United Kingdom Mortgage/Loan Broker Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

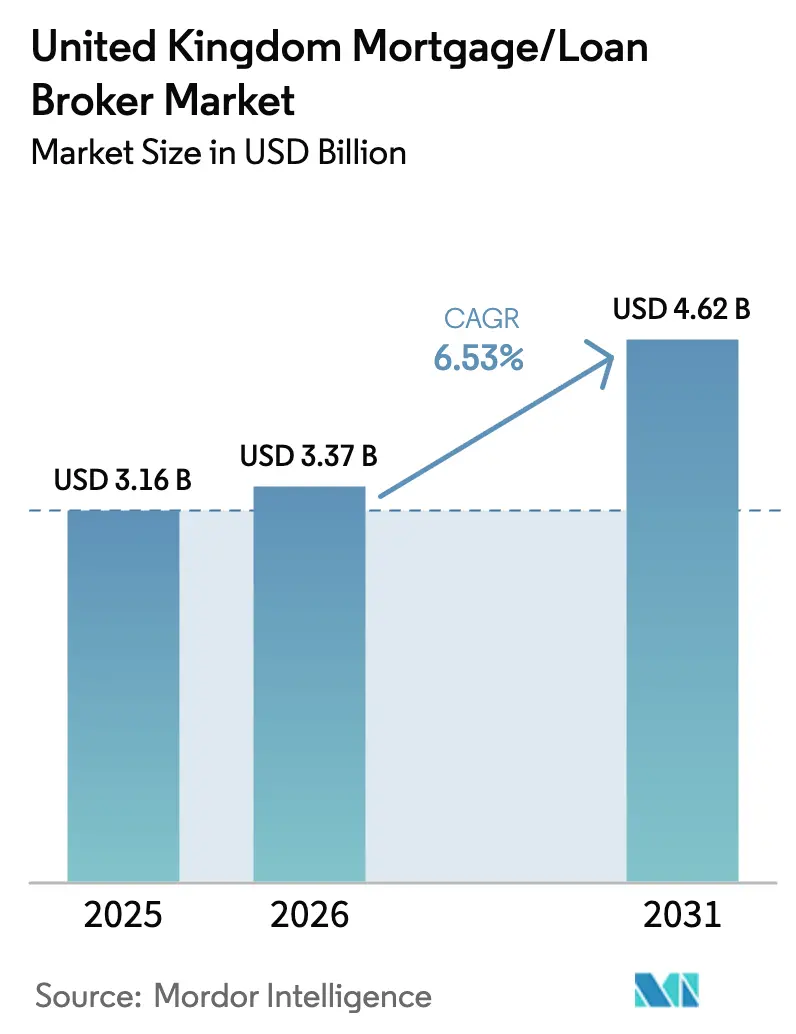

| Base Year Market Size (2025) | USD 3.16 Billion |

| Market Size (2026) | USD 3.37 Billion |

| Market Size (2031) | USD 4.62 Billion |

| Growth Rate (2026 - 2031) | 6.53% CAGR |

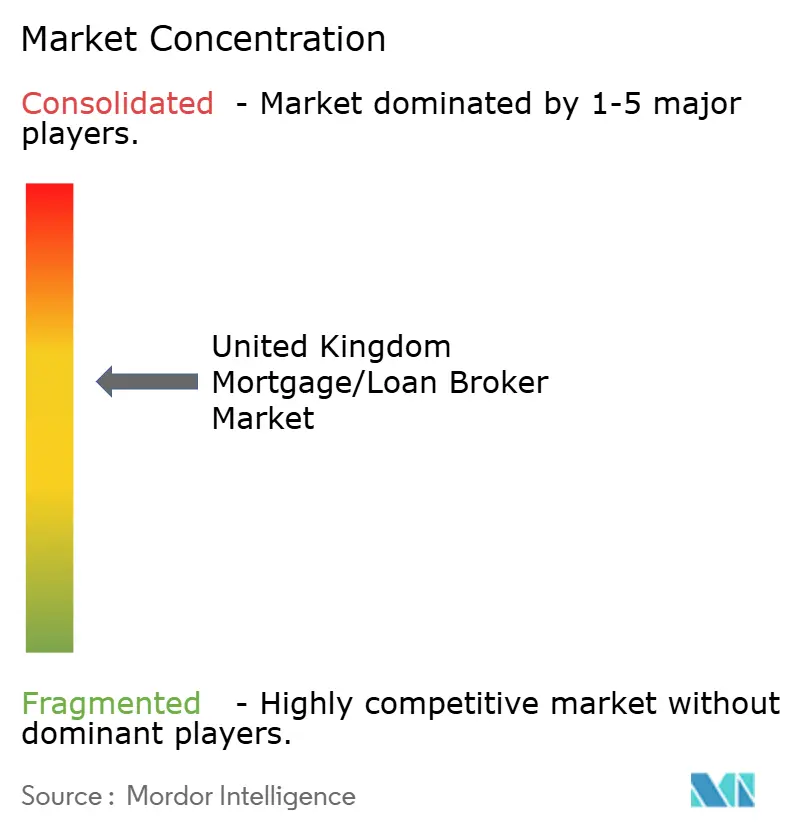

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Mortgage/Loan Broker Market Analysis by Mordor Intelligence

The United Kingdom Mortgage/Loan Broker Market size in 2026 is estimated at USD 3.37 billion, growing from 2025 value of USD 3.16 billion with 2031 projections showing USD 4.62 billion, growing at 6.53% CAGR over 2026-2031.

Technology-enabled onboarding, Consumer Duty compliance, and embedded-finance partnerships are enlarging the professional advice channel as borrowers seek tailored solutions across more than 200 active lenders. Hybrid service models that blend in-person guidance with digital convenience improve engagement and fuel repeat business, while scale economies allow large brokers to absorb compliance costs and negotiate superior procuration fees. Niche specialists capture complex cases—buy-to-let, self-employed, near-prime—where data-driven matching delivers high approval rates. Rising professional-indemnity premiums and a shortage of CeMAP-qualified advisers create capacity gaps, yet strategic automation and apprenticeship programs offset the drag, sustaining momentum in the United Kingdom mortgage broker market [1]Financial Conduct Authority, “Financial Lives 2025 Survey,” fca.org.uk.

Key Report Takeaways

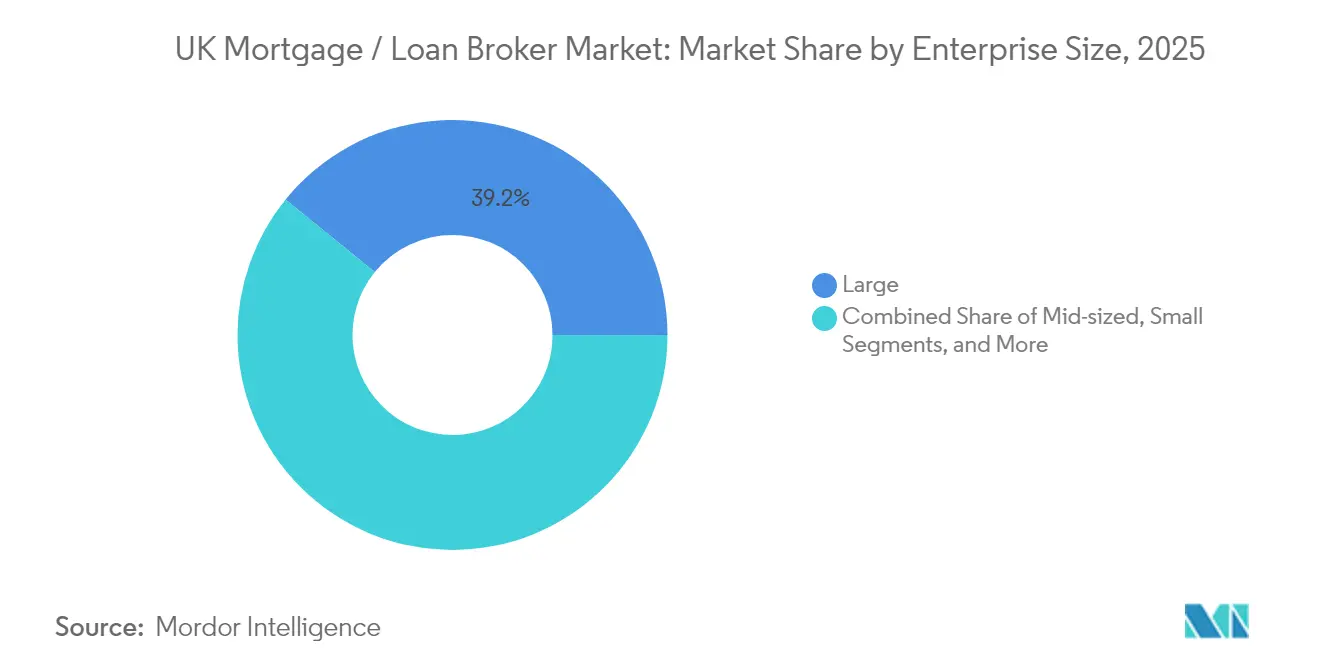

- By enterprise size, large brokers led with 39.15% of the United Kingdom mortgage broker market share in 2025; small brokers are projected to have a 7.62% CAGR through 2031.

- By application, home loans represented 55.90% of the United Kingdom mortgage broker market size in 2025, while commercial and industrial loans are projected to expand at an 7.88% CAGR to 2031.

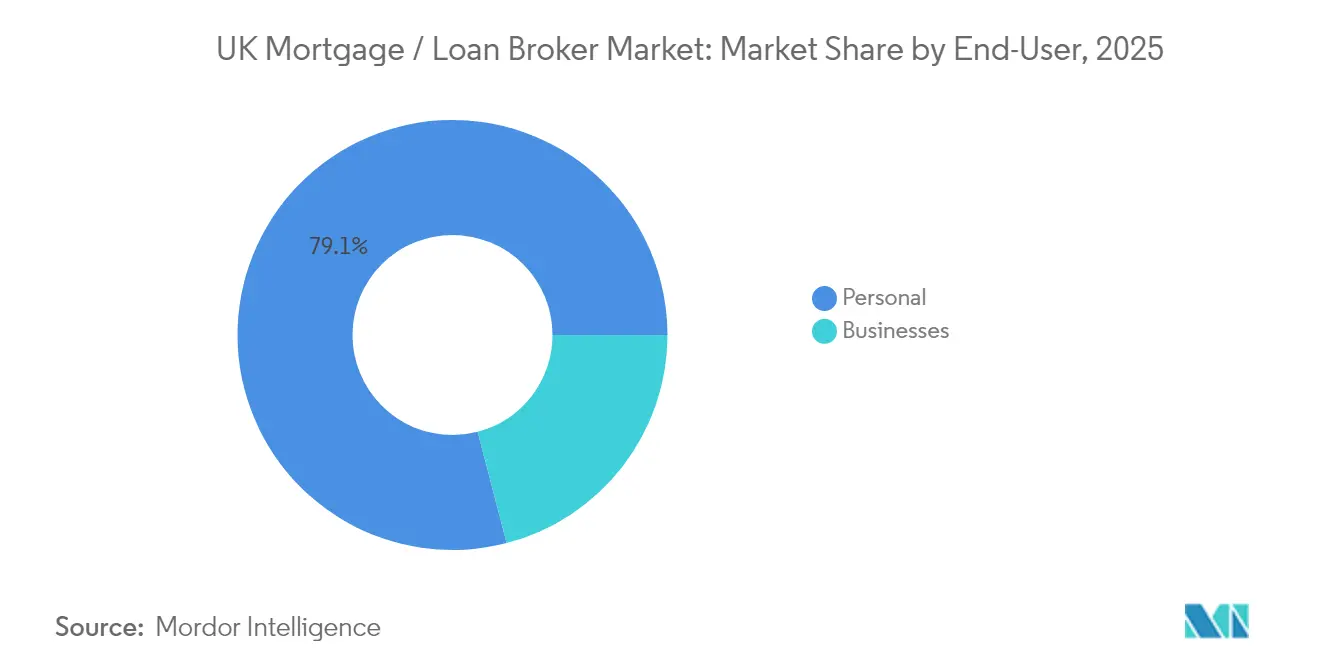

- By end-user, personal borrowers commanded 79.05% of the United Kingdom mortgage broker market share in 2025; business customers are expected to rise at a 8.72% CAGR over the forecast horizon.

- By distribution channel, offline advice retained 66.20% share of the United Kingdom mortgage broker market in 2025; online platforms are expected to grow at 9.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Mortgage/Loan Broker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging intermediary share of mortgage originations | +1.2% | United Kingdom-wide; strongest in London & Southeast | Medium term (2–4 years) |

| FCA Consumer-Duty rules elevating advice quality standards | +0.8% | United Kingdom-wide | Short term (≤ 2 years) |

| Rapid digital-ID & Open-Banking-based onboarding | +1.0% | United Kingdom-wide; early uptake in urban centers | Medium term (2–4 years) |

| Embedded-finance partnerships with estate-agent chains | +0.7% | United Kingdom-wide; dense transaction corridors | Long term (≥ 4 years) |

| AI-driven risk-tiering unlocking near-prime borrower pool | +0.9% | United Kingdom-wide; underserved cohorts | Long term (≥ 4 years) |

| Tokenized real-estate pilots creating novel lending niches | +0.4% | London & major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Intermediary Share of Mortgage Originations

Borrowers now route a majority of new mortgage business through brokers as product complexity grows across more than 200 active lenders[2]UK Finance, “Mortgage Lending Trends 2025,” ukfinance.org.uk. Lenders favor broker channels that lower acquisition costs and deliver pre-qualified cases, a dynamic that intensified during 2024’s rate swings. Specialist advisers excel in buy-to-let, self-employed, and near-prime segments where direct-to-consumer models struggle to map nuanced risk appetites. Larger networks overlay data analytics on pipeline flows to spot emerging lender criteria in real time, further widening their competitive moat. This structural shift cements brokers as the primary gatekeepers of United Kingdom mortgage distribution.

FCA Consumer-Duty Rules Elevating Advice Quality Standards

The Consumer Duty demands that brokers to evidence of fair value and positive customer outcomes, raising compliance thresholds throughout 2025[3]Financial Conduct Authority, “Consumer Duty Final Rules,” fca.org.uk. Firms with robust audit trails and outcome monitoring platforms turn regulation into a competitive advantage, while smaller practices weigh merger or exit. Mandatory closed-book reviews trigger proactive engagement with legacy clients, opening opportunities to refinance on improved terms. Enhanced professionalism bolsters consumer trust and strengthens brokers’ leverage in procuration-fee negotiations with lenders. Collectively, these factors lift service quality and support market expansion.

Rapid Digital-ID & Open-Banking-Based Onboarding

Open-Banking APIs allow instant income verification, shrinking application cycles from weeks to days. Tandem Bank’s tie-up with Sikoia illustrates how automated document capture slashes back-office costs and accelerates approvals. Brokers harness these tools to submit cleaner cases, raising conversion rates for borderline applicants. Customers appreciate friction-free journeys, driving word-of-mouth referrals that lower lead-generation spend. Firms that neglect digital onboarding risk marginalization as service benchmarks rise.

Embedded-Finance Partnerships with Estate-Agent Chains

Integrated property ecosystems embed mortgage advice at the viewing stage, boosting capture rates and shortening completion timelines. Connells Group links 1,200 estate branches with 1,000+ advisers to funnel warm leads into its brokerage arm. Shared CRM data synchronizes milestones across search, offer, and financing, reducing fall-throughs. The model extends to new-build developers, conveyancers, and insurers, unlocking multi-product revenue per client. Private-equity investors favor these capital-light, high-recurrence platforms, signaling sustained growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mortgage-rate volatility compressing broker commissions | -1.1% | United Kingdom-wide; acute in refinancing | Short term (≤ 2 years) |

| Stricter LTV/LTI stress-testing curbing loan eligibility | -0.7% | United Kingdom-wide | Medium term (2–4 years) |

| Rising professional-indemnity premiums for brokers | -0.5% | United Kingdom-wide; heavier on small firms | Short term (≤ 2 years) |

| Shortage of CeMAP-qualified advisers (aging talent pool) | -0.8% | United Kingdom-wide; rural gaps | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mortgage-Rate Volatility Compressing Broker Commissions

Bank of England rate moves narrowed lender margins, leading to leaner procuration fees and shorter fixed-rate life cycles. Advisers mitigate income swings by levying flat advice fees, upselling protection policies, and chasing volume bonuses. Larger networks negotiate tiered grids, while independents pivot toward specialist segments with higher fee tolerance. Greater revenue variability complicates cash-flow planning, yet diversification strategies cushion the blow.

Stricter LTV/LTI Stress-Testing Curbs Loan Eligibility

Enhanced affordability buffers introduced post-pandemic mean borrowers must clear tougher loan-to-value and loan-to-income hurdles. First-time buyers and self-employed applicants feel the pinch, shrinking brokerable volumes. Advisers adapt by exploring guarantor structures, joint borrower-sole proprietor models, and shared-ownership schemes, albeit at greater advisory effort. Some borrowers delay purchases, extending case pipelines and heightening fall-through risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Size: Scale Advantages Drive Consolidation

Large brokers captured 39.15% of the United Kingdom mortgage broker market share in 2025, propelled by enterprise-grade compliance systems and data-driven case allocation that lift approval odds. Robust negotiation power secures preferential procurement grids even as commission spreads narrow, anchoring margins. Mid-sized networks cultivate a balance of personal service and infrastructure heft, outsourcing white-label platforms to match big-broker functionality without full capex. Solo advisers leverage hyper-local relationships to win referral loyalty unavailable to national chains.

Small brokers hold a modest slice of the United Kingdom mortgage broker market size yet register a 7.62% CAGR through 2031. Entrepreneurial agility lets them specialize in expatriate lending, later-life equity release, and complex income structures where premium advisory fees offset scale deficits. Franchise affiliations pool compliance costs and technology access, preserving independence while meeting Consumer Duty obligations.

By Application: Commercial Lending Drives Growth Acceleration

The home loans segment controlled 55.90% of the United Kingdom mortgage broker market size in 2025 as advisers manage affordability tests and rapid product repricing. Residential stability rests on household formation and cultural preference for ownership, while the broker role intensifies around product switching at fixed-rate expiries. Buy-to-let remains active, but prudential tightening caps leverage.

The commercial and industrial loans segment is projected to advance at 7.88% CAGR, diversifying revenue beyond cyclical residential flows. SME owners tap brokers for property purchases and expansion capital as rate stabilization revives business confidence. Lenders value broker-packaged deals that arrive with audited accounts and robust service coverage, cementing broker relevance across the expanding United Kingdom mortgage broker market.

By End-User: Business Segment Accelerates Despite Personal Dominance

The personal customers segment accounted for 79.05% of % the United Kingdom mortgage broker market size in 2025. First-time buyers demand detailed guidance through high loan-to-value schemes, while remortgagers seek cost-efficient switches amid payment-shock concerns. High-net-worth borrowers rely on specialist structuring for cross-border income streams.The business borrowers segment is expected to grow at a 8.72% CAGR, driven by property acquisition and refinancing of pandemic-era debt. Brokers curate lender panels eager for yield and structure complex covenants into digestible credit narratives. Digital deal rooms widen lender bidding, trimming spreads and enhancing adviser fee potential.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Offline advice kept 66.20% of the United Kingdom mortgage broker market share in 2025, serving clients who value in-person reassurance for six-figure liabilities. Face-to-face channels ease coordination with surveyors and solicitors, smoothing chains in complex cases.

Online platforms are projected to rise at a 9.85% CAGR as borrowers embrace 24/7 eligibility engines and video consultations. Habito, Trussle, and similar pioneers combine algorithms with human advisers for nuanced guidance. Hybrid models deliver digital speed plus personal touch, setting service expectations across the United Kingdom mortgage broker market.

Geography Analysis

London and the Southeast dominate transaction value as high asset prices magnify fee income. Brokers adept in international-buyer compliance manage complex documentation for cross-border clients, deepening metropolitan concentration. Average loan sizes stretch margins, reinforcing capital steering toward these hubs.Northern England and Scotland display resilient volumes due to diversified regional economies and moderate price-to-income ratios. Mutual-bank partnerships and community ties allow advisers to secure fast approvals, sustaining throughput even during macro volatility.

Wales and Northern Ireland emerge as frontier territories as digital platforms extend coverage. Cross-border protocol nuances in Northern Ireland introduce documentation complexity, boosting demand for specialist advice. Satellite offices and partner arrangements embed local knowledge, enhancing geographic diversification for the United Kingdom mortgage broker market.

Competitive Landscape

The market concentration is moderately fragmented, with the landscape featuring national chains, digital pure-plays, and regional boutiques. Sesame Bankhall Group’s 2025 stake in New Homes Mortgage Services adds 40 advisers and 45,000 clients, illustrating consolidation trends. National networks pursue bolt-ons to gain specialist skills and new-build exposure.

Competitive differentiation flows from data analytics, embedded partnerships, and talent. Connells Group leverages estate-agency referrals; MQube’s chatbot resolves 90% lender-criteria queries, freeing advisers for relationship work. High street incumbents invest in AI to maintain efficiency parity with digital natives.

Private-equity attention intensifies around scalable brokerages with recurring revenue. Technology vendors license modular onboarding stacks to adviser networks, while niche players exploit underserved segments—self-employed borrowers, near-prime credit, later-life lending—where bespoke structuring beats algorithmic templates. Moderate fragmentation persists, yet consolidation steadily progresses across the United Kingdom mortgage broker market.

United Kingdom Mortgage/Loan Broker Industry Leaders

London & Country (L&C)

Mortgage Advice Bureau

Connells Group / Countrywide MS

Habito

Trussle Lab Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Financial Conduct Authority initiated consultations on easing stress tests and simplifying remortgage rules.

- January 2025: Sesame Bankhall Group bought a strategic stake in New Homes Mortgage Services LLP, adding 40 advisers and annual lending of GBP 760 million.

- January 2025: Tandem Bank partnered with Sikoia to automate income verification, reducing mortgage processing times.

- November 2024: MQube launched an AI chatbot that handles 90% broker criteria queries, boosting lender support efficiency.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom mortgage / loan broker market as the annual commission and fee income earned by independent, networked, and tied intermediaries that originate residential or commercial mortgage loans for UK-based borrowers.

Revenue derived from direct-to-lender digital portals, in-house bank advisers, and credit-repair agents lies outside this scope.

Segmentation Overview

- By Enterprise Size

- Large

- Mid-sized

- Small

- Solo Practitioners

- By Application

- Home Loans

- Commercial and Industrial Loans

- Vehicle Loans

- Other Loans

- By End-User

- Personal

- Businesses

- By Distribution Channel

- Online

- Offline

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed CeMAP-qualified advisers, network compliance heads, and lender business-development managers across England, Scotland, and Wales to validate commission spreads, digital-lead penetration, and expected refinance volumes. Short surveys with first-time-buyer clients helped ground assumptions on average loan sizes and channel preferences.

Desk Research

We began by mapping the market with publicly available datasets such as the Financial Conduct Authority's MLAR tables, Bank of England gross-lending releases, HM Land Registry transaction files, and Intermediary Mortgage Lenders Association trackers. Trade group white papers (UK Finance, IMLA), broker network disclosures, and peer-reviewed journals on household debt complemented the view. Subscription assets from D&B Hoovers and Dow Jones Factiva supplied firm-level revenue splits and deal flows. These sources are illustrative, not exhaustive, and many additional references were consulted for triangulation.

Market-Sizing & Forecasting

A single top-down build linking FCA-reported gross advances, the share routed through brokers, and weighted commission yields sets the 2025 baseline. Select bottom-up checks (sampled network revenues and online lead-gen fees) are then applied to reconcile anomalies. Key drivers in the model include broker penetration of new lending, remortgage wave timing, average loan size, headline bank rate path, and adviser head-count growth. Forecasts through 2030 employ multivariate regression with scenario overlays that stress interest-rate and housing-turnover variables; coefficients are fine-tuned using guidance from our primary interviews.

Data Validation & Update Cycle

Outputs pass automated variance flags against historic FCA series, followed by dual-analyst peer review before sign-off. Reports refresh every 12 months, with interim revisions triggered by base-rate moves above 75 bps or government scheme launches. A last-minute data sweep is completed just before client delivery.

Credibility Anchor: Why Our UK Mortgage Baseline Stands Firm

Published figures often diverge because some publishers treat total loan value as 'market size,' others roll lender branch sales into the broker universe, and refresh cadences vary. Mordor's disciplined revenue-only scope, annual refresh, and dual-sided model temper both over-inflated loan-value counts and excessively conservative broker-fee snapshots.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.16 B (2025) | Mordor Intelligence | - |

| GBP 2.2 B (2024) | Regional Consultancy A | Omits online-only start-ups and models at calendar rather than fiscal year, leading to under-capture of post-Q1 rebound |

| GBP 244.8 B (2025) | Trade Journal B | Measures gross loans arranged, not intermediary revenue, inflating totals |

| USD 38.21 B (2024) | Global Consultancy C | Covers the entire mortgage ecosystem, including lenders, thus overstating broker segment |

The comparison shows that headline gaps stem mainly from scope and metric choices, not arithmetic errors. By isolating broker earnings, blending official lending statistics with on-the-ground revenue evidence, and refreshing annually, Mordor Intelligence delivers a balanced, repeatable baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the UK mortgage broker market?

The UK mortgage broker market stands at USD 3.37 billion in 2026 and is forecast to reach USD 4.62 billion by 2031.

Which segment is growing fastest within the UK mortgage broker market?

Commercial and industrial loans show the highest growth, expanding at an 7.88% CAGR as SME borrowing rebounds.

How is regulation influencing mortgage brokers?

The FCA’s Consumer Duty raises advice quality standards and compliance costs, favoring well-capitalized networks while driving consolidation.

Why are online mortgage brokers gaining share?

Digital onboarding, 24/7 eligibility engines, and video consultations deliver convenience, propelling online platforms at a 9.85% CAGR.

What challenges do mortgage brokers face?

Commission compression from rate volatility, rising professional-indemnity premiums, and a shortage of CeMAP-qualified advisers create headwinds.

How concentrated is the UK mortgage broker market?

The top five players hold a considerable share of the market, indicating moderate consolidation with ample scope for regional and digital specialists.

Page last updated on: