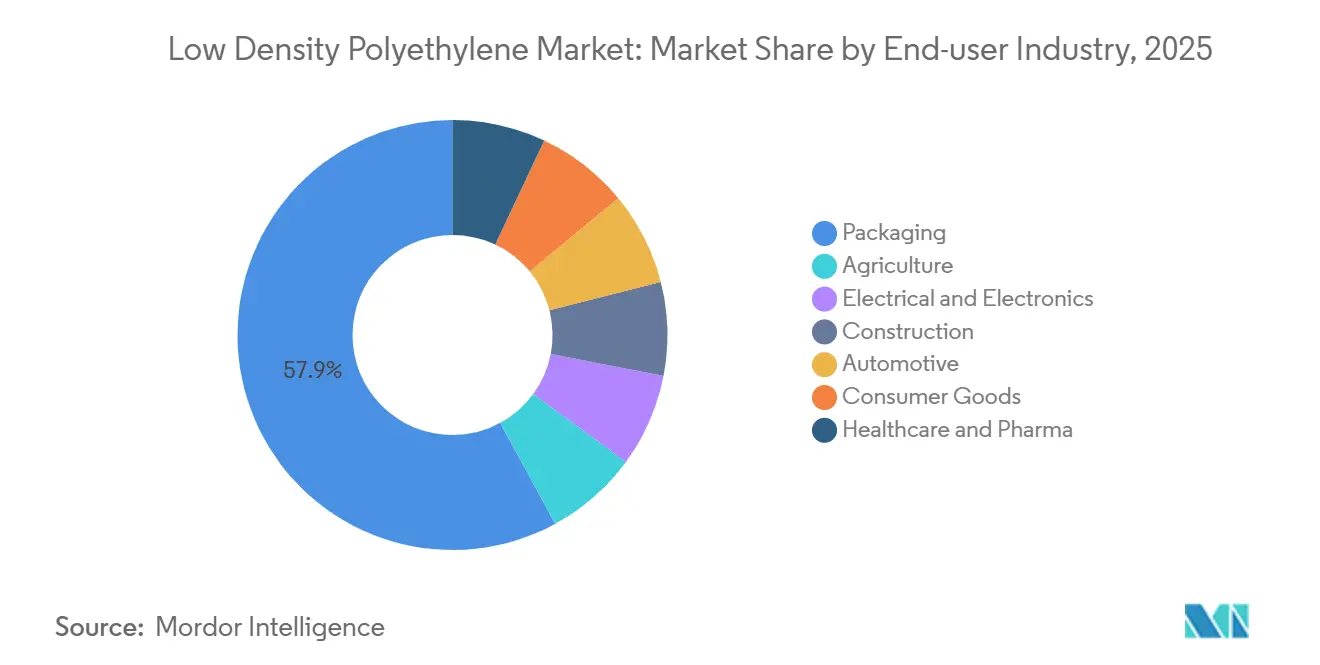

- By end-user industry, packaging accounted for a 57.93% share of the low density polyethylene market size in 2025. Healthcare and pharmaceuticals record the highest expected CAGR at 4.12% through 203.

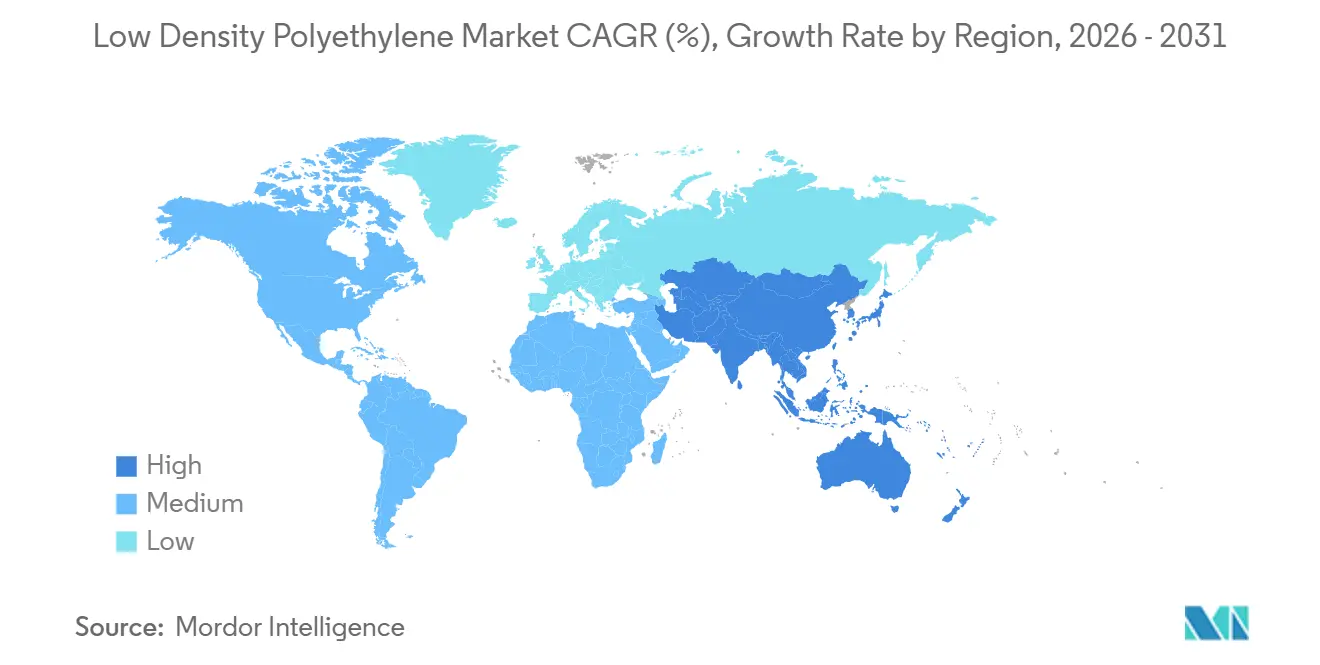

- By geography, Asia-Pacific accounted for 47.36% share of the low density polyethylene market in 2025 and is anticipated to expand with a 4.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Low Density Polyethylene Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in e-commerce flexible packaging | +0.9% | Global, with concentration in North America, China, India | Medium term (2-4 years) |

| Rising demand for agricultural films | +0.7% | APAC (India, China, Vietnam, Thailand), Middle East, Latin America | Long term (≥ 4 years) |

| Preference for extrusion-coated applications | +0.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Solar-panel encapsulant film uptake | +0.6% | APAC (China, India), Europe, North America | Long term (≥ 4 years) |

| Advanced recycling enabling premium LDPE grades | +0.4% | Europe, North America, early adoption in Japan and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in E-Commerce Flexible Packaging

Parcel volumes rose 18% in 2025 as Amazon, Alibaba, and regional platforms adopted mono-material LDPE mailers that satisfy extended-producer-responsibility rules in California, France, and Germany. LDPE seals at 105-115 °C, enabling pouch lines above 200 m/min—25% faster than polypropylene laminates that require corona treatment. Converters in India and Vietnam merged 15% post-consumer resin into 30-40 µm blown films to meet July 2024 plastic-waste mandates, generating a USD 150/ton premium for certified feedstock. Dow’s INNATE resin, launched Q2 2025, lets brands down-gauge films by 20% yet keep 400 g dart-drop impact, cutting scope-3 emissions. Curbside-recyclable structures are therefore expanding the low density polyethylene market at the expense of multi-layer laminates lacking viable end-of-life pathways.

Rising Demand for Agricultural Films

Protected-agriculture acreage climbed 12% in India and 9% in Vietnam during 2024-2025, incentivized by subsidies that require UV-stabilized LDPE with a 3-5 year service life. LDPE transmits 400-600 nm light, optimizing photosynthetically active radiation for tomatoes and capsicums while flexing under 40 °C tropical swings[1]Food & Agriculture Organization, “Protected Cultivation in Asia,” fao.org. China consumed nearly 1.4 million tons of mulch film in 2025, 60% of it LDPE, because linear grades tear at 25 N/mm². Braskem’s October 2025 bio-based grade targets European organic farms and biodegrades 98% within 18 months under composting conditions. Silage-wrap demand grew 7% in New Zealand, Ireland, and Argentina as dairies shifted from baled hay to anaerobic ensiling, relying on LDPE’s oxygen-barrier to curb spoilage.

Preference for Extrusion-Coated Applications

Cartonboard suppliers specified 15-20 g/m² LDPE coatings to displace PET laminations for repulpable liquid packaging. LDPE’s 6-8 g/10 min melt index runs at greater than 400 m/min, 30% faster than HDPE, which risks board scorching at 280 °C[2]Dow Inc., “INNATE Precision Packaging Resins,” dow.com. By late 2025, 40% of European aseptic-carton lines will be converted to LDPE-coated substrates, trimming package carbon footprints 25% while preserving a six-month UHT-milk shelf life. The FDA reaffirmed LDPE coatings’ food-contact compliance in March 2025, provided residual catalysts stay below 10 ppm. Growth in frozen-food barrier paper, up 14% during 2025, further boosts the low density polyethylene market because LDPE’s 1.2 g/m²/24 h MVTR halts ice-crystal formation.

Solar-Panel Encapsulant Film Uptake

Global photovoltaic output hit 600 GW in 2025, with LDPE-EVA co-polymer encapsulants in 85% of modules. LDPE’s resistivity above 10¹⁴ Ω-cm averts potential-induced degradation in 1,500 V systems, increasingly standard for utility solar farms. Hanwha raised film capacity by 30 kt/yr in Q3 2025, targeting Middle-East installations where greater than 50 °C ambients demand sub-100 °C glass-transition polymers. Polyolefin-elastomer blends gained share because they eliminate EVA’s acetic-acid off-gassing that corrodes junction boxes. Chinese imports of encapsulant film dropped 22% as local producers added 180 kt of annual lines.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from LLDPE and HDPE | -0.8% | Global, particularly in North America and Europe for packaging films | Short term (≤ 2 years) |

| Ethylene feedstock price volatility | -0.5% | Global, with acute impact in Europe and Northeast Asia (naphtha-based) | Short term (≤ 2 years) |

| European Union bans on mono-layer polyolefin films | -0.3% | Europe, with spillover influence on export-oriented converters in Turkey and North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from LLDPE and HDPE

Between 2020 and 2025, LLDPE captured 12 percentage points of stretch-film volume by enabling converters to down-gauge from 23 µm to 17 µm without puncture-resistance loss. LDPE still offers 400-500 g dart-drop impact for frozen-food applications, yet its USD 150/ton Q4 2025 premium pushed cost-sensitive buyers toward LLDPE. HDPE substitution accelerated in blow-molded bottles, where stress-crack resistance outperforms LDPE by 50%. Chevron Phillips Chemical’s 2024 MARLEX bimodal HDPE mimics LDPE processability, allowing pallet makers to phase out LDPE caps and crates. Consequently, high-pressure LDPE reactors operated below 70% utilization in 2025 versus greater than 80% for LLDPE lines.

Ethylene Feedstock Price Volatility

European ethylene contracts jumped from EUR 850/t in January to EUR 1,150/t by June 2025 as cracker outages met 30% costlier naphtha. High-pressure LDPE consumes 1.02-1.05 t of ethylene per ton of polymer, slashing Q2 2025 margins to USD 80-120/t—below the USD 150/t cash-cost threshold, prompting Versalis to close Italian units. North American ethane crackers retained USD 200-250/t advantages, but Mont Belvieu spot ethane spiked 35% in August 2025 as LNG export terminals siphoned feedstock. Chinese coal-to-olefins plants faced breakeven pressures above USD 85/bbl Brent, causing spot tightness that lifted Asian LDPE prices 12% in September 2025. CME futures show 28% implied volatility for 2026 delivery, double pre-pandemic averages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wire Insulation Outpaces Film Maturity

Films kept 56.71% of the 2025 volume but anticipated grow with a relatively low growth rate as LLDPE and HDPE encroached on stretch-film and rigid-container niches. The low density polyethylene market size for wire and cable is projected to expand at 4.14% CAGR between 2026-2031, while films hold a dominant yet maturing footprint. Borealis debuted LDPE 2426H in March 2025 for 400 kV cables, offering water-tree retardance greater than 10,000 h.

Injection molding (caps and closures) is witnessing growth propelled by pharmaceutical vial demand needing USP Class VI compliance. Blow-molded containers are growing as HDPE’s rigidity supports e-commerce logistics. Nevertheless, the low density polyethylene market remains resilient because emerging subsea-cable, data-center, and high-voltage applications offset mature film demand.

By End-User Industry: Healthcare Leads Growth Trajectory

Healthcare and pharmaceuticals will advance at 4.12% through 2031, the fastest end-use, as blow-fill-seal lines require extractables less than 5 ppm and endotoxin levels less than 0.25 EU/mL. Packaging still commands 57.93% of low density polyethylene market share in 2025 yet grows at a relatively low CAGR because of LLDPE stretch-wrap gains and HDPE rigid-packaging substitution. Agriculture demand is driven by subsidies for greenhouse and mulch films, while electrical and electronics are climbing on 5G rollouts.

The low-density polyethylene market size tied to healthcare vials and IV bags is set to grow faster than any other end-use at 4.12% CAGR between 2026-2031. LyondellBasell’s Purell PE 1840H extends saline bag shelf life to 24 months, cutting hospital inventory costs by 18%. Meanwhile, extended-producer-responsibility fees in California, France, and Japan pressure branded packaging to migrate to recyclable paper mailers, trimming LDPE demand. Even so, LDPE retains advantages in clarity and freeze-thaw performance needed for biologics shipments.

Geography Analysis

Asia-Pacific captured 47.36% of 2025 volume and will grow at 4.47% through 2031, propelled by China’s 8.2 million tons of new LDPE capacity commissioned 2025-2026 for greenhouse film and extrusion-coating demand. Southeast Asian plants ran at 91% utilization in late 2025 because global additions skewed to linear grades, leaving conventional LDPE in deficit outside China. India’s low density polyethylene market confronted below-cost Chinese imports, triggering an anti-dumping probe in November 2024. Japan and South Korea invested heavily in chemical recycling, targeting 200 kt capacity by 2028. Vietnam boosted imports 14% in 2025 as electronics assembly and greenhouse acreage expanded under state subsidies.

North America market demand is supported by shale-ethane cost advantages. No new LDPE units are slated in Chevron Phillips Chemical’s USD 8.5 billion Golden Triangle Polymers complex, tightening regional supply and underpinning premiums. Canada’s greenhouse-film demand lifted national LDPE use 4.2% in 2025. Mexico 's market is driven by near-shoring of wire-harness and medical-device manufacturing. California’s 30% PCR rule for 2030 has already raised mechanically recycled LDPE premiums to USD 180/ton.

Europe accounted for a significant market share in 2025 volume, but growing with modest CAGR because Versalis shuttered 400 kt of capacity and stringent PPWR rules ban non-recyclable mono-layer films from 2028. German demand slipped in 2025 as automotive output dropped 6% and converters pivoted to PET-based laminates to meet VerpackG targets. Repsol’s 300 kt LLDPE line at Sines underscores industry reluctance to invest in costly high-pressure LDPE units. Nordic growth is tied to data-center fiber and greenhouse films financed under EU rural-development funds. Turkey is acting as re-export hub for MENA markets despite lira depreciation.

South America and the Middle East-Africa together are witnessing a rising demand for low-density polyethylene due to rapidly growing industrialization in the regions. Brazil’s agricultural-film demand and Saudi ethane-based expansions keep the low density polyethylene market momentum intact.

Competitive Landscape

The low density polyethylene market is moderately consolidated. The top five players account for a significant market share, with regional incumbents such as Reliance Industries, PTT Global Chemical, and Hanwha Solutions reinforcing positions through captive downstream integration. Strategic thrusts cluster around feedstock integration—Braskem inked a long-term ethane deal with Petrobras for its USD 840 million Rio de Janeiro upgrade in October 2025—investment in pyrolysis and solvent-based recycling to satisfy Europe’s 30% PCR mandate, and research and development of specialty medical and photovoltaic grades that command USD 200-400/ton premiums.

Process innovation is reshaping cost curves. INEOS’s EP3894452 (June 2024) cuts compression energy by 18%, saving USD 25/ton. Dow’s WO2025012345 (January 2025) proposes gas-phase metallocene LDPE with long-chain branching at 30% lower capex. Regulatory fragmentation within the EU, where Italy counts chemical recycling in recycled-content metrics, and Austria does not, raises compliance overhead, favoring large converters able to secure multi-jurisdictional certifications. First movers in advanced recycling, such as LyondellBasell, with only 0.2% penetration yet exclusive municipal-waste contracts, could entrench feedstock access and block late entrants.

Low Density Polyethylene Industry Leaders

ExxonMobil Corporation

LyondellBasell Industries Holdings BV

Dow

SABIC

China Petrochemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Dow and Mura Technology partnered to scale hydrothermal liquefaction to 600 kt/yr of mixed plastic by 2030, achieving 90% mass yield.

- March 2025: Borealis launched LDPE 2426H for 400 kV extra-high-voltage cables featuring over 10,000 h water-tree retardance.

Global Low Density Polyethylene Market Report Scope

Low-density polyethylene (LDPE), a thermoplastic polymer, is predominantly sourced from petrochemical feedstock. LDPE can endure consistent temperatures of up to 80°C (176°F) for brief durations and can withstand temperatures reaching 90°C (194 °F). Known for its flexibility and toughness, LDPE can be manufactured in translucent and opaque variants.

The low-density polyethylene market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into blow molded, films, injection molded, sheets, foams, and wire and cable insulation. By end-user industry, the market is segmented into agriculture, electrical and electronics, packaging, construction, automotive, consumer goods, and healthcare and pharma. The report also includes the market size and forecasts for the low density polyethylene (LDPE) market in 27 countries across major regions. For each segment, the market sizing and forecast are in terms of volume (tons).

By Product Type

| Blow Molded |

| Films |

| Injection Molded |

| Sheets |

| Foams |

| Wire and Cable Insulation |

By End-user Industry

| Agriculture |

| Electrical and Electronics |

| Packaging |

| Construction |

| Automotive |

| Consumer Goods |

| Healthcare and Pharma |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Blow Molded | |

| Films | ||

| Injection Molded | ||

| Sheets | ||

| Foams | ||

| Wire and Cable Insulation | ||

| By End-user Industry | Agriculture | |

| Electrical and Electronics | ||

| Packaging | ||

| Construction | ||

| Automotive | ||

| Consumer Goods | ||

| Healthcare and Pharma | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is demand for LDPE wire and cable insulation growing?

The segment is forecast to expand at 4.14% CAGR through 2031 on the back of renewable-energy grids, 5G rollouts, and EV charging needs.

Which geographic region contributes the most to global LDPE consumption?

Asia-Pacific accounted for 47.36% of 2025 volume and is projected to lead growth at 4.47% CAGR.

What impact will EU packaging rules have on LDPE films?

The 2024 Packaging and Packaging Waste Regulation effectively bans non-recyclable mono-layer LDPE in 2028, pressuring 1.2 Mt of current demand to shift toward recyclable structures.

Why is healthcare the fastest-growing LDPE end-use?

Blow-fill-seal sterile packaging requires LDPE grades with ultra-low extractables and clarity, driving a forecast 4.12% CAGR to 2031.

How are producers addressing sustainability demands?

Leading suppliers invest in chemical recycling and bio-attributed feedstocks, enabling premium circular LDPE grades that attract USD 300-400/ton price uplifts while meeting 30% PCR mandates.

What is the current market size of Low Density Polyethylene Market?

The Low Density Polyethylene Market size is projected to expand from 27.23 million tons in 2025 and 28.21 million tons in 2026 to 33.65 million tons by 2031, registering a CAGR of 3.59% between 2026 to 2031.

Page last updated on: