UK Facade Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.5 Billion |

| Market Size (2026) | USD 10.99 Billion |

| Market Size (2031) | USD 13.79 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Facade Market Analysis by Mordor Intelligence

UK façade market size in 2026 is estimated at USD 10.99 billion, growing from 2025 value of USD 10.5 billion with 2031 projections showing USD 13.79 billion, growing at 4.63% CAGR over 2026-2031. Rapid post-Grenfell safety reforms, net-zero envelope mandates, and mounting demand from the data-center construction pipeline underpin growth. Developers now prioritize non-combustible, thermally efficient façades over upfront cost savings, while extended VAT relief on energy-saving materials is accelerating the adoption of building-integrated photovoltaics (BIPV). England leads spending but Wales is the fastest-growing geography on the back of large mixed-use schemes in Cardiff. Competitive dynamics have shifted toward compliance credentials, with Saint-Gobain’s USD 815 million takeover of OVNIVER and Kingspan’s insulation push illustrating vertical-integration plays. At the same time, a shortage of 251,500 construction workers by 2028 is catalyzing modular off-site façades that lower on-site labor intensity[1]Construction Industry Training Board, “CSN Industry Outlook 2024-2028,” citb.co.uk

Key Report Takeaways

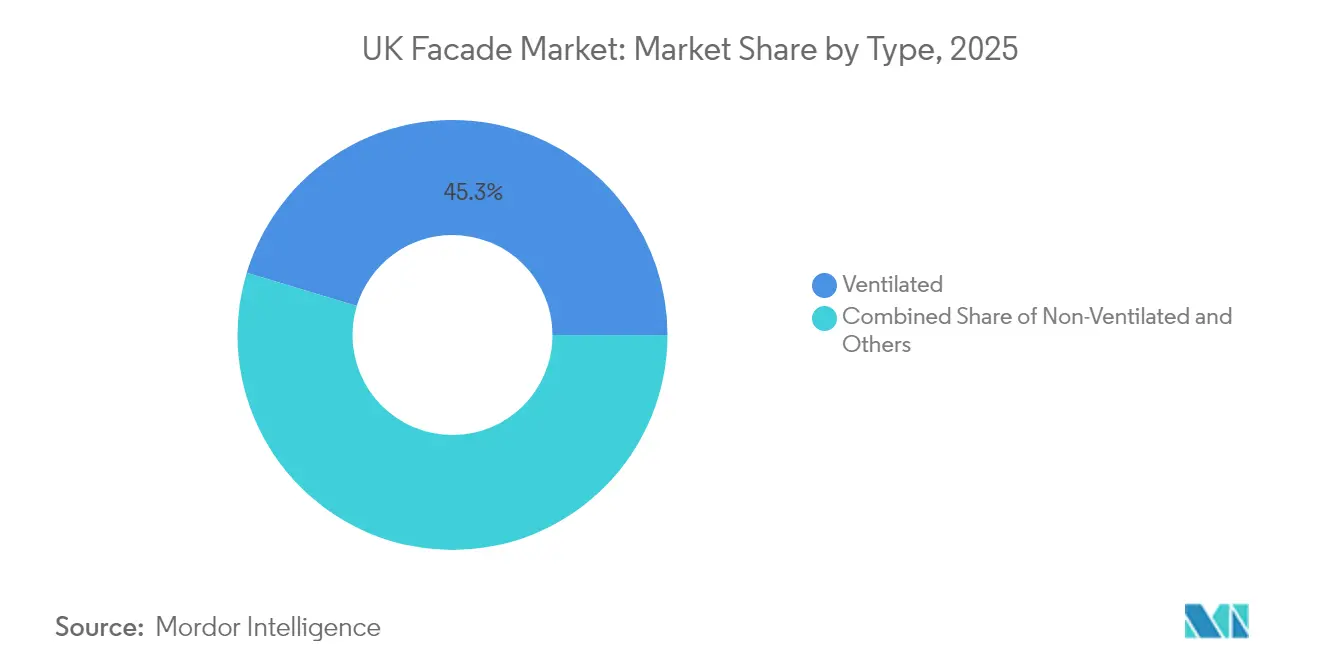

- By façade type, ventilated systems captured 45.32% of the UK façade market share in 2025 and are expanding at a 7.65% CAGR between 2026-2031.

- By system configuration, rainscreen cladding led with 32.74% revenue in 2025, while unitised curtain walls are the fastest-growing at 8.47% CAGR between 2026-2031.

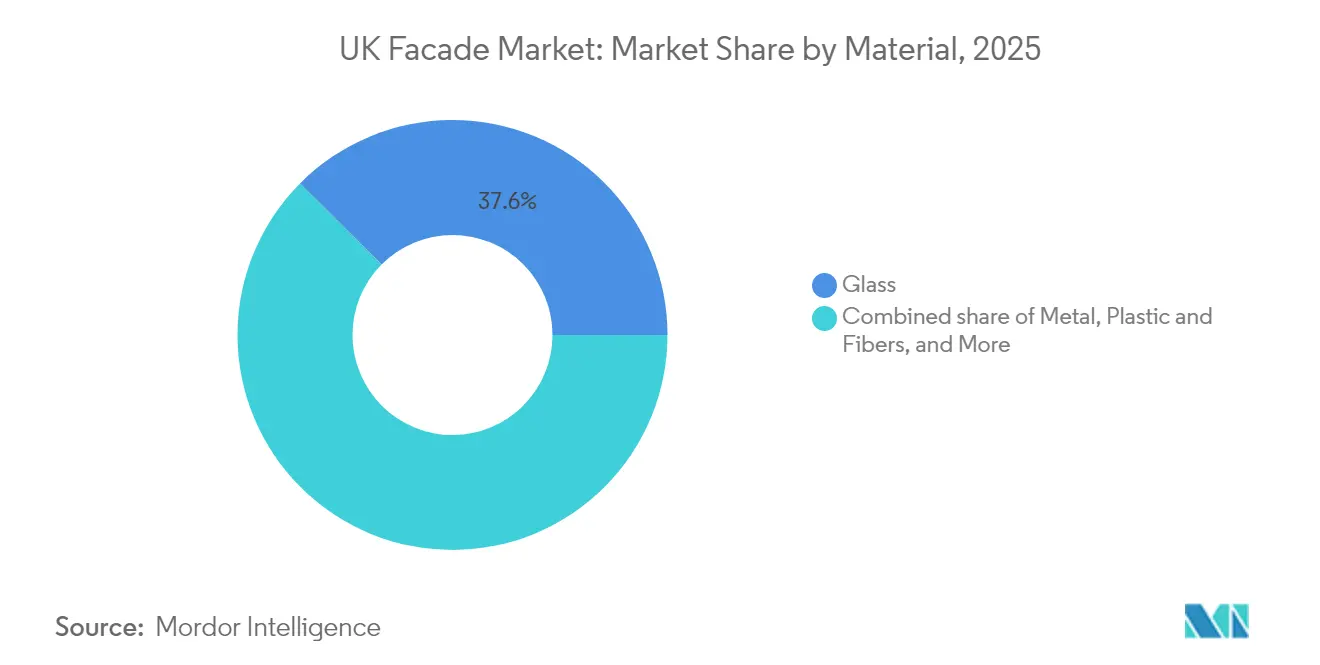

- By material, glass held a 37.55% share of the UK façade market size in 2025; Other Segment is advancing at 12.1% annually, buoyed by VAT exemptions effective until March 2027.

- By installation, renovation, and retrofit applications are growing at 8.66% CAGR versus 60.35% share for new-build projects in 2025, propelled by London’s “Retrofit First” policy.

- By end-user, commercial buildings commanded 53.22% of the UK façade market in 2025, with data-center demand pushing the segment at a 6.98% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Facade Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Grenfell recladding surge | +1.2% | England core, spill-over to Wales, Scotland | Medium term (2-4 years) |

| Net-zero 2050 envelope mandates | +0.8% | Global | Long term (≥ 4 years) |

| Modular off-site build adoption | +0.6% | England, Scotland | Medium term (2-4 years) |

| Data-centre build boom | +0.5% | England core, selective Scotland sites | Short term (≤ 2 years) |

| VAT relief energising BIPV façades | +0.4% | England, Wales, Scotland | Short term (≤ 2 years) |

| London "Retrofit First" policy | +0.2% | London, selective England metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Grenfell Recladding Surge

The Building Safety Act 2022 identified 5,052 residential blocks over 11 meters with unsafe cladding as of April 2025, with 2,477 already undergoing remediation [2]UK Department for Levelling Up, “Building Safety Remediation Monthly Data Release,” gov.uk. First-tier Tribunal rulings now deem even “medium” fire-risk ratings unacceptable, broadening liability exposure. Insurers are excluding combustible façades, effectively mandating A1-rated systems. VAT deductions on remediation work further lower upgrade costs. Established suppliers with certified, non-combustible portfolios are therefore capturing outsized demand.

Net-Zero 2050 Envelope Mandates

The Future Homes Standard, due in 2025, requires steep cuts in operational carbon, while London obliges whole-life carbon assessments for schemes above 1,000 m². Research shows glass accounts for up to 60% of façade embodied carbon, prompting manufacturers to develop high-recycled-content glazing.[3]Arup, “Understanding the Carbon Footprint of Façades,” arup.com Government recognition of data centers as nationally significant infrastructure is shortening planning timelines but tightening energy-performance criteria. Public-sector BREEAM “Excellent” thresholds now hinge on façade decarbonization, illustrated by Cardiff’s Velindre Cancer Centre.

Modular Off-Site Build Adoption

Government studies highlight that volumetric modular delivery, when coupled with early Design-for-Manufacture decisions, mitigates quality risks and speeds completion. Labor shortages—251,500 extra workers needed by 2028—make factory-built façades attractive. High-rise automation research confirms improved geometric tolerances and connection robustness for façade modules. Data-center developers are leading adoption because the approach compresses delivery schedules without compromising performance.[4]XYZ Reality, “2025 Data Center Trends,” xyzreality.com

Data-Center Build Boom

England’s technology corridors host a GBP 10 billion (USD 13 billion) AI campus at Blyth and a GBP 3.75 billion (USD 5.06 billion) hyperscale site in Hertfordshire, both requiring high-performance façades capable of managing elevated heat loads. European data-center demand is set to expand grid power needs by 160% by 2030, intensifying the call for energy-efficient envelopes. Façade systems now integrate smart shading and passive cooling features to control internal temperatures while meeting stringent PUE targets. Edge-computing roll-outs are also spurring retrofit solutions that slot into existing urban shells.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminium & glass price volatility | -0.7% | Global | Short term (≤ 2 years) |

| Shortage of certified façade labour | -0.5% | England core, Scotland, Wales | Medium term (2-4 years) |

| Insurance exclusions for combustible systems | -0.3% | England, Wales, Scotland | Short term (≤ 2 years) |

| Embodied-carbon caps (London Plan) | -0.2% | London, selective England metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aluminium & Glass Price Volatility

Energy-intensive aluminium smelting faces shifting supply dynamics and geopolitical trade risks that filter through to façade budgets. UK construction material indices recorded a 2.0% year-on-year decline as of June 2024, yet spot prices remain unstable, complicating cost planning for long-lead façade contracts. Flat-glass producers are investing in automation to curb unplanned downtime that can top GBP 1 million (USD 1.3501 million) per minute.

Shortage of Certified Façade Labor

Only 60,000 of the 251,500 additional construction workers required by 2029 will be government-funded trainees, prolonging skill shortages. Façade installers must now evidence competency under Building Safety Act regulations, narrowing the available talent pool. Heat-pump engineering shortfalls underscore the wider scarcity of building-envelope skills. Prefabricated, unitised systems that reduce on-site labor are therefore winning specification priority.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ventilated Systems Drive Performance Innovation

Ventilated systems accounted for 45.32% of UK façade market share in 2025, and the segment is set to grow at a 7.65% CAGR through 2031. Their cavity design limits fire propagation and enhances thermal regulation, aligning with Building Safety Act compliance and net-zero targets two priorities that now shape nearly every tender in the UK façade market. The technology is evolving toward smart modules such as seele’s ISOshade®, which uses embedded sensors and AI-driven louvers to modulate solar gain without active energy consumption. Demand is also rising for ventilated retrofits on occupied residential towers, leveraging VAT relief and insurance incentives to replace combustible cladding. As insurers tighten underwriting, developers increasingly view ventilated systems as the baseline solution rather than an upgrade.

By Façade System Type: Unitised Innovation Challenges Rainscreen Dominance

Rainscreen cladding captured 32.74% of UK façade market revenue in 2025, reflecting its versatility and proven A1-rated assemblies. However, unitised curtain walls are advancing at an 8.47% CAGR to 2031, driven by factory-controlled quality and faster installation that counters labor shortages in the UK façade market. Manufacturers are blurring lines between systems; hybrid unitised-rainscreen solutions promise the aesthetic freedom of rainscreens with the speed advantages of unitised panels. CWCT-certified mock-ups are now mandatory on most high-rise projects, favoring suppliers that can test entire unitised assemblies under worst-case load scenarios. As modular builders standardize bay sizes, unitised panels are becoming the default interface.

By Material: BIPV Glass Disrupts Traditional Specifications

Glass held 37.55% of UK façade market size in 2025, but Other segment is expanding at 12.1% annually thanks to VAT exemptions and net-zero commitments. Vitro’s Solarvolt™ panels and Guardian-ML System solar windows capture daylight while generating up to 33 Wp/m². University of York research reports vertical bifacial arrays delivering winter power gains of 24.5%, a notable advantage for northerly latitudes. Metals maintain relevance for fire performance, while plastics face rising insurance exclusions. Developers increasingly specify low-carbon aluminium with high recycled content, pushing producers toward closed-loop supply models.

By Installation: Retrofit Acceleration Transforms Market Dynamics

New-builds represented 60.35% of 2025 installations, yet retrofit demand is forecast to grow at 8.66% CAGR through 2031 as London’s Retrofit First mandate and whole-life-carbon caps favor building reuse. Retrofit projects are leveraging VAT deductions for remediation to finance façade upgrades. The retrofit wave requires flexible panelized systems that can interface with unknown substrate conditions and variable floor heights. Suppliers offering detailed digital surveys and parametric panelization are gaining share as clients demand minimal tenant disruption-another competitive differentiator in the UK façade market.

By End-User: Commercial Sector Leads Innovation Adoption

Commercial buildings controlled 53.22% of UK façade market revenue in 2025 and are projected to expand at 6.98% CAGR to 2031, buoyed by hyperscale data-center projects and ESG-driven office refurbishments. Developers accept premium pricing for BIPV and intelligent façades that lower operational carbon or improve occupant well-being.

Residential demand remains volume-rich but price-sensitive; social landlords often adopt standardized ventilated panels to meet both safety and budget constraints. Industrial and institutional segments adopt niche innovations-think blast-resistant or radiation-shielding façades-but represent smaller slices of overall spend.

Geography Analysis

England generated 69.45% of UK façade market revenue in 2025, driven by London’s stringent whole-life carbon rules and high concentration of high-rise projects. Planning reforms that fast-track data centers and life-science campuses further consolidate spending in the South-East, although regional authorities adopt similar safety standards, extending compliance-driven demand across the country.

Wales delivers the fastest growth at 6.28% CAGR through 2031. Cardiff’s 50-story tower and the Velindre Cancer Centre exemplify large schemes requiring advanced façades that align with BREEAM “Excellent” ambitions. The Ffrâm24 framework, with 80% of approved suppliers local, improves supply-chain resilience for Welsh projects. Scotland maintains steady façade demand from public-realm investments such as the Dunard Centre concert hall and university expansions, albeit under tighter public-spending oversight. The Single Building Assessment pilot covering 107 blocks is expected to unlock remediation pipelines once funding is clarified. Northern Ireland records consistent but smaller volumes, with quarterly construction output stabilizing since mid-2024.

Competitive Landscape

The UK façade market is moderately concentrated: the top five suppliers control roughly 48% of combined revenue, and recent M&A activity points toward further consolidation. Saint-Gobain’s USD 815 million OVNIVER deal expands its non-combustible product range, while Kingspan’s Steico acquisition boosts bio-based insulation capabilities. Forterro’s back-to-back software buys reveal a push toward integrated digital design-to-manufacture workflows for windows and façades.

Value propositions now hinge on third-party certification, supply-chain transparency, and service bundling (design-assist, digital twinning, and on-site quality control). Kingspan reports a 65% drop in scope 1 and 2 emissions since 2020, signaling that decarbonization credentials drive tender success. Meanwhile, mid-tier players are partnering with international system houses—Schüco’s tie-up with Skyline Windows is a case in point—to gain access to tested, code-ready assemblies. Technological differentiation centers on BIPV integration, AI-enabled shading, and prefabricated volumetric façade “cassettes” that can be installed with a fraction of traditional labor. Suppliers investing early in digital fabrication and low-carbon materials are likely to expand their share as insurers and asset owners demand quantifiable performance data.

UK Facade Industry Leaders

Permasteelisa

Schüco UK

Kingspan Insulated Panels UK

Saint-Gobain Glass UK

AluK (GB) Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Forterro bought BM Group to deepen its fenestration-software stack after acquiring Orgadata in 2024.

- August 2024: UK government extended VAT relief on energy-saving materials, including BIPV, until March 2027.

- July 2024: Saint-Gobain Glass unveiled COOL-LITE® XTREME 61/29 ORAÉ® and other high-recycled-content glazing at Glasstec.

- May 2024: Vitro Architectural Glass launched Solarvolt™ BIPV modules for overhead glazing and façade elements.

UK Facade Market Report Scope

Originating from the Italian word 'facciata', the term 'facade' refers to the exterior faces of a building. While it encompasses all external faces, it's often used to denote the main or front face. Alongside the roof, the facade stands as a crucial element, serving as the primary shield against weather elements like rain, snow, wind, and sun, which can jeopardize a structure's integrity. Typically, a facade is the prominent or decorative front exterior of a building. Engineers emphasize the facade's significance, particularly for its influence on energy efficiency.

The UK facade market is segmented by type (ventilated, non-ventilated, and others), by material (glass, metal, plastic and fibers, stones, and others), and by end users (commercial, residential, and others). The report offers market size and forecast in terms of value (USD) for all the above segments.

| Ventilated |

| Non-Ventilated |

| Others |

| Rainscreen Cladding |

| Curtain-Wall Systems |

| Others |

| Glass |

| Metal |

| Plastic & Fibres |

| Stone |

| Others |

| New Construction |

| Renovation & Retrofit |

| Commercial |

| Residential |

| Others |

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Type | Ventilated |

| Non-Ventilated | |

| Others | |

| By Facade System Type | Rainscreen Cladding |

| Curtain-Wall Systems | |

| Others | |

| By Material | Glass |

| Metal | |

| Plastic & Fibres | |

| Stone | |

| Others | |

| By Installation | New Construction |

| Renovation & Retrofit | |

| By End-User | Commercial |

| Residential | |

| Others | |

| By Region | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Key Questions Answered in the Report

How large is the UK façade market in 2026?

The UK façade market is projected to reach USD 10.99 billion in 2026, on track for a 4.63% CAGR through 2031.

Which façade type is growing the fastest?

Ventilated façade systems are expanding at a 7.65% CAGR, driven by safety compliance and superior thermal performance.

What role does BIPV play in future UK façades?

Building-integrated photovoltaic glass is growing 12.1% each year, aided by VAT relief and net-zero targets that reward on-site power generation.

Why are unitised curtain walls gaining share?

Factory-built unitised panels cut installation time and reduce reliance on scarce certified labor, leading to an 8.47% CAGR forecast.

How is regulation shaping façade procurement?

The Building Safety Act 2022 and London’s whole-life carbon rules compel developers to specify non-combustible, low-carbon façades with robust documentation.

Page last updated on: