Unified Communication As A Service (UCaaS) In Retail Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

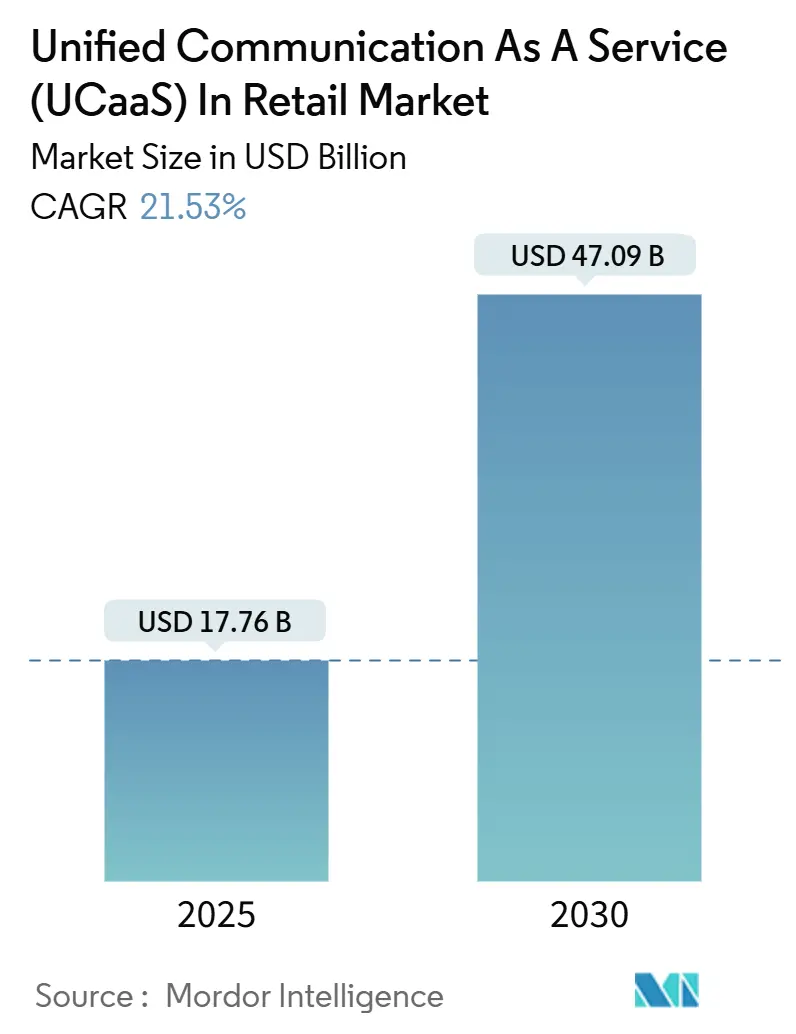

| Market Size (2025) | USD 17.76 Billion |

| Market Size (2030) | USD 47.09 Billion |

| Growth Rate (2025 - 2030) | 21.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unified Communication As A Service (UCaaS) In Retail Market Analysis by Mordor Intelligence

The unified communication as a service in retail market size reached USD 17.76 billion in 2025 and is forecast to climb to USD 47.09 billion by 2030, posting a 21.53% CAGR over the period. Growth reflects retailers’ pivot toward cloud-native platforms that bundle voice, video, messaging, and collaboration into a single subscription. Accelerating e-commerce penetration, the operational complexity of micro-fulfillment centers, and sunset timelines for analog phone lines are nudging retailers to retire on-premises private branch exchange systems in favor of scalable, pay-as-you-go alternatives. Telephony replacement cycles continue to anchor deployments, yet artificial-intelligence-driven contact center applications are expanding fastest as omnichannel strategies move real-time customer engagement to the cloud. Parallel momentum for hybrid workloads is emerging, with retailers retaining sensitive data on-premises to meet sovereignty mandates while bursting to the public cloud for elastic conferencing capacity. Competitive intensity is rising as telecommunications carriers, cloud-native specialists, and hyperscale productivity-suite vendors race to pre-integrate with merchandise, labor-management, and customer-data systems, shortening time-to-value for retail information-technology teams.

Key Report Takeaways

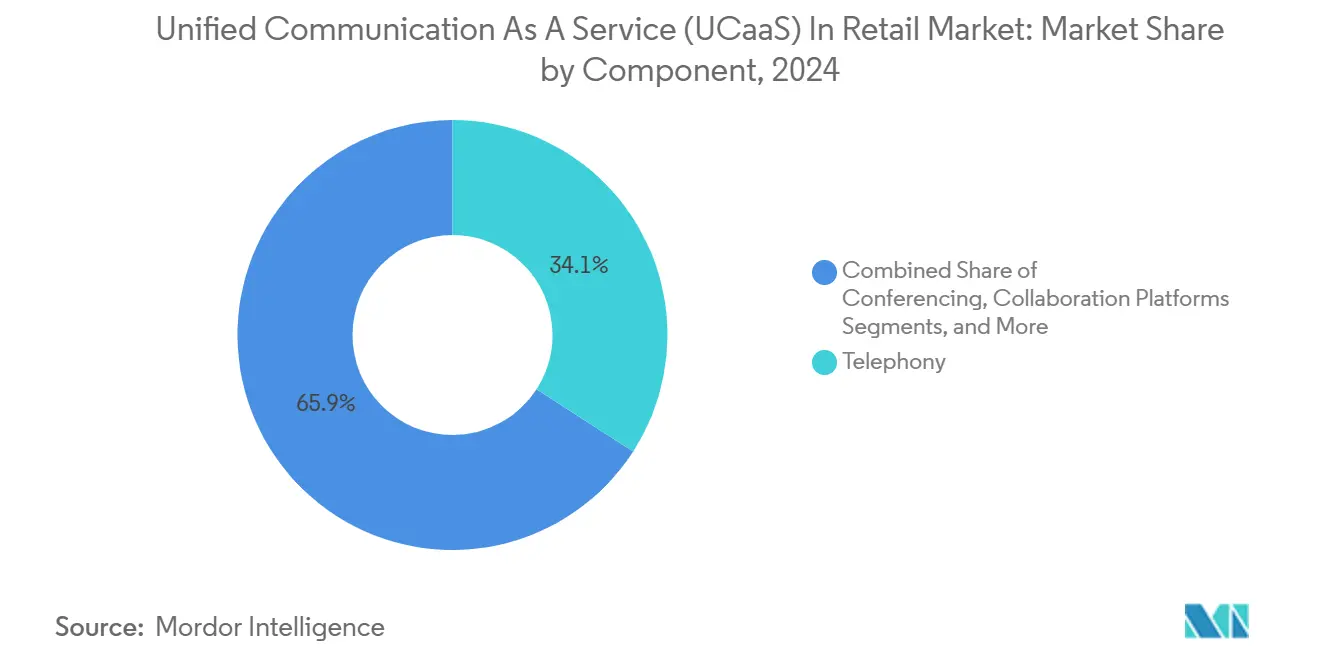

- By component, contact center applications are advancing at a 22.24% CAGR through 2030, while telephony accounted for 34.12% of the unified communication as a service market share in the retail sector in 2024.

- By deployment model, hybrid cloud workloads are projected to expand at 23.18% through 2030; public cloud retained a 46.37% share of the unified communication as a service market in the retail sector in 2024.

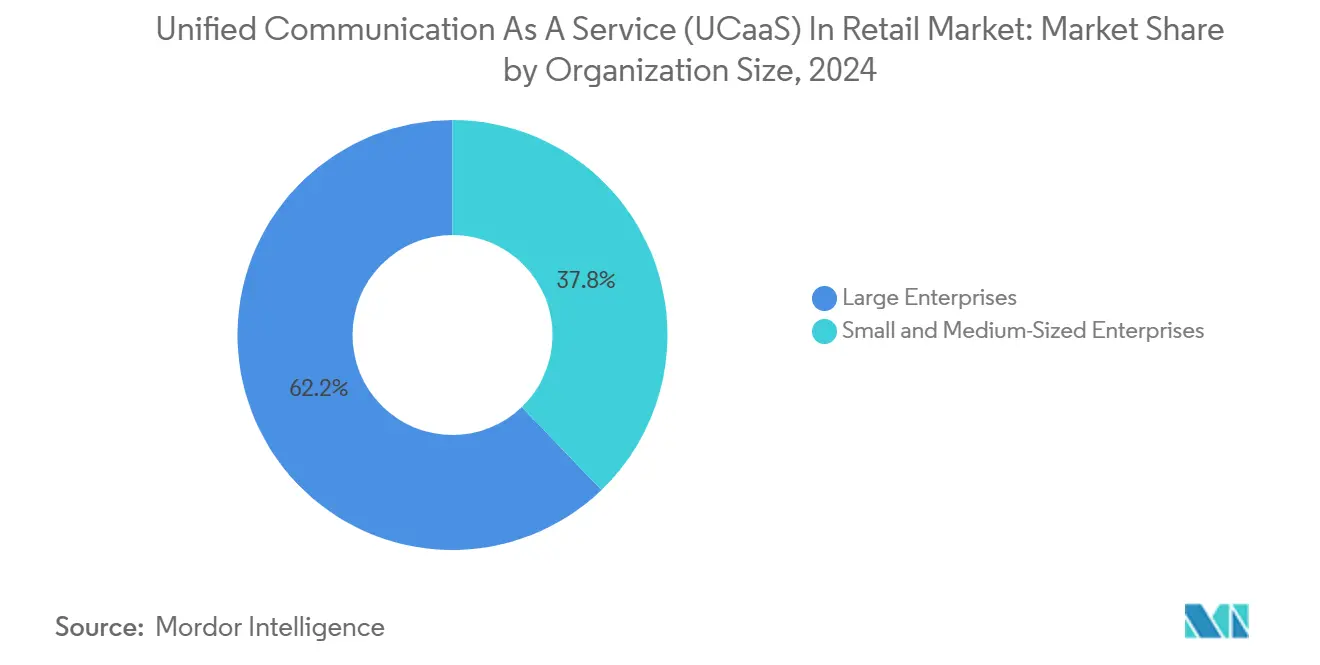

- By organization size, large enterprises captured 62.18% of spending in 2024; however, small and medium-sized retailers are projected to grow at a rate of 23.12% through 2030.

- By store format, supermarkets and hypermarkets accounted for 38.72% of deployments in 2024; e-commerce and omnichannel retailers are expected to grow at a 21.73% CAGR toward 2030.

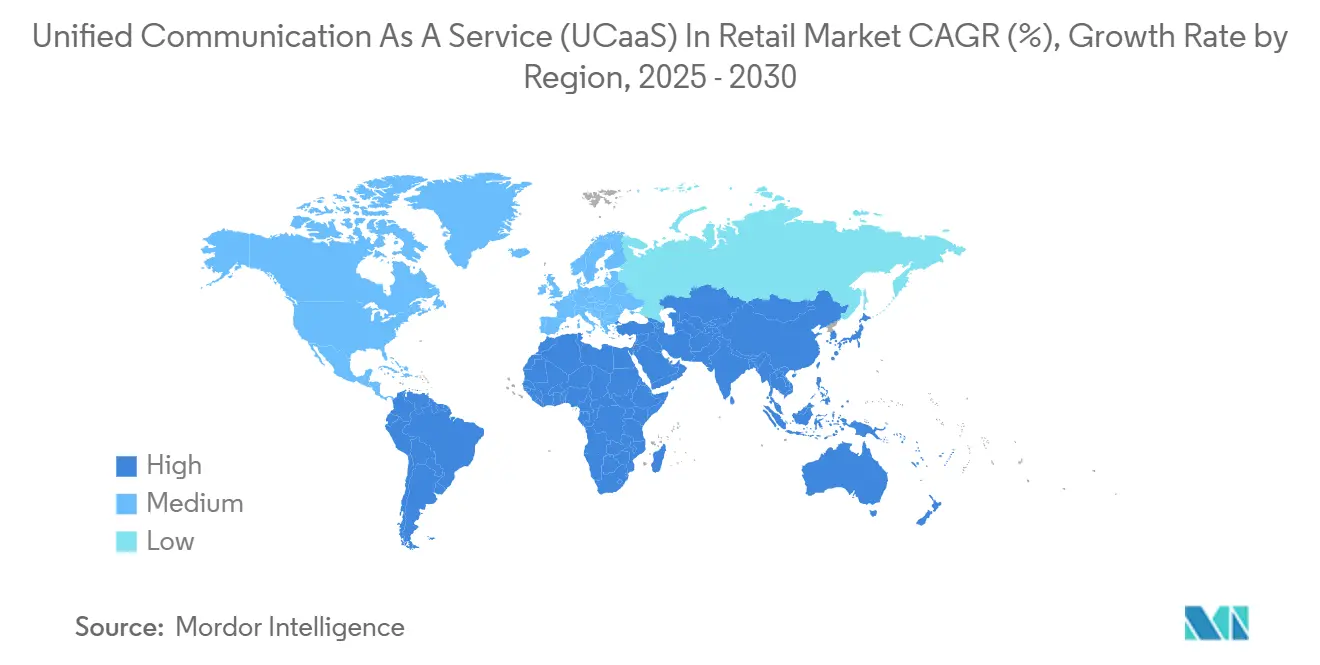

- By geography, North America generated 33.56% of 2024 revenue, while Asia-Pacific is on track for a 22.34% CAGR through 2030.

Global Unified Communication As A Service (UCaaS) In Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of IP Applications for In-Store Operations | +4.2% | Global, with early concentration in North America and Western Europe | Medium term (2-4 years) |

| Increased Demand for Mobility and BYOD Policies | +3.8% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Rising Emphasis on Omnichannel Retail Experience | +4.5% | Global, led by North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Growing Demand from Small and Medium-Sized Businesses | +3.1% | Global, with pronounced uptake in emerging markets across Asia-Pacific, Latin America, and Africa | Long term (≥ 4 years) |

| Proliferation of Micro-Fulfillment Centers Requiring Real-Time UCaaS | +2.7% | North America and Europe, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| GDPR-Driven Preference for In-Region UCaaS Data Centers | +2.3% | Europe, with spillover to markets adopting similar frameworks (Brazil, India, South Africa) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of IP Applications for In-Store Operations

Retailers are shifting from circuit-switched lines to Internet Protocol voice, video, and messaging to streamline task management, inventory alerts, and clienteling on mobile devices. Zebra Technologies reported that 7.7 million frontline retail staff lacked dedicated devices in 2024, signaling latent demand for bring-your-own-device-ready–ready UCaaS clients. Looming public-switched telephone network shutdowns in markets such as the United Kingdom and Australia intensify the urgency, with Ofcom confirming the retirement of analog services by 2027.[1]Ofcom, “All IP Programme Update,” ofcom.org.uk Unified interfaces now enable associates to escalate inquiries to remote experts on video, retrieve real-time inventory through application programming interface calls, and coordinate curb-side pickup without toggling between apps, reducing average handling time and improving first-call resolution.

Increased Demand for Mobility and BYOD Policies

High turnover and variable staffing drive retailers to support personal-device access securely. WorkJam’s 2024 survey found 66% of workers willing to use personal phones if security controls exist. UCaaS platforms answer with end-to-end encryption, multi-factor authentication, and mobile-device-management hooks, trimming per-employee communication costs by up to 40% according to documented deployments by regional grocery chains. Mobility extends to management layers, where district leaders conduct virtual store walks over video, reducing travel spend and enabling higher-frequency coaching.

Rising Emphasis on Omnichannel Retail Experience

Consumers routinely hop channels during a single purchase. Genesys cloud contact routing now surfaces browsing context, loyalty status, and purchase history to agents, reducing repeated inquiries. McKinsey’s 2024 multichannel study showed 73% of shoppers interacted across channels, though only 29% enjoyed consistency; UCaaS bridges that gap through unified voice, chat, and video endpoints integrated with order-management systems. Real-time collaboration lets store associates summon product specialists over video to replicate flagship-store expertise in smaller formats, boosting conversion.

Growing Demand from Small and Medium-Sized Businesses

Subscription models eliminate up-front hardware, drawing SMEs that previously could not justify private branch exchange investments. Case studies from 8x8 reveal 40% lower five-year total cost of ownership for chains below 250 employees after migrating to cloud voice. License-based scaling lets retailers add seasonal workers without stranded capacity, while pre-built connectors into e-commerce and payments shrink deployment times from months to weeks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Integration of Legacy Systems with Cloud Platforms | -2.8% | Global, most acute in North America and Europe with extensive legacy infrastructure | Medium term (2-4 years) |

| Heightened Data Security and Privacy Concerns | -2.1% | Global, with regulatory intensity highest in Europe, California, and emerging markets adopting GDPR-style frameworks | Long term (≥ 4 years) |

| Dependence on High-Quality Connectivity in Rural Locations | -1.6% | North America, Latin America, Africa, and rural Asia-Pacific regions | Long term (≥ 4 years) |

| Retail Workforce Union Policies Restricting Call Monitoring | -0.9% | Europe, select North American jurisdictions, and unionized retail segments globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Integration of Legacy Systems With Cloud Platforms

IBM’s 2024 cloud-modernization study found 68% of retailers citing integration hurdles as the top cloud-migration barrier.[2]IBM, “Cloud Modernization in Retail 2024,” ibm.com Typical chains run more than 20 separate store and head-office applications, many built on proprietary protocols that need bespoke middleware to connect with UCaaS. Delays inflate costs and create synchronization risks that can disrupt inventory visibility or order routing. Integration-platform-as-a-service offerings reduce friction but add subscription overhead and require specialized skills.

Heightened Data Security and Privacy Concerns

Verizon’s 2024 investigations flagged a 23% rise in breaches across retail and hospitality, with compromised credentials prevalent. UCaaS providers supply encryption and zero-trust frameworks, yet endpoint hygiene, access governance, and workforce training remain retailer responsibilities. Small businesses without dedicated security personnel face the greatest exposure and must lean on vendor-managed controls, careful role-based permissions, and audit logging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Contact Centers Gain as AI Reshapes Customer Engagement

Contact center applications represent the fastest-moving slice of the unified communication as a service in retail market. They are projected to expand at 22.24% through 2030 as retailers embed generative artificial intelligence for intent detection, sentiment analysis, and agent coaching. Telephony still delivered 34.12% of 2024 revenue, ensuring a large installed base for upsell of analytics and automation tool sets. The unified communication as a service in retail market size for contact center applications is forecast to contribute USD 14.09 billion of incremental revenue by 2030. Unified messaging and conferencing retain demand for asynchronous shift coordination and virtual training, while team collaboration workspaces such as Microsoft Teams knit document sharing, project tracking, and video into one pane of glass.

Unified suites shorten procurement cycles, drive license loyalty, and keep average selling prices resilient in a commoditizing voice backdrop. Retailers report double-digit reductions in average handling time and first-call resolution improvements when AI-powered agent-assist functions surface knowledge-base articles automatically during calls. Twilio customer implementations register 18% handling-time reduction after embedding purchase-history pop-ups from customer-data-platform integrations.

By Deployment Model: Hybrid Architectures Balance Sovereignty and Scalability

Public-cloud-hosted platforms captured 46.37% of 2024 revenue, buoyed by near-instant provisioning, automatic patching, and pay-per-seat economics that appeal to resource-constrained chains. Yet the unified communication as a service in retail market is witnessing accelerated hybrid uptake, with a 23.18% forecast CAGR, as retailers insulate regulated data or latency-sensitive workloads within private clouds or on-premises nodes. A European luxury banner kept customer-interaction recordings in a Swiss private cloud while bursting overflow media streams to AWS during high-traffic holiday windows.

Edge compute and software-defined wide-area networking further blur deployment categories by allowing video consults and inventory queries to be processed within stores for sub-50-millisecond response times. Private-cloud adoption remains stable in highly regulated segments but growth is capped by capital expenses and refresh cycles. Total cost analyses show hybrid positions costing 15% less than pure private over five years when idle capacity is factored.

By Organization Size: SMEs Embrace Subscription Economics

The unified communication as a service in retail market size skews toward large enterprises today 62.18% of 2024 spend because global store networks accrue more seats and require advanced workforce-optimization features. Nonetheless, SMEs are the growth engine: at 23.12% forecast CAGR they will capture incremental share through 2030 as licensing tiers start at single-digit seat counts and administration dashboards become intuitive for non-specialists.

Subscription pricing eliminates upfront server purchases, handset fleets, and dedicated IT hires, letting independent boutiques match enterprise-grade customer experience. Case studies from 8x8 Retail Connect document 12% labor-productivity lift after integrating shift-scheduling alerts directly into voice and messaging clients. Feature democratization flattens competitive dynamics, enabling single-store jewelers to offer curb-side video clienteling resembling national luxury brands.

By Retail Store Format: E-Commerce Convergence Drives Omnichannel Investment

Supermarkets and hypermarkets dominate existing footprints thanks to large workforces managing perishable stock, checkout lanes, and home-delivery orchestration. Their UCaaS blueprints emphasize 99.999% voice uptime, tight point-of-sale integration, and cost per seat below USD 15. The unified communication as a service in retail market share for this format was 38.72% in 2024, aided by grocery chains embedding voice-directed picking and supplier-collaboration channels.

E-commerce and omnichannel banners headline the growth story. Their 21.73% CAGR stems from needing 360-degree customer-journey views across web, social, and store. UCaaS contact-center suites integrate with Shopify, Magento, and enterprise order-management systems so that agents can refund, upsell, or re-route shipments mid-conversation. Zoom’s retail contact center recovered 14% of abandoned carts with automated outbound reminders triggered by real-time inventory status. Specialty and convenience formats adopt mobile-first UCaaS for vendor communication, price-check escalation, and back-of-house inventory queries, removing landlines entirely in new builds.

Geography Analysis

North America remains the revenue cornerstone, supplying 33.56% of 2024 turnover. U.S. carriers such as AT&T and Verizon offer migration incentives as public-switched telephone networks wind down, prompting chains to swap analog trunks for SIP and cloud endpoints. Contact-center modernizations lead projects, with retailers overlaying AI to detect sentiment, auto-score compliance, and surface next-best actions in two languages for Canada’s bilingual context. Mexico’s near-shoring boom increases demand for cross-border collaboration tools, synchronizing merchandise buyers with factory planners through shared video and messaging rooms.

Asia-Pacific is the clear acceleration zone, forecast at a 22.34% CAGR to 2030. Smartphone penetration above 70% in urban China, India, and Southeast Asia catalyzes mobile-first UCaaS uptake. China’s retailers embed Tencent WeChat mini-programs inside UCaaS interfaces so store associates can message shoppers, process digital payments, and confirm last-mile delivery statuses within a single pane. India’s Digital India blueprint removes ambiguity over public-cloud usage, enabling quick-commerce dark-store operators to coordinate riders via geofenced voice channels. Australia’s analog switch-off timelines mirror the U.K.’s, forcing chain stores to migrate before 2027; the Australian Communications and Media Authority is actively broadcasting cut-off dates to retailers.[3]Australian Communications and Media Authority, “Public-Switched Network Closure Timeline 2024,” acma.gov.au

Europe blends robust installed bases with strict data-protection regulations. GDPR penalties up to 4% of global revenue elevate data-residency guarantees to RFP essentials. Microsoft and Cisco maintain multiple in-region clusters to qualify. The United Kingdom juggles Brexit-induced regulatory divergence yet shares the U.K. PSTN sunset deadline of 2027, accelerating migration. Germany and France push video clienteling in luxury and automotive boutiques, requiring 4K streams and on-premises session recording. Southern Europe’s tourism malls adopt multilingual voice-translation widgets to serve transient shoppers. Beyond Europe, Brazil enforces an LGPD framework analogous to GDPR, nudging retailers to prefer in-country data centers. Middle Eastern growth concentrates in Saudi Arabia’s Vision 2030 retail-modernization agenda and the United Arab Emirates’ mall-heavy footfall. Africa’s leadership rests with South Africa and Kenya, where 4G coverage allows leapfrogging to cloud calling without legacy PBX baggage.

Competitive Landscape

No vendor surpasses 15% revenue, giving the unified communication as a service in retail market a moderate fragmentation profile. Incumbent carriers Verizon, AT&T, BT bundle connectivity and cloud PBX under multi-year contracts, leveraging existing circuits and field-service armies. Cloud-native pioneers RingCentral and 8x8 differentiate through rapid feature sprints and out-of-the-box retail connectors. Hyperscale suite vendors Microsoft, Cisco, and Zoom lock in enterprises by embedding voice and video inside broader productivity stacks, converting Office 365, Webex, or Zoom Workplace seats into UCaaS adoption.

Integration depth is the decisive battleground. Vendors shipping pre-built connectors to Oracle Retail, SAP for Retail, NCR Counterpoint, Stripe, and Shopify slash launch times from quarters to weeks, an edge for resource-lean chains. Cisco’s 2024 acquisition of a workforce-engagement suite, for USD 425 million, bolts AI-driven quality management and compliance auto-redaction onto Webex Contact Center. Microsoft’s January 2025 general availability of Azure Communication Services inside Dynamics 365 removes the need for separate UCaaS licenses and surfaces customer data natively during interactions.

Pricing pressure persists, with per user per month falling mid-single digits annually. Vendors offset erosion through tiered AI add-ons and revenue-share models on outbound SMS or telephone minutes. Cisco registered 47 patents in 2024 around natural-language routing and predictive capacity planning.[4]Cisco Systems, “Patent Filings 2024,” uspto.gov Startups leverage large language models to automate tier-1 support; early pilots show 40% deflection of live-agent chats in fashion e-commerce cohorts. Vertical solutions emerge for grocery perishable alerts, luxury appointment scheduling, and quick-commerce rider dispatch, signaling white-space for niche specialists.

Unified Communication As A Service (UCaaS) In Retail Industry Leaders

RingCentral Inc.

8x8 Inc.

Verizon Communications Inc.

Mitel Networks Corporation

Comcast Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft introduced native Azure Communication Services hooks within Dynamics 365 Customer Service, letting agents place voice, video, or chat from CRM records and auto-log interactions.

- December 2024: RingCentral and Salesforce launched embedded calling, messaging, and video inside Service Cloud, plus dashboards correlating communication KPIs with customer lifetime value.

- November 2024: Zoom rolled out Zoom Contact Center for Retail, integrating with Shopify and Magento to surface real-time order status and AI chatbots for tier-1 automation.

- October 2024: Genesys secured USD 580 million from private equity to accelerate AI orchestration for retail predictive engagement.

Global Unified Communication As A Service (UCaaS) In Retail Market Report Scope

The Unified Communication as a Service (UCaaS) in the Retail Market refers to the provision and adoption of cloud-based communication and collaboration solutions, including unified messaging, telephony, conferencing, collaboration platforms, and contact center services, across the global retail industry. It encompasses deployments across public, private, and hybrid cloud models and is utilized by both small and medium-sized enterprises, as well as large retail organizations. The market encompasses a range of retail formats, including supermarkets, specialty stores, convenience stores, and e-commerce or omnichannel retailers, which support their operational efficiency and customer engagement needs.

The Unified Communication as a Service in Retail Market Report is Segmented by Component (Unified Messaging, Telephony, Conferencing, Collaboration Platforms, Contact Center), Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), Retail Store Format (Supermarkets and Hypermarkets, Specialty Stores, Convenience Stores, E-Commerce and Omnichannel Retailers), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Unified Messaging |

| Telephony |

| Conferencing |

| Collaboration Platforms |

| Contact Center |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| Supermarkets and Hypermarkets |

| Specialty Stores |

| Convenience Stores |

| E-Commerce and Omnichannel Retailers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Component | Unified Messaging | ||

| Telephony | |||

| Conferencing | |||

| Collaboration Platforms | |||

| Contact Center | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Organization Size | Small and Medium-Sized Enterprises | ||

| Large Enterprises | |||

| By Retail Store Format | Supermarkets and Hypermarkets | ||

| Specialty Stores | |||

| Convenience Stores | |||

| E-Commerce and Omnichannel Retailers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 value of the unified communication as a service in retail market?

The unified communication as a service in retail market size totaled USD 17.76 billion in 2025.

How fast is the market expected to expand through 2030?

It is projected to advance at a 21.53% CAGR, reaching USD 47.09 billion by 2030.

Which component is growing quickest inside retail UCaaS deployments?

AI-enabled contact center software leads with a 22.24% forecast CAGR to 2030.

Why are hybrid cloud architectures gaining favor among retailers?

Hybrid deployments let retailers keep sensitive data on-premises to meet sovereignty laws while scaling video and call recording in the public cloud.

Which region shows the highest growth potential?

Asia-Pacific, forecast to grow at a 22.34% CAGR, driven by mobile commerce and digital-transformation programs.

How does UCaaS benefit small and medium-sized retailers financially?

Subscription pricing removes up-front hardware outlays and cuts five-year total communication cost by up to 40% compared with legacy PBX solutions.

Page last updated on: