Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.88 Billion |

| Market Size (2026) | USD 7.21 Billion |

| Market Size (2031) | USD 9.11 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Event Management Market Analysis by Mordor Intelligence

The GCC event management market size was valued at USD 6.88 billion in 2025 and estimated to grow from USD 7.21 billion in 2026 to reach USD 9.11 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031). Growth rests on sovereign diversification plans, post-pandemic MICE recovery, and a large, digitally fluent youth cohort that craves immersive festivals and esports tournaments. Saudi Arabia’s Vision 2030 and Dubai’s visitor-economy agenda incentivize next-generation venues while Qatar leverages World Cup legacy facilities to pull blue-chip conferences. Mobile ticketing, AI-driven audience analytics, and augmented-reality crowd engagement tools lift monetization and sponsorship conversion, thereby nudging the GCC event management market toward data-centric business models. Meanwhile, the revenue mix is tilting away from pure exhibitions toward hybrid business-plus-lifestyle gatherings that string together conferences, concerts, and influencer-led pop-ups. Operators that fuse global standards with Arabic-first digital experiences and low-carbon operations hold a clear competitive advantage when vying for state contracts or ultra-premium brand activations.

Key Report Takeaways

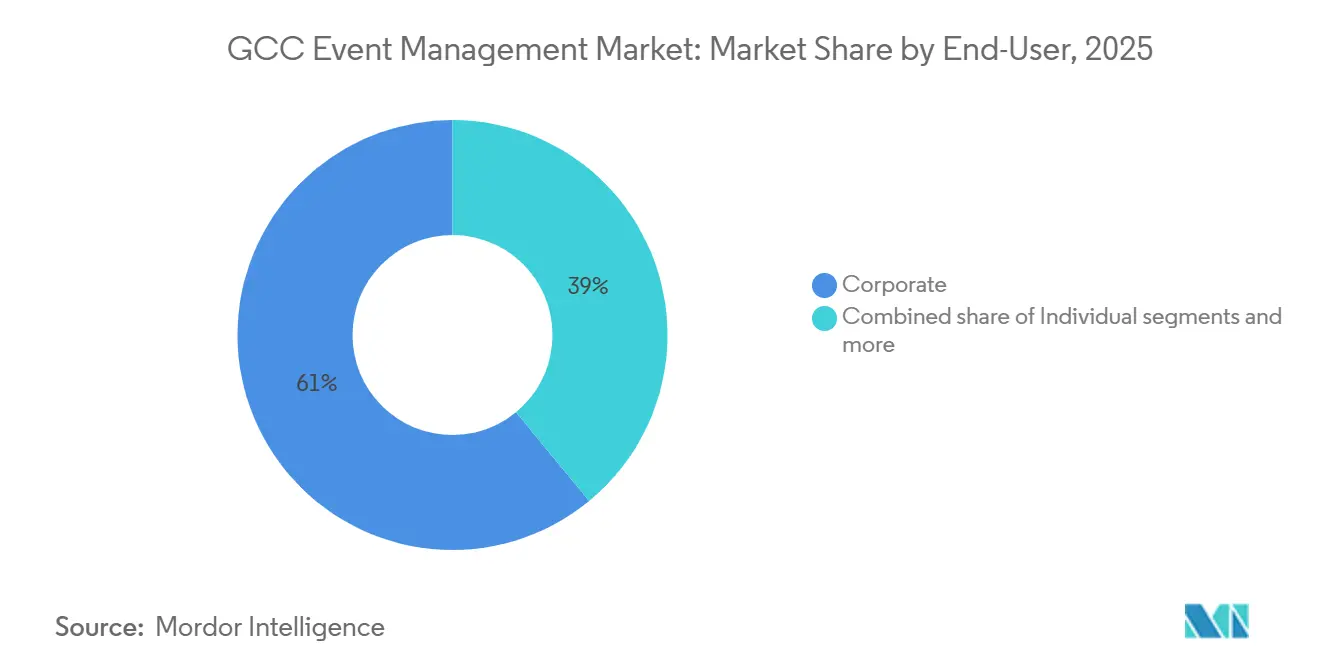

- By end-user, corporate accounted for 60.96% of the GCC event management market share in 2025, while the public segment within the GCC event management market size is projected to grow at the fastest CAGR of 12.42% between 2026 and 2031.

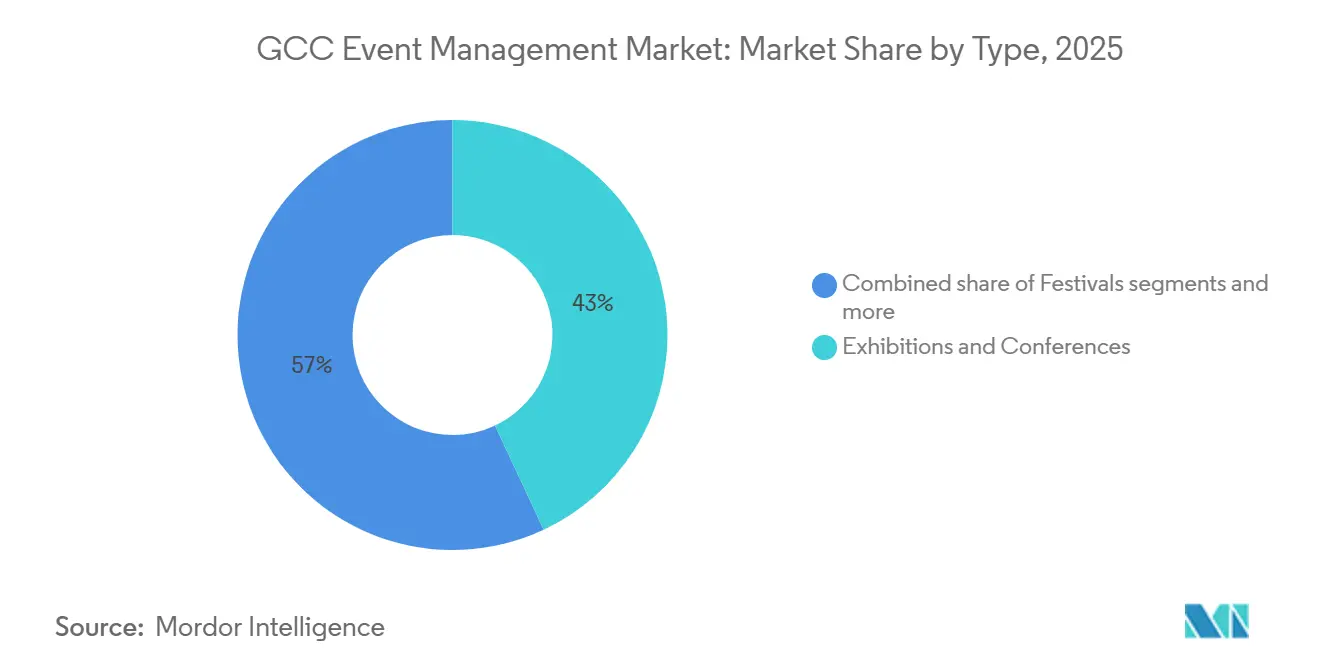

- By type, exhibitions & conferences captured 43.03% of the GCC event management market share in 2025, whereas the GCC event management market size for festivals is forecast to expand at a CAGR of 13.78% from 2026 to 2031.

- By revenue source, ticket sales represented 53.22% of the GCC event management market share in 2025, while the GCC event management market size for sponsorships is expected to post a growth rate of 11.94% CAGR during 2026–2031.

- By geography, Saudi Arabia led with 45.20% of the GCC event management market share in 2025, while the GCC event management market size in Qatar is anticipated to witness the highest growth rate at 13.21% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Event Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dubai's Vision 2030 & tourism initiatives fuel mega-projects | +1.8% | Saudi Arabia, United Arab Emirates core, spillover to Qatar, Bahrain | Long term (≥ 4 years) |

| Government boosts events with supportive policies & funding | +1.2% | GCC-wide, strongest in Saudi Arabia & United Arab Emirates | Medium term (2-4 years) |

| Corporate MICE demand rebounds strongly after the pandemic | +0.9% | Global, with GCC benefiting from Asia–Middle East corridor expansion | Short term (≤ 2 years) |

| Shifting consumer preferences & youth-centric trends drive growth | +0.7% | Saudi Arabia, United Arab Emirates, Qatar lead, moderate in Kuwait, Bahrain, Oman | Long term (≥ 4 years) |

| Adoption of mobile, fraud-proof digital ticketing on the rise | +0.5% | United Arab Emirates & Saudi Arabia early adopters, Qatar and Kuwait follow | Medium term (2-4 years) |

| Global audiences captivated by AI/AR immersive experiences | +0.6% | United Arab Emirates and Saudi primary hubs, selective Qatar venues | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dubai's Vision 2030 & tourism initiatives fuel mega-projects

Saudi Arabia’s multiyear capital program for sports, culture, and entertainment builds sustained demand for venues and city-scale logistics that support large delegations and high-capacity events. The FIFA World Cup 2034 award and the Asian Winter Games 2029 at Trojena underscore a pipeline that enhances the GCC event management market through 2031 and beyond [1]Source: Saudi Vision 2030, “Saudi Vision 2030 Annual Report 2024,” Government of Saudi Arabia, vision2030.gov.sa. Dubai’s established exhibition and convention ecosystem continues to secure global meetings, and Expo City’s growth plan adds flexibility for multi-venue formats and legacy events that repeat annually. Saudi Arabia’s Events Investment Fund target for foreign direct investment signals underwriting support for venue development, which strengthens bids for flagship events that draw international attendance [2]Source: German-Saudi Arabian Liaison Office, “Events Investment Fund Overview,” GESALO, german-saudi-business.org. Metro and airport capacity upgrades reduce access bottlenecks and extend average dwell time per attendee, improving exhibitor and sponsor return within the GCC event management market.

Government boosts events with supportive policies & funding

Saudi Arabia’s General Entertainment Authority processed a high volume of licenses in 2024 and enabled attendance at scale, which indicates lower permitting friction and stronger support for compliant organizers. Budget allocations to municipal services and economic resources add a fiscal backstop for festivals and trade events when delivery risk is high, which increases the confidence to schedule multi-year programs. The planned unified GCC tourist visa aims to reduce cross-border travel barriers and encourages itineraries that include multiple stops across the region for association congresses and corporate roadshows. Qatar’s liberalized entry policy for 95-plus nationalities eases planning for organizers that serve international communities and helps scale MICE attendance in Doha within the GCC event management market. New sustainability duties in the United Arab Emirates require greenhouse-gas reporting, which rewards larger organizers that can invest in measurement and supplier alignment.

Corporate MICE demand rebounds strongly after the pandemic

Business events in Saudi Arabia and the United Arab Emirates captured significant bid wins in 2025, including medical congresses and policy forums that value in-person networking and sponsor activations. Corporate event budgets remain flexible for strategic conferences, which supports multi-year contracts and steadier calendars for organizers in the GCC event management market. Dubai’s record-setting pipeline reinforced destination preference for high-assurance event delivery and diverse venue formats, while Saudi Arabia’s MICE growth rate signals long-term share gains as new infrastructure opens. Organizers are consolidating post-event content workflows to sustain year-round engagement and nurture sponsor outcomes across cycles. The net effect is a higher baseline of recurring events that sustains floor space demand, exhibitor pipelines, and premium sponsorship inventory in the GCC event management market.

Adoption of mobile, fraud-proof digital ticketing on the rise

AI-enhanced search and discovery on leading ticketing portals reduces friction and lifts conversion, particularly for price-sensitive and time-sensitive queries in the GCC event management market. Blockchain-based ticketing research shows that lightweight AI can flag suspicious activity in real time, which reduces scalping and improves access equity for fans. Pilots tied to marquee seasons in Saudi Arabia indicate that higher-capacity venues may require fraud prevention features to secure licenses over time [3]Source: General Entertainment Authority, “Statistics and Licensing,” Government of Saudi Arabia, gea.gov.sa. Payment diversity and refund guarantees on third-party platforms reinforce trust and encourage a shift from legacy box offices to digital checkouts. User scale on regional platforms suggests a behavioral tipping point that accelerates online purchasing across categories in the GCC event management market [4]Source: Platinumlist, “Ticketing and Event Discovery,” Platinumlist, platinumlist.net. Organizers that adopt fraud-resistant systems gain pricing confidence for premium tiers and can protect brand equity against undercutting on secondary markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outdoor events in the GCC face challenges from seasonality and the region's extreme climate | -0.8% | GCC-wide, most acute in Kuwait and United Arab Emirates interior regions | Short term (≤ 2 years) |

| GCC event management market is constrained by a limited pool of certified professionals | -0.6% | Saudi Arabia, United Arab Emirates pressure zones | Medium term (2-4 years) |

| Geopolitical and security concerns are affecting event attendance | -0.4% | GCC-wide, event-specific sensitivity | Medium term (2-4 years) |

| Low penetration of event insurance increases risks for organizers | -0.3% | Saudi Arabia, United Arab Emirates, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outdoor events in the GCC face challenges from seasonality and the region's extreme climate

Record high temperatures in 2025 confirmed that outdoor events are economically viable in cooler months only, which compresses the schedule and increases competition for peak-season dates. Flash floods in 2024 disrupted air travel and ground transport, showing that even shoulder months carry weather risks that force last-minute cancellations or format changes. Thermal mitigation systems help at the margin, but energy use and compliance with net-zero commitments limit deployment at scale. Peak-season venue rates move higher as demand concentrates, which creates budget pressure for mid-tier organizers in the GCC event management market. City-level drainage and stormwater projects will help later in the decade, but near-term calendars remain vulnerable to weather volatility.

GCC event management market is constrained by a limited pool of certified professionals

New hotel inventory opened in 2025 and more is under construction through 2026, which increases demand for experienced operations, revenue management, and sales talent. Saudization and Emiratisation quotas raise compliance costs and intensify hiring competition, which increases turnover risk for private organizers in the GCC event management market. Subsidy programs in the United Arab Emirates support entry-level hiring, but do not solve for senior expertise required to deliver large, complex events on tight timelines. Recruitment firms report multiple offer situations for critical roles, which inflates compensation and squeezes margins for independent promoters. Micro-credential programs accelerate frontline skills but may not fill strategic gaps in contract negotiation and risk modeling in the GCC event management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Corporate Dominance Masks Public Segment’s Coming Surge

In 2025, corporate clients accounted for 60.96% of the GCC event management market share as in-person selling and relationship-building returned to pre-pandemic levels for leadership forums, product launches, and global sales meetings. Organizers with multi-year association contracts captured stable revenue, while single-event corporate off-sites faced tighter budgets and tougher pricing discussions. Governments are accelerating cultural programs and public festivals that drive inbound tourism and city branding, which lifts the public segment growth outlook within the GCC event management market. Visa reforms and destination marketing broaden the base for association congresses and sector showcases, especially as venue capacity increases in Saudi Arabia. ESG reporting requirements in the United Arab Emirates shape procurement cycles and supplier selection, which adds a compliance premium to frequent corporate events and favors better-capitalized operators.

The public segment is forecast to post the fastest growth at 12.42% CAGR through 2031 as sovereign-backed programs underwrite large-scale cultural calendars and destination festivals. Individual consumers benefit from rising disposable income and a steady slate of weekend entertainment, which spreads demand across music, sports, and family-friendly formats in the GCC event management market. As calendars mature, repeatable citywide events anchor hotel bookings and airlift, which strengthens sponsor propositions and improves planning certainty. Organizers that align with public-sector funding cycles can secure prime dates and premium venues, while those reliant on discretionary corporate demand must differentiate on content and attendee value. These patterns keep corporate spend as the baseline but position the public segment as the growth engine across 2026–2031 for the GCC event management industry.

By Type: Exhibitions Lead, but Festivals Clock Fastest Growth at 13.78% CAGR

Exhibitions and conferences captured 43.03% in 2025, supported by high-density venues in Dubai and ongoing capacity expansion in Riyadh that reinforce the GCC event management market. Exhibitions concentrate B2B value in shorter time windows and drive wider supplier ecosystems from stand design to lead-generation services. Festivals are projected to expand at a 13.78% CAGR through 2031 as cultural calendars and live entertainment scale across Saudi Arabia and the United Arab Emirates. Corporate events and seminars deliver predictable mid-tier volumes, while sports events bifurcate between marquee draws and participation-led formats with thinner margins. Music concerts face cost inflation for headline talent and production, which increases reliance on sponsor revenue and premium hospitality tiers in the GCC event management market.

Format choices reflect venue availability and sponsor objectives, with exhibitions sustaining repeat bookings due to measurable exhibitor outcomes and festivals scaling with broad consumer appeal. Regulations differ by format and jurisdiction, which adds planning complexity for alcohol service, family zoning, and crowd management. Sustainability certifications are now routine for government tenders, which favors established exhibition organizers with environmental management systems. Long-lead exhibitions are sensitive to macro slowdowns that delay capital purchases, while festivals carry weather and headline-talent risk that peak in the warmer months. These trade-offs keep exhibitions as the revenue anchor while festivals drive incremental growth for the GCC event management industry.

By Revenue Source: Ticket Sales Dominant, Sponsorships Fastest at 11.94% CAGR

Ticket sales represented 53.22% of the GCC event management market size in 2025, led by festivals, concerts, and sports that monetize seats and standing space across cooler months. Capacity ceilings and seasonality cap the expansion of sellable inventory, which shifts the growth focus to higher yield from premium tiers and bundled experiences. Sponsorships are forecast to grow at 11.94% CAGR through 2031 as brands pay more for exclusive rights, data packages, and curated hospitality access at marquee events in the GCC event management market. Organizers are building sponsor-success teams to improve activation design and reporting that sustains multi-year renewals. Other revenue sources, such as merchandise, vendor fees, licensing, and VIP experiences, offer incremental yield that scales with audience quality.

Ticket revenue grows with attendance, while sponsorship grows with audience profile and media reach, which makes sponsor strategy a priority for organizers with premium calendars. Partnerships like exclusive payment providers add a high-margin layer above ticket yields and create cross-promotion channels. Digital ticketing data enables segmentation and audience insights that improve sponsor ROI and on-site conversion within the GCC event management market. Organizers are refining tiered offerings to reduce discounting late in the cycle and to protect price integrity against secondary markets. These shifts place sponsorship and data-driven services at the center of growth while tickets remain the volume foundation of the GCC event management market size.

Geography Analysis

Saudi Arabia led with 45.20% of the GCC event management market share in 2025 as NEOM, Qiddiya, and large civic infrastructure projects translated into higher venue capacity and a more diverse event mix. Government-backed investment vehicles reduce delivery risk for new builds and encourage scheduling of global-scale events that attract multi-day stays. Talent constraints and localization mandates add operational complexity, which increases the value of strong local partnerships and robust training programs. The United Arab Emirates remains a leading destination for established conferences and exhibitions, with Dubai’s 2024 results demonstrating consistent bid wins and delegate counts that support high hotel occupancy. Abu Dhabi’s focus on motorsport, culture, and sustainability adds complementary formats that spread demand across the calendar.

Qatar is projected to post the highest growth at a 13.21% CAGR in 2026–2031, supported by Expo 2030-related investments, visa facilitation, and a MICE strategy that targets association events and sector showcases. As Saudi Arabia and Qatar sprint to expand hotel inventory and transit capacity, organizers gain more options for large delegations and multi-venue formats. Bahrain and Oman compete with niche verticals and cost-competitive propositions, which suit specialized events with targeted audiences in the GCC event management market. Smaller domestic populations and airlift limits require tighter alignment between event formats and destination strengths. Seasonal climate constraints shift outdoor activity to coastal and highland locations, which concentrate peak-season calendars in Jeddah, Dubai, and Doha.

During 2026–2031, Saudi Arabia’s capacity additions and demand programs are expected to shift more international events eastward from Dubai while Qatar’s liberalized entry policies increase the probability of repeat bookings. The unified GCC tourist visa, once activated, should improve multi-stop itineraries and lift cross-border attendance for itinerant events that cycle through GCC cities. Organizers that align date selection with climate windows and infrastructure readiness will optimize delivery risk and attendee experience for the GCC event management market. Within this context, the GCC event management market size for Qatar is projected to expand at a 13.21% CAGR between 2026 and 2031 under the current policy and project pipeline.

Competitive Landscape

Competitive intensity is rising as large platforms pursue vertical integration across software, ticketing, venue operations, and analytics within the GCC event management market. Cvent’s 2025 acquisitions of ON24 and Goldcast expand post-event content automation and hybrid delivery features that larger conference organizers require. Live Nation Middle East deepened its Expo City Dubai partnership to manage multiple anchor venues and to embed zero waste and renewable energy priorities into event operations. These moves differentiate on compliance, reporting, and sponsor ROI, which are critical for winning government tenders and multi-year contracts. Organizers that cannot meet sustainability or data standards face higher barriers to entry in the GCC event management market.

At the same time, tier-two and tier-three specialists grow by focusing on verticals where subject-matter expertise and association relationships outweigh economies of scale. Ticketing platforms deploy AI-based discovery and fraud prevention research to capture market share from legacy box office models. General service contractors differentiate through verified environmental credentials and supplier programs that reduce event waste and emissions. These capabilities are increasingly important to secure public-sector work in Saudi Arabia and Qatar. The resulting pattern is a barbell shape that privileges integrated leaders at the top and nimble specialists in niches across the GCC event management market.

Commercial models now emphasize sponsor-led economics and post-event engagement to offset inflation in production, venue, and talent costs. Exclusive payment partnerships, presale programs, and premium hospitality tiers expand marginal revenue per attendee for concerts and festivals. In exhibitions, AI matchmaking and first-party data unlock better exhibitor outcomes and contract renewals, which stabilize floor plans and budgets. Across segments, platforms that unify ticketing, content, analytics, and sustainability reporting hold an advantage when bidding for headline events in the GCC event management market. Over the next planning cycle, category leaders will likely continue M&A or long-term operating partnerships to secure venue access and strengthen sponsor pipelines.

GCC Event Management Industry Leaders

SELA

MDLBEAST

Live Nation Middle East

Flash Entertainment

Platinumlist

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Cvent completed the acquisition of ON24 for USD 400 million and separately acquired Goldcast, expanding its portfolio into post-event content automation, with the intent to help organizers convert session content into evergreen assets and boost hybrid capabilities.

- November 2025: Live Nation Entertainment announced an expanded Mastercard partnership to include the Middle East, granting Mastercard exclusive payment-partner status at select concerts along with presale and VIP access benefits for cardholders.

- September 2025: BRAG, a Live Nation Middle East entity, partnered with Expo City Dubai to manage Jubilee Park, Al Forsan Park, and Dubai Millennium Amphitheater with commitments to carbon measurement, zero waste to landfill, renewable power, and reduced single-use plastics.

- April 2025: GRI Club hosted “Empowered by GCC – Global Capital Connectors Series” at Emirates Palace Mandarin Oriental, featuring 126 senior decision-makers from sovereign wealth funds and private wealth organizations focused on real-estate capital flows. The event introduced a closed-door pitch format that facilitated USD 2.1 billion in indicative deals.

GCC Event Management Market Report Scope

Event management entails the strategic application of project management principles to plan, execute, and oversee large-scale events.

The GCC event management industry is segmented by event type and by application. By type, the industry is segmented into meetings, incentives, conventions, exhibitions, and other event types. By application, the industry is segmented into academic, business, political, and other applications. The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

By End-User

| Corporate |

| Individual |

| Public |

By Type

| Music Concert |

| Festivals |

| Sports |

| Exhibitions and Conferences |

| Corporate Events and Seminars |

| Other Types |

By Revenue Sources

| Ticket Sales |

| Sponsorships |

| Other Revenue Sources |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| By End-User | Corporate |

| Individual | |

| Public | |

| By Type | Music Concert |

| Festivals | |

| Sports | |

| Exhibitions and Conferences | |

| Corporate Events and Seminars | |

| Other Types | |

| By Revenue Sources | Ticket Sales |

| Sponsorships | |

| Other Revenue Sources | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman |

Key Questions Answered in the Report

What is the current size and growth outlook for the GCC event management market?

The GCC event management market size reached USD 6.88 billion in 2025 and is projected to reach USD 9.11 billion by 2031 at a 4.78% CAGR for 2026–2031.

Which end-user category is growing fastest within the GCC event management market?

The public segment is projected to expand at a 12.42% CAGR through 2031, supported by sovereign-backed cultural programs and destination festivals.

What revenue streams matter most for organizers in the GCC?

Ticket sales represented 53.22% in 2025, while sponsorships are projected to grow at 11.94% CAGR and are becoming the key margin driver for large-format events.

Which event type leads and which is the fastest growing across the GCC?

Exhibitions and conferences held 43.03% in 2025, while festivals are projected to grow fastest at a 13.78% CAGR to 2031.

What revenue streams matter most for organizers in the GCC?

Ticket sales represented 53.22% in 2025, while sponsorships are projected to grow at 11.94% CAGR and are becoming the key margin driver for large-format events.

Which GCC market leads and which is growing fastest?

Saudi Arabia led with 45.20% in 2025, and Qatar is projected to record the highest growth at a 13.21% CAGR from 2026 to 2031.

What are the biggest operating constraints for event planners across the GCC?

Extreme heat and weather volatility limit outdoor calendars, while skilled talent shortages and localization mandates add cost and delivery risk for organizers.

Page last updated on: