Market Overview

| Study Period | 2020 - 2031 |

|---|---|

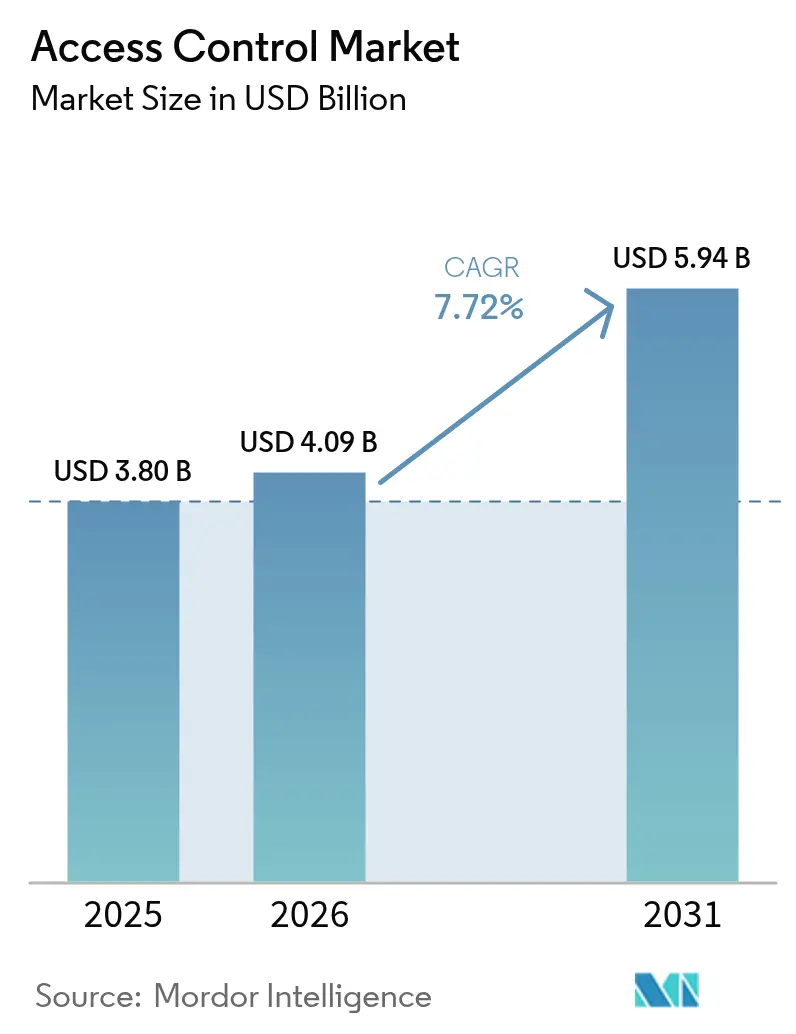

| Market Size (2026) | USD 4.09 Billion |

| Market Size (2031) | USD 5.94 Billion |

| Growth Rate (2026 - 2031) | 7.72% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Access Control Market Analysis by Mordor Intelligence

The access control market size in 2026 is estimated at USD 4.09 billion, growing from 2025 value of USD 3.80 billion with 2031 projections showing USD 5.94 billion, growing at 7.72% CAGR over 2026-2031. Demand is intensifying as cloud management, mobile credentials and biometrics replace legacy keys and cards across corporate, public-sector and critical-infrastructure facilities. Stricter data-protection regulations, the premium placed on contactless user experiences and convergence with video surveillance are reinforcing the upgrade cycle. Price escalations linked to semiconductor shortages are nudging buyers toward software-defined architectures that future-proof capital expenditure while mitigating supply-chain risk.

Key Report Takeaways

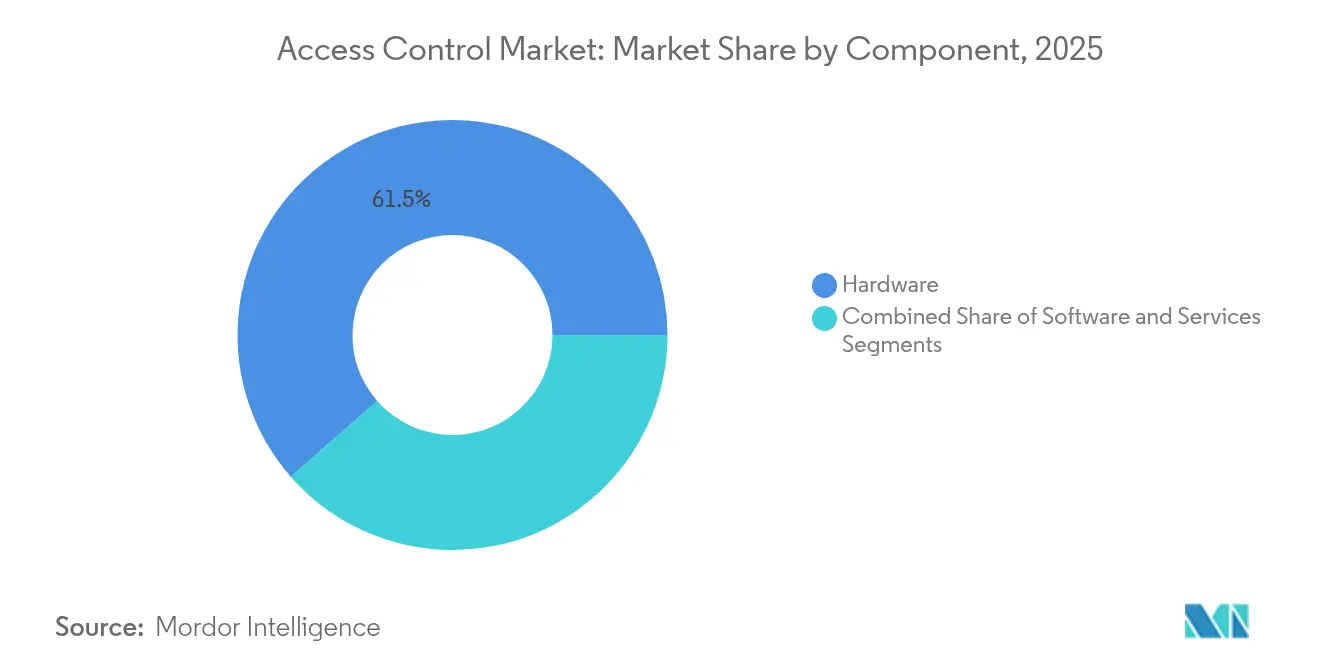

- By component, hardware led with 61.45% revenue share in 2025; software is forecast to expand at a 8.78% CAGR to 2031.

- By ACaaS deployment, hosted models captured 51.60% of the access control market share in 2025, while hybrid ACaaS is projected to grow at 8.35% CAGR through 2031.

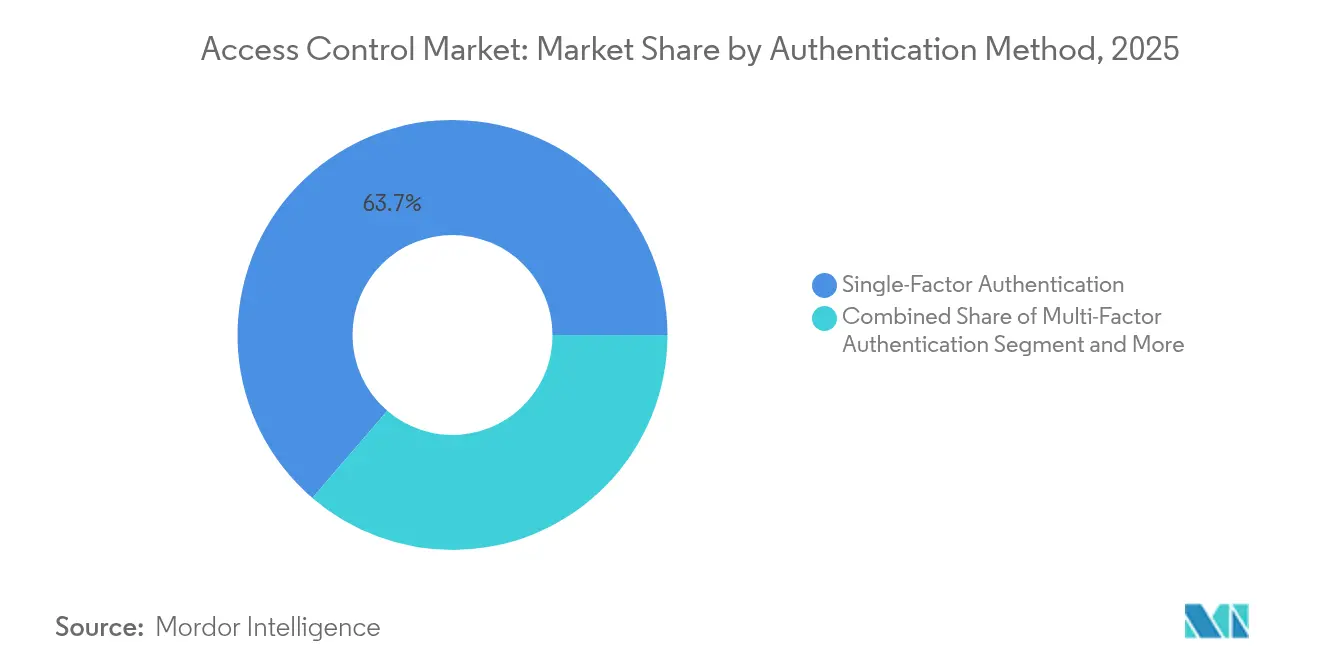

- By authentication method, single-factor systems held 63.70% share in 2025; mobile credential technologies are advancing at an 7.95% CAGR.

- By connectivity, RFID/NFC retained 57.75% share in 2025; ultra-wideband solutions are scaling at 8.22% CAGR.

- By end-user, commercial buildings led with 31.10% of access control market size in 2025; healthcare facilities are expanding at 8.41% CAGR.

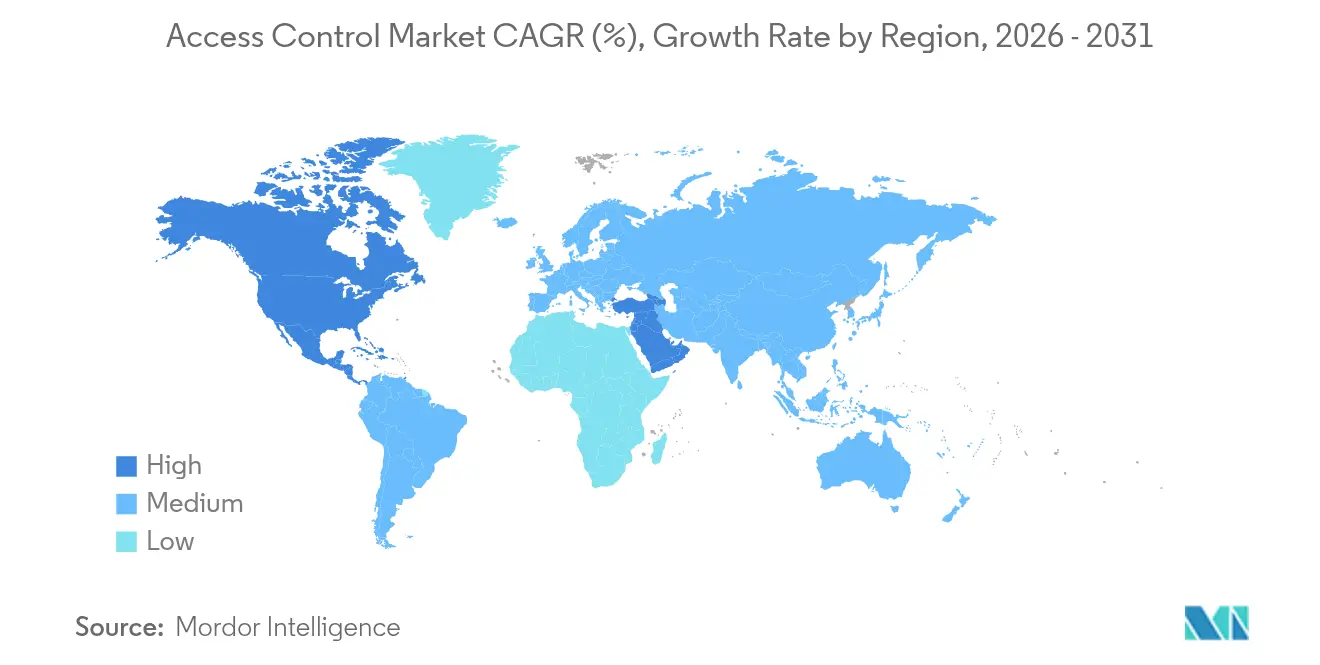

- Regionally, North America commanded 38.30% share in 2025; the Middle East is growing the fastest at 9.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Access Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Mandates for Electronic Access in GDPR-Sensitive EU Data Centers | +1.8% | Europe, with spillover to North America | Medium term (2-4 years) |

| Contactless Mobile Credential Uptake in North American Corporate Real-Estate | +1.5% | North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Smart-City and Critical-Infrastructure Programs Boosting Biometrics in the Middle East | +1.2% | Middle East, with early adoption in UAE and Saudi Arabia | Long term (≥ 4 years) |

| Expansion of APAC Co-working Spaces Driving Cloud-Based ACaaS | +1.0% | Asia-Pacific core, with spillover to global markets | Medium term (2-4 years) |

| IP Video–Access Control Convergence Upgrades at European Transport Hubs | +0.9% | Europe, with selective adoption in North America | Medium term (2-4 years) |

| Retrofit Demand from Ageing Key-Card Systems in US Higher-Education | +0.8% | North America, with similar trends in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for Electronic Access in GDPR-Sensitive EU Data Centers

The NIS2 directive, effective October 2024, requires multi-factor authentication and tamper-resistant audit trails across every physical entry point. Data-center operators are accelerating migration from legacy cards to biometric or mobile credentials to meet encryption and continuous-monitoring clauses. Vendor supply-chain scrutiny raises procurement thresholds, steering demand toward platforms offering automated compliance reporting. Synergies between NIS2 and GDPR are creating a premium for unified solutions that protect personal data while enforcing physical security, lifting overall replacement budgets across the access control market.[1]Cisco, “Products – NIS2 Compliance for Industries White Paper,” cisco.com

Contactless Mobile Credential Uptake in North American Corporate Real-Estate

Commercial landlords are issuing Apple Wallet and Google Pay credentials that unlock turnstiles, elevators and suites without physical interaction. Remote provisioning cuts badge issuance costs and supports flexible seating policies. Encrypted over-the-air updates let facility teams deactivate lost phones instantly, tightening security while enhancing tenant experience. The solution’s compatibility with existing smartphone infrastructure eliminates card-printer overheads, strengthening its business case. Fast deployment cycles translate into visible gains in operational efficiency, reinforcing momentum for the access control market.[2]Soloinsight, “Mobile Credentials,” soloinsight.com

Smart-City and Critical-Infrastructure Programs Boosting Biometrics in the Middle East

The UAE’s plan to replace physical IDs with nationwide biometric verification is catalyzing large-scale facial and iris systems across government, healthcare and transportation campuses. Saudi Arabia’s border-control upgrade processes 120,000 fingerprint transactions daily, underscoring regional appetite for high-throughput biometric access. These flagship projects have lowered risk perception around multi-modal biometrics, encouraging private developers to adopt similar solutions. Favorable regulatory stances that prioritize security over privacy speed procurement, positioning the Middle East as an innovation sandbox that influences global access control market specifications.

Expansion of APAC Co-working Spaces Driving Cloud-Based ACaaS

Rising flexible-workspace penetration across South Korea, Japan and India demands scalable, subscription-driven access control as a service that automates member onboarding and billing synchronously with booking apps. [3]Airfob, “Why Access Control is the Secret to Coworking Profitability in the UK?” airfob.com Hosted ACaaS eliminates server ownership, lowering capex for operators opening multiple locations in rapid succession. Real-time utilization analytics feed dynamic pricing models, reinforcing revenue management. Hybrid deployments that cache credentials locally satisfy data-sovereignty regulations while preserving cloud analytics, widening enterprise adoption. This use case keeps the access control market on a steady upward curve, particularly among technology-savvy founders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security Compliance Costs for EU Cloud Deployments (NIS2) | -1.2% | Europe, with regulatory spillover effects | Medium term (2-4 years) |

| Secure MCU Chip Shortages Affecting Reader Shipments | -0.9% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Privacy Pushback on Facial Recognition in US and EU States | -0.8% | North America and Europe | Long term (≥ 4 years) |

| SME Budget Constraints in South America | -0.6% | South America, with selective impact in other emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Compliance Costs for EU Cloud Deployments (NIS2)

Cloud-hosted access platforms must add continuous threat-monitoring, secure code-signing and documented development pipelines to satisfy NIS2, lifting vendor operating costs by 15–20%. Small providers struggle to absorb audit fees and penetration-test expenses, triggering consolidation as buyers gravitate toward global brands with certified infrastructure. Some EU enterprises defer upgrades, stretching the replacement cycle, which marginally tempers the access control market growth outlook.

Secure MCU Chip Shortages Affecting Reader Shipments

Tight supply of cryptographic MCUs extends lead times for biometric and multi-tech readers to 16 weeks, prompting OEM list-price increases of 3.5-15%. ASSA ABLOY raised electronic product prices 9.9% in 2024 to offset component inflation. Project delays erode installer margins and complicate budgeting for education and healthcare clients. Accelerated redesigns around alternative chips divert engineering resources from innovation pipelines, modestly suppressing near-term access control market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Innovation Drives Hardware Dominance

Hardware led 2025 revenue with 61.45% share, reflecting the essential need for electronic locks, controllers and biometric readers in physical deployments. University retrofits alone drove substantial lock refresh cycles as campuses shifted to mobile-ready infrastructure. Electronic locks posted the fastest unit growth, powered by ultra-wideband modules that enable hands-free entry. Biometric multi-sensor readers gained traction in laboratories and pharmacies demanding high-assurance verification.

Software is growing at 8.78% CAGR to 2031, adding predictive analytics and AI-driven anomaly detection to management consoles. Cloud control planes unify disparate sites, allowing real-time policy pushes and automated compliance audits. Video-access convergence within dashboards strengthens investigative capabilities, while open APIs invite ecosystem development. Integration services and recurring support contracts widen partner revenue, positioning managed services as a resilient annuity layer within the access control industry.

By ACaaS Deployment: Hybrid Models Gain Enterprise Traction

Hosted ACaaS controlled 51.60% of 2025 deployments, driven by SMEs favoring predictable subscriptions over server ownership. Feature parity with on-prem solutions, plus automatic updates, reduces the skills burden for lean IT departments. Granular tenant portals help co-working brands manage thousands of members dynamically, deepening customer loyalty within the access control market.

Hybrid ACaaS is the fastest-growing model at 8.35% CAGR, balancing cloud orchestration with local edge storage for regulated entities. Hospitals route sensitive logs to on-site appliances during network outages, then synchronize to the cloud for analytics once connectivity returns. Managed ACaaS retains a niche for complex, multi-vendor estates needing bespoke integrations, but platforms are steadily converging toward self-service paradigms that scale across sectors in the wider access control market.

By Authentication Method: Mobile Credentials Challenge Single-Factor Dominance

Single-factor systems still hold 63.70% adoption through widespread key cards and numeric pads catering to basic perimeter security. However, regulatory pressures and high-profile breaches expose their limitations. Replacement cycles accelerate in finance, pharma and critical infrastructure where tamper evidencing and traceability are paramount.

Mobile credentials packaged inside Apple Wallet or Google Pay are rising at 7.95% CAGR, delivering encrypted Bluetooth and NFC exchanges that resist cloning. Administrators provision or revoke rights instantly over the air, lowering operational cost per user. Multi-factor deployments layering biometrics atop mobile IDs deliver frictionless yet strong authentication, steering the overall access control market toward converged identity paradigms.

By End-User Vertical: Healthcare Drives Fastest Growth

Commercial facilities generated 31.10% of access control market size in 2025 as landlords aligned security upgrades with sustainability retrofits. Integrated mobile access and space-analytics tools optimize tenant engagement while lowering badge issuance toil.

Healthcare settings, posting 8.41% CAGR, implement role-based permissions for pharmacies, operating theaters and record rooms in line with HIPAA policy. Contactless biometrics support infection-control regimes, while emergency lockdown features enhance threat response. Industrial, government and transport hubs maintain specialized demand for ruggedized, OT-friendly readers, sustaining long-tail growth for the broader access control market.

Geography Analysis

North America maintained 38.30% 2025 revenue share underpinned by large-scale modernizations in corporate campuses, universities and hospitals. US higher-education retrofits, such as the University of Kentucky’s 9,000-door conversion, illustrate campus-wide embrace of mobile-ready platforms that blend access control with attendance analytics. Canada’s smart-building incentives and Mexico’s cross-border logistics facilities add incremental demand. Venture investment in UWB and biometric startups keeps the region at the forefront of technology innovation within the access control market.

The Middle East is the fastest-growing territory at 9.22% CAGR through 2031, lifted by sovereign smart-city agendas and security-first regulatory frameworks. UAE and Saudi Arabia demonstrate large-scale rollouts of facial, iris and fingerprint systems that replace physical IDs, while Qatar and Oman embed access control into nationwide IoT command centers. Local integrators build on global vendor SDKs, creating region-specific solutions that accelerate market localization.

Europe exhibits steady growth despite stringent privacy legislation. NIS2 and the EU AI Act require explicit consent and transparency for biometric use. Organizations respond by adopting hybrid ACaaS so that sensitive biometric templates remain on European soil. Germany, France and the UK prioritize open-protocol systems to avoid vendor lock-in, while Nordic operators pioneer sustainable, low-power readers. Eastern European transport hubs upgrade card-based barriers with mobile and video-verified entry, all contributing to incremental access control market revenue.

Regulatory Landscape

Access control deployments are increasingly shaped by public-sector cybersecurity baselines and privacy-by-design requirements that link physical entry systems to audit-ready identity governance. In the United States, NIST finalized SP 800-53 Release 5.2.0 in August 2025, adding resiliency and software assurance controls that cascade into procurement requirements for security systems used in federal and critical-infrastructure environments. In June 2026, the U.S. General Services Administration updated ADM 3490.1 to mandate baseline minimum security standards for federally owned facilities, reinforcing requirements for standardized countermeasures for intrusion detection and related security systems.

In Europe, policy and standards are tightening around biometric processing and AI-enabled security, raising the bar for consent, transparency, and secure handling of sensitive templates. CEN/TC 224 published CEN/TR 18241:2026 in January 2026 to guide privacy-by-design for biometric access control products under GDPR Article 25. Separately, the EU AI Act high-risk system timeline for Annex III use cases (including biometric identification and critical infrastructure monitoring) saw a provisional legislative update in May 2026 that extended the deadline from August 2, 2026 to December 2, 2027. The change introduces timing uncertainty that influences vendor roadmaps and buyer rollout sequencing for AI-assisted biometrics.

Competitive Landscape

The market remains moderately fragmented, yet consolidation momentum is clear as leading manufacturers deepen vertical integration. Honeywell’s USD 4.95 billion purchase of Carrier’s Global Access Solutions unit in 2024 delivered LenelS2, Onity and Supra brands, boosting annual sales by USD 1 billion. ASSA ABLOY followed with successive acquisitions of SKIDATA, 3millID and Third Millennium, broadening reader portfolios and parking-access capabilities.

Strategic alliances reinforce technology differentiation. Allegion spearheaded the Aliro mobile-access protocol with the Connectivity Standards Alliance to foster interoperability and lock in smartphone ecosystems. The FiRa Consortium unites chipset, handset and lock vendors around UWB secure ranging standards, reducing integration friction and accelerating premium-tier deployments.

Financial results confirm pivot toward electronic and software revenues. Allegion’s Q1 2025 Americas segment grew 5.4% on strong electronic access uptake. Dormakaba delivered 4.9% organic Access Solutions growth by optimizing pricing amid component inflation. Vendors funnel expanded gross profit into AI, edge computing and privacy-by-design R&D, setting the competitive tone for the access control market.

Access Control Industry Leaders

Suprema Inc.

Hanwha Techwin Co. Ltd

Thales Group (Gemalto NV)

Bosch Security System Inc.

Honeywell International Inc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is opening where buyers are moving from siloed hardware to unified, software-defined security operations that combine access control, video, and identity data under common governance. In 2026, trade-channel and survey-based indicators suggest this shift is already visible, with 60% of security respondents reporting use of unified or integrated security platforms, and SDM pointing to mobile credentials, biometrics, unification, and cybersecurity as core growth drivers for access control upgrades. This favors vendors and integrators that can deliver open-ecosystem deployments (APIs, multi-vendor interoperability) and hybrid-cloud architectures that keep sensitive logs or biometric templates local while enabling centralized policy and reporting.

Standards activity and rising incident pressure also support opportunity around auditability and access hygiene, especially for distributed enterprises and content-sensitive environments. EN ISO/IEC 29146:2026, published in March 2026, frames access management for networked ICT environments and reinforces alignment between logical access controls and physical access controls, strengthening the business case for identity-centric, Zero Trust style implementations that link door events to broader IAM workflows. Separately, the Trusted Partner Network reported in April 2026 that Q1 2026 Security Alerts exceeded the total for all of 2025, pointing to elevated exposure from credential-based attacks and misconfigurations. That backdrop is driving demand for stronger credential lifecycle management, automated policy enforcement, and continuous monitoring across both physical and cyber domains.

Recent Industry Developments

- July 2026: Suprema released the XPass Q2 multi-technology access control reader supporting QR, barcode, RFID, and mobile credentials, designed to work with its BioStar X platform. The launch expands credential optionality for mixed-use sites that need visitor QR flows alongside employee RFID and mobile IDs. It also reinforces the shift toward unified platforms that simplify deployments across diverse end-user environments.

- October 2025: Thales received a high-level Common Criteria EAL6+ certification from ANSSI for its MultiApp 5.2 Premium PQC quantum-resistant smartcard for digital identities. This strengthens Thales's position in high-assurance credential ecosystems that can be used for both physical and logical access. Post-quantum readiness and independent certification raise the compliance bar for identity-backed access control deployments in regulated environments.

- November 2024: Hanwha Vision formed a strategic partnership with Morphean to deliver direct-to-cloud video surveillance solutions. Cloud video integrations support broader security platform consolidation, enabling tighter operational coupling between video verification and access control events. The partnership aligns with growing preference for hosted and hybrid architectures that reduce on-site infrastructure while preserving centralized management.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the access control market covers revenues from systems that control and track physical entry and movement in buildings and sites, including hardware, software, and related services, across major regions.

Scope exclusions: pure cybersecurity identity and access management for software logins, when it is not tied to physical entry control use cases, is not counted.

Segmentation Overview

- By Component

- Hardware

- Card / Proximity / Smart-card Readers

- Biometric Readers (Fingerprint, Face, Iris, Multimodal)

- Electronic Locks (Magnetic, Electric Strike, Deadbolt, Wireless Smart Lock)

- Controllers and Panels

- Software

- Access Control Management Suites

- Video Management Integration Plug-ins

- Services

- Installation and Integration

- Support and Maintenance

- Hardware

- By Access Control-as-a-Service (Deployment)

- Hosted ACaaS

- Managed ACaaS

- Hybrid ACaaS

- By Authentication Method

- Single-Factor Authentication

- Multi-Factor Authentication

- Mobile Credential / Bluetooth LE

- By Connectivity Technology

- RFID / NFC

- Smart Cards (125 kHz, 13.56 MHz)

- Bluetooth Low Energy

- Ultra-Wideband (UWB)

- By End-User Vertical

- Commercial Buildings

- Industrial and Manufacturing

- Government and Public Sector

- Transport and Logistics

- Healthcare Facilities

- Military and Defense Installations

- Residential and Smart Homes

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- GCC

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a fact base on construction activity, public safety spend, and security equipment demand, then mapping how these signals translate into access control adoption.

Public sources were used to anchor assumptions, such as World Bank and OECD macro indicators, UN Comtrade trade statistics for relevant electronics categories, and government procurement portals that show tender volumes for building security upgrades. To keep the model grounded, we also reviewed standards and guidance notes from NIST, plus trade and association materials that describe physical security practices and certification. Company annual reports, investor presentations, and press releases were used to understand product mix shifts, for example hardware versus software and service attach rates.

Where available, we referenced paid database subscriptions for company financials and intelligence, patent databases, and shipment-level import and export checks to validate directionally. These desk research sources are illustrative rather than exhaustive, and additional public and paid references were used to collect and cross-check data.

Primary Interviews and Surveys

Primary work focused on validating what gets deployed and what customers pay for, since access control pricing can vary by site type, credential choice, and integration depth. We spoke with manufacturers, system integrators, distributors, facility security heads, and large end users across APAC, EMEA, and the Americas, so the model reflects how projects are specified, installed, and renewed.

Respondent input was used to close gaps in service attach assumptions, the cloud versus on-premises mix, and realistic ASP progression by device class and contract type.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 19% | APAC: 39% |

| Mid tier: 55% | Functional/Unit leaders: 23% | EMEA: 36% |

| Smaller Players: 19% | Managers: 58% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using top-down reconstruction first, translating construction and retrofit activity, security spending signals, and installed base expansion into demand for readers, controllers, locks, software licenses, and services across regions. The totals were then corroborated with selective bottom-up approximations, such as sampling typical site volumes, applying observed ASP ranges by device type, and cross-checking against supplier revenue splits, with adjustments when the two views disagreed.

Key inputs in the model included new commercial floor space additions and retrofit rates, government and critical infrastructure upgrade programs, penetration of mobile credentials and multi-factor authentication in new installs, cloud hosted deployment adoption, and service renewal behavior (maintenance, software updates, and managed access control). Because unit pricing can shift with hardware refresh cycles and component cost changes, ASPs were treated as a tracked assumption by product group and refreshed using recent project quotes and distributor feedback.

Forecasting used scenario analysis supported by regression-style checks, linking growth to construction cycles, public safety budgets, and technology adoption curves, then moderating outcomes using what interviewees indicated about lead times and project conversion. Where country-level bottom-up inputs were thin, we applied peer-market proxies based on building stock and security spend signals, then revalidated the outputs with regional expert feedback before finalizing.

Data Validation & Update Cycle

Results were validated through multiple checks, including comparing regional totals with independent signals such as construction activity, import patterns for access control electronics, and the expected split of hardware, software, and services. When large variances appeared, assumptions were reopened and rechecked, and follow-up calls were triggered to confirm whether the issue came from scope, pricing, or deployment mix.

Before sign-off, the model goes through multi-step analyst review, with checks on calculations, conversion logic, and unit economics assumptions for internal consistency. Reports are refreshed annually, and interim updates are made when material events occur, for example supply shocks, policy changes, or major pricing resets. Right before delivery, a final pass is performed to reflect the latest available information.

Mordor Intelligence's Global Access Control Market Market Size Compared Against Other Published Estimates

Published market sizes for access control can vary widely, even when they appear to measure the same thing, because the boundary between physical access control, logical access control, and adjacent security categories is handled inconsistently. Differences also arise from how firms treat services, how they update pricing, and which year and currency conversion timing they use.

In this study, the refresh cadence and exchange-rate timing are kept aligned to the stated market year, and hardware ASPs are revalidated against recent project quotes and channel feedback before totals are finalized. This is also why the 2026 value in Mordor Intelligence stays closer to a physical access control demand pool rather than a broader access management definition.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.09 B (2026) | |

| Global Consultancy A | USD 11.62 B (2025) | Uses a broader access control framing that includes logical access control types and wider application coverage, which inflates the value versus a physical entry control-only boundary. The base year is different, and pricing is often carried forward with less frequent ASP refresh checks by device class. |

| Industry Publisher B | USD 10.76 B (2024) | Anchors to an earlier year and tends to aggregate access control with adjacent security software and services under offering buckets, which can pull in spend beyond door-level control. Currency timing and the historical window used can also shift the start value upward when older ASPs are not fully normalized. |

Across the three figures, most of the spread comes from what is counted as access control and when price and currency assumptions are frozen. By keeping scope tied to physical access control components and by regularly rechecking ASPs and mix shifts during updates, the estimate stays traceable to clear demand indicators and repeatable steps.

Key Questions Answered in the Report

What is the current size of the access control market and its growth outlook?

The global access control market size stands at USD 4.09 billion in 2026 and is forecast to reach USD 5.94 billion by 2031 at an 7.72% CAGR.

Which region is expanding the fastest?

The Middle East is projected to grow at a 9.22% CAGR through 2031, driven by government-backed biometric programs and smart-city investments.

Why are mobile credentials gaining traction?

Mobile IDs eliminate physical card management, enable encrypted over-the-air provisioning and align with hybrid work patterns, supporting an 7.95% CAGR adoption rate.

How are semiconductor shortages affecting the market?

Secure MCU constraints are extending reader lead times to 16 weeks and have triggered 3.5-15% price increases, moderating short-term hardware growth.

Page last updated on: