The United Kingdom Home Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

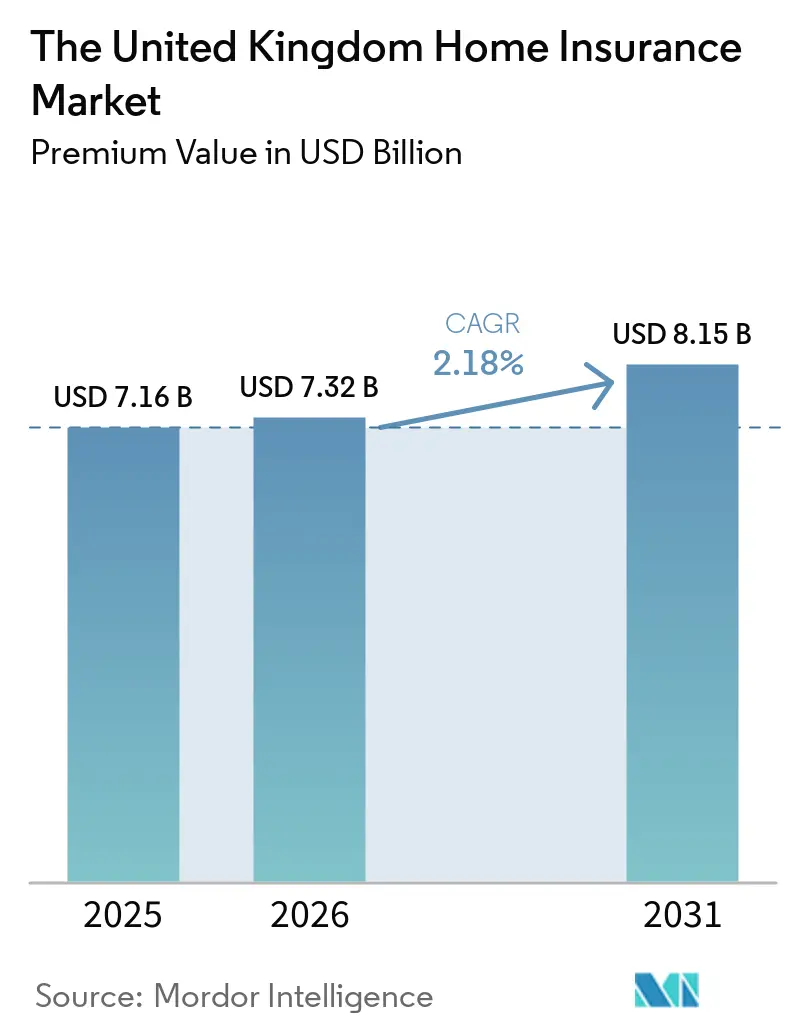

| Base Year Market Size (2025) | USD 7.16 Billion |

| Market Size (2026) | USD 7.32 Billion |

| Market Size (2031) | USD 8.15 Billion |

| Growth Rate (2026 - 2031) | 2.18% CAGR |

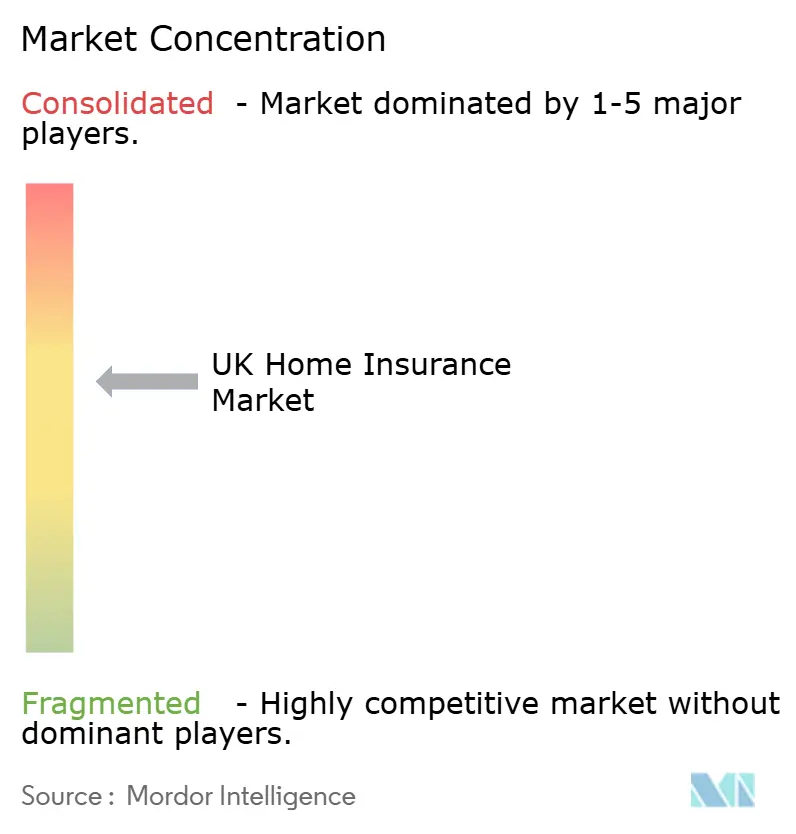

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

The United Kingdom Home Insurance Market Analysis by Mordor Intelligence

The UK home insurance market size is expected to grow from USD 7.16 billion in 2025 to USD 7.32 billion in 2026 and is forecast to reach USD 8.15 billion by 2031 at 2.18% CAGR over 2026-2031. UK home insurance market is on a steady growth trajectory, buoyed by premium adjustments that offset rising claims costs, climate-induced damages, and construction inflation post-Brexit. England plays a pivotal role in the market's overall performance. Regulatory shifts curbing "price walking" and tech-driven underwriting advancements are stabilizing profit margins. Additionally, the Bank of England's base-rate cut in May 2025 is spurring mortgage approvals, expanding the pool of insured properties. On another front, the rise of smart-home technologies and integrated insurance solutions is paving the way for enhanced risk assessment and distribution, enabling insurers to harness data for greater efficiency and scalability.

Key Report Takeaways

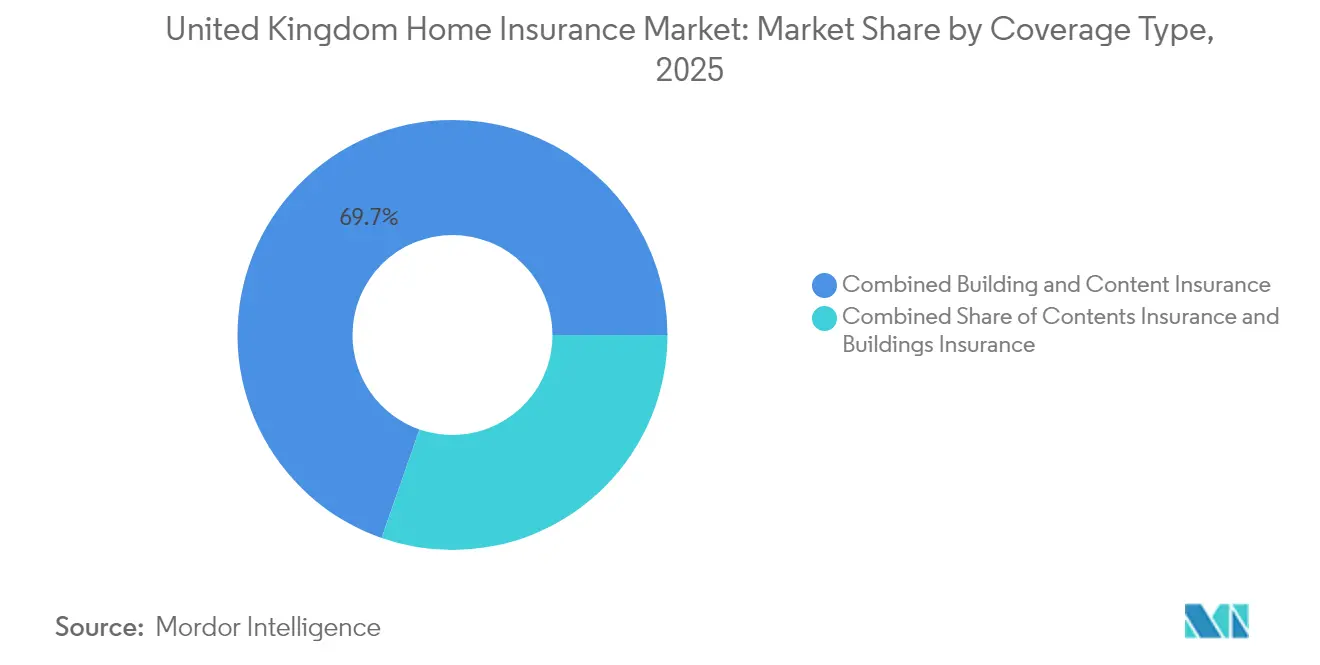

- By Coverage type, combined buildings & contents policies led with 69.65% of the United Kingdom home insurance market share in 2025; this segment is also projected to deliver the fastest 3.08% CAGR to 2031.

- By Distribution channel, online/aggregator platforms are growing at a 3.96% CAGR, while bancassurance held 25.85% revenue share of the United Kingdom home insurance market in 2025.

- By Geography, England accounted for a dominant 71.65% revenue share in 2025; Northern Ireland recorded the sharpest 50.85% annual premium increase that year.

- By Customer type, homeowners generated 59.55% of written premiums in 2025, whereas landlords are seeing rapid product innovation around loss-of-rent protection.

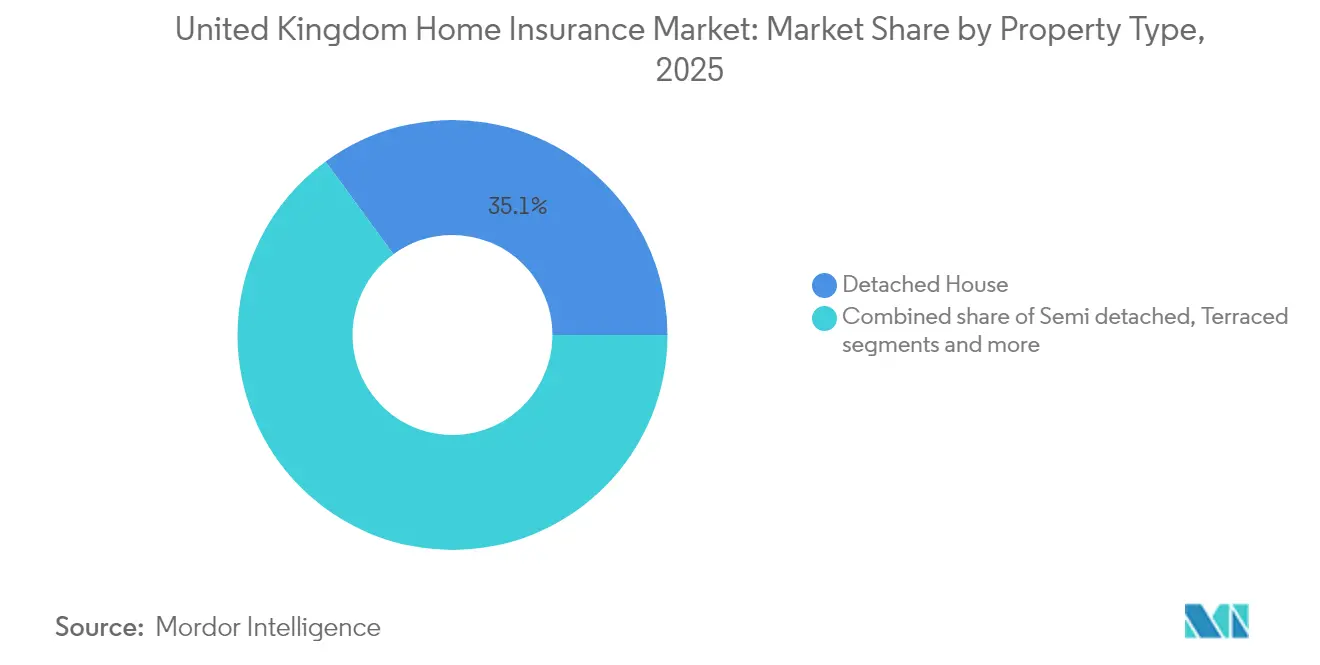

- By Property type, detached houses captured 35.05% of the United Kingdom home insurance market size in 2025, as their high rebuild values command larger sums insured.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

The United Kingdom Home Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-driven surge in severe weather claims | +0.7% | Coastal England, Scotland, Wales | Long term (≥ 4 years) |

| FCA GIPP pricing-practice reform | +0.5% | National, strongest in cities | Medium term (2–4 years) |

| Smart-home IoT penetration | +0.4% | London, urban England | Medium term (2–4 years) |

| Embedded insurance via digital banks | +0.6% | National, Southeast focus | Medium term (2–4 years) |

| Growth in buy-to-let sector | +0.3% | National, with higher impact in urban investment hotspots | Medium term (2-4 years) |

| Mortgage Lending Rebound Post-BoE Rate Cuts | +0.4% | National, with a concentration in first-time buyer markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climate-Driven Surge in Severe Weather Claims Accelerating Combined-Policy Uptake in Coastal England

More intense storms and floods are reshaping risk appetites across coastal regions. Natural catastrophes generated USD 417 billion of global economic losses in 2024, with insured coverage at only 37%[1]Gallagher Re, “Natural Catastrophe and Climate Report 2024,” ajg.com. About 5 million people in England and Wales live in flood-risk zones, and severe events could translate into insured losses that exceed GBP 20 billion. AXA has mapped several East Coast communities facing heightened exposure[2]AXA UK, “Research reveals areas of England most vulnerable to extreme weather,” axa.co.uk. As a result, households are migrating to combined policies that provide a single deductible and broader protection. Insurers are refining catastrophe models, layering reinsurance, and lobbying for public-private flood-mitigation schemes that can temper long-run loss ratios.

FCA “GIPP” Pricing-Practice Reform Boosting Customer Switching & Policy Upgrades

The FCA's "GIPP" pricing reform is reshaping the UK home insurance landscape, spurring more customer switches and policy upgrades. The 2022 rules[3]Financial Conduct Authority, “General Insurance Pricing Practices – Questions & Answers,” fca.org.uk, which prevent renewal prices from surpassing new-business quotes, have effectively eradicated loyalty penalties. This change led to a notable uptick in activity on comparison sites. As a result, average premiums saw an initial rise of over 10% in 2024. However, by year's end, competitive pricing from new entrants tempered these rates. Insurers are now pivoting towards enhanced offerings, like zero-deductible policies and broader home-emergency coverage, to bolster customer retention. While larger carriers have swiftly adapted, smaller intermediaries are still fine-tuning their compliance documentation, fueling a wave of consolidation in the sector.

Penetration of Smart-Home IoT Devices Enabling Telematics-Style Premium Discounts in London

As homeowners increasingly adopt smart-home IoT devices—ranging from leak detectors and smoke sensors to comprehensive security systems—home insurance pricing is evolving. Insurers are moving away from traditional pricing proxies, embracing real-time, behavior-based models. For instance, LeakBot's advanced water-monitoring systems are curbing water damage claims. This not only allows insurers to offer premium discounts, often covering the device costs, but also equips them with critical data on property conditions, refining their underwriting processes. Bundling these devices with insurance policies has led to heightened customer satisfaction, bolstering policy retention, and paving the way for cross-selling opportunities. London, with its pronounced digital engagement, is at the forefront, spearheading smart-home insurance pilots and hinting at potential urban expansion.

Embedded Insurance Partnerships with Digital-Only Banks Capturing First-Time Buyers

Insurers and digital-only banks are joining forces to simplify home insurance access, especially for first-time buyers. By integrating coverage into the mortgage approval process, these platforms remove hurdles that often deter younger, tech-savvy consumers. In the UK, most digital-bank users are open to purchasing insurance this way, with Barclays’ in-app home insurance offers already witnessing a surge in interest. With the evolution of open-finance capabilities, real-time property data can auto-fill quotes, speeding up underwriting and boosting conversion rates. These integrated models not only cut distribution costs but also broaden insurers' reach into traditionally overlooked tenant and millennial demographics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Claims inflation from post-Brexit material costs | -0.5% | National, Southeast strain | Medium term (2–4 years) |

| Under-insurance gap amid volatile rebuild index | -0.4% | High-value areas nationwide | Medium term (2–4 years) |

| Aggregator-Driven Price Competition | -0.4% | National, with stronger impact in price-sensitive segments | Medium term (2-4 years) |

| Flood-Risk Zoning Exclusions in East Anglia | -0.3% | East Anglia, coastal regions, and flood-prone river valleys | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Claims Inflation from Post-Brexit Building-Material Cost Spikes

Post-Brexit surges in building-material costs are putting a strain on the United Kingdom home insurance market. Key inputs, such as steel and timber, have seen steep price hikes, leading to average claims that outstrip premium adjustments and squeeze insurer profits. Supply chain volatility has been heightened by trade disruptions and import tariffs. Meanwhile, labor shortages—worsened by a decline in EU migration—are extending repair timelines and inflating costs for alternative accommodations. This pressure is felt most acutely in Southeast England, where elevated property values and significant rebuild demands intensify the financial challenges for insurers.

Under-Insurance Gap Widening Amid Volatile Rebuild-Cost Index

In the United Kingdom home insurance sector, a widening under-insurance gap is becoming increasingly problematic. Properties are often insured for only two-thirds of their actual rebuild value. This discrepancy leads to average-clause deductions during claims, a challenge especially pronounced for high-net-worth homes, heritage buildings, and flats that need specialized materials like cladding. With rising cost-of-living pressures, 2024 saw nearly one in five consumers either canceling or scaling back their coverage, exacerbating the issue. Insurers, in a bid to enhance accuracy, have started mandating professional valuations at the policy's inception. However, this requirement imposes an upfront cost burden on budget-conscious households, adding another layer of complexity to the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage: Combined Policies Dominate Amid Rising Risks

Combined buildings & contents cover generated 69.65% of written premiums in 2025 and is expanding at a 3.08% CAGR to 2031. The UK home insurance market size for this segment is forecast to surpass USD 5.68 billion by the end of the period. Uptake is driven by value-seeking homeowners who prefer one renewal date and fewer coverage gaps. Heightened flood events and burglary concerns accelerate migration from standalone products as bundled options often include emergency assistance add-ons.

The building-only line, though smaller, experienced 14.9% premium inflation in 2023 as rebuild indices spiked. Mortgage lenders insist on adequate building sums insured, anchoring demand even during economic slowdowns. Content-only cover remains underpenetrated; 25% of households hold no contents policy, exposing a latent growth pocket for insurers that can package affordable, modular products with low deductibles for renters.

By Customer Type: Homeowners Seek Enhanced Protection

Homeowners hold a 59.55% premium share, benefiting from bank-driven insurance requirements at mortgage origination. The UK home insurance market share for landlords is rising as property investors restructure portfolios post-Section 24 tax changes. These landlords increasingly select enhanced loss-of-rent extensions that protect cash flow during repair-related vacancies.

Tenants represent an untapped revenue pool. Embedded offers at digital-rent platforms and in-app personal-property add-ons are starting to boost penetration. Flexible monthly contracts appeal to house sharers and remote workers who shift residences frequently. Insurers that streamline proof-of-address and payment options stand to win loyalty in this mobile demographic.

By Property Type: Detached Houses Command Premium Share

Detached houses contributed 35.05% of the United Kingdom home insurance market size in 2025, given their high average rebuild cost and exposure to storm damage. Semi-detached and terraced stock remains price sensitive yet offers stability due to shared walls that can moderate claims severity. Flats and apartments posted the steepest premium rise, climbing 36% to an average GBP 221 per policy in Q1 2024. Post-Grenfell remediation and cladding-compliance costs fueled insurer caution.

Bedsits saw average premiums reach GBP 423, reflecting older construction, multiple occupancies, and higher fire-risk scores. Geographic flood-zoning now influences underwriting more profoundly, with properties in flood-zone 3 of East Anglia often facing exclusions unless resilience measures are verified.

By Distribution Channel: Digital Platforms Gain Ground

Online aggregators are growing at a 3.96% CAGR to 2031 and already influence more than half of new-business quotes. The UK home insurance market benefits from transparency yet suffers margin compression, with insurers earning around 2% underwriting returns on comparison-site traffic. Bancassurance controls 25.85% of 2025 premiums by cross-selling during mortgage origination and leveraging trust in established banking brands.

Direct-to-consumer insurer portals retain relevance among customers seeking brand reassurance. Brokers remain vital for bespoke high-net-worth covers that need specialist valuations. Insurtech carriers such as Urban Jungle apply AI-driven onboarding to serve flexible tenant segments, illustrating how technology can carve niches that traditional incumbents overlook.

Geography Analysis

England dominates with 71.65% of written premiums in 2025, reflecting dense housing stock, high property values, and significant exposure to coastal flooding. Greater London premiums averaged GBP 333 in Q1 2024 after a 36% surge, mirroring both rebuild costs and theft-risk scores. Flood-risk mapping shows roughly 10% of English homes sit in hazard zones, many in new developments built despite planning objections. The Environment Agency continues to press for resilient infrastructure investment.

Scotland’s tighter land-use rules and strong public-sector flood-defense spending yield more stable risk patterns. Premium growth remains moderate, with insurers praising local authority drainage upgrades that cap claim frequency. Northern Ireland logged the steepest premium jump in 2025, up 50.85% to GBP 383, partly due to a small pool of underwriters and higher average sum insured per dwelling.

Wales shares topographical challenges with England, yet a smaller scale. Coastal communities in the Severn and Dee estuaries face rising sea levels, prompting joint public-private initiatives for sea-wall fortification. Insurtech clusters have emerged in Cardiff and Edinburgh, illustrating a nationwide shift in insurance innovation away from London as two-thirds of UK insurtechs now operate outside the capital.

Competitive Landscape

Strategic M&A is redrawing market power. Aviva’s GBP 3.7 billion purchase of Direct Line will create the country’s largest composite motor and home player. Ageas’s planned acquisition of esure for EUR 1.51 billion positions the Belgian group as the third-largest UK personal-lines player, boosting online aggregator penetration. Consolidation offers scale economies in data science, reinsurance buying, and regulatory compliance.

Price comparison websites intensify competition, compressing underwriting margins while capturing an estimated 53% of revenue through ancillary commissions. To escape price battles, incumbents invest in AI to accelerate claims triage and personalize renewals. Deloitte reports that 76% of insurance executives have piloted generative AI models in policy servicing as of mid-2024.

Opportunity remains in bridging protection gaps for renters and flood-zone owners. Parametric start-ups experiment with fixed payouts that trigger on rainfall thresholds, reducing adjudication costs. British Gas Insurance leverages its parent’s 7 million energy customers to cross-sell boiler-breakdown and buildings cover, illustrating how non-traditional entrants can use existing relationships to capture share.

The United Kingdom Home Insurance Industry Leaders

Aviva plc

Admiral Group plc

Direct Line Insurance Group plc

AXA Insurance UK Ltd

Allianz Holdings (LV=)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bain Capital agreed to sell esure to Ageas for EUR 1.51 billion, creating the third-largest personal-lines insurer.

- April 2025: The FCA proposed amendments that simplify product-governance obligations for insurers.

- December 2024: Aviva announced the GBP 3.7 billion acquisition of Direct Line, reshaping the competitive field.

- October 2024: The FCA opened a study on premium finance charges attached to home and motor policies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom home-insurance market as the gross written premiums generated in the country from policies that protect residential buildings and their contents against perils such as fire, theft, weather, and accidental damage, whether the cover is sold as separate buildings or contents policies or as a combined package. Policies purchased by homeowners, landlords, and tenants are all captured because, according to Mordor Intelligence, they form one demand pool driven by the same risk variables.

Scope exclusion: Standalone gadget insurance that is not bundled within a home policy, as well as structural warranties tied to new-build houses, are excluded.

Segmentation Overview

- By Coverage

- Buildings Insurance

- Contents Insurance

- Combined Buildings & Contents Insurance

- By Customer Type

- Homeowners

- Landlords

- Tenants/Renters

- By Property Type

- Detached Houses

- Semi-Detached Houses

- Terraced Houses

- Flats & Apartments

- By Distribution Channel

- Direct (Insurer Websites & Call-centres)

- Bancassurance (Banks & Building Societies)

- Brokers & Independent Advisers

- Aggregators / Price-Comparison Websites

- Affinity & Retailer Partnerships

- Digital-Only / Insurtech Carriers

- By Region

- England

- Scotland

- Wales

- Northern Ireland

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed underwriting managers, broker executives, price-comparison platform product leads, and insurtech founders across England, Scotland, Wales, and Northern Ireland. These conversations validated loss-ratio assumptions, emerging peril riders, and typical renewal discounts, then bridged gaps in publicly disclosed premium splits.

Desk Research

We first mapped the demand base through publicly available tier-1 sources such as the Association of British Insurers loss-data portal, Office for National Statistics household stock tables, Bank of England premium rate trackers, and Financial Conduct Authority product-level filings. Complementary insight on weather severity and flood zones was obtained from Met Office datasets, while consumer switching behavior was gleaned from press releases and quarterly surveys archived in Dow Jones Factiva and D&B Hoovers.

Those repositories establish baseline volumes, average rebuild costs, and distribution-channel movement. Additional context came from parliamentary committee papers, housing price indices, and peer-reviewed studies on climate-related claims trends. The sources cited above are illustrative only; many other publications were reviewed for cross-checks and clarification.

Market-Sizing & Forecasting

A hybrid top-down build begins with annual gross written premium totals reported by insurers and the ABI, which are then reconciled with household counts, mortgage originations, and penetration rates. Results are corroborated through bottom-up spot checks that roll up sampled average premiums by dwelling type and channel. Five market fingerprints, owner-occupied housing stock, average rebuild cost index, frequency of named storms, mortgage approvals, and aggregator quote volumes, feed a multivariate regression that projects demand to 2030. Where policy-level data are thin, ratio estimates from expert interviews are applied, and any variance above 5 percent triggers a model rebalance.

Data Validation & Update Cycle

Model outputs undergo variance checks against historical claims, insurer earnings releases, and macro housing indicators. Senior analysts review anomalies before sign-off. We refresh every twelve months, with interim updates if severe weather or regulatory shifts materially alter premiums; a final sense-check is completed just before report release.

Why Our UK Home Insurance Baseline Deserves Confidence

Published figures often differ because each firm chooses its own coverage basket, currency conversion point, and forecast cadence.

Key gap drivers include inclusion of landlord-only lines, whether renewals are counted, assumptions on rebuild-cost inflation, and the age of the base year. Because Mordor aligns scope with ABI definitions, applies uniform 2024 exchange rates, and refreshes annually, our baseline remains tightly anchored.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.16 B (2025) | Mordor Intelligence | - |

| GBP 5.3 B (2025) | Regional Consultancy A | counts new policies only, omits renewals, narrower peril list |

| USD 5.19 B (2023) | Trade Journal B | older base year, limited inflation adjustment, infrequent refresh |

| USD 9.0 B (2024) | Industry Association C | bundles landlord warranty and specialty flood covers, top-down only |

Taken together, the comparison shows that when scope alignment and multi-variable validation are applied, Mordor's estimate strikes a balanced middle ground that decision-makers can trace back to clearly published inputs and reproducible steps.

Key Questions Answered in the Report

What is the projected size of the UK home insurance market by 2031?

The UK home insurance market size is forecast to reach USD 8.15 billion by 2031, expanding at a 2.18% CAGR from 2026.

Which coverage type is growing the fastest?

Combined buildings & contents policies are advancing at a 3.08% CAGR through 2031 as households seek comprehensive protection from climate-related losses.

How are regulatory reforms affecting premium pricing?

FCA rules that ban renewal premiums from exceeding new-business quotes have increased transparency, encouraging customer switching and modestly raising average premiums nationwide

Why are smart-home devices important for insurers?

Connected sensors reduce claim frequency and severity by detecting leaks or fires early, enabling insurers to offer usage-based discounts and gather real-time risk data.

Page last updated on: