UAE Product Testing Lab Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

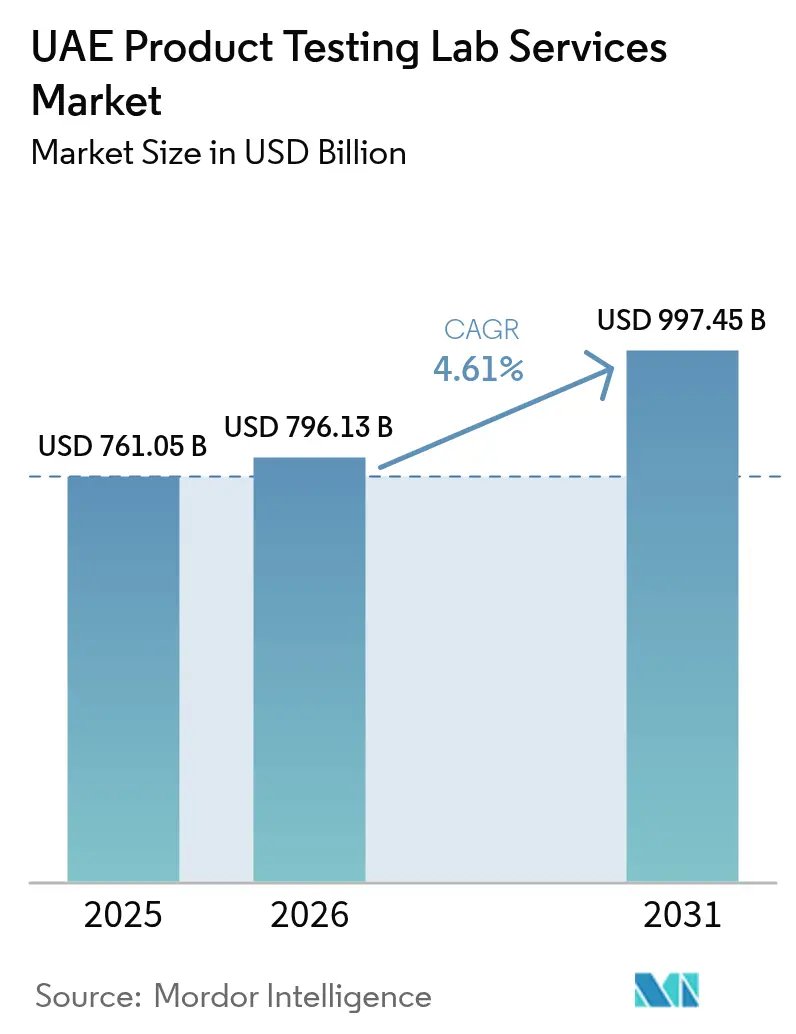

| Base Year Market Size (2025) | USD 761.05 Billion |

| Market Size (2026) | USD 796.13 Billion |

| Market Size (2031) | USD 997.45 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Product Testing Lab Services Market Analysis by Mordor Intelligence

The UAE product testing lab services market size is expected to grow from USD 761.05 million in 2025 to USD 796.13 million in 2026 and is forecast to reach USD 997.45 million by 2031 at 4.61% CAGR over 2026-2031. Heightened enforcement of Emirates Authority for Standardization and Metrology (ESMA) conformity schemes, sustained investments under Operation 300bn, and the expanding portfolio of mega-infrastructure projects are the chief forces shaping expansion. Rising demand for end-to-end quality assurance across consumer, industrial, and infrastructure value chains is reinforcing the dominance of outsourced third-party laboratories. Certification uptake is accelerating as exporters seek “Made in the Emirates” credentials to access wider Gulf Cooperation Council (GCC) markets. Digital-twin-based remote testing, halal compliance verification beyond food products, and sophisticated biotech workflows are creating avenues for niche specialization. Competitive intensity remains moderate because high capital expenditure and accreditation barriers constrain new entrants while favoring incumbents with global networks and advanced instrumentation[1].https://u.ae/en/about-the-uae/strategies-initiatives-and-awards/federal-governments-strategies-and-plans/operation-300bn

Key Report Takeaways

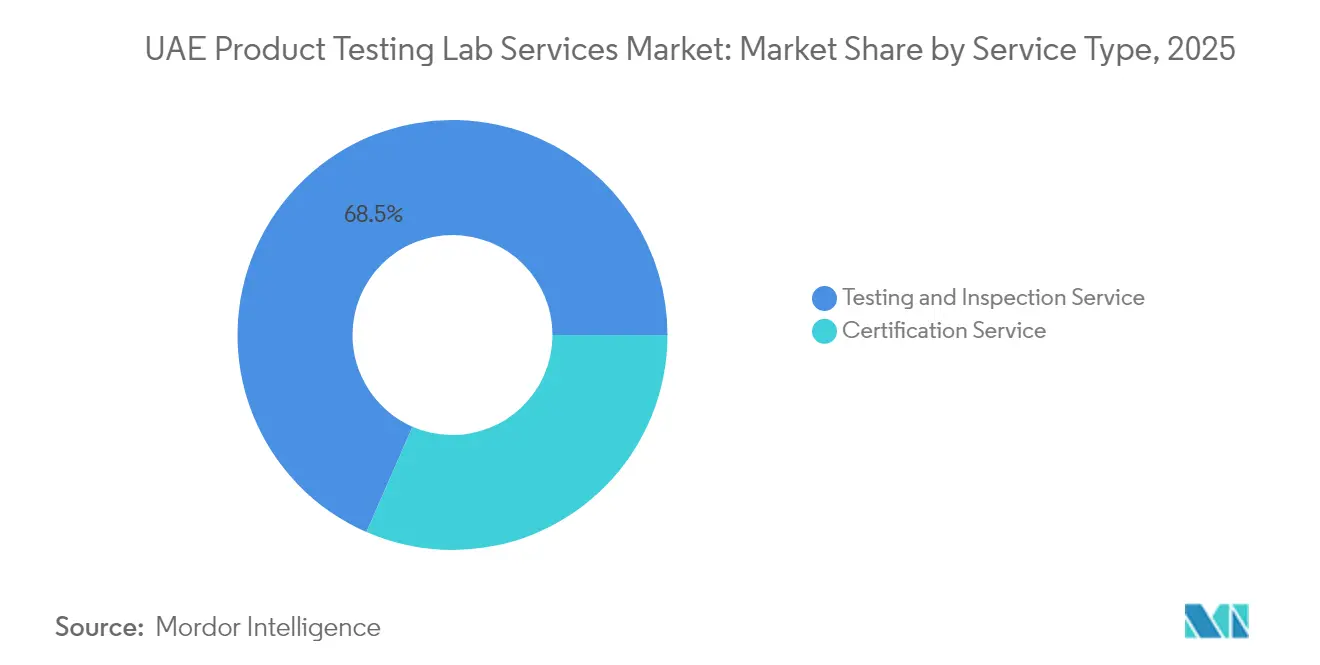

- By service type, testing and inspection held 68.45% of the UAE product testing lab services market share in 2025, while certification services are projected to expand at a 6.43% CAGR through 2031.

- By sourcing, the outsourced segment captured 71.60% share of the UAE product testing lab services market size in 2025 and is expanding at a 6.48% CAGR to 2031.

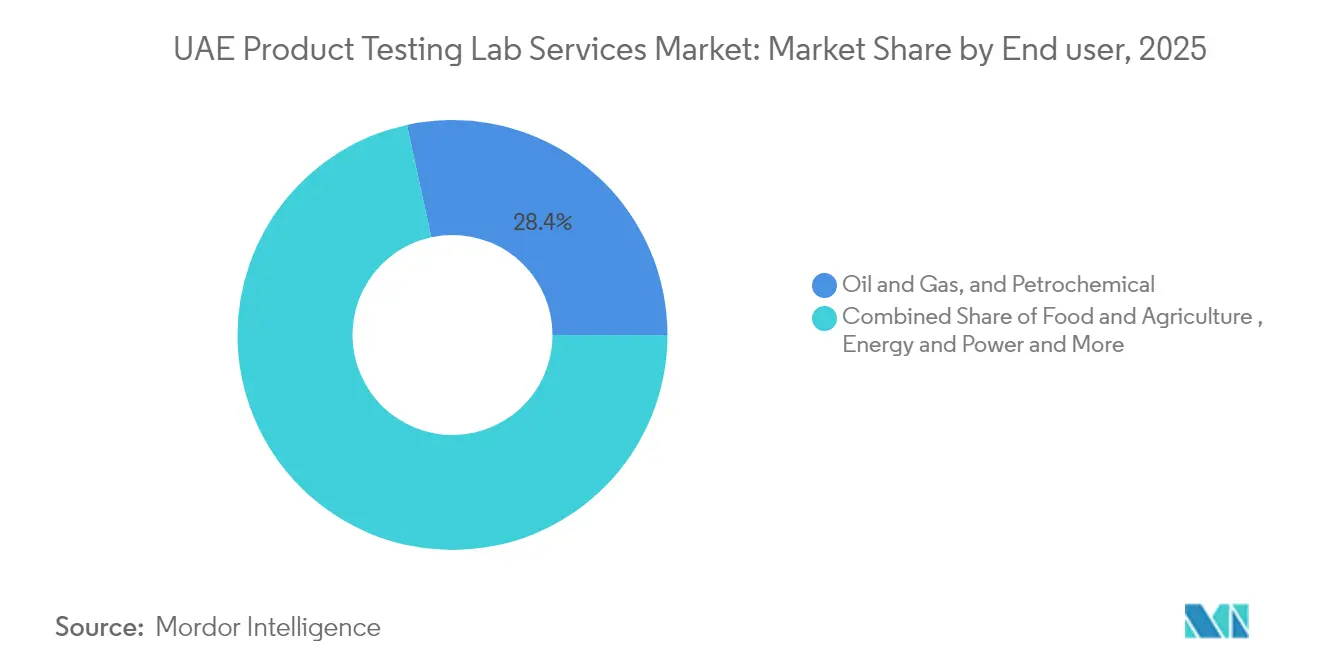

- By end user, oil and gas accounted for 28.40% share of the UAE product testing lab services market size in 2025, and the energy and power segment is advancing at a 6.63% CAGR through 2031.

- By geography, Dubai led with 40.40% revenue share in 2025; Abu Dhabi is advancing at a 6.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Product Testing Lab Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial diversification (Operation 300bn) | +1.8% | National, with concentration in Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Mandatory ESMA conformity schemes | +1.2% | Global, with primary enforcement in UAE | Short term (≤ 2 years) |

| Mega-infrastructure & smart-city projects | +1.1% | Dubai, Abu Dhabi core markets | Long term (≥ 4 years) |

| Local biotech & pharma scale-up | +0.9% | Abu Dhabi, Dubai Healthcare City clusters | Long term (≥ 4 years) |

| Halal compliance testing demand | +0.7% | Global export markets, UAE domestic | Medium term (2-4 years) |

| Digital-twin enabled remote testing in O&G | +0.6% | Abu Dhabi, offshore operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industrial Diversification (Operation 300bn)

The Ministry of Industry and Advanced Technology (MoIAT) targets a GDP contribution from manufacturing of 20% by 2031; this adds new factories in aerospace, precision-machining, and pharma that rely on advanced materials characterization and cleanroom monitoring[2]https://u.ae/en/about-the-uae/strategies-initiatives-and-awards/federal-governments-strategies-and-plans/operation-300bn.Each new line installation must pass vibration, durability, and contamination checks that outsourced partners are uniquely positioned to provide. Laboratories open satellite units inside industrial zones to cut logistics delays, and portable spectroscopy devices shorten approval timelines. The policy’s local-content requirements increase supply-chain traceability audits, driving double-digit growth in supplier qualification and process validation engagements. These contracts favor labs that maintain blockchain-enabled documentation and multilingual audit teams.

Mandatory ESMA Conformity Schemes Drive Market Standardization

ESMA requires every imported or locally manufactured consumer good, construction material, and industrial component to obtain accredited conformity certification, creating durable demand for high-volume safety testing, performance verification, and factory audit services. Laboratories with ISO/IEC 17025 scopes for electrical, mechanical, and chemical analyses gain recurring revenue because importers must renew certificates periodically. The program has broadened to toys, home appliances, and automotive parts, which multiplies test throughput. Multinational labs leverage global expertise to help distributors navigate GCC customs clearance, while domestic facilities add specialized chambers to comply with evolving electromagnetic and environmental protocols. The immediate result is a consistent sample inflow that raises utilization rates and stabilizes cash flows during economic cycles.

Mega-Infrastructure & smart-city projects

Projects such as the Mohammed bin Rashid Al Maktoum Solar Park, Expo City Dubai smart-district upgrades, and the Barakah Nuclear Energy Plant lock in multi-year needs for materials, geotechnical, and nondestructive testing. Each photovoltaic module lot undergoes accelerated aging, salt-mist, and insulation resistance tests executed to IEC standards. Smart-building rollouts demand interoperability and cybersecurity checks for connected sensors before commissioning. Nuclear work scopes include tensile, fracture-toughness, and gamma-spectrometry procedures that only a handful of UAE laboratories can perform, which cements their utilization for up to ten years.

Local Biotech and Pharma Scale-Up

Abu Dhabi’s Omics Centre of Excellence and Dubai’s flourishing contract-manufacturing clusters are propelling requests for sterility, endotoxin, and next-generation sequencing assays. Clinical-grade cleanrooms require environmental monitoring, and every formulation change triggers stability and extractables testing under ICH guidelines. Research hospitals outsource molecular diagnostics such as whole-genome sequencing and liquid biopsy validation, elevating revenue per sample well above commodity chemical analyses. Laboratories holding both College of American Pathologists (CAP) and local Department of Health approvals obtain preferred-provider status, creating high-margin niches within the UAE product testing lab services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour shortage | -1.1% | National, with acute impact in Abu Dhabi, Dubai | Medium term (2-4 years) |

| Cannibalisation by in-house corporate labs | -0.9% | Dubai, Abu Dhabi industrial clusters | Long term (≥ 4 years) |

| High CAPEX for advanced instruments | -0.8% | National, affecting all emirates | Short term (≤ 2 years) |

| Import dependence for reference materials | -0.6% | National, with supply chain vulnerabilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortage

The UAE testing laboratory sector faces acute shortages of qualified technicians, analytical chemists, and specialized testing personnel, particularly in emerging areas including genomics, advanced materials testing, and digital diagnostics. Competition from higher-paying sectors, including oil and gas, healthcare, and technology, creates recruitment challenges for testing laboratories[3]https://www.yellowpages-uae.com/uae/abu-dhabi/food-laboratory-calibration.The requirement for specialized certifications and continuous professional development adds to training costs and staff retention challenges. International recruitment provides partial solutions but involves visa processing delays and cultural adaptation requirements that can impact service delivery timelines and quality consistency.

High CAPEX for advanced instruments

Advanced testing instrumentation costs create significant barriers for laboratory establishment and capability expansion, particularly affecting specialized testing areas, including molecular diagnostics, materials characterization, and environmental analysis. Regulatory requirements for cord blood laboratories demonstrate this challenge, with mandatory AED 10 million bonds per facility limiting market participation to well-capitalized entities. The rapid evolution of testing technologies requires continuous capital investment to maintain competitiveness, while specialized equipment often requires extended validation periods and regulatory approvals. Smaller laboratories face particular challenges in justifying investments for low-volume, high-value testing services, leading to market consolidation around established players with sufficient capital resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification Acceleration in UAE Product Testing Lab Services Market

The UAE product testing lab services market posted a 68.45% revenue tilt toward testing and inspection in 2025, underscoring the abiding need for physical validation at every trade checkpoint. Robust sample inflows from electrical and construction lines enable laboratories to amortize multi-million-dirham chambers efficiently. The segment’s entrenched share reflects its indispensability across heavily regulated downstream sectors.

Certification services are climbing at a 6.43% CAGR to 2031 because GCC wholesalers and African partners increasingly request verifiable product pedigrees before ordering. The UAE product testing lab services market size for certification is expected to exceed USD 345 million by 2031, powered by “Made in the Emirates” labels that demand impartial system audits. Global majors exploit their multi-scheme credentials to bundle factory inspections with customs documentation, while local players partner with Islamic councils to authenticate halal claims for cosmeceuticals.

Accredited bodies also monetize digital certificates stored on blockchain ledgers, which minimizes counterfeiting and speeds customs clearance. Over the forecast, certificate revenues are projected to nearly double their 2025 baseline as more exporters chase preferential tariffs under GCC harmonization.

By Sourcing Type: Outsourced Dominance Shapes UAE Product Testing Lab Services Market

Outsourced laboratories absorbed 71.60% of overall revenue in 2025 and are forecast to advance at a 6.48% CAGR, keeping the model entrenched within the UAE product testing lab services market. Stringent ESMA scopes and MoIAT sector-specific protocols require investments beyond the balance sheets of most manufacturers, making external providers the default path to compliance.

The outsourced segment is propelled by renewable and biotech firms that face sporadic, highly specialized tests that cannot justify in-house labs. Remote witness testing through augmented reality further widens reach and compresses cycle times. By 2031, the UAE product testing lab services market size generated from outsourcing may top USD 792.65 million, bolstered by contracts that bundle calibration, validation, and training.

In-house facilities remain relevant inside flagship oil and gas complexes where continuous corrosion and crude-assay data underpin process safety. Nevertheless, even energy majors outsource non-routine polymer and nano-material evaluations to third parties that own tailored rigs, maintaining outsourced dominance.

By End User: Energy Transition Drives UAE Product Testing Lab Services Market Evolution

Oil and gas contributed 28.40% of 2025 turnover, mirroring legacy refinery, pipeline, and drilling commitments. Routine hydrocarbon fingerprinting, weld integrity checks, and environmental surveillance sustain baseline volumes. Digital twins inside upstream assets raise demand for live data validation that high-spec labs deliver through fiber-linked corrosion probes

The energy and power vertical is climbing at 6.63% CAGR, the fastest among end users, as solar parks, green-hydrogen pilots, and grid-scale batteries call for accelerated life-cycle and resilience studies. The UAE product testing lab services market size for energy applications is on pace to reach USD 118.6 million in 2031. Laboratories are adding UV-fluorescence systems and megawatt-class inverter benches to meet IEC 61215 and IEEE 1547 protocols.

Consumer goods, construction, and agriculture show steady, population-driven throughput. Aerospace and rail push demand for vibration and flame-spread analytics, reinforcing Abu Dhabi’s aerospace industrial zone as a hub for dynamic-test cells.

Geography Analysis

Dubai remained the epicenter of the UAE product testing lab services market in 2025, holding a 40.40% share thanks to Jebel Ali Port, a deep free-zone ecosystem, and investor-friendly licensing. Free-zone rules permit 100% foreign ownership, prompting multinationals to anchor regional headquarters and ISO‐accredited labs in the emirate. Smart-city programs mandate pre-deployment verification for every connected streetlight, elevator sensor, and transit kiosk, sustaining a strong pipeline of electromechanical and cybersecurity tests.

Abu Dhabi is the fastest grower at 6.74% CAGR through 2031, driven by G42 Healthcare’s Emirati Genome Program, record solar investments, and biopharma cluster incentives. The Department of Health has made premarital genetic tests compulsory since February 2025, funneling thousands of additional samples monthly to regional molecular labs. Capital spending in Al Dhafra Solar PV and the upcoming Abu Dhabi Hydrogen Demonstration Plant accelerates electrical and environmental testing engagements, drawing international providers to set up in KIZAD and Masdar City.

Sharjah, Ras Al Khaimah, and Fujairah collectively account for the remainder but maintain mid-single-digit growth as their industrial estates mature. Sharjah’s Hamriyah Free Zone lures steel and polymer extruders that require metallurgical tests, while Ras Al Khaimah’s cement expansion boosts geotechnical investigations. Federal mutual-recognition arrangements allow cross-emirate certificates, so firms in smaller emirates rely on Dubai or Abu Dhabi laboratories for niche methods, optimizing national capacity allocation.

Regulatory Landscape

The UAE product testing lab services market operates under a federal product safety and conformity framework led by the Ministry of Industry and Advanced Technology (MoIAT), with the Emirates National Accreditation System (ENAS) acting as the national accreditation body. For regulated product categories, MoIAT conformity pathways such as the Emirates Conformity Assessment Scheme (ECAS) and Emirates Quality Mark (EQM) link market access to accredited test evidence, and laboratories typically need ISO/IEC 17025 accreditation for their reports to be recognized in conformity files.

In practice, the compliance workflow connects testing outputs to trade enablement, including Certificate of Conformity requirements for market entry and customs clearance, alongside defined options such as a product status statement for specific temporary clearance cases. MoIAT also pushes digitized compliance management through Conformity Hub and related e-services, which raises the need for standardized reporting formats, traceability-ready documentation, and audit-ready quality systems for labs serving importers, manufacturers, and exporters.

Value Chain Analysis

Demand typically starts with importers, local manufacturers, project owners, and government-linked entities that need to meet regulated-product and project specifications, then moves into sampling and testing requests across chemical, mechanical, electrical, microbiology, and specialist workflows. Laboratories (global TIC networks and local specialists) convert samples into test reports, inspection findings, and certification dossiers that feed MoIAT conformity certificate issuance for regulated products, while also supporting municipal and sector-specific approval pathways for construction, infrastructure, and industrial operations.

Upstream inputs include instruments, reference materials, consumables, proficiency testing participation, and qualified staff needed to sustain ISO/IEC 17025 performance and scope maintenance. Downstream interfaces include customs clearance processes and buyer quality assurance programs across oil and gas, energy, food, and consumer goods. A critical structural checkpoint is accreditation and permitting, with ENAS accreditation under MoIAT at the federal level, and Dubai-specific pathways where the Emirates International Accreditation Centre (EIAC) is the accreditation authority and Dubai Municipality requires conformity assessment entities to hold a commercial license and an activity permit under Regulation No. 2 of 2010. Bottlenecks concentrate on maintaining valid accreditation, passing periodic audits, and completing proficiency testing or inter-laboratory comparisons, which increases switching costs for customers and tends to favor labs that can keep broad scopes active across multiple end-user verticals.

Competitive Landscape

Competition rests on accreditation scope breadth, capital resilience, and digital innovation. Global majors SGS Gulf, Bureau Veritas UAE, and Intertek merge international best practices with local field teams to serve energy, consumer, and transport conglomerates. Their worldwide laboratory networks ease re-testing for export markets, a value proposition local firms cannot easily replicate.

Local stalwarts Al Hoty-Stanger Laboratories and Independent Soil Testing Laboratories hold deep relationships with municipal authorities and real-estate developers, ensuring continuous civil-materials throughput. Cord-blood testing has attracted specialist players such as CellSave ADSCC, though AED 10 million bond requirements limit entrants and foster niche concentration.

Technology is becoming the prime differentiator. SGS Gulf’s blockchain-enabled certificate vault slashes customs clearance times, while Bureau Veritas pilots drone-based tank inspections that cut shutdown costs by 40%. Intertek’s AI-powered defect recognition shortens metallography reporting to minutes. Laboratories embracing lab-information-management-system (LIMS) upgrades report double-digit efficiency gains and stronger client retention, indicating a pivot from price to digital value.

UAE Product Testing Lab Services Industry Leaders

Intertek Group PLC

SGS Gulf Limited

Bureau Veritas UAE

Al Hoty-Stanger Laboratories

Lonestar Technical Services LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Digitization of national and emirate-level quality infrastructure is creating room for labs that can embed compliance workflows directly into customer operations. In Abu Dhabi, the Abu Dhabi Quality and Conformity Council (ADQCC) launched the Quality Hub at the Make it in the Emirates (MIITE) 2026 event, and in June 2026 introduced the Mawthooq digital platform to integrate and manage testing and inspection laboratories, including application submissions and certification renewals. These steps increase the value of labs that can deliver faster, standardized, platform-ready data exchange, and package testing together with documentation management for industrial customers scaling local production under Operation 300bn.

Opportunities also cluster around regulated-product expansion and cross-border market access needs that extend beyond basic testing into certification support, factory audits, and multi-scheme readiness. Providers that maintain ENAS (or recognized equivalent) accreditation, MoIAT registration, and the operating prerequisites for conformity assessment bodies, including trade licensing and liability insurance thresholds, can build repeatable service lines linked to recurring certificate cycles, customs processes, and export documentation. Niche specialization areas referenced in the market, including halal compliance verification beyond food products, digital-twin-enabled remote testing in oil and gas, and advanced biotech and pharma testing workflows, support higher-value engagements where scope breadth, recognized approvals, and quality systems differentiate suppliers.

Recent Industry Developments

- June 2026: Intertek announced the full operation of a new energy testing laboratory in the Hamriyah Free Zone, Sharjah, serving energy and commodities customers. The added local capacity strengthens turnaround times for high-frequency testing needs and supports industrial activity outside the Dubai and Abu Dhabi core, aligning with the markets outsourced testing dominance.

- February 2026: SGS in the UAE received authorization from Omans Directorate General for Specifications and Metrology to issue the Omani Quality Mark, effective March 1, 2026. This approval expands a UAE-based TIC providers ability to support cross-border conformity needs, reducing friction for manufacturers and traders seeking Gulf market access through a single service relationship.

- January 2026: Bureau Veritas announced it was awarded an ADNOC inspection services contract for the TA ZIZ Chemicals Industrial Zone in Al Ruwais Industrial City. The win reinforces the role of large industrial zones as multi-year demand anchors for inspection and testing-related services, while increasing competitive pressure on providers without comparable energy and industrial credentials.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is counted as revenues earned in the UAE from product testing lab services that check product safety, quality, and compliance, including lab-based testing and related documentation support needed for market access.

Scope exclusions: It excludes pure inspection-only work done fully on-site without lab testing, consulting-only engagements, and internal in-house testing activity that is not billed as a lab service.

Segmentation Overview

- By Service Type

- Testing and Inspection Service

- Certification Service

- By Sourcing Type

- Outsourced

- In-House

- By End User

- Consumer Goods and Retail

- Food and Agriculture

- Oil & Gas, and Petrochemical

- Construction and Engineering

- Energy and Power

- Industrial & General Manufacturing

- Transportation (Aerospace and Rail)

- Others - Automotive, etc.

- By Geography

- Abu Dhabi

- Dubai

- Sharjah

- Rest of UAE

Data Sources, Market Sizing, and Validation

Desk Research

For this UAE market, we start by compiling the rulebook and demand signals that explain why testing is purchased and how fast volumes can move. Public sources used include national conformity and standards updates (such as ESMA-linked schemes), UAE customs and trade statistics, UAE Federal Competitiveness and Statistics Centre datasets, Dubai and Abu Dhabi government publications on industrial and construction activity, and open technical papers on product safety and laboratory accreditation.

Next, the desk work is converted into inputs that can be modeled. We review company annual reports, investor presentations, press releases, and tender notices to understand service mix, lab expansion plans, and typical customer industries. We then cross-check select company financial and news intelligence databases, an import export shipment-level database, and a patent database to validate activity levels and technology shifts. These desk sources are not exhaustive, and additional public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions with people who buy, specify, or deliver testing in the UAE. This included lab operators, quality heads at manufacturers, importers, and compliance consultants supporting product registrations. We also used calls to confirm how pricing is quoted (per test, per batch, or per certification package), where outsourcing is preferred over in-house labs, and how demand differs across Dubai, Abu Dhabi, Sharjah, and other emirates.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | |

| Mid tier: 42% | Functional/Unit leaders: 41% | |

| Smaller Players: 22% | Managers: 45% |

Market-Sizing & Forecasting

Sizing is built by first reconstructing the serviced demand pool from UAE end-use activity and compliance touchpoints, and then applying testing intensity assumptions that match how often products must be validated (by category and by route to market). The model uses a top-down and bottom-up mix, where the top-down side is anchored on indicators such as import volumes for regulated goods, manufacturing output, construction and infrastructure project flow, and the pace of product registrations and conformity checks.

Those totals are then corroborated with selective bottom-up checks using sampled price per test, typical test bundles, and estimated throughput capacity for accredited labs. Where direct throughput inputs are not available, gaps are handled by using conservative utilization bands. Forecasting relies on scenario analysis with short lists of drivers, including regulatory changes, new lab capacity additions, changes in outsourcing share, and pricing movement for multi-parameter test packages. Assumptions are adjusted after expert feedback so the final growth path stays realistic for the UAE.

Data Validation & Update Cycle

Validation is done in steps so that results do not rely on a single data stream. We compare outputs against independent signals like trade flows, project activity, and disclosed expansion plans, and then we run variance checks across emirates, service types, and end-user industries to spot any outliers.

Before sign-off, the model is reviewed by another analyst, and follow-up calls are triggered when a key assumption shifts or when an unexpected jump appears in a sub-market. Reports are refreshed annually, with interim updates when material events occur. A final pre-delivery review is completed so clients receive an updated view.

Mordor Intelligence's UAE Product Testing Lab Services Market Sizing Compared With Other Published Estimates

Published market sizes for UAE product testing labs do not always match because the boundaries can move, and the same service can be counted under testing only or under broader TIC spending. Differences also come from which year is treated as the base, whether values are reported in millions or billions, and how much of in-house lab work is treated as market revenue.

By tracking service-line revenues and activity drivers like regulated import volumes and conformity testing intensity, Mordor Intelligence keeps the scope tied to paid lab testing services in the UAE. This is why some wider TIC estimates and mixed lab definitions land farther away.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 761.05 M (2025) | |

| Global Research Publisher A | USD 4.54 B (2024) | Uses a broader lab market framing with higher value capture, likely folding in wider testing categories and adjacent TIC and support services. This can inflate the total versus billed product testing lab services only. |

| Industry Publisher B | USD 3.10 B (2024) | Sizes the overall UAE TIC market and then presents a single total, so inspection and certification spend may be included. The boundary between on-site inspection and lab testing is not clearly separated. |

The spread in the table mainly comes from scope, since some sources count a wider TIC wallet while this study keeps the focus on lab testing services that are billed to customers. When the demand pool is rebuilt from clear activity indicators and checked with price and throughput reality checks, the final number is easier to explain and reuse across years.

Key Questions Answered in the Report

What is the current value of the UAE product testing lab services market?

The UAE product testing lab services market size reached USD 796.13 million in 2026.

How fast is the sector growing through 2031?

Revenue is projected to climb to USD 997.45 million by 2031, marking a 4.61% CAGR over 2026-2031.

Which emirate represents the largest regional opportunity for laboratory providers?

Dubai maintained a 40.40% share in 2025 due to its free zones and trade-hub status.

Which end-user vertical is expanding at the quickest pace?

The energy and power segment is advancing at a 6.63% CAGR as renewable projects proliferate.

Page last updated on: