AI In Medical Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

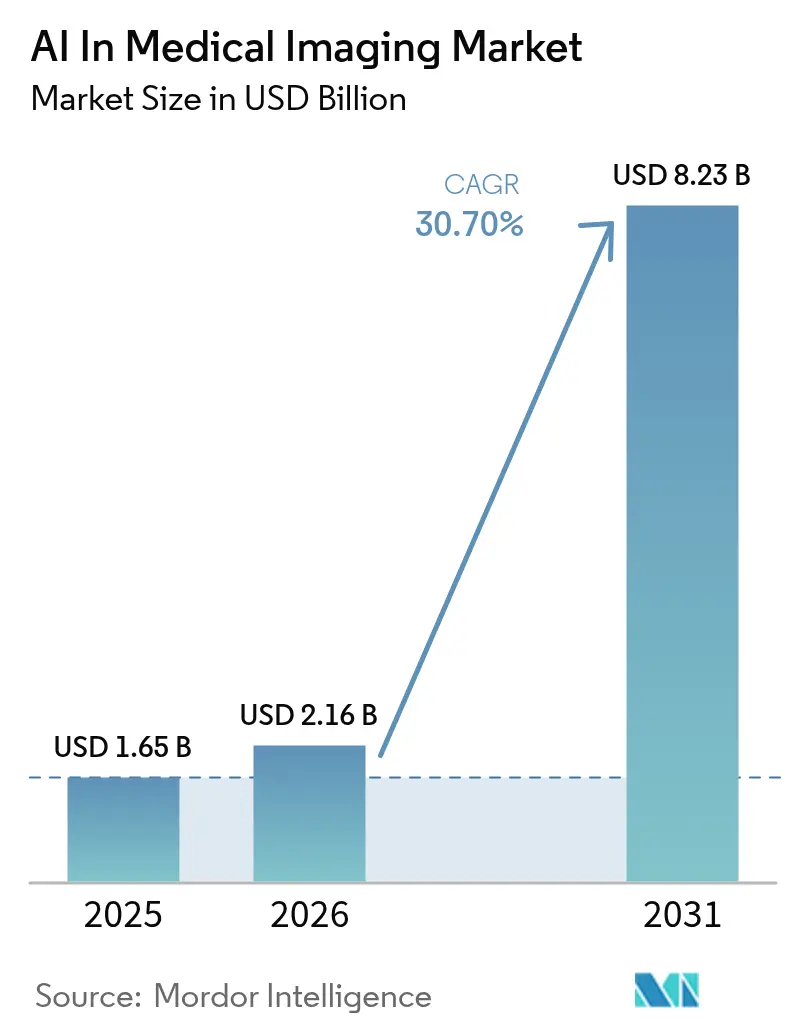

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 8.23 Billion |

| Growth Rate (2026 - 2031) | 30.70% CAGR |

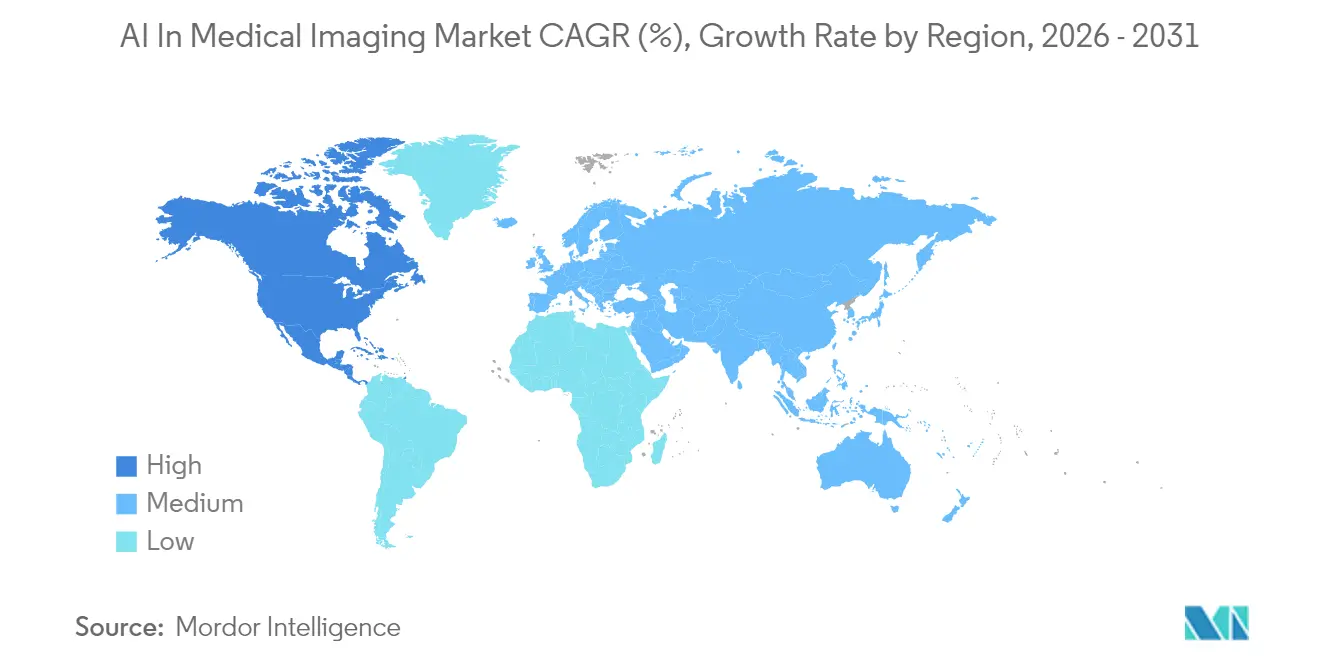

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Medical Imaging Market Analysis by Mordor Intelligence

The AI In Medical Imaging Market size market is expected to grow from USD 1.65 billion in 2025 to USD 2.16 billion in 2026 and is forecast to reach USD 8.23 billion by 2031 at 30.7% CAGR over 2026-2031.

This jump underscores a shift from pilot projects to routine use across radiology, oncology and emergency care. Faster FDA clearances, cloud-hosted imaging archives and pay-for-performance incentives are shortening purchasing cycles. Multi-vendor interoperability standards now let algorithms plug into existing Picture Archiving and Communication Systems (PACS), reducing integration costs. Providers also see AI as a practical response to rising scan volumes and the widening radiologist shortfall, which is forecast to reach 19,500 in the United States by 2034. Asia’s cancer-screening mandates, Europe’s cross-border image-sharing rules and national AI grants in the United States and United Kingdom are creating fresh demand pockets that vendors are racing to serve.

Key Report Takeaways

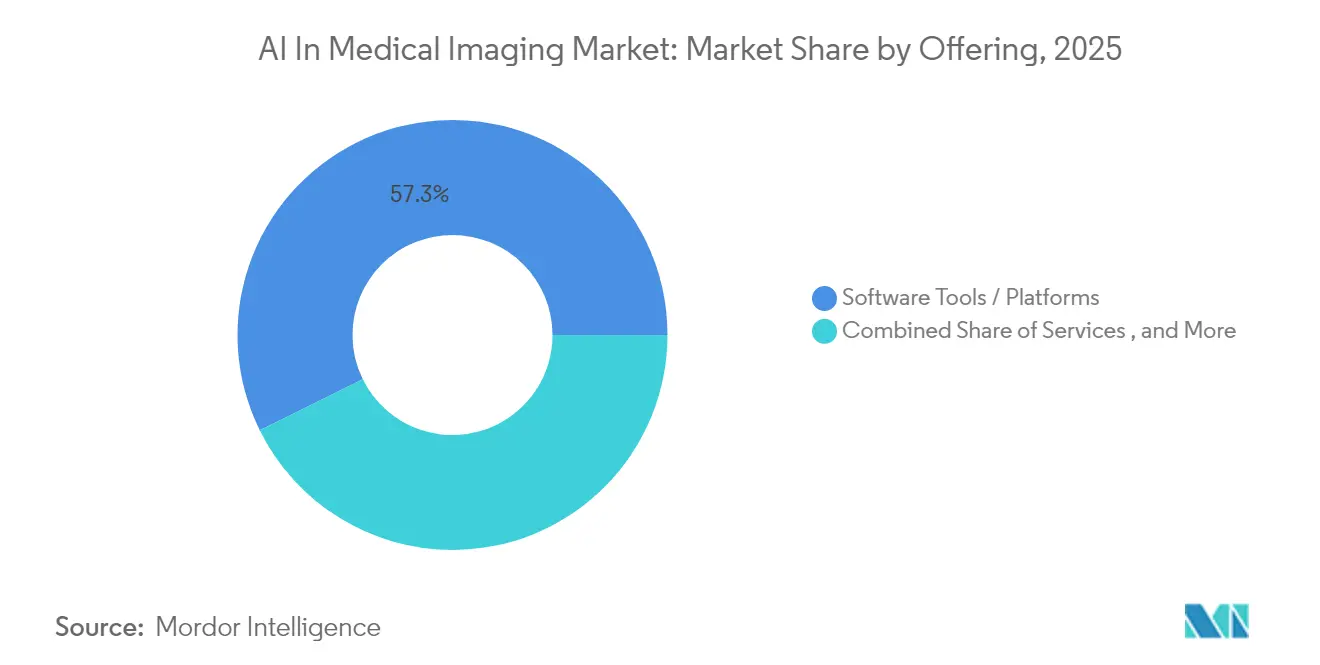

- By offering, software platforms led with 57.30% of the AI in medical imaging market share in 2025, while services are projected to expand at a 31.4% CAGR through 2031.

- By imaging modality, CT contributed 27.60% revenue share in 2025, whereas ultrasound is forecast to grow at 31.0% CAGR to 2031.

- By application, oncology accounted for 30.40% of the AI in medical imaging market size in 2025, and pulmonology is advancing at a 33.5% CAGR over 2026-2031.

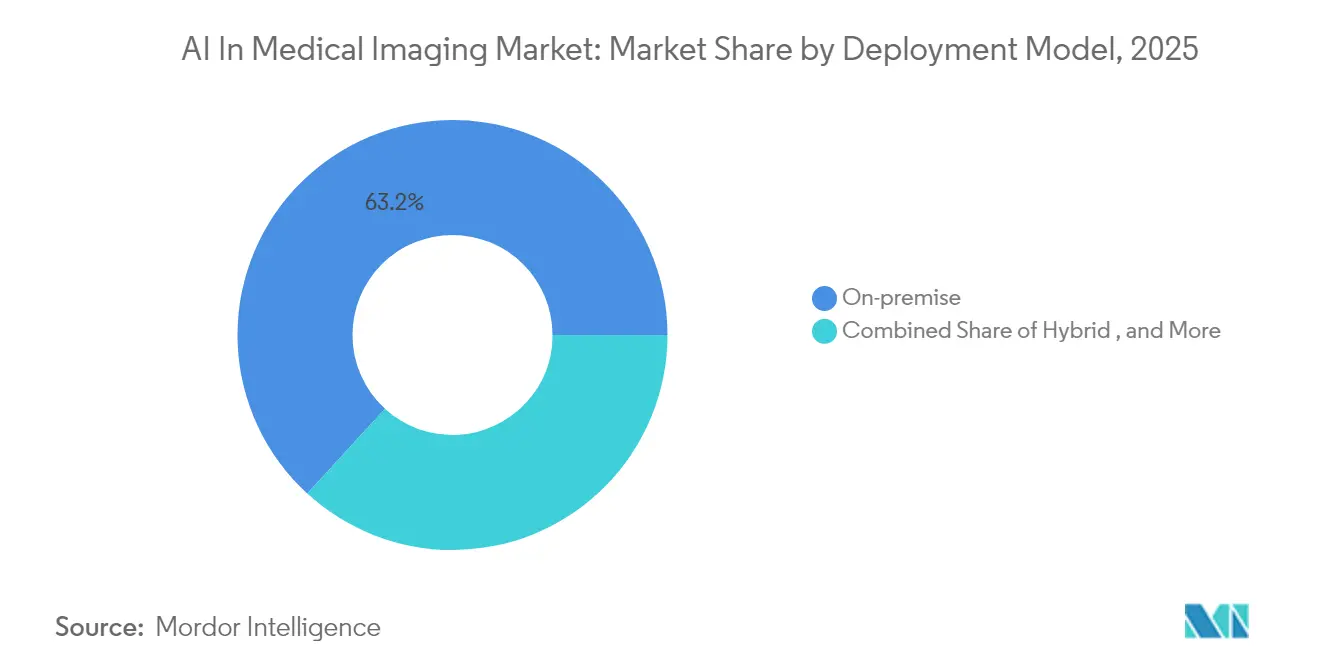

- By deployment model, on-premise systems held 63.20% share of the AI in medical imaging market size in 2025, yet cloud solutions are projected to climb at 35.4% CAGR to 2031.

- By end user, hospitals and clinics commanded 70.30% of 2025 revenue, while teleradiology providers registered the highest forecast CAGR at 34.9%.

- By geography, North America led with 40.60% revenue share in 2025; Asia is the fastest-growing region, expected to post a 32.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI In Medical Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of multi-vendor PACS interoperability standards | +6.20% | North America and Europe | Medium term (2–4 years) |

| Accelerating oncology screening mandates in Asia | +5.80% | Asia | Medium term (2–4 years) |

| Large-scale national AI diagnostics grants | +4.70% | North America and Europe | Medium term (2–4 years) |

| Growing shortage of radiologists boosting teleradiology | +5.30% | Europe and Middle East | Short term (≤ 2 years) |

| Enterprise-level Cloud Migration of Imaging Archives by U.S. IDNs | +4.30% | United States, expanding to Canada and Western Europe | Medium term (2–4 years) |

| Commercial Roll-out of FDA and CE Cleared SaMD Algorithms for Stroke Triage | +3.70% | North America and Europe; emerging adoption in Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid expansion of multi-vendor PACS interoperability standards in U.S. and EU

Cross-border imaging exchange rules from the EU eHealth Network and upcoming U.S. interoperability provisions allow algorithms to read scans stored on any certified PACS. Early pilots using FHIR-based federated frameworks achieved 95% data-retrieval accuracy and cut latency by 38%, enabling faster triage in acute settings while maintaining data sovereignty

Accelerating oncology screening mandates in Asia (China, Japan, South Korea)

Government-funded programs are adding millions of extra CT and endoscopy exams each year. South Korea’s national gastric-cancer initiative demonstrates favorable cost-utility ratios, and Japan now detects 70% of lung cancers at Stage I or II when AI flags incidental nodules.

Large-scale national AI diagnostics grants

Programs such as NIH Bridge2AI are funding algorithm development, workforce training, and bias-mitigation research. In the United Kingdom, NHS-AI pilots of e-Stroke have lifted mechanical-thrombectomy rates by 62% and shortened patient transfer times, translating research investment into measurable care improvements.

Growing shortage of radiologists boosting teleradiology adoption in Nordics & GCC

Rising scan volumes and limited specialist availability press health systems to outsource reads. AI-enhanced teleradiology platforms now offer automated triage, structured reporting, and quality-control dashboards, helping providers uphold turnaround-time targets without expanding headcount.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented data-governance laws are hindering cross-border model training | –3.2% | EU and Asia | Medium term (2–4 years) |

| High per-scan inference costs on edge GPUs in low-volume clinics | –2.8% | Global (emerging markets) | Short term (≤ 2 years) |

| Liability Ambiguity Around AI-assisted Diagnosis in EU MDR | –2.3% | EU | Medium term (2–4 years) |

| CAPEX Freeze in Small and Rural Hospitals Post-COVID Capital Depletion | –1.7% | North America and Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented data-governance laws are hindering cross-border AI model training

The EU AI Act classifies diagnostic algorithms as high-risk, demanding rigorous conformity assessments. Divergent consent rules across Asia further limit the use of multi-country datasets, which in turn degrade model generalizability and slow down approvals, especially for rare-disease cohorts.[2]European Commission, “Artificial Intelligence Act – High-Risk Medical Devices,” ec.europa.eu

High per-scan inference costs on edge GPUs in low-volume clinics

GPU hardware enables sub-second inference but remains expensive. Benchmark tests show bone-age models jump from 1.4 to 267 images per second on GPUs, yet capital and maintenance outlays restrict adoption to larger hubs. CPU-optimized toolkits from Intel offer relief but are still rolling out.[1] Intel, “AI-Driven Medical Imaging Performance on Xeon and Arc Architecture,” intel.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platforms Consolidate Enterprise Workflows

The software tools and platforms segment captured 57.30% of 2025 revenue, underlining its role as the operating layer for algorithm orchestration and lifecycle management across hospital networks. Services are adding value through workflow redesign and post-deployment monitoring and are forecast to post the fastest 31.4% CAGR during 2026-2031. Vendors now bundle implementation, clinical-validation and cybersecurity support, reflecting provider preference for turnkey engagements that minimize disruption. Edge-enabled appliances remain a niche but are gaining traction for stroke and trauma hubs where every second matters. Hospitals appreciate vendor-neutral marketplaces that host dozens of cleared algorithms behind a single sign-on. GE HealthCare’s Genesis stack lets radiologists select applications à la carte and deploy updates without manual re-validation, lowering total cost of ownership and accelerating time-to-benefit GE HealthCare. Such architectures anchor the AI in medical imaging market and will shape procurement for the remainder of the decade.

By Imaging Modality: CT Holds Lead, Ultrasound Rises Fast

CT retained 27.60% share of the AI in medical imaging market in 2025 thanks to its ubiquity in trauma, chest and neuro protocols. Algorithmic triage in stroke care is now standard in many urban stroke centers, shrinking door-to-needle times. Photon-counting CT, newly commercialized, promises sharper cardiac images, opening fertile ground for next-generation models. Ultrasound is projected to outpace all other modalities with a 31.0% CAGR through 2031. Hand-held probes paired with real-time AI guidance help emergency staff locate internal bleeding and assist midwives in fetal-growth checks. The portability of modern devices increases scan frequency, feeding ever larger datasets into training pipelines. MRI and PET continue to see algorithmic gains in noise reduction and quantitative mapping, yet their growth remains tied to scanner throughput constraints and reimbursement complexities.

By Application: Oncology Remains Anchor, Pulmonology Accelerates

Oncology commanded 30.40% of 2025 revenue, cementing its position as the largest use-case cluster within the AI in medical imaging market. Algorithms now delineate tumors, assign TNM stages and estimate therapy response, assisting multidisciplinary boards in treatment planning. Radiomics features extracted by AI also inform early-phase drug trials, shortening discovery cycles for pharma partners. Pulmonology will expand the fastest at 33.5% CAGR during 2026-2031. COVID-19 left health systems with heightened vigilance on respiratory conditions, spurring investment in tools that detect interstitial lung disease, pulmonary embolism and chronic obstructive patterns. AI platforms that scan chest radiographs in community clinics catch abnormalities quickly and route suspicious cases for confirmatory CT, supporting earlier interventions.

By Deployment Model: Cloud Adoption Gains Momentum

On-premise installations still represent 63.20% of current deployments, a legacy of stringent data-security policies and real-time performance needs. Yet the economics of scale now favor hosted models. Cloud-ready archives slash infrastructure refresh costs and enable cross-site reading pools, pivotal for networks coping with staff shortages. The cloud segment is slated to post a 35.4% CAGR through 2031, making it the fastest-growing deployment tier within the AI in medical imaging market. Hybrid architectures bring local caching for urgent studies and cloud elasticity for longitudinal analytics. Philips HealthSuite Imaging on Amazon Web Services illustrates how vendors blend local responsiveness with centralized governance, delivering unified worklists to radiologists irrespective of location

By End User: Hospitals Dominate, Teleradiology Providers Surge

Hospitals and clinics held 70.30% revenue share in 2025, reflecting their ownership of advanced scanners, Picture Archiving systems and specialist expertise. Survey data show almost one-half of large hospitals already use at least one imaging-AI tool in regular practice. They seek unified dashboards that highlight critical cases, automate measurements and feed structured findings into electronic health records. Teleradiology providers will record a 34.9% CAGR, the highest across end-user groups. Regional hubs redistribute workload across time zones so reports arrive before morning rounds. AI accelerates preliminary reads, allowing scarce subspecialists to focus on complex studies while maintaining rapid turnaround. Ambulatory surgery centers and academic institutes adopt AI mainly for workflow efficiency, quality assurance and algorithm-validation research.

Geography Analysis

North America led the AI in medical imaging market with 40.60% share in 2025. Robust health IT infrastructure, proactive FDA clearances and reimbursement pathways bolster adoption. Integrated Delivery Networks rapidly migrate archives to the cloud to pool radiologists and unlock predictive analytics. Canada’s fresh approval of chest and neuro AI applications signals wider regional uptake. Asia is the fastest-growing geography, projected at 32.5% CAGR to 2031. China counts dozens of homegrown cleared devices, and Japan funds nationwide lung-cancer screening that leans heavily on AI triage. South Korea’s national programs display cost-effectiveness that encourages similar rollouts. India advances TB-focused tools for low-resource clinics, highlighting the versatility of AI across income brackets. Europe balances opportunity and caution. The Medical Devices Regulation heightens compliance requirements, yet pan-EU image-exchange guidelines unlock a broader data pool that benefits algorithm robustness. The Nordics pioneer teleradiology to serve remote regions, while France embarks on long-term imaging-value partnerships that incorporate sustainability clauses and research funding.

Regulatory Landscape

Regulation is tightening around imaging AI for Software as a Medical Device (SaMD), while also creating clearer pathways for iterative model updates. In the United States, the FDA has been formalizing how AI-enabled radiology software is classified and reviewed, including the use of Predetermined Change Control Plans (PCCPs). This approach lets manufacturers make pre-authorized modifications under defined controls, rather than treating every update as a new submission.

In June 2026, the FDA published a final order (effective June 17, 2026) that codified radiological machine learning-based quantitative imaging software with a PCCP into Class II with specific special controls. It reinforces lifecycle governance and post-market expectations for adaptive algorithms. Globally, the International Medical Device Regulators Forum (IMDRF) opened public consultation in April 2026 on a Technical Framework for Artificial Intelligence Life Cycle Management (consultation closing July 10, 2026), pointing to continued convergence on risk management, human oversight, and change management across markets.

Value Chain Analysis

The value chain starts with data generation and capture on imaging modalities (CT, MRI, X-ray, ultrasound), then moves into image management (PACS/VNA and enterprise imaging), algorithm development and validation, regulatory clearance, and deployment into clinical workflows. Imaging OEMs such as GE HealthCare, Siemens Healthineers, Philips, and Canon increasingly package AI into modality workstations and enterprise stacks, while AI-native vendors (including Aidoc, Lunit, and Qure.ai) supply condition-specific modules that need integration with existing PACS/RIS/EHR workflows. Cloud and compute layers from hyperscalers and accelerators (including NVIDIA) also matter, particularly as provider groups migrate archives and standardize multi-site reading.

Commercialization and scaling rely on orchestration and governance platforms that manage multi-vendor algorithm marketplaces, monitoring, and updates. Service partners support workflow redesign, cybersecurity, and post-deployment performance tracking. Bottlenecks persist around data liquidity and exchange, as cross-border sharing shifts from fragmented, legacy setups to cloud-enabled exchange. This is happening alongside growing integration and operational burdens when multiple algorithms are deployed across sites, under evolving regulatory expectations such as EU MDR and emerging AI-specific requirements in Europe, while U.S. processes increasingly emphasize PCCP-style lifecycle management for updates.

Competitive Landscape

Competition is vibrant and fragmented. Incumbent modality vendors leverage installed bases to insert AI across scanners, workstations, and cloud suites. GE HealthCare lists 72 FDA-cleared applications, Siemens Healthineers has 64, and Philips holds 27, signaling a deepening feature race. Acquisitions such as GE HealthCare’s purchase of MIM Software expand multimodality integration capabilities and strengthen lock-in.

Specialist firms including Aidoc, RapidAI and Qure.ai innovate rapidly in stroke, trauma and pulmonary use cases. They license modules through vendor-neutral marketplaces and partner with scanner makers to shorten deployment cycles. Yet only a handful of algorithms enjoy clear payment codes, underscoring the immaturity of reimbursement frameworks. Start-ups therefore diversify into decision-support bundles that deliver measurable turn-around time gains, a metric hospitals can monetize internally.

Cloud hyperscalers influence the stack from below, offering AI-optimized storage tiers and federated learning services. These moves lower entry barriers for niche developers and intensify price pressure on proprietary archives, adding another layer to competitive dynamics within the AI in medical imaging market.

AI In Medical Imaging Industry Leaders

Siemens Healthineers AG

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

NVIDIA Corporation

Aidoc Medical Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity lies in lifecycle-managed, continuously improving imaging AI products, supported by clearer regulatory mechanisms for controlled updates. The FDA final order effective June 17, 2026, which codifies radiological machine learning-based quantitative imaging software with a PCCP into Class II with special controls, offers a more structured route for vendors to operationalize frequent model upgrades. That framework better aligns with hospital demand for faster refresh cycles and supports vendor-neutral marketplace strategies.

There is also whitespace in multi-indication workflows and modality expansion beyond single-use tools, particularly where vendors can bundle triage, measurement, and reporting assistance into enterprise platforms. Recent FDA 510(k) clearances reflect this direction, including Philips advancing AI-enabled imaging workflows across CT and ultrasound with new clearances in 2026, and GE HealthCare adding AI-enabled auto-contouring for radiation therapy planning with a PCCP-backed product update. As cloud-first enterprise imaging consolidates, vendors that pair interoperable integration (PACS/VNA and cross-site reading) with governance features such as monitoring, audit trails, and controlled change management are positioned to support provider requirements in oncology, acute triage, and high-volume routine imaging.

Recent Industry Developments

- June 2026: GE HealthCare received US FDA 510(k) clearance for MIM Contour ProtegeAI+ 2.0, expanding AI-enabled auto-contouring for radiation therapy planning and incorporating a Predetermined Change Control Plan. The clearance supports faster, controlled model updates across additional anatomies and workflows, aligning product iteration speed with clinical demands in oncology planning.

- June 2026: Philips received US FDA 510(k) clearance for Elevate Plus for EPIQ Elite and Affiniti ultrasound systems, adding AI and automation designed to standardize routine general imaging exams. The update strengthens ultrasound workflow consistency and reduces operator variability, which is central to scaling point-of-care and high-throughput ultrasound use cases.

- March 2026: GE HealthCare completed its acquisition of Intelerad for USD 2.3 billion to expand cloud-first, AI-enabled enterprise imaging software capabilities. The deal deepens GE HealthCare's position in enterprise imaging infrastructure, strengthening distribution and integration pathways for imaging AI across multi-site provider networks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from AI software and related services that help acquire, process, analyze, or triage medical images used in clinical and research workflows, across common imaging modalities and care settings.

Scope exclusions: We exclude general purpose IT infrastructure, imaging hardware sales that are not AI enabled, and non-imaging AI used only for admin tasks.

Segmentation Overview

- By Offering

- Software Tools / Platforms

- Services

- Hardware / Integrated Solutions

- By Imaging Modality

- X-ray

- Computed Tomography (CT)

- Magnetic Resonance Imaging (MRI)

- Ultrasound

- Positron Emission Tomography (PET) / SPECT

- By Application

- Oncology

- Neurology

- Cardiology

- Musculoskeletal and Orthopedics

- Breast Imaging

- Pulmonology

- By Deployment Model

- On-premise

- Cloud / Web-based

- Hybrid

- By End User

- Hospitals and Clinics

- Diagnostic Imaging Centers

- Ambulatory Surgery Centers (ASC)

- Research and Academic Institutes

- Teleradiology Providers

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Chile

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Nordics (Sweden, Norway, Finland, Denmark)

- Rest of Europe

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Asia Pacific

- China

- India

- Japan

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the addressable imaging workflow and the AI components that can be priced and sold, and then aligning this with how healthcare spending is reported publicly. We referenced non-paywalled sources such as the World Health Organization, OECD health statistics, the US FDA device databases for AI enabled imaging clearances, the National Institutes of Health publications, and radiology association websites that discuss procedure and workload trends.

To make the model practical, we also reviewed company annual reports, investor decks, earnings call transcripts, and reputable press coverage on AI deployments in radiology and imaging centers. In a few cases, we used a paid subscription focused on company financials and another on patents to confirm product direction and monetization signals, which we then checked against public statements. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how AI in imaging is bought and deployed, including license structures, service attachments, and how adoption differs by modality and care setting. We spoke with a mix of solution providers, hospital and diagnostic imaging buyers, and clinical users across major regions, so our assumptions on penetration, pricing, and replacement cycles could be adjusted to observed purchasing behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 20% | APAC: 47% |

| Mid tier: 51% | Functional/Unit leaders: 33% | EMEA: 31% |

| Smaller Players: 22% | Managers: 47% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool reconstruction, where imaging procedure intensity, installed base of imaging systems, and realistic AI attach rates were used to form the paid adoption base by modality and end user. After that, revenue was derived by applying observed price ranges for software tools or platforms and the typical services mix that comes with implementation and support.

To keep the totals grounded, the model was corroborated through selective bottom-up checks using supplier revenue disclosures, sampled contract structures from interviews, and simple volume times ASP sanity checks for high adoption use cases (for example, triage and detection in CT and X-ray). Key inputs that were monitored include regulatory clearance momentum for imaging AI, cloud versus on-premise deployment preference, hospital budget cycles for radiology IT, modality level workflow bottlenecks, and the pace of reimbursement and guideline support in major markets. Forecasts used scenario analysis supported by expert views, with assumptions varied for adoption speed, price compression, and services share as deployments scale.

Data Validation & Update Cycle

Outputs were checked against independent signals such as diagnostic imaging utilization trends, known rollout patterns in large hospital groups, and the implied spend per site based on interview inputs. When a segment result looked unusual, the driver assumptions were revisited, and follow-up outreach was triggered to confirm if the variance was real or model driven.

Before sign-off, the file goes through multi-step analyst review, so definitions, arithmetic, and currency conversions are consistent across regions and years. Reports are refreshed annually, and interim updates are made when material events occur, such as major policy shifts or sudden demand changes. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Medical Imaging AI Market Estimate Compared With Other Published Estimates

Published figures for AI in medical imaging often do not match, even when the topic name looks the same at first glance. The gaps usually come from what is counted as part of imaging AI revenue, the year used for currency conversion, and how quickly adoption is assumed to spread across modalities and sites.

Some estimates fold in a wider bundle that can include broader AI systems and adjacent digital health layers sold around imaging workflows. In Mordor Intelligence, the model counts only AI software tools or platforms and related services that are directly used for medical image acquisition, processing, and interpretation, and it keeps imaging hardware and generic hospital IT outside the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.65 B (2025) | |

| Global Consultancy A | USD 1.80 B (2025) | Typically uses a broader segment map that can include a wider set of AI product categories, and the pricing path often assumes faster platform upsell across multiple applications in the same site. |

| Industry Publisher B | USD 1.92 B (2025) | Often includes systems level revenue and a wider services bundle, and assumptions on average deal size can be set using aggressive enterprise rollout scenarios with fewer checks against modality level adoption timing. |

The spread in the table is mainly explained by category coverage and how quickly prices and adoption are scaled across hospitals and imaging centers. By keeping the revenue lines tied to clear imaging AI use cases and then checking penetration and ASP logic through interviews and simple cross-checks, the estimate stays traceable to inputs a buyer can follow and reproduce.

Key Questions Answered in the Report

What is the current size of the AI in medical imaging market?

The AI in medical imaging market size is USD 2.16 billion in 2026 and is forecast to reach USD 8.23 billion by 2031.

Which segment leads the market by offering?

Software platforms hold the largest 57.30% share, thanks to their role in orchestrating algorithms across PACS and cloud archives.

What modality is growing fastest?

Ultrasound is projected to register a 31.0% CAGR from 2026-2031, driven by point-of-care applications and real-time AI guidance.

Why is Asia the fastest-growing region?

Government-mandated cancer-screening programs and accelerated device approvals are pushing Asia to a 32.5% regional CAGR.

Which region has the biggest share in AI In Medical Imaging Market?

In 2025, the North America accounts for the largest market share in AI In Medical Imaging Market.

How does cloud deployment benefit providers?

Cloud archives cut infrastructure costs and let radiologists collaborate across sites, supporting a 35.4% CAGR for the deployment model.

Are AI tools reimbursed today?

Only a handful of algorithms have explicit payment codes, but providers justify investments through productivity gains and reduced turnaround times.

Page last updated on: