UCaaS In Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

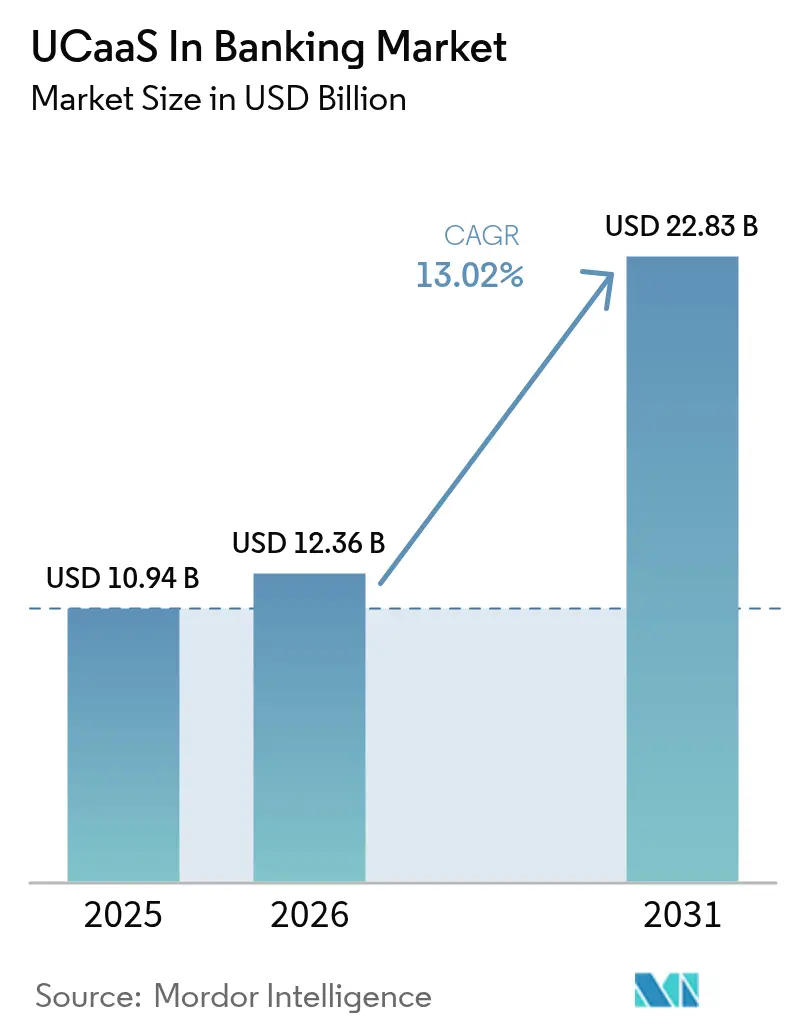

| Market Size (2026) | USD 12.36 Billion |

| Market Size (2031) | USD 22.83 Billion |

| Growth Rate (2026 - 2031) | 13.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UCaaS In Banking Market Analysis by Mordor Intelligence

The UCaaS in banking market size was valued at USD 10.94 billion in 2025 and estimated to grow from USD 12.36 billion in 2026 to reach USD 22.83 billion by 2031, at a CAGR of 13.02% during the forecast period (2026-2031). The expansion reflects a decisive industry shift toward cloud-native communications that sustain hybrid workforces and satisfy strict regulatory audit trails[1]Orange Business Services, “The Future of Banking: How Digital Transformation Enhances Customer Experience,” digital.orange-business.com. Heightened demand for seamless customer engagement, accelerated fintech partnerships, and accelerated time-to-market for new digital products further uplift adoption. Public-cloud UCaaS remains pervasive, yet hybrid architectures are gaining ground as banks seek fine-grained data-sovereignty control without forfeiting the flexibility of elastic capacity. Strategic deployments—such as Barclays’ global roll-out of Microsoft Teams—spotlight how integrated platforms rationalize legacy voice estates, consolidate collaboration tools and contain total cost of ownership. Competitive intensity is shaped by telecom incumbents battling cloud-native specialists that embed artificial-intelligence (AI) functions such as real-time language translation, sentiment scoring and compliance surveillance.

Key Report Takeaways

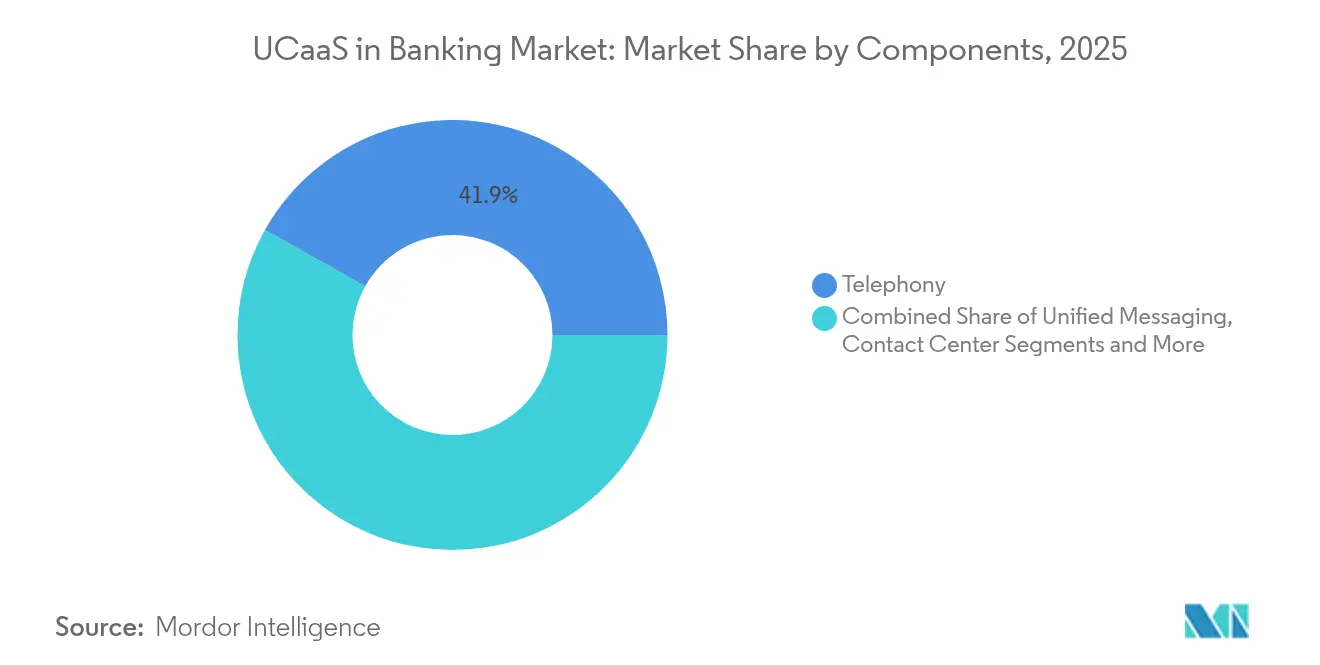

- By component, telephony retained 41.88% of UCaaS in banking market share in 2025, while collaboration platforms are set to accelerate at an 18.04% CAGR through 2031.

- By deployment model, public-cloud captured 60.72% share of the UCaaS in banking market size in 2025; hybrid-cloud is projected to expand at 18.74% CAGR between 2026-2031.

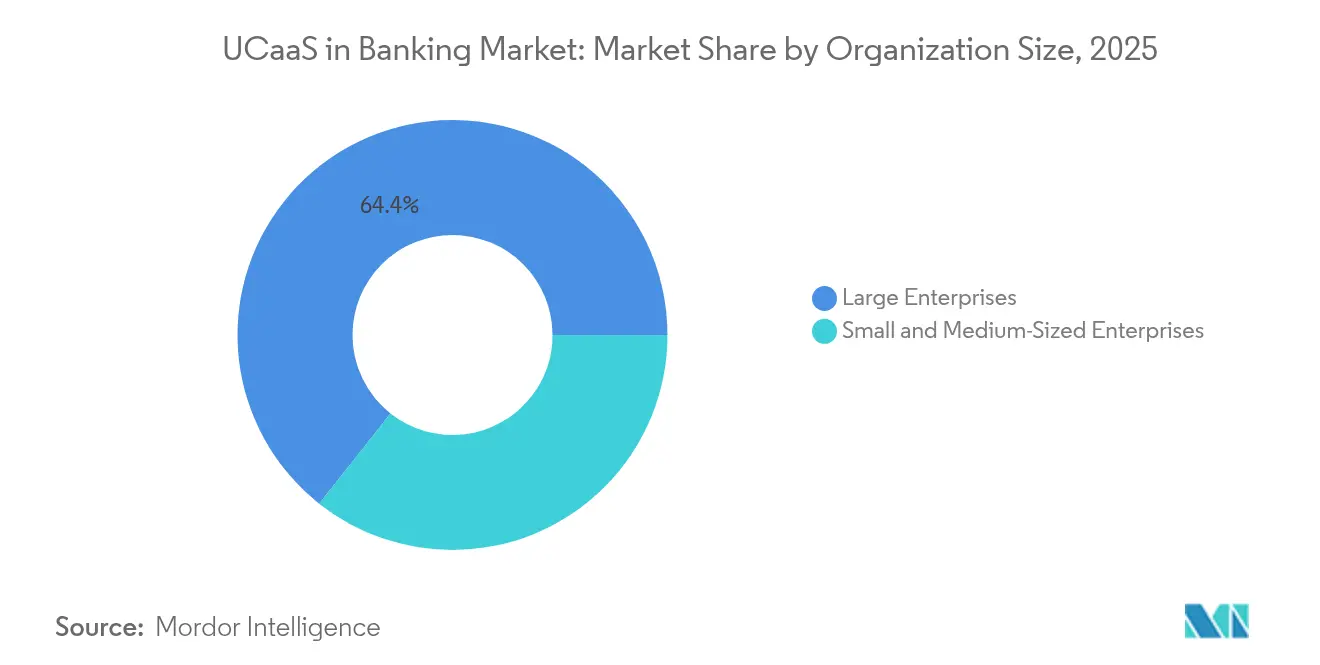

- By organization size, large enterprises commanded 64.35% of UCaaS in banking market size in 2025, whereas SMEs are projected to rise at a 19.55% CAGR to 2031.

- By banking application, retail banking held 44.12% of UCaaS in banking market share in 2025; corporate and wholesale banking is forecast to advance at 16.72% CAGR through 2031.

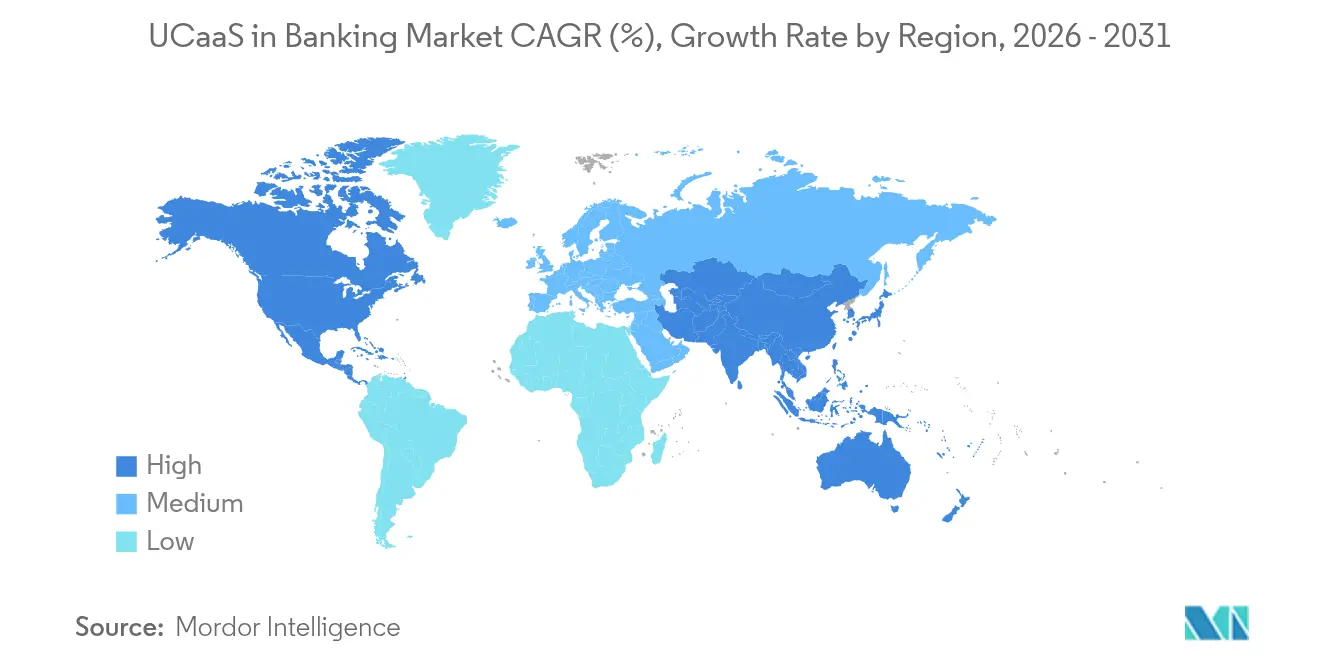

- By geography, North America held 36.25% of UCaaS in banking market share in 2025; Asia-Pacific is forecast to advance at 14.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global UCaaS In Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BYOD and workforce mobility | +2.8% | Global; higher in North America and Europe | Medium term (2-4 years) |

| Enterprise-wide UC integration | +2.1% | Global; strong in Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Digital-only banking expansion | +3.2% | Primarily Asia-Pacific; spill-over to MEA and LatAm | Short term (≤ 2 years) |

| AI-enabled UCaaS for compliance monitoring | +1.9% | North America and EU; expanding to Asia-Pacific | Medium term (2-4 years) |

| 5G private branch networks | +1.4% | Global; early in developed markets | Long term (≥ 4 years) |

| Embedded CPaaS in banking apps | +2.6% | Global; stronger in digital-first markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BYOD and Workforce Mobility

Banking institutions are dismantling desk-phone dependencies as hybrid workforces normalize personal device use. UCaaS tools that encrypt traffic end-to-end, enforce role-based policies and federate identity allow staff to connect from any location without jeopardizing compliance. Mizuho Securities’ decision to migrate external communications to Zoom under an active-host billing model underscores how flexible licensing reduces dormant seat costs while sustaining auditability. BYOD strategies cut hardware outlays and elevate employee satisfaction, yet they demand advanced mobile-device-management and geo-fencing to meet sectoral data-loss-prevention rules. The interplay between mobility enablement and UCaaS security solidifies competitive advantage for banks able to blend flexibility with rigorous supervision.

Need for Enterprise-wide UC Integration

Historically, siloed voice, chat and trading-floor channels obstructed fluid collaboration. Contemporary UCaaS platforms unify these touchpoints and embed workflow triggers so alerts and documents flow between branches, contact centers and compliance desks. NTT Communications underpins more than 190 countries with a single-tenant global UC fabric, allowing multinational banks to standardize dial plans, reporting and policy enforcement while trimming maintenance overhead. Integration imperatives intensify during mergers, when newly acquired branches must migrate rapidly. Leading solutions now apply AI to route queries to the best-suited specialist, elevating first-call-resolution metrics and optimizing workforce allocation. Unified lineage across channels also simplifies e-discovery requests, which regulators expect within hours.

Digital-only Banking Expansion

Neobanks launch without legacy PBX anchors, favoring cloud APIs that embed chat, voice and video in their mobile apps. Unity Metro Bank’s WhatsApp wallet illustrates how conversational interfaces double as transaction rails, blending engagement and payments. High-growth entrants demand subscription models that scale parallel to customer onboarding peaks, making pay-as-you-grow UCaaS contracts attractive. AI chatbots provide always-on assistance, while event-driven messaging instantly confirms transfers or fraud flags. The digital-first dynamic is most pronounced in Southeast Asia and Latin America, where smartphone banking leapfrogs branch-centric channels. Vendors that offer low-code orchestration and pre-certified compliance modules are positioned to capture this surge.

AI-Enabled UCaaS for Compliance Monitoring

Financial watchdogs broaden scope beyond voice capture to include video, screen sharing and encrypted chat. NICE Actimize’s SURVEIL-X monitors 100% of regulated employee communications across 150+ languages and myriad apps, using natural-language-processing to curb misconduct before it triggers penalties. Generative AI overlays now furnish real-time coaching prompts, instructing agents to avoid restricted phrasing. Banks benefit from reduced false-positive caseloads and expedited case closure. As regulatory fine sizes escalate, proactive surveillance shifts from optional to mandatory—cementing AI-infused UCaaS as a compliance backbone rather than a productivity add-on.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low cloud-UC awareness in tier-2/3 banks | -1.8% | Global; most acute in emerging markets | Medium term (2-4 years) |

| Stringent data-security and residency mandates | -2.1% | EU and selectAsia-Pacificjurisdictions | Long term (≥ 4 years) |

| Legacy on-prem PBX lock-ins | -1.4% | North America and Europe | Short term (≤ 2 years) |

| Vendor API lock-in risk | -0.9% | Global; primarily large-enterprise segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Cloud-UC Awareness in Tier-2/3 Banks

Community institutions often lack specialist staff to evaluate UCaaS proposals, defaulting to incumbent telcos for plain-old telephony. A U.S. Treasury-commissioned assessment warns that limited cloud acumen exposes smaller banks to hidden resiliency and cyber risks, prolonging legacy usage and constraining modernization. Educational accelerators, blueprint templates and managed-service bundles therefore play a pivotal role in lowering entry barriers. Providers that extend migration incentives, turnkey security controls and regulatory documentation can unlock this underserved cohort.

Stringent Data-Security and Residency Mandates

Sovereign rules require certain client records to remain within national borders, complicating lift-and-shift strategies. Financial institutions juggling GDPR alongside sectoral statutes lean toward hybrid deployments, where sensitive recordings stay on-prem while less-critical workloads burst to regional clouds. Microsoft’s prescriptive compliance framework for U.S. banking illustrates how predefined blueprints streamline risk assessments and accelerate regulator sign-offs. Nonetheless, cross-border banks must overlay intricate key-management, dual-control and continuous-audit capabilities, inflating project timelines and costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Telephony Dominance Amid Platform Convergence

Telephony accounted for 41.88% of the UCaaS in banking market size in 2025 as voice remains indispensable for fraud verification, trade execution and customer identity confirmation. Collaboration suites, however, are projected to drive an 18.04% CAGR through 2031 as video, persistent chat and shared-document workspaces coalesce into a single pane. The convergence reduces swivel-chair actions for relationship managers, speeding onboarding and issue resolution. Five9 reports that natural-language-processing routers now direct 80% of inbound calls to the correct skill group without human triage, trimming abandonment rates. Unified messaging compresses email, SMS and secure chat feeds into threaded histories, boosting compliance auditability. Video-banking kiosks extend advisory services to rural zones, while communication-platform APIs embed two-factor-authentication voice calls directly into mobile apps. This modularity ensures banks add channels without re-architecting back-end cores, reinforcing platform stickiness and raising switching costs.

Demand for embedded communications intensifies as banks deploy contextual notifications—loan-approval pings, FX-rate alerts and card-usage anomalies—through in-app banners, RCS and OTT messengers. Webex CPaaS banking modules deliver out-of-the-box templates for WhatsApp and Apple Messages, accelerating deployment while retaining encryption and audit logging. Such API-first models empower developers to orchestrate journeys where a chatbot escalates to secure video when high-value transactions exceed preset thresholds. Gartner predicts that by 2030, API-driven channels will account for half of financial-services outbound traffic, underscoring telephony’s gradual transition from standalone product to foundational service within integrated suites.

By Deployment Model: Hybrid Cloud Acceleration

Public-cloud captured 60.72% of UCaaS in banking market share in 2025 on the back of turnkey scalability and consumption pricing. Yet hybrid approaches, forecasting a 18.74% CAGR to 2031, reflect heightened boardroom focus on jurisdictional compliance and latency-sensitive workloads. First Horizon Bank’s Webex Contact Center migration showcased a layered architecture where recordings of regulated staff remained on-prem while AI analytics processed anonymized data in Cisco’s multitenant cloud. This blueprint allowed the bank to maintain 20,000 endpoints and 750 agents under one console without breaching fiduciary data-handling obligations.

Private-cloud remains an option for global systemically important banks with bespoke encryption and sovereignty mandates, although capital and staffing requirements curb its wider appeal. Hybrid strategies support phased migration: institutions can retire aging PBXs site by site, funneling traffic via session-border controllers to a cloud core. Continuous-integration pipelines then deliver feature drops such as noise suppression or auto-redaction without downtime. Given rising environmental, social and governance commitments, workload elasticity also lowers idle energy use, helping banks hit carbon-cut targets.

By Organization Size: SME Growth Momentum

Large enterprises stewarded 64.35% of the UCaaS in banking market size in 2025, leveraging global contracts and dedicated compliance modules. However, SME adoption is predicted to surge at 19.55% CAGR through 2031 as cost-per-seat declines and onboarding wizards obviate deep IT expertise. ATB Financial’s migration to RingCentral enabled 5,300 staff across branch, home and contact-center locations to retire disparate PBX leases in favor of a single SLA, freeing budget for front-office innovation. Subscription packages bundle E-911, call-recording and sentiment analytics that were formerly cost-prohibitive.

Cloud bursting also benefits community banks that experience seasonal loan-origination spikes. They can dial capacity up for mortgage campaigns and scale back post-closing, paying only for active usage. Moreover, UCaaS providers are extending sandbox environments so SME developers can test chatbots, IVR flows and CRM connectors without risking production disruption. This democratization narrows the digital-experience gap between tier-3 institutions and nationwide incumbents, intensifying competitive parity in customer engagement.

By Banking Application: Corporate Banking Acceleration

Retail banking held 44.12% of UCaaS in banking market size in 2025 as high-volume contact centers tackled balance inquiries and card-dispute calls. Corporate and wholesale banking, however, is on course for a 16.72% CAGR by 2031 because multinational clients require omnichannel, round-the-clock support aligned with complex treasury workflows. Secure video rooms facilitate multi-sig authorizations, while virtual deal-rooms enable syndicated-loan negotiations across jurisdictions. EnableX notes that embedded CPaaS workflows trigger real-time alerts on cross-border remittances, cutting exception-handling times and boosting satisfaction ratings.

Investment-banking desks adopt conversation-capture engines that transcribe and tag trader calls, linking them with order-management records to satisfy MiFID II voice-trade retention rules. Digital-wallet spin-offs within conglomerate banks further elevate UCaaS volumes as micro-payment pings and balance reminders proliferate. The convergence of communications and transaction payloads thus positions UCaaS not merely as a utility but as a revenue-enabling platform that deepens wallet share and stickiness in corporate segments.

Geography Analysis

North America retained 36.25% UCaaS in banking market share in 2025, capitalizing on mature cloud regulations and sizeable budgets for enterprise modernization. Barclays, UBS and Citigroup exemplify large-scale deployments that marry collaboration suites with AI copilots to streamline advisor workflows . Despite headway, many regional banks remain tethered to depreciating PBXs, as less than 40% of businesses have completed migration. Hybrid rollouts therefore dominate, balancing transformation momentum with risk-management caution.

Asia-Pacific leads growth at 14.54% CAGR through 2031 as mobile-first demographics spur digital banks to embed voice and messaging directly in apps. Japanese carriers such as NTT and SoftBank export UCaaS footprints globally, while partnerships between Vonage and local integrators digitize contact-center estates throughout Southeast Asia. Conversational-AI adoption rises in concert, lifting first-contact resolution and enabling 24/7 multilingual servicing.

Europe emphasizes data-sovereignty, prompting banks to prefer region-locked clouds or sovereign partnerships. UniCredit’s USD 400 million acquisition of Vodeno delivers a cloud-native platform with built-in smart-contract engines, aligning with PSD2 open-banking requisites while expanding white-label capabilities. In the Middle East and Africa, cloud adoption leapfrogs legacy PBX phases; for instance, Ecobank’s alliance with Google Cloud powers analytics-driven inclusion programs across 35 nations. These markets underline UCaaS’ role in bridging service gaps where physical branches remain sparse.

Competitive Landscape

The UCaaS in banking market is moderately concentrated. Microsoft leverages its 400-million-seat Office ecosystem to cross-sell Teams voice workloads, supported by Azure’s compliance envelope. RingCentral holds 20% share of the broader UCaaS arena and reports more than 1,000 deployments of AI Receptionist within financial-services clients . Cisco, Avaya and Mitel convert entrenched TDM estates through migration toolkits, while cloud-native challengers 8x8 and Dialpad differentiate via AI summarization and sentiment dashboards.

MandA continues to reshape vendor rosters. Ericsson’s USD 6.2 billion purchase of Vonage marries 5G network APIs with UCaaS to support Quality-of-Service-guaranteed enterprise calling [NO-JITTER]. Intermedia’s absorption of NEC’s UNIVERGE BLUE boosts verticalized banking templates complete with call-recording retention and speech analytics. Providers increasingly embed CPaaS layers so core banking vendors can call voice, SMS and video functions programmatically, catalyzing Banking-as-a-Service propositions. Success pivots on multilayer encryption, zero-trust architectures and industry-aligned governance documentation that satisfy examiners without inflating operational overhead.

UCaaS In Banking Industry Leaders

RingCentral, Inc.

8X8 Inc.

Cisco Systems Inc.

Microsoft Corporation

Zoom Video Communications, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: UniCredit completed its EUR 376 million (USD 400 million) buy-out of Aion Bank and Vodeno to gain cloud-based BaaS APIs and smart-contract tooling .

- March 2025: NatWest and OpenAI formed a partnership to embed generative-AI assistants across fraud-detection and financial-planning journeys .

- February 2025: Barclays deployed Microsoft Teams across worldwide operations to harmonize collaboration and retire fragmented voice systems .

- February 2025: UBS partnered with Microsoft to co-create AI “Smart Assistants” using Azure AI Search and OpenAI Service for real-time advisor briefings .

Global UCaaS In Banking Market Report Scope

UCaaS refers to a service model where the provider delivers different telecom or communications applications, software products and processes generally over the web.The UCaaS in banking market is segmented byvarious types of components used for UC, size of the organization, and geography.By type of components, the market studied is segmented into telephony, contact center, unified messaging, collaboration platform. By organization size, the market studied is segmented into large enterprises and small & medium enterprises. Integrated solutions offered by UCaaS vendors areconsidered in the scope of the study.

| Telephony |

| Unified Messaging |

| Contact Center |

| Collaboration Platform |

| Video Conferencing |

| Communication-Platform APIs |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Retail Banking |

| Corporate and Wholesale Banking |

| Investment Banking |

| Payment and FinTech Subsidiaries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Telephony | ||

| Unified Messaging | |||

| Contact Center | |||

| Collaboration Platform | |||

| Video Conferencing | |||

| Communication-Platform APIs | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises | |||

| By Banking Application | Retail Banking | ||

| Corporate and Wholesale Banking | |||

| Investment Banking | |||

| Payment and FinTech Subsidiaries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the UCaaS in banking market?

The UCaaS in banking market is valued at USD 12.36 billion in 2026.

How fast will the UCaaS in banking market grow?

The market is projected to post a 13.02% CAGR and reach USD 22.83 billion by 2031.

Which deployment model is expanding the quickest?

Hybrid-cloud UCaaS is advancing at 18.74% CAGR as banks pursue data-sovereignty compliance alongside cloud agility.

Why are collaboration platforms gaining traction in banks?

Collaboration suites integrate video, chat and document sharing, enabling banks to improve customer experience and cross-functional efficiency, driving an 18.04% CAGR for the segment.

Page last updated on: