UAE Industrial Waste Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

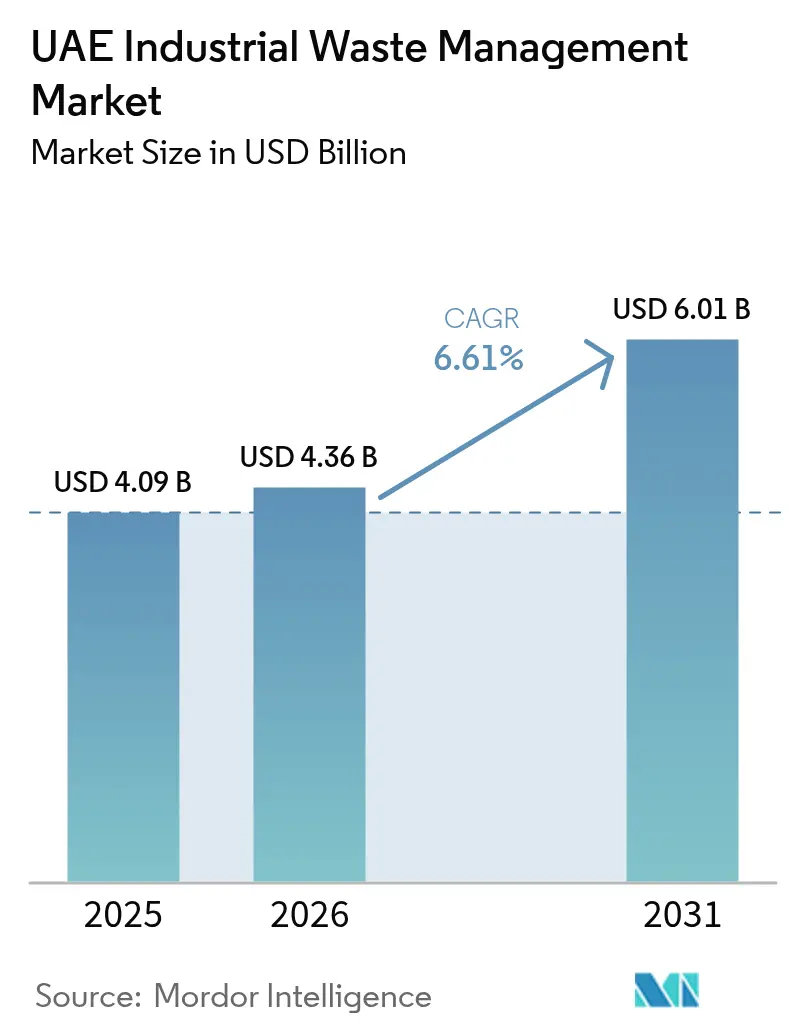

| Base Year Market Size (2025) | USD 4.09 Billion |

| Market Size (2026) | USD 4.36 Billion |

| Market Size (2031) | USD 6.01 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

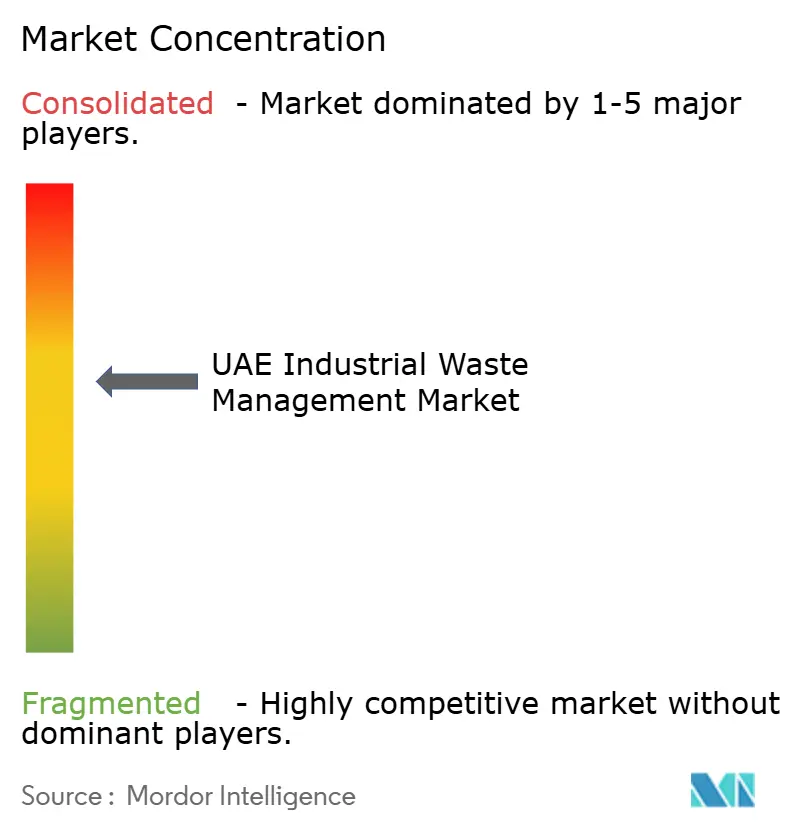

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Industrial Waste Management Market Analysis by Mordor Intelligence

The UAE industrial waste management market size was valued at USD 4.09 billion in 2025 and is estimated to grow from USD 4.36 billion in 2026 to USD 6.01 billion by 2031, at a CAGR of 6.61% during the forecast period (2026-2031). Stricter landfill-diversion targets, escalating disposal fees, and early-stage extended producer responsibility (EPR) programs are pushing generators to favor recycling, energy recovery, and on-site pre-treatment instead of landfilling. Mega waste-to-energy (WtE) plants in Dubai and Abu Dhabi guarantee offtake for mixed residuals, while a January 2026 value-added-tax (VAT) reverse-charge rule formalizes scrap trading and tightens audit trails. Digital tools such as Tahweel’s national recyclables exchange improve price discovery for smaller collectors, and rising hazardous-waste capacity at the Ruwais hub addresses a long-standing treatment deficit. Against this backdrop, vertically integrated players with sorting or thermal assets enjoy an expanding cost advantage over operators relying solely on collection.

Key Report Takeaways

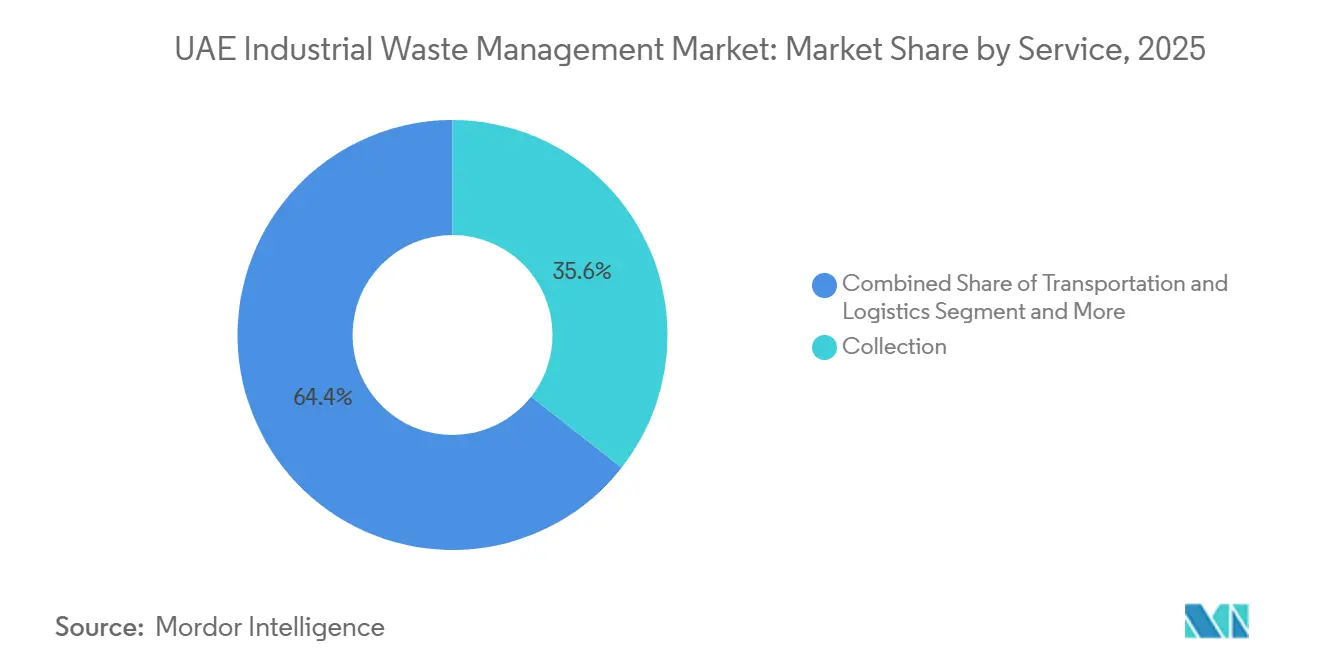

- By service, collection led with a 35.6% revenue share in 2025; recycling and material recovery is forecast to advance at a 7.91% CAGR through 2031.

- By disposal method, landfill captured 54.35% of 2025 volumes, whereas incineration and energy recovery is projected to grow at an 8.51% CAGR to 2031.

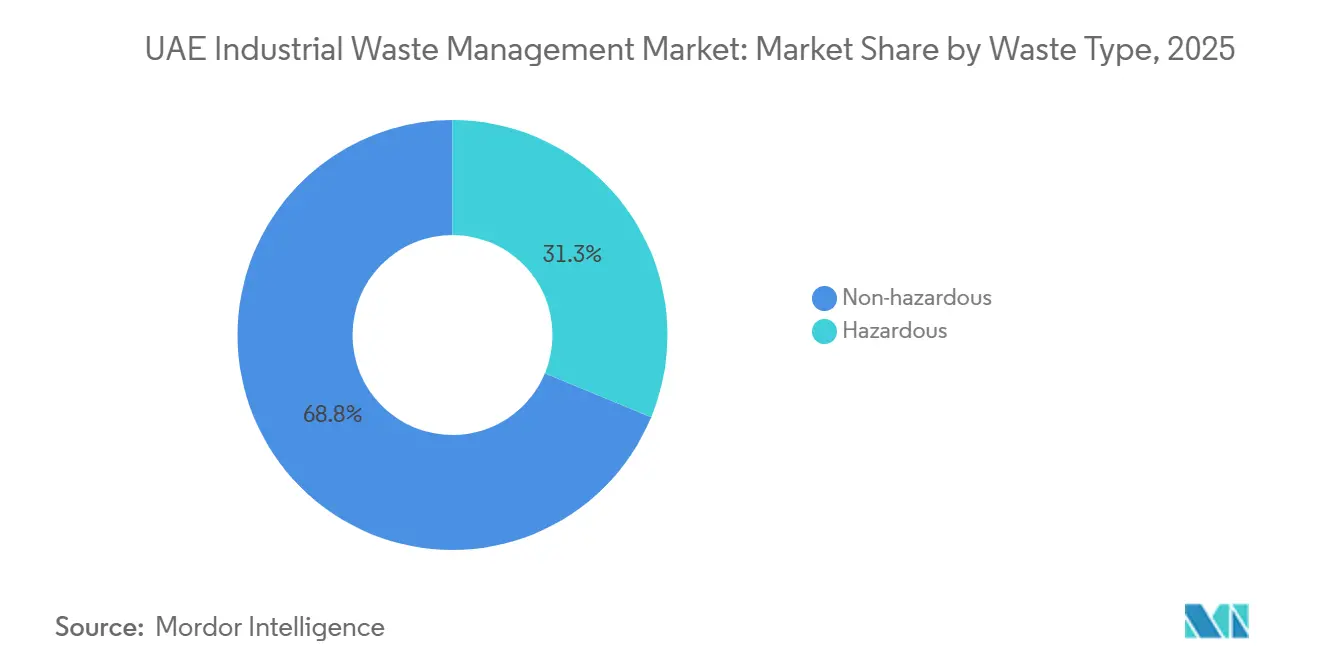

- By waste type, non-hazardous streams accounted for 68.75% of 2025 tonnage, while hazardous-waste treatment is expected to rise at a 7.5% CAGR as the Ruwais hub expands.

- By industry, oil and gas generated 32.5% of 2025 industrial waste; construction materials is the fastest-growing source at a 9.11% CAGR through 2031.

- Bee’ah, Tadweer, and Veolia collectively controlled about 40% of 2025 revenue, underscoring a moderately concentrated competitive field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United arab emirates representing one among them. The global report on industrial waste management market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

UAE Industrial Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide EPR roll-out for packaging, e-waste and batteries (framework slated 2026) | +1.5% | Abu Dhabi and Dubai pilots, national by 2027 | Medium term (2-4 years) |

| Mega WtE assets (Warsan 1.9 Mt 2025; Al-Dhafra 0.9 Mt 2027) secure diversion capacity | +1.3% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Dubai Law No. 18 (2024) enforces permits, GPS-tracked haulage and escalating landfill fees | +1.2% | Dubai, spillover into Sharjah and Ajman | Short term (≤ 2 years) |

| VAT reverse-charge on scrap metal (Jan 2026) formalizes trade | +0.8% | National, hubs in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Ruwais hazardous-waste hub scales to 165 kt/yr | +0.7% | Abu Dhabi (Ruwais) | Medium term (2-4 years) |

| Tahweel digital marketplace unlocks liquidity for recyclables | +0.6% | National, early uptake in Abu Dhabi and Dubai | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nationwide EPR Roll-Out for Packaging, E-Waste and Batteries

Pilot EPR schemes launched in July 2025 require brand owners to fund post-consumer collection, with diversion quotas rising from 30% in 2026 to 60% by 2030.[1]Ministry of Climate Change and Environment, “EPR Framework Guidelines,” moccae.gov.ae Early signatories such as Union Paper Mills and Tetra Pak installed a USD 0.68 million carton-recycling line, while Enviroserve and Imdaad are deploying smart e-waste bins across free-zone workplaces. Importantly, an export fee of USD 109 per tonne on plastics and USD 82 per tonne on aluminum keeps most EPR-collected streams onshore, bolstering feedstock security for domestic re-processors.

Mega WtE Assets Online Secure Diversion Capacity

The Warsan plant processed 1.9 million tonnes in 2025 and supplied 200–220 MW to Dubai’s grid, displacing roughly 400,000 tCO₂ annually. Abu Dhabi’s 0.9-million-tonne Al-Dhafra facility will add 80 MW when it starts in 2027, helping the emirate reach an 80% diversion rate before 2030. Guaranteed offtake under long-term power-purchase agreements (PPAs) improves tipping-fee economics for collectors and underpins lender confidence for future phases.

Dubai Law No. 18 of 2024 Enforces Permits, GPS-Tracked Haulage and Rising Fees

Mandatory GPS on every waste truck and steep annual fee increases have erased price advantages for unregistered haulers, channeling more tonnage toward licensed operators.[2]Government of Dubai, “Law No. 18 of 2024,” dubai.gov.ae Tipping charges already stand at USD 27.23 per tonne for mixed waste and up to USD 136.1 per tonne for hazardous loads, while sorted recyclables pay only USD 8.17. Heavy fines of up to USD 5446 per offence curb illegal dumping, and Dubai Municipality intends to close all landfills by 2027. The rule, therefore, accelerates source-segregation investment and rewards firms with in-house treatment or WtE capacity.

VAT Reverse-Charge on Scrap Metal Formalizes Trade

Effective 14 January 2026, buyers, not suppliers, remit VAT on ferrous scrap, closing a loophole where unregistered traders pocketed the tax.[3]Federal Tax Authority, “Cabinet Decision 153 of 2025,” tax.gov.ae The policy is expected to formalize roughly 30% of flows that previously escaped documentation, enriching audit trails for mills like Emirates Steel and ensuring reliable local supply amid a USD 109 per-tonne export levy on scrap.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patchy emirate-level fee structure encourages cross-hauling | -0.5% | National, acute between Sharjah and Abu Dhabi | Short term (≤ 2 years) |

| Domestic lithium-ion and specialist e-waste capacity lags demand until 2027 | -0.4% | National, assets in Dubai and Abu Dhabi | Medium term (2-4 years) |

| High-chlorine RDF curbs cement-kiln co-processing | -0.3% | Umm Al Quwain plant, national cement sector | Long term (≥ 4 years) |

| Scrap-export duty evasion via trans-shipment erodes feedstock | -0.3% | National, routes through Bahrain and Jebel Ali | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patchy Emirate-Level Fee Structure Incentivizes Cross-Hauling

Landfill charges range from USD 13.61 per tonne in Sharjah to USD 61.27 per tonne in Abu Dhabi, creating a USD 47.65 price gap that outweighs a typical USD 8.17 transport cost.[4]Dubai Municipality, “Landfill Fee Schedule,” dubai.gov.ae Haulers divert waste to cheaper emirates, undermining local diversion targets and squeezing compliant operators. Although Ajman levied USD 5446 fines on violators in 2024, enforcement remains inconsistent, and the absence of a federal floor fee prolongs arbitrage opportunities.

Domestic Lithium-ion and Specialist E-Waste Capacity Lags Demand

The UAE generated 5,000–7,000 tonnes of lithium-ion batteries in 2025 but had only 1,500 tonnes of processing capacity, forcing exporters to absorb USD 200–USD 300 per-tonne freight costs to Europe or South Korea. KEZAD’s 5,000-tonne line will not start before Q2 2027, prolonging a two-year supply bottleneck, while Dubatt’s feasibility study for an additional 5,000 tonnes remains without a firm commissioning date.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Recycling Gains Share as EPR Shifts Liability Upstream

Collection commanded 35.6% of 2025 revenue, reflecting route density and the capital tied up in GPS-equipped fleets central to Dubai Law 18 compliance. However, the UAE industrial waste management market size for recycling and material recovery is forecast to rise at a 7.91% CAGR, outpacing every other service line. Digital tools such as Tahweel allow small collectors to auction plastics and metals directly, narrowing spreads and lifting margins. Union Paper Mills and Tetra Pak’s carton line shows how brand owners lock in recycled feedstock to meet EPR quotas, while Tadweer’s UpCycle subsidiary funnels sorted streams to Sharjah’s expanding WtE plant. These moves deepen integration and dilute the share of pure collection players, gradually tilting contract renewals toward firms with sorting or conversion assets.

Growth momentum in transportation and logistics hinges on compliance technology: every truck must transmit live coordinates, and permit renewals link to audit histories, raising barriers for informal haulers. Treatment and disposal remain the second-largest service but face a structural decline once Dubai closes landfills in 2027. In response, Bee’ah and Averda are re-deploying capital from landfill cells into transfer and WtE infrastructure, a hedge against tightening gate-fees and diversion mandates. Overall, service dynamics illustrate how EPR and landfill economics are rewriting revenue pools inside the UAE industrial waste management market.

By Disposal Method: Incineration & Energy Recovery Accelerates

Landfill absorbed 54.35% of 2025 tonnage, yet incineration and energy recovery is projected to expand at an 8.51% CAGR through 2031, the sharpest rate among all methods. Warsan’s 1.9-million-tonne plant alone dwarfs historic throughput, while Al-Dhafra’s 0.9-million-tonne design will redirect mixed flows from Abu Dhabi’s high-fee landfills. Because WtE plants hold long-run PPAs, collectors enjoy predictable tip charges and avoid the volatility tied to commodity recycling markets, lifting bankability for fleet upgrades. Cement co-processing processes more than 110,000 tonnes annually, but chlorine thresholds cap upside, channeling higher-chlorine RDF to WtE outlets instead.

Recycling maintains a solid foothold, yet its share is sensitive to commodity cycles and relies on regulatory push from EPR. Dubai Municipality’s 2027 landfill-closure plan will straight-jacket disposal volumes, making integrated operators with WtE assets central to the UAE industrial waste management market share race. In effect, thermal solutions complement, not cannibalize, high-value recycling by handling the residue that cannot meet strict material purity.

By Waste Type: Hazardous Streams Show the Fastest Climb

Non-hazardous waste represented 68.75% of 2025 volumes, but hazardous waste is forecast to register a 7.5% CAGR as the Ruwais hub lifts capacity to 165,000 tpa. The UAE industrial waste management market size tied to hazardous treatment enjoys premium gate-fees and long contracts with refiners and chemical majors. ADNOC Gas already diverts nearly half its hazardous load through approved recyclers to avoid disposal charges as high as USD 272 per tonne for flammable material. New BeAAT expansions add further heat to competition, suggesting pricing power may ease once incremental capacity comes onstream.

For non-hazardous streams, digital auctioning shrinks brokerage spreads, and Ministerial Decision 21/2019 permits up to 40% recycled aggregate in new builds, supporting downstream outlets for construction debris. Together, these countervailing trends keep overall tonnage balanced, but value pools migrate toward specialized hazardous-waste handling in the medium term.

By Industry: Construction Materials Becomes the Fastest Riser

Oil and gas dominated with 32.5% of 2025 waste tonnage, anchored by drilling mud, produced-water solids, and catalyst fines. Yet construction materials is set to be the quickest climber at a 9.11% CAGR as megaprojects like Abu Dhabi’s Zayed City and Dubai’s Expo City generate mountains of concrete and rebar. Under Ministerial Decision 21/2019, public works must include recycled aggregates, creating pull-through demand for Al Dhafra Recycling Industries’ 7,000-tonne-per-shift line. Meanwhile, the EPR model forces electronics and battery OEMs to shoulder end-of-life costs, nudging them toward long-term offtake agreements with processors like Enviroserve.

Steelmakers also capture upside: the VAT reverse-charge and a USD 109 per-tonne export duty redirect scrap flows inward, giving Emirates Steel a buffer against imported billet costs. In aggregate, sectoral demand patterns suggest construction will narrow the tonnage gap with oil and gas before the decade ends, underpinning diversified feedstock streams for recyclers and WtE operators inside the UAE industrial waste management market.

Geography Analysis

Abu Dhabi and Dubai collectively generated close to 70% of 2025 industrial waste, a concentration driven by refining, petrochemical, and large-scale construction activity. Abu Dhabi’s USD 61.27 per-tonne landfill fee, the nation’s highest, funnels waste toward the Ruwais hazardous-waste hub and will soon feed the 0.9-million-tonne Al-Dhafra WtE plant that comes online in 2027. Dubai, by contrast, processed 1.9 million tonnes through the Warsan facility in 2025 and applies escalating landfill charges that already stand at USD 27.23 per tonne for mixed loads. Mandatory GPS on every truck tightens enforcement, and a policy to shutter all landfills by 2027 forces generators to pre-sort or pay premium incineration fees.

Sharjah is steering toward zero-waste through a Phase 2 WtE expansion that doubles capacity to 60 MW, yet its landfill fee remains just USD 13.61, encouraging cross-border hauling from higher-cost emirates. Ajman’s recent USD 5446 fines show sporadic crackdowns, but until a federal floor emerges, price arbitrage will persist. Northern emirates such as Fujairah and Ras Al Khaimah contribute smaller volumes but benefit from proximity to Jebel Ali Port and scheduled Etihad Rail links, lowering export costs for recovered metals.

Khalifa Economic Zones Abu Dhabi (KEZAD) is fast becoming a specialist recycling node: a 5,000-tonne lithium-ion facility, a Bee’ah waste-management JV, and integrated smart-bin pilots align with industrial tenants seeking ESG compliance. In Dubai Industrial Park, Enviroserve’s 100,000-tonne e-scrap campus anchors refrigerant reclaim and circuit-board recovery. These clusters underscore how infrastructure density, fee structures, and regulatory stringency decide where value accrues within the UAE industrial waste management market.

Mordor Intelligence provides coverage of the industrial waste management market across other key regional markets, including North America, Europe, and Middle East, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Competition revolves around integrated platforms that combine collection with high-barrier treatment or energy assets. Bee’ah, Tadweer, and Veolia jointly hold about 40% of revenue, and each invests in vertical slices: Bee’ah co-owns the Warsan WtE plant and spearheads Tahweel’s digital exchange; Tadweer spun off specialist arms such as UpCycle to extract value from sorting and conversion; Veolia anchors hazardous treatment at Ruwais. Their strategic moves signal a pivot from tonnage capture to margin capture through technology and asset control.

Niche players exploit white-space in underserved streams. Enviroserve holds the only refrigerant-reclaim license and a 100,000-tonne e-scrap line, giving it leverage as EPR rules bite. Geocycle processes tire-derived fuel and low-chlorine RDF for cement kilns, while Al Dhafra Recycling Industries carves a position in recycled aggregates for government projects. Averda’s 2025 purchase of Zenath Recycling expands its Dubai fleet by 38 trucks, showing how mid-tier haulers scale rapidly through bolt-on acquisitions rather than greenfield builds.

Digitalization is a decisive lever. Tahweel’s timed auctions compress margins but increase transparency, encouraging second-tier collectors to join formal channels. ISO 14001:2015 certification, now standard among top players, raises compliance costs and shuts out informal rivals, nudging the sector toward moderate consolidation. Under a combined 40% market share for the top three, the UAE industrial waste management market earns a concentration score of 6, reflecting a cluster of sizable incumbents with still-meaningful room for specialist challengers.

UAE Industrial Waste Management Industry Leaders

Bee’ah (Sharjah Environmental)

Tadweer (Abu Dhabi Waste Management Co.)

Veolia Middle East

Averda

Dulsco Environment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bee’ah, the Ministry of Energy and Infrastructure, and LOHUM launched a JV to recycle 1,500 tonnes of EV batteries in 2026, tripling capacity by year three.

- January 2026: KEZAD and Bee’ah formed a 51–49 JV for integrated waste services across KEZAD zones.

- January 2026: KEZAD and Witthal agreed to build a 5,000-ton lithium-ion line for commissioning in Q2 2027.

- January 2026: Emirates Global Aluminum began output at its 185,000-ton aluminum-recycling plant.

UAE Industrial Waste Management Market Report Scope

The market has been studied based on the hazardous and non-hazardous wastes generated by different industries. The report highlights the operational specialization of the key waste management companies in the country, to understand the business strategies and the upcoming technologies, which are used for the effective treatment of the numerous wastes generated by various industries.

| Collection |

| Transportation & Logistics |

| Treatment & Disposal |

| Recycling & Material Recovery |

| Landfill |

| Recycling |

| Incineration & Energy Recovery (RDF, SRF, WtE) |

| Non-hazardous |

| Hazardous |

| Chemicals & Petrochemicals |

| Oil & Gas |

| Power Generation |

| Metal & Mining |

| Food & Beverage Processing |

| Pharmaceuticals |

| Electrical & Electronics |

| Construction Materials |

| By Service | Collection |

| Transportation & Logistics | |

| Treatment & Disposal | |

| Recycling & Material Recovery | |

| By Disposal Method | Landfill |

| Recycling | |

| Incineration & Energy Recovery (RDF, SRF, WtE) | |

| By Waste Type | Non-hazardous |

| Hazardous | |

| By Industry | Chemicals & Petrochemicals |

| Oil & Gas | |

| Power Generation | |

| Metal & Mining | |

| Food & Beverage Processing | |

| Pharmaceuticals | |

| Electrical & Electronics | |

| Construction Materials |

Key Questions Answered in the Report

How large is the UAE industrial waste management market in 2026?

It is valued at USD 4.36 billion and is projected to reach USD 6.01 billion by 2031.

Which service segment leads revenue today?

Collection services hold 33.62% of 2025 revenue, but recycling & material recovery is the fastest-growing at an 8.07% CAGR.

What is driving investment in waste-to-energy plants?

Dual revenue from disposal fees and electricity sales, backed by the 75% landfill-diversion mandate, is accelerating plant construction.

Why is hazardous-waste demand rising?

Federal Decree-Law No. 11 of 2024 forces industries to track and reduce emissions, prompting outsourcing to licensed hazardous-waste specialists.

Which emirate shows the most advanced waste infrastructure?

Sharjah leads with 90% diversion and a fully operational 27 MW WtE plant, serving as a regional benchmark.

Are there growth opportunities in e-waste recycling?

Yes; the UAE produces 162 kt of e-waste annually but lacks large-scale battery and electronics recovery plants, creating a significant market gap.

Page last updated on: