United Arab Emirates Construction And Demolition Waste Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

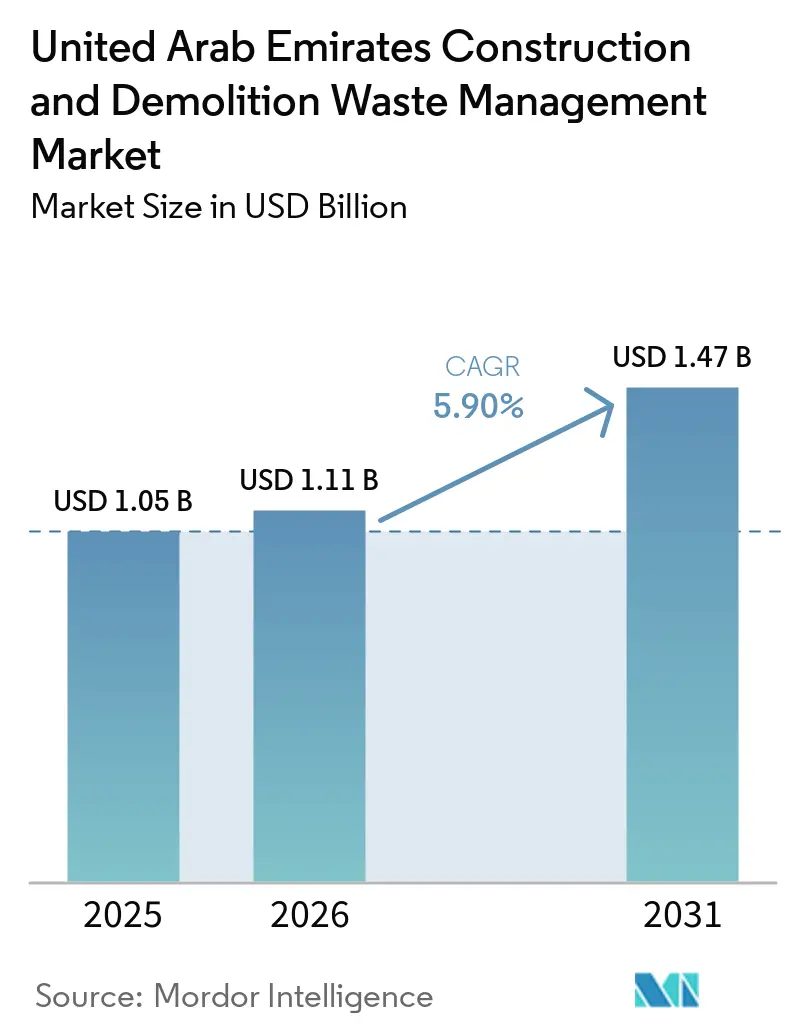

| Base Year Market Size (2025) | USD 1.05 Billion |

| Market Size (2026) | USD 1.11 Billion |

| Market Size (2031) | USD 1.47 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Construction And Demolition Waste Management Market Analysis by Mordor Intelligence

The United Arab Emirates Construction And Demolition Waste Management Market size is expected to increase from USD 1.05 billion in 2025 to USD 1.11 billion in 2026 and reach USD 1.47 billion by 2031, growing at a CAGR of 5.90% over 2026-2031.

Growth in the United Arab Emirates construction and demolition waste management market reflects accelerating landfill-diversion mandates, circular-economy policy enforcement, and rising infrastructure investments in Dubai, Abu Dhabi, and Sharjah. Dubai’s Law No. 18 of 2024 sets a clear end-date for landfills and requires contractors to direct construction and demolition, or C&D, loads to licensed recycling plants, material-recovery facilities, or energy recovery pathways. Law No. 18 of 2024 enforces the 2027 landfill phase-out deadline and mandates routing of C&D loads into licensed channels. Federal policy also enables the substitution of recycled aggregates in road and building works where materials meet specifications, reinforcing market pull for high-quality recovered inputs. C&D streams account for a high share of solid-waste tonnage across the Emirates, which raises the premium on segregation protocols, digital waste tracking, and processing capacity suited to concrete, steel, asphalt, gypsum, and timber in parallel. Enforcement systems now rely on auditable manifests and GPS verification to link demolition completion to lawful disposal, which tightens compliance and supports the United Arab Emirates construction and demolition waste management market’s formalization trend.

Key Report Takeaways

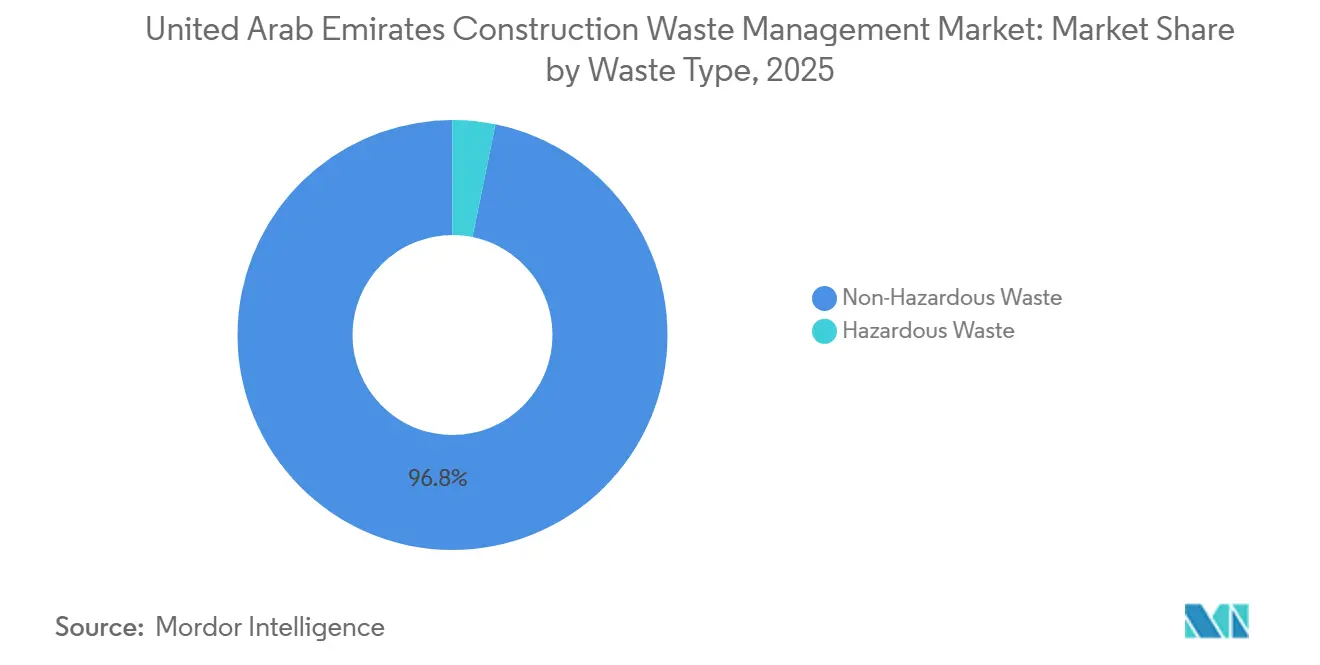

- By waste type, non-hazardous held 96.8% share of the United Arab Emirates construction and demolition waste management market size in 2025, while hazardous is projected to record the fastest growth at 6.2% CAGR through 2031.

- By service, recycling and material recovery led with 39.7% of the United Arab Emirates construction and demolition waste management market share in 2025, while the same segment is forecast to expand at a 5.9% CAGR to 2031.

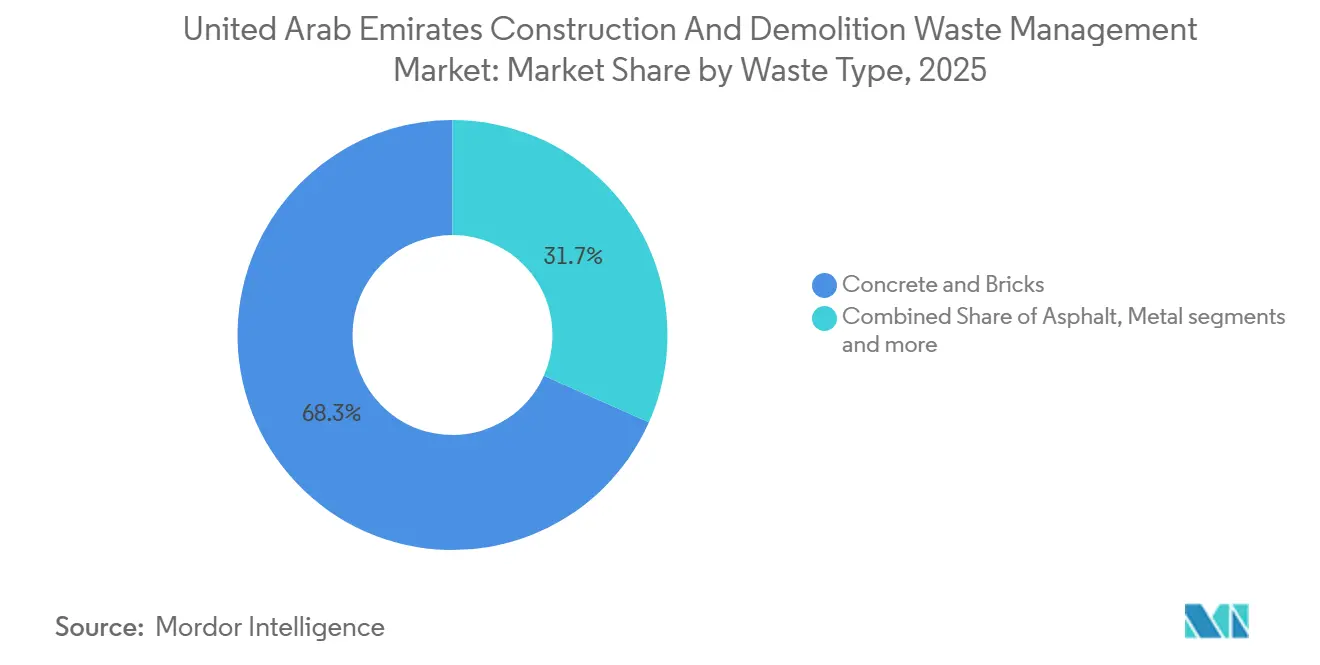

- By material, concrete and bricks commanded 69.0% share in 2025, while gypsum and drywall are the fastest-growing sub-segments at 6.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United arab emirates representing one among them. The global report on construction and demolition waste management market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United Arab Emirates Construction And Demolition Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Construction Activity and Major Infrastructure Development Projects | +1.5% | Dubai and Abu Dhabi core, and spill over to the Northern Emirates | Medium term (2-4 years) |

| Strong Government Regulations and Mandatory Waste Diversion Policies | +1.2% | National, with the strictest enforcement in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| United Arab Emirates Circular Economy Policy 2021-2031 and Net Zero 2050 Targets | +1.0% | National, embedded in federal procurement and strategic planning | Medium term (2-4 years) |

| Green Building Certifications and Sustainability Rating Systems (LEED, Estidama) | +0.8% | National, with early gains in Dubai, Abu Dhabi, and Sharjah | Long term (≥ 4 years) |

| Waste-to-Energy Infrastructure and Advanced Recycling Technologies | +0.7% | National, concentrated in Sharjah, Dubai, Abu Dhabi | Long term (≥ 4 years) |

| Economic Benefits and Cost Savings from Recycled Materials | +0.7% | National, especially relevant for large developers and contractors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Construction Activity and Major Infrastructure Development Projects

Abu Dhabi’s Department of Municipalities and Transport reported approvals for nearly 75 million square meters of development in 2025, spanning residential, industrial, technology, and hospitality uses, which sets up elevated C&D flows in 2026 and 2027. Expo City Dubai has been expanding its exhibition and district-scale capacity to anchor a larger urban innovation hub by 2027, which extends the region’s fit-out and refurbishment cycles and the associated gypsum, packaging, and MEP waste streams. The BINAA AI-driven permits platform, launched in 2025, reduced issuance times for villa permits and cut resubmissions, which accelerates lawful project starts and compresses schedules across the approvals-to-construction pipeline. Building-permit volumes rose in 2025, and training programs upskilled thousands of consultants and contractors, which supports consistent compliance with mandatory waste planning requirements in the years ahead. These trends reinforce the outlook for the United Arab Emirates construction and demolition waste management market as project volumes and fit-outs continue in major development zones.

Strong Government Regulations and Mandatory Waste Diversion Policies

Dubai’s Law No. 18 of 2024, effective thirty days post-publication, codifies strict C&D controls, including perimeter controls at demolition sites and multi-year record-keeping of waste volumes for both non-hazardous and hazardous streams.[1]The Supreme Legislation Committee in the Emirate of Dubai, “Law No. (18) of 2024 Regulating Waste Management in the Emirate of Dubai,” Government of Dubai, dlp.dubai.gov.ae Provisions empower authorities to require the use of recycled inputs or alternative fuels in industrial processes where feasible, reinforcing demand for compliant secondary materials. Federal Law No. 12 of 2018 bans open dumping and burning of C&D waste and imposes corporate penalties that escalate for repeat offenses, which shifts risk calculus toward reliable recycling channels. In Abu Dhabi, the Environment Agency requires GPS-stamped declarations for all waste movements and ties clearance of demolition permits to proof of delivery at licensed sites, which elevates transparency across the waste chain.[2]Environment Agency – Abu Dhabi, “Declaration of Waste Disposal in Licensed Sites,” Environment Agency – Abu Dhabi, ead.gov.ae The United Arab Emirates Circular Economy Policy 2021-2031 adds performance indicators for C&D generation intensity and annual reporting by emirates, which integrates C&D metrics into national sustainability dashboards.

United Arab Emirates Circular Economy Policy 2021-2031 and Net Zero 2050 Targets

Federal policy designates infrastructure as a priority sector for circularity and stipulates measures that prioritize recycled content, update green building codes, and encourage renovation and reuse strategies in project planning. The United Arab Emirates Net Zero 2050 strategy assigns waste a defined program area under a whole-of-economy decarbonization effort, aligning resource efficiency in construction with national climate commitments. Performance tracking for C&D waste per unit of GDP introduces a structural incentive to favor modular construction, prefabrication, and design-for-disassembly, which reduce waste intensity over the life cycle of assets. The policy’s annual reporting and federal coordination tighten accountability across emirates, which translates into more consistent diversion targets and monitoring requirements for project owners and contractors. These frameworks help the United Arab Emirates' construction and demolition waste management market align capital allocation with verifiable environmental outcomes that support ESG-linked financing standards.[3]FAO Legal Office, “UAE Circular Economy Policy 2021–2031,” FAOLEX, faolex.fao.org

Green Building Certifications and Sustainability Rating Systems

Abu Dhabi’s Pearl Rating System requires a minimum 30% diversion of C&D waste for project approval and raises thresholds to 50-70% for higher Pearl tiers, which embeds waste targets into core development workflows. LEED v4.1 awards points for diverting 50% and 75% of C&D waste, which encourages on-site segregation of concrete, steel, timber, and cardboard supported by time-stamped manifests and weighbridge tickets. Dubai’s digital waste control stack requires contractors to maintain compliant documentation and supports AI verification at facilities, which raises confidence in diversion claims used for certification submittals. Federal Law No. 12 obligates source segregation and controlled disposal for exempted materials, which aligns regulatory baselines with rating system expectations on auditability. These certification pathways reinforce demand signals for recycled aggregates and verified material recovery that the United Arab Emirates construction and demolition waste management market can meet at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Awareness and Knowledge on Waste Management Best Practices | -0.5% | National, with gaps in the smaller contractors and subcontractor tiers | Short term (≤ 2 years) |

| Poor On-Site Waste Segregation and Implementation Gaps | -0.4% | National, concentrated in fast-paced urban projects | Short term (≤ 2 years) |

| High Initial Investment Costs for Recycling Infrastructure | -0.4% | National, acute for private investors in the Northern Emirates | Medium term (2-4 years) |

| Market Acceptability and Quality Concerns for Recycled Materials | -0.3% | National, particularly in structural applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Awareness and Knowledge on Waste Management Best Practices

On congested urban sites in Dubai and Abu Dhabi, mixed loads are common when time pressure and heat conditions prompt crews to prioritize task completion over segregation, which leads to rejections at facilities and added costs from re-collection and delays. Contamination levels as low as 5-10% can trigger skip rejection, and rejected loads can cost several thousand dirhams when transport, downtime, and rework are combined, which weakens the economic case for recycling for contractors who do not invest in supervision at the point of generation. Law No. 18 of 2024 places ultimate responsibility for site waste on main contractors, so fragmented subcontractor tiers without continuity or training can amplify audit findings and escalate penalties. Frequent workforce churn and short-term contracts hinder steady behavior change around color-coded bins and load purity, which sustains implementation gaps even where written plans exist. Municipalities now use AI cameras and instant WTN verification to flag discrepancies, which increases the visibility of non-compliance and heightens the need for training and clear on-site controls.

Poor On-Site Waste Segregation and Implementation Gaps

Industry analyses from United Arab Emirates demolition operations show that inadequate source segregation remains the main barrier to high recycling rates, where limited site space, restricted working hours, and neighbor concerns reduce tolerance for multi-bin layouts and frequent collections. In dense precincts with narrow access, single-stream collection is often used to maximize payload per trip, but this choice undermines clean segregation and downgrade rates at material recovery facilities. Project designs and tender documents rarely allocate dedicated sorting zones or set clear diversion targets, which forces late-stage retrofits to waste plans after mobilization when site footprints are already committed. Improper interim storage of items like lithium batteries, paint residues, and combustible timber raises fire risks, which leads supervisors to expedite removal instead of sorting and reduces downstream recyclability. AI-powered inspections now detect mismatches between WTN descriptions and actual loads, and rejected skips impose double transport, idle workforce, and administrative costs that far exceed original disposal fees, which pressures contractors to redesign site processes and supervision.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Waste Type: Non-Hazardous Dominates, Yet Hazardous Streams Accelerate

Non-hazardous streams, including concrete, bricks, clean soil, asphalt, timber, and metals, held 96.8% of tonnage in 2025, the product of concrete-intensive construction typologies and deep excavation works across high-rise and mixed-use assets. The United Arab Emirates construction and demolition waste management market benefits from strict handling rules for hazardous streams that require licensed transport and dedicated facilities, which increases transparency and reduces the incidence of uncontrolled dumping. In parallel, co-processing channels for hazardous residues in cement kilns under federal oversight have expanded lawful end-use options for materials that cannot be conventionally recycled. Hazardous waste includes legacy asbestos-containing materials, paint sludges, contaminated soils, and treated timber, and it is shaped by retrofits and demolitions in older estates alongside strict enforcement that reduces informal disposal incentives. The United Arab Emirates construction and demolition waste management market continues to track these shifts, as project cycles move from heavy civil works to interior fit-outs where composition becomes more complex, and supervision demand rises.

The United Arab Emirates construction and demolition waste management market size for hazardous waste is projected to expand at a 6.2% CAGR through 2031, supported by industrial redevelopments, better declaration of hazardous materials, and wider uptake of licensed handlers. For non-hazardous streams, improved on-site crushing and backfilling have allowed more reuse of concrete and soil, which keeps disposal volumes lower even when construction activity is high. Contractors recognize that a lack of proper declaration can trigger shutdowns or bond forfeitures under municipal enforcement, which creates incentives to plan hazardous-waste workflows early in project timelines. As circular procurement expands, the United Arab Emirates construction and demolition waste management industry is concentrating on traceable chains of custody and quality control so that hazardous streams reach compliant outlets under federal and emirate regulations.

By Service: Recycling and Material Recovery Commands Largest Share and Fastest Growth

Recycling and material recovery led with 39.7% of the United Arab Emirates construction and demolition waste management market share in 2025, driven by mandatory diversion targets and the policy allowance to replace a share of virgin aggregates where specifications are met. The United Arab Emirates construction and demolition waste management market size for recycling and material recovery is forecast to grow at a 5.9% CAGR to 2031, aligned with the closure of remaining landfills in Dubai and expanded processing of clean, segregated loads. Collection and transportation services operate at lower margins due to licensing access and competition, which keeps growth near the market average. Sorting and segregation services now incorporate AI vision and advanced recovery lines, yet manual sorting for mixed loads remains prevalent and limits scalability in fast-track projects. The United Arab Emirates construction and demolition waste management market relies on large, licensed plants that produce quality-assured recycled aggregates for public procurement and infrastructure use in line with emirate specifications.

Gate fees continue to reinforce segregation economics, with lower charges for clean concrete compared to mixed loads, which encourages color-coded skips and on-site supervision to keep loads within specification. Abu Dhabi's Tadweer facility processes roughly 8,000 tonnes per day. Since commencing operations over a decade ago, the facility has produced more than 13 million tonnes of recycled aggregate, with approximately 2.9 million tonnes processed annually in recent years. Sharjah’s integrated complex diverts a very high share of incoming C&D loads and manufactures concrete blocks and pavers from recovered rubble, which strengthens demand for consistent feedstock from contractors. The United Arab Emirates construction and demolition waste management market is also benefiting from licensed energy recovery for non-recyclables, which narrows the role of landfilling and redirects residuals into controlled pathways.

By Material: Concrete and Bricks Anchor Tonnage, Gypsum Growth Reflects Fit-Out Cycles

Concrete and bricks commanded 69.0% of the United Arab Emirates construction and demolition waste management market share in 2025, reflecting cast-in-place methods, precast usage, and masonry in villas and mid-rise assets. Recycled concrete aggregates from licensed facilities meet emirate specifications for bedding, backfill, and haul roads, which supports substitution in public works where quality conformance is documented. Metals such as rebar, aluminum cladding, and copper carry negative disposal costs due to scrap value, which incentivizes thorough segregation at the source. Timber and other organics have secondary uses where contamination risks are controlled under municipal guidelines, which widens circular outlets beyond aggregates. As interior fit-outs intensify in hospitality and commercial towers, gypsum volumes rise and require segregation from concrete to avoid contamination penalties at facilities.

The United Arab Emirates construction and demolition waste management market size for gypsum and drywall is set to grow at a 6.0% CAGR through 2031, driven by recurrent office reconfigurations and hotel refurbishment cycles that emphasize high-purity segregation for downstream recovery. Soil and sand are often reused on-site for landscaping or backfilling, and when exported off-site, they attract lower disposal fees than mixed debris but can still constrain trucking capacity on dense urban projects. The United Arab Emirates construction and demolition waste management market is also shaped by quality assurance processes at material recovery facilities, where AI and manual inspection reduce contamination and maintain specification compliance for recycled outputs. These material-flow patterns reinforce the importance of early-stage waste plans that align with procurement cycles and tender requirements in government and private projects.

Geography Analysis

Dubai generates an estimated 5,000 tonnes of C&D waste daily and contributes a large share of national C&D tonnage, which aligns with sustained building activity in mixed-use districts and growth corridors across the emirate. Law No. 18 of 2024 sets a firm end-date for landfills by 2027 and mandates routing of C&D loads into licensed channels, which makes diversion performance a prerequisite for project close-out. The emirate uses AI cameras at facility entry gates, GPS-tracked bins, and instant verification of Waste Transfer Notes, which raises the cost of non-compliance via load rejections and project delays. Contractors that cannot substantiate diversion performance risk hold on completion certificates under the integrated municipal enforcement framework, which tightens compliance incentives further.

Abu Dhabi accounted for a substantial portion of national C&D flows and approved nearly 75 million square meters of new development in 2025, spanning residential, industrial, and hospitality projects that will raise C&D volumes in the next two years. The emirate’s Tadweer facility processes roughly 8,000 tonnes per day and has produced more than 13 million tonnes of recycled aggregate since operations began, and these outputs are now standard in road contracts and public works. Abu Dhabi’s Pearl Rating System sets a 30% minimum diversion baseline for project approvals and tightens requirements to 50-70% for higher Pearl tiers, which integrates waste performance into approvals and certification. EAD mandates digital declarations that link waste movements to licensed facilities, which binds demolition clearances to lawful disposal and supports audit trails across the chain of custody.

Sharjah and the Northern Emirates contribute a smaller share of national tonnage yet drive innovation in integrated processing and advanced recovery. BEEAH’s complex in Sharjah achieves a citywide diversion rate above 90% and processes more than 500,000 tonnes annually through specialized sorting and material remanufacturing lines, which demonstrates scalable circular operations. The Sharjah waste-to-energy plant is on track to double its output to about 60 MW by late 2026, expanding controlled outlets for non-recyclable fractions and reducing reliance on landfilling. BEEAH also announced the Middle East’s first commercial-scale hydrogen-from-waste facility, expected to produce about 7 tonnes per day of fuel-cell grade hydrogen in its initial phase by 2027, which signals new circular energy vectors for hard-to-recycle waste. Dulsco’s sites in Ajman and Umm Al Quwain divert a high share of intake and recover aggregates and sand for reuse, and the company demonstrated high diversion performance during Expo 2020 operations. These operating profiles show how the United Arab Emirates construction and demolition waste management market advances through both integrated anchor facilities and focused regional capacity that together cover multi-stream processing and verified outputs.

Competitive Landscape

The United Arab Emirates construction and demolition waste management market features several vertically integrated operators alongside a long tail of licensed haulers and specialists that compete on responsiveness and niche services. BEEAH Group operates a multi-facility complex in Sharjah that achieves a very high diversion rate and produces recycled-concrete products and alternative fuels for industrial use, which supports reliable circular outlets at scale. Tadweer Group runs high-throughput processing in Abu Dhabi and participates in energy recovery partnerships, which positions it to convert non-recyclables into controlled energy outputs under municipal oversight. Holcim’s Geocycle United Arab Emirates co-processes hazardous residues and tire shreds under federal permits in cement kilns, which provides compliance-grade outlets for streams that cannot be mechanically recycled. Dulsco Environment operates regional facilities with high diversion performance and demonstrated large-scale event operations, which indicates strong capability in integrated collection, sorting, and material sales. Competitive advantage is shaped by regulatory know-how, quality assurance, and secured off-takes that stabilize revenue across multiple material streams under evolving diversion mandates.

Strategy patterns in the United Arab Emirates construction and demolition waste management market include asset builders investing in waste-to-energy and hydrogen-from-waste facilities, circular integrators bundling demolition, sorting, and remanufacturing, and digital enablers improving routing and reporting to cut transaction costs. BEEAH and KEZAD Group formed a joint venture in January 2026 to deliver integrated services across Abu Dhabi economic zones and free zones, adding a Circular Environmental Facility and staged rollouts covering collection, tracking, sorting, and later recycling and recovery. BEEAH also launched facilities management services that leverage environmental expertise in digitalized, net-zero-oriented building operations, which widens its solutions portfolio across the built environment. Hazardous-waste logistics and co-processing remain a differentiator for Geocycle under strict federal oversight, while circular material producers benefit from long-term agreements with cement and construction-materials buyers that substitute fossil inputs with waste-derived fuels and aggregates.

White-space opportunities concentrate on mobile crushing close to large jobsites, hazardous-waste handling for free-zone retrofits, and advisory services to develop C&D waste management plans aligned to municipal digital systems. Documentation via Waste Transfer Notes, GPS-stamped manifests, and time-stamped weighbridge tickets is now a non-negotiable baseline that bidders must demonstrate for public-sector and class-A private projects. Main contractors hold responsibility for site waste under Dubai’s framework and need to invest in training and supervision to keep contamination below rejection thresholds at material recovery facilities. As municipalities expand digital verification, performance gaps between tier-one operators and smaller haulers are likely to drive partnerships or consolidation, which will support quality and traceability standards that the United Arab Emirates construction and demolition waste management market increasingly requires.

United Arab Emirates Construction And Demolition Waste Management Industry Leaders

Bee'ah (BEEAH Group)

Averda

Imdaad

Al Dhafra Recycling Industries (Tadweer)

Green Mountains Recycling Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Abu Dhabi’s Department of Municipalities and Transport reported approvals for nearly 75 million square meters of development in 2025 and highlighted the BINAA AI-driven permits platform’s impact on reducing processing times and resubmissions, which supports orderly project mobilization and code compliance.

- January 2026: KEZAD Group and BEEAH Group formed a 51-49 joint venture to deliver integrated waste services across Abu Dhabi’s economic cities and free zones, beginning with collection, tracking, sorting, and street cleaning, and expanding to recycling, composting, and industrial waste recovery.

- January 2025: BEEAH and partners announced the Middle East’s first commercial-scale hydrogen-from-waste plant in Sharjah, with commissioning of the initial phase targeted for 2027 and planned daily output of fuel-cell grade hydrogen in the first stage.

- January 2025: BEEAH and Masdar announced Phase Two expansion plans for the Sharjah Waste to Energy plant to double output and increase processing capacity for hard-to-recycle waste under a joint venture framework.

United Arab Emirates Construction And Demolition Waste Management Market Report Scope

The UAE Construction and Demolition Waste Management Market is Segmented by Waste Type (Non-Hazardous Waste, and Hazardous Waste), by Material (Concrete & Bricks, Asphalt, Metal, Timber, Soil and Sand, Gypsum & Drywall, and Others), by Service (Collection & Transportation, Sorting & Segregation, Recycling & Material Recovery, and Landfilling & Disposal), and by Geography (UAE). The Market Forecasts are Provided in Terms of Value (USD).

| Non-Hazardous Waste |

| Hazardous Waste |

| Concrete & Bricks |

| Asphalt |

| Metal |

| Timber |

| Soil and Sand |

| Gypsum & Drywall |

| Others (Plastic, Treated Wood, Glass) |

| Collection & Transportation |

| Sorting & Segregation |

| Recycling & Material Recovery |

| Landfilling & Disposal |

| By Waste Type | Non-Hazardous Waste |

| Hazardous Waste | |

| By Material | Concrete & Bricks |

| Asphalt | |

| Metal | |

| Timber | |

| Soil and Sand | |

| Gypsum & Drywall | |

| Others (Plastic, Treated Wood, Glass) | |

| By Service | Collection & Transportation |

| Sorting & Segregation | |

| Recycling & Material Recovery | |

| Landfilling & Disposal |

Key Questions Answered in the Report

What is the current size and growth outlook for the United Arab Emirates construction and demolition waste management market?

The United Arab Emirates construction and demolition waste management market size was USD 1.05 billion in 2025 and is projected to reach USD 1.47 billion by 2031 at a 5.9% CAGR during 2026-2031.

Which services and materials lead performance in the United Arab Emirates construction and demolition waste management market?

Recycling and material recovery led with 39.7% share in 2025, while concrete and bricks accounted for 69.0% by material, and gypsum is the fastest-growing sub-segment at 6.0% CAGR through 2031.

What regulations most influence C&D waste handling in the United Arab Emirates?

Dubai’s Law No. 18 of 2024 mandates diversion to licensed facilities, Federal Law No. 12 of 2018 bans open dumping and burning, and Abu Dhabi’s EAD requires GPS-stamped disposal declarations for licensed sites.

What are the main on-site challenges to improving diversion rates in the United Arab Emirates?

Limited space, fast schedules, and heat can lead to mixed loads that facilities reject, which adds double transport and rework costs and requires tighter supervision and training to keep contamination low.

How do Abu Dhabi and Dubai differ in their C&D waste compliance frameworks?

Dubai ties completion to documented diversion and digital verification under Law 18 of 2024, while Abu Dhabi combines Pearl Rating diversion floors with EAD’s GPS-stamped declarations for lawful disposal.

Which recent corporate actions matter most in the United Arab Emirates C&D space?

The KEZAD–BEEAH joint venture for integrated services, BEEAH’s Sharjah waste-to-energy expansion, and Geocycle’s hazardous-waste co-processing footprint strengthen capacity and compliance-grade outlets.

Page last updated on: