UAV Payload and Subsystems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.61 Billion |

| Market Size (2031) | USD 13.55 Billion |

| Growth Rate (2026 - 2031) | 9.49% CAGR |

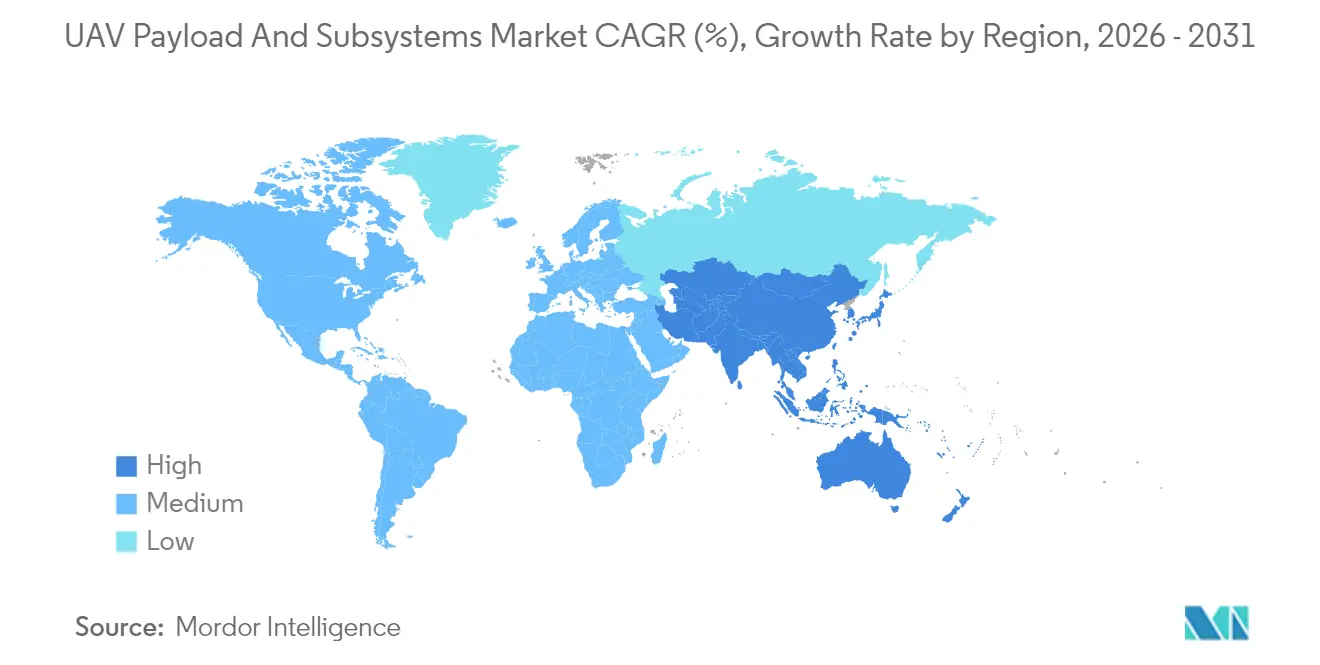

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAV Payload and Subsystems Market Analysis by Mordor Intelligence

The UAV payload and subsystems market size was valued at USD 7.86 billion in 2025 and estimated to grow from USD 8.61 billion in 2026 to reach USD 13.55 billion by 2031, at a CAGR of 9.49% during the forecast period (2026-2031). Ongoing military-modernization programs, higher defense outlays, and institutional shifts toward unmanned platforms anchor this growth trajectory. The US Department of Defense alone earmarked USD 10.1 billion for unmanned-vehicle acquisition and R&D in fiscal 2025, highlighting sustained federal commitment. Electronic-warfare (EW) payloads post the fastest segment CAGR at 10.35%, while tactical UAVs remain the volume leaders, capturing 27.85% of the UAV-class segmentation. Regionally, North America retains the largest position with a 35.45% share in 2024, but Asia-Pacific logs the highest 9.75% CAGR, propelled by East Asia’s defense-spending jump to USD 411 billion in 2023. Endurance-critical propulsion and power subsystems command 37.85% share, whereas flight-control systems record an 11.23% CAGR as autonomy becomes essential in GPS-denied environments.

Key Report Takeaways

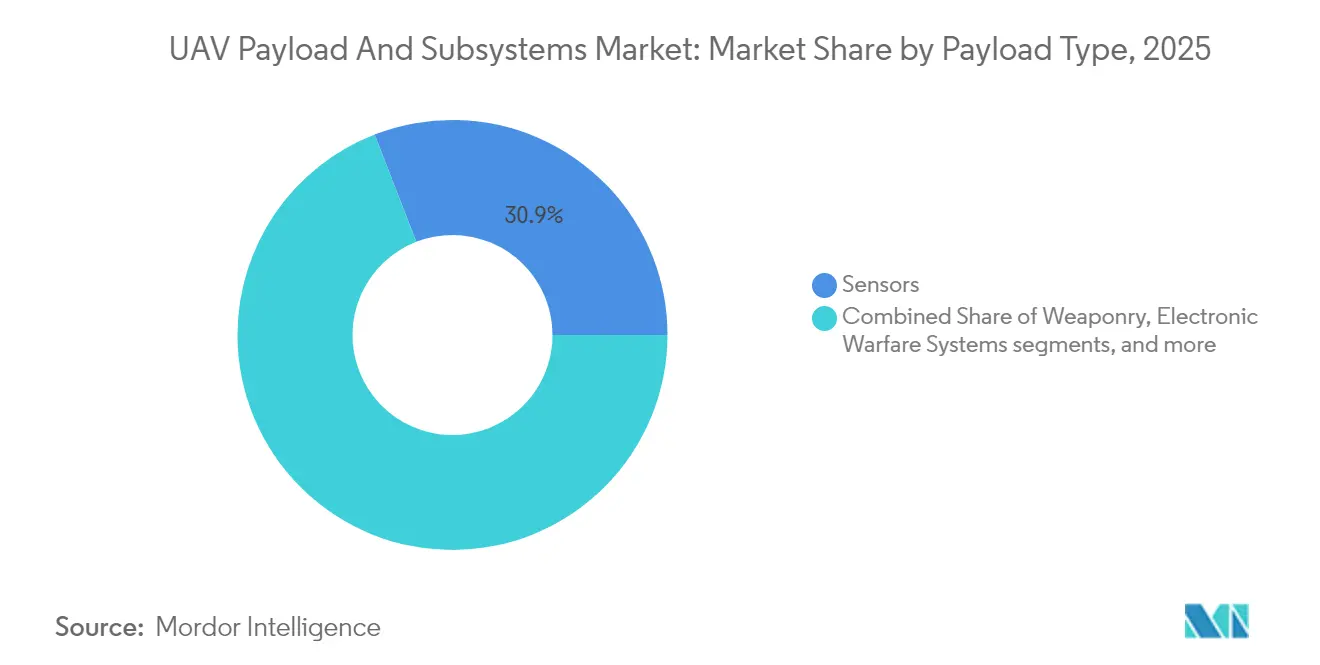

- By payload type, sensors held 30.90% of the UAV payload and subsystems market share in 2025, whereas electronic-warfare systems are projected to expand at a 10.16% CAGR to 2031.

- By subsystem type, propulsion and power captured 37.20% revenue share in 2025; flight control systems will post the fastest 11.04% CAGR through 2031.

- By UAV class, tactical platforms accounted for 27.40% of the UAV payload and subsystems market size in 2025, while the HALE segment is set to grow at a 12.26% CAGR to 2031.

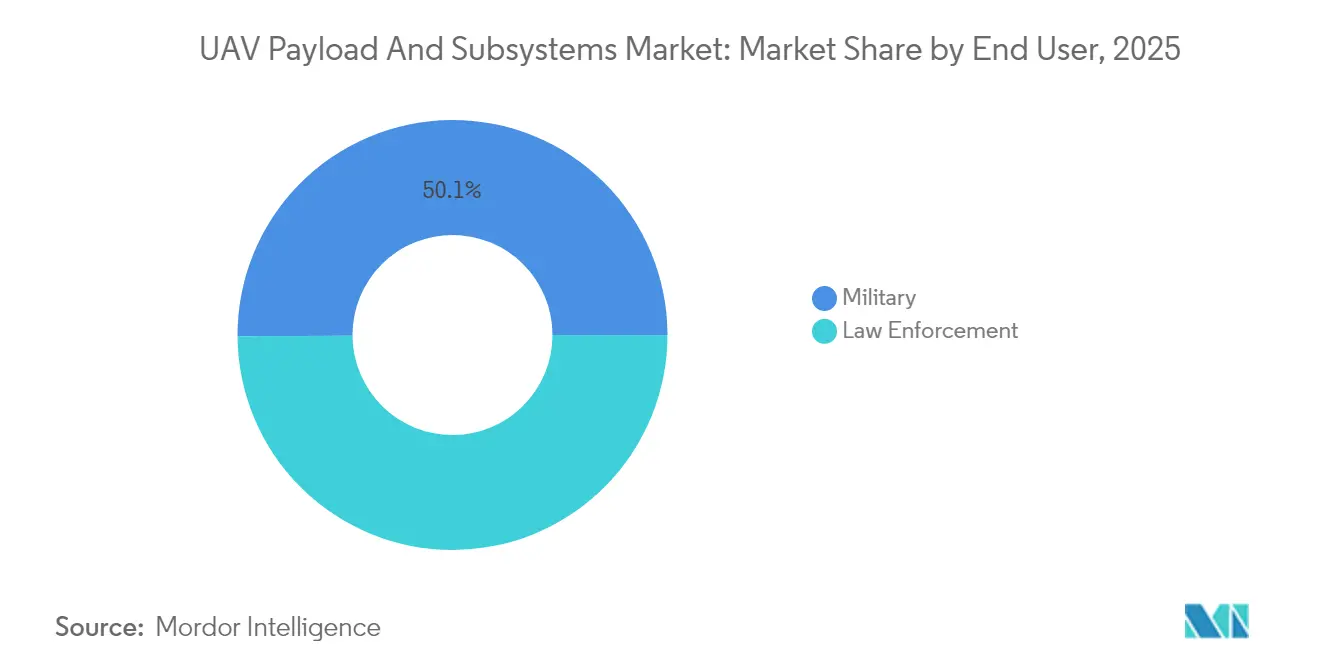

- By end-user, defence and security captured 50.10% revenue share in 2025; law enforcement systems will post the fastest 9.38% CAGR through 2031.

- By application, ISR missions contributed 49.10% share of the UAV payload and subsystems market size in 2025; combat/strike missions represent the quickest-rising application at 12.08% CAGR.

- By geography, North America held 35.10% of the UAV payload and subsystems market share in 2025; Asia-Pacific shows the strongest 9.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global UAV Payload and Subsystems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding defense ISR budgets | +1.8% | Global; North America and Asia-Pacific concentrated | Medium term (2-4 years) |

| On-board AI processors for contested environments | +1.2% | Global; led by North America and Europe | Short term (≤ 2 years) |

| Swarm concepts driving interoperable communications subsystems | +1.5% | North America and Asia-Pacific core | Long term (≥ 4 years) |

| Modular Open-Systems Architecture (MOSA) mandates | +0.9% | North America and allied nations | Medium term (2-4 years) |

| Geopolitical tensions driving procurement acceleration | +1.1% | Global; contested regions emphasized | Short term (≤ 2 years) |

| Shift toward domestic manufacturing capabilities | +0.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding defense ISR budgets

Rising intelligence, surveillance, and reconnaissance allocations underline how information dominance shapes modern force planning. The FY-2025 US budget dedicates USD 10.1 billion to unmanned systems that blend sensor fusion with real-time processing.[1]US Department of Defense, “FY25 Budget Request – Unmanned Systems Fact Sheet,” defense.gov Comparable spending moves in Japan, South Korea, and Australia confirm a shared belief that faster data cycles shorten the kill chain and protect crews. Procurement offices now prioritize multi-spectral sensors, high-bandwidth datalinks, and onboard analytics that can convert raw imagery into actionable cues during a single pass. This demand surge positions the UAV payload and subsystems market for sustained double-digit growth through the decade.

On-board AI processors for contested environments

Edge-computing chipsets allow drones to identify threats and adjust flight paths without cloud connectivity. MIT testing cut trajectory-tracking error by 50%, proving that onboard inference improves autonomy when jamming blocks command links. Militaries now specify rugged AI hardware that endures vibration, temperature swings, and electromagnetic attack, ensuring mission completion even when GNSS signals vanish. These processors also enable rapid sensor fusion, letting operators push more payload types onto the same airframe. As a result, avionics suppliers that integrate advanced GPUs and neural accelerators see rising order volumes.

Swarm concepts driving interoperable communications subsystems

DARPA’s OFFSET field events showed drone teams achieving 85% target-identification accuracy through mesh networking.[2]Defense Advanced Research Projects Agency, “OFFSET Swarm Exercise Results,” darpa.mil Coordinated flight demands time-synchronized links, low-probability-of-intercept waveforms, and decentralized processing so any node can assume command if a leader fails. Defense buyers are therefore procuring frequency-agile radios that hop across bands to outmaneuver jammers. Software-defined stacks further let operators upload new encryption or routing schemes in hours, not months. These capabilities transform individual UAVs into collective assets that saturate defenses by sheer volume and agility.

Modular Open-Systems Architecture (MOSA) mandates

Pentagon acquisition rules now require MOSA compliance, forcing contractors to publish interface specs and adopt standard data buses.[3]Office of the Under Secretary of Defense for Acquisition & Sustainment, “Modular Open Systems Architecture Memo,” acq.osd.mil Open architectures let armed services plug in a next-generation sensor or jammer without redesigning the entire airframe. Lifecycle costs fall because upgrades look more like smartphone app installs than depot overhauls. Vendors that embrace MOSA can enter programs midstream, disrupting incumbents who once relied on proprietary lock-in. For militaries, the payoff is faster fielding of countermeasures against emerging threats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control and flight-regulation hurdles | -0.7% | Global | Medium term (2-4 years) |

| Weight–power trade-offs limiting endurance | -0.5% | Global | Long term (≥ 4 years) |

| RF-spectrum congestion affects datalinks | -0.4% | Global; contested zones | Short term (≤ 2 years) |

| Rare-earth supply risks for advanced sensors | -0.3% | Global; Asia-Pacific vulnerable | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Export-control and flight-regulation hurdles

ITAR, EAR, and MTCR rules oblige manufacturers to vet every component and customer, creating paperwork that can delay deliveries by months.[4]US Department of State, “International Traffic in Arms Regulations,” state.gov Firms often design “export-light” versions that drop advanced encryption, range, or payload options, diluting performance to stay compliant. Smaller innovators struggle with the legal overhead, ceding market share to primes that maintain in-house compliance teams. Civil aviation regulators add another layer, mandating see-and-avoid sensors and fail-safe controls before flights in national airspace. Together, these barriers restrict the global diffusion of cutting-edge subsystems.

Weight–power trade-offs limiting endurance

Battery energy density and combustion-engine efficiency set hard ceilings on how long a UAV can stay aloft. Directed-energy weapons, wide-aperture radars, and high-capacity datalinks consume more watts than previous payloads, tightening the design margin. Engineers chase lighter airframes, new chemistries, and hybrid generators, yet progress remains incremental rather than revolutionary. Every extra kilogram removed from the structure can save fleets tens of thousands of operational dollars, so materials research commands large R&D budgets. Until a breakthrough—such as solid-state batteries—emerges, operators must balance mission scope against finite onboard power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payload Type: Electronic-Warfare Systems Lead Innovation

Sensors accounted for USD 2.43 billion and 30.90% of the UAV payload and subsystems market in 2025. Electronic-warfare configurations, however, will outpace all others at a 10.16% CAGR as spectrum dominance becomes indispensable. The UAV payload and subsystems market size for EW is forecast to double by 2031, helped by modular pod architectures that retrofit onto legacy airframes. US Marine Corps integration of T-SOAR pods on MQ-9 demonstrators underscores a doctrine shift toward active counter-radar measures.

Weaponized payloads log mid-single-digit growth, buoyed by miniaturized glide munitions and loitering warheads. Imaging payloads gain from AI-powered automatic-target-recognition algorithms, easing operator workload. Communications and datalinks struggle with RF congestion, yet demand persists for L-band and S-band relays that guarantee resilient mesh networks in swarms. Niche “other” payloads—chemical detection, cyber-exfiltration kits—capture small but strategic orders.

By Subsystem Type: Flight-Control Systems Drive Autonomy

Propulsion and power retained a 37.20% share in 2025, reflecting their status as the primary cost element. Heavy-fuel engines, hybrid generators, and high-voltage distribution harnesses dominate procurement. Conversely, flight-control software and hardware will grow 11.04% annually, the highest among subsystems, as autonomy drives procurement. The UAV payload and subsystems market size tied to flight-control suites is projected at USD 2.29 billion by 2031, up from USD 1.22 billion in 2025. Draper’s guidance package on Stratolaunch’s Talon-A1 shows how advanced control laws enable hypersonic profiles.

Navigation and guidance modules blend MEMS inertial sensors with celestial and terrain-referenced updates to maintain precision without GNSS. Honeywell’s Compact Inertial Navigation System delivers centimeter accuracy, widening mission envelopes. Communications subsystems pivot toward open-architecture radios with anti-jam modes. Automated launch-and-recovery gear is evolving rapidly to support dispersed operations from roads or naval decks.

By UAV Class: HALE Platforms Capture Strategic Missions

Tactical airframes remained the largest cohort, with a 27.40% share during 2025, reflecting flexibility across brigade and division levels. High-altitude long-endurance craft, though smaller in unit numbers, will lead value growth at a 12.26% CAGR. The UAV payload and subsystems market share for HALE is set to climb sharply as governments fund persistent ISR constellations orbiting above 60,000 ft. China’s WZ-9 “Divine Eagle” anti-stealth platform exemplifies HALE’s role in wide-area missile defense.

Mini and micro categories benefit from squad-level adoption, leveraging advances in nano-gimbals and micro-fuel cells. Fixed-wing architectures still provide best-in-class range and endurance, while VTOL variants solve last-mile deployment constraints, especially in maritime theaters.

By End User: Military Dominance with Government Growth

The military commanded 50.10% of spending in 2025, purchasing premium-grade subsystems certified for contested battlefields. Border security and disaster response agencies are the fastest-growing civilian cohort, adopting rugged versions to secure frontiers and critical infrastructure. US Customs and Border Protection continues Predator-B patrols, validating the crossover of military designs into homeland security roles. Cost-conscious government buyers stimulate demand for scalable architectures, encouraging vendors to deliver COTS-based payload lines that adapt to defense and civilian standards.

Law-enforcement uptake accelerates for crowd monitoring and tactical reconnaissance, though privacy concerns keep operating envelopes restricted. Humanitarian agencies deploy ISR pods for disaster mapping, often leasing capacity through contractor-owned, contractor-operated (COCO) models.

By Application: Combat Missions Gain Prominence

ISR maintained a 49.10% revenue share in 2025. Yet, combat and strike profiles will accelerate fastest at 12.08% CAGR, propelled by loitering munitions and precision-strike systems that deliver kinetic effects at reduced risk. Successes of expendable first-person-view drones in Eastern Europe illustrate cost-disruptive lethality. Mapping and surveying support pre-mission planning, while search-and-rescue remains vital for personnel recovery in denied areas. The UAV payload and subsystems industry increasingly favors multi-mission packages that reconfigure rapidly between ISR and strike roles.

Geography Analysis

North America’s mature defense ecosystem delivered 35.10% of global revenue in 2025. The region benefits from robust R&D and E funding, joint industry-government labs, and clear acquisition roadmaps. The UAV payload and subsystems market leverages volume programs such as MQ-25, XQ-58, and collaborative-combat-aircraft prototypes, ensuring stable OEM order books.

Asia-Pacific registers the steepest 9.62% CAGR. Rising territorial tensions spur indigenous development programs across China, India, Japan, and South Korea. Joint-venture factories in India produce heavy-fuel engines and composite wings, while Singapore’s defense-research agency co-develops AI-navigation chips with local SMEs. Government offsets mandate local content, encouraging supplier footprints across the region.

Europe ranks third by value, sustained by NATO interoperability mandates. The Eurodrone MALE initiative and loyal-wingman projects in the United Kingdom and Italy anchor demand for sensor and EW payloads certified to STANAG standards. However, stringent export rules occasionally hamper third-country sales.

The Middle East shows lumpy yet significant demand tied to rapid capabilities acquisition. Saudi Arabia and the UAE invest in localized final-assembly lines to secure technology transfer, while Israel’s component suppliers continue exporting radar, EO-IR, and datalink kits. Africa remains nascent and limited by fiscal constraints, but is adopting affordable Chinese and Turkish tactical models for border security.

Competitive Landscape

The UAV payload and subsystems market tilts toward moderate concentration. Legacy primes—Lockheed Martin, Northrop Grumman, Boeing, and General Atomics Aeronautical Systems—retain platform integration advantages and long-standing customer links. Their combined presence still accounts for roughly 45–55% of global subsystem revenue. Disruptors such as Anduril and Shield AI compete via AI-native architectures and agile software updates, buoyed by USD 3.76 billion and USD 930 million venture injections, respectively. Strategic partnerships are proliferating: GA-ASI and BAE Systems co-demonstrated autonomous EW on the MQ-20; Honeywell collaborates with Korean Aerospace Industries on open-architecture avionics; and RTX integrates low-SWaP-C AESA radars into emerging Group 3 airframes.

Open-systems mandates erode vendor lock-in. Suppliers promoting interface-agnostic payloads are best positioned for spiraling upgrades. White-space opportunities lie in swarm communication chipsets, solid-state directed-energy power supplies, and sovereign-manufacture rare-earth magnetics. Late-mover disadvantage threatens firms clinging to proprietary buses.

UAV Payload and Subsystems Industry Leaders

Northrop Grumman Corporation

Lockheed Martin Corporation

Israel Aerospace Industries Ltd.

Teledyne Technologies Incorporated

AeroVironment, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Thales introduced a compact electronic warfare payload, designed for small drones, enabling them to detect and pinpoint radio signals.

- May 2025: The United States and Qatar signed a USD 3 billion defense package, including USD 2 billion for MQ-9B Reapers and USD 1 billion for FS-LIDS counter-UAS batteries, signaling sustained export appetite for advanced UAV ecosystems.

- February 2025: HevenDrones introduced 'The Raider', a hydrogen-powered uncrewed aerial system (UAS). The Raider is an advancement of its H2D drone series, boasting enhanced endurance, a wider range of payload options, and an increased payload capacity, especially compared to the H2D55.

- January 2025: Target Arm secured a USD 2.04 million Army Small Business Innovation Research (SBIR) contract to develop its Arsenal-Modular Mission Payload (A-MMP) system. The system enables autonomous launch and recovery of small unmanned aerial systems (sUAS), including rotary and fixed-wing drones.

- September 2024: Draganfly Inc. launched the APEX Drone for military and law enforcement surveillance operations. The APEX offers 45 minutes of flight time and a 5-pound payload capacity for mission-critical applications.

Global UAV Payload and Subsystems Market Report Scope

UAVs are unmanned platforms that utilize onboard sensors to function effectively and perform according to their specified mission profile. The sensors are integrated onboard as payloads are used for controlling several aspects of the flight of the UAVs. Besides providing a complete battlefield assessment from an aerial perspective, the onboard payload systems are also used for gathering mission data and transmitting them to ground-based data centers for evaluation.

The UAV payload and subsystems market is segmented by payload and geography. By payload, the market is segmented into sensors, weaponry, radar, communications, and other payloads. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa. The report also covers market sizes and forecasts of different geographical regions. Moreover, the report offers a market forecast in terms of value in USD million. Furthermore, the report also includes various key statistics on the market status of leading market players and provides key trends and opportunities in the UAV payload and subsystems market.

| Sensors |

| Weaponry |

| Communications and Datalinks |

| Electronic Warfare (EW) Systems |

| Imaging and Mapping Systems |

| Other Payloads |

| Propulsion and Power |

| Flight Control Systems (FCS) |

| Navigation and Guidance |

| Communications and Datalinks |

| Launch and Recovery Systems |

| Nano and Micro UAVs (Less than 2 kg) |

| Mini UAVs (2 to 20 kg) |

| Tactical UAVs (20 to 150 kg) |

| MALE |

| HALE |

| Fixed-Wing VTOL UAVs |

| Military |

| Law Enforcement |

| Intelligence, Surveillance, and Reconnaissance (ISR) |

| Combat/Strike |

| Logistics |

| Search and Rescue (SAR) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Payload Type | Sensors | ||

| Weaponry | |||

| Communications and Datalinks | |||

| Electronic Warfare (EW) Systems | |||

| Imaging and Mapping Systems | |||

| Other Payloads | |||

| By Subsystem Type | Propulsion and Power | ||

| Flight Control Systems (FCS) | |||

| Navigation and Guidance | |||

| Communications and Datalinks | |||

| Launch and Recovery Systems | |||

| By UAV Class | Nano and Micro UAVs (Less than 2 kg) | ||

| Mini UAVs (2 to 20 kg) | |||

| Tactical UAVs (20 to 150 kg) | |||

| MALE | |||

| HALE | |||

| Fixed-Wing VTOL UAVs | |||

| By End User | Military | ||

| Law Enforcement | |||

| By Application | Intelligence, Surveillance, and Reconnaissance (ISR) | ||

| Combat/Strike | |||

| Logistics | |||

| Search and Rescue (SAR) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the UAV payload and subsystems market?

The market is valued at USD 8.61 billion in 2026.

How fast is the UAV payload and subsystems market expected to grow?

It is projected to expand at a 9.49% CAGR, reaching USD 13.55 billion by 2031.

Which region will grow the quickest through 2031?

Asia-Pacific is forecasted to post the fastest 9.62% CAGR, driven by rising defense spending.

Which payload type is expanding the fastest?

Electronic warfare (EW) payloads lead with a 10.16% CAGR as spectrum supremacy becomes critical.

Why are flight-control systems a key investment area?

Autonomous operations in GPS-denied zones demand advanced flight-control suites, pushing this subsystem to an 11.04% CAGR.

Who are the major players in the UAV payload and subsystems market?

Legacy primes-Lockheed Martin Corporation, Northrop Grumman Corporation, Israel Aerospace Industries Ltd., AeroVironment, Inc. and Teledyne Technologies Incorporated-lead in the UAV payload and subsystems market.

Page last updated on: