Waste Disposal Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.7 Billion |

| Market Size (2031) | USD 6.08 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

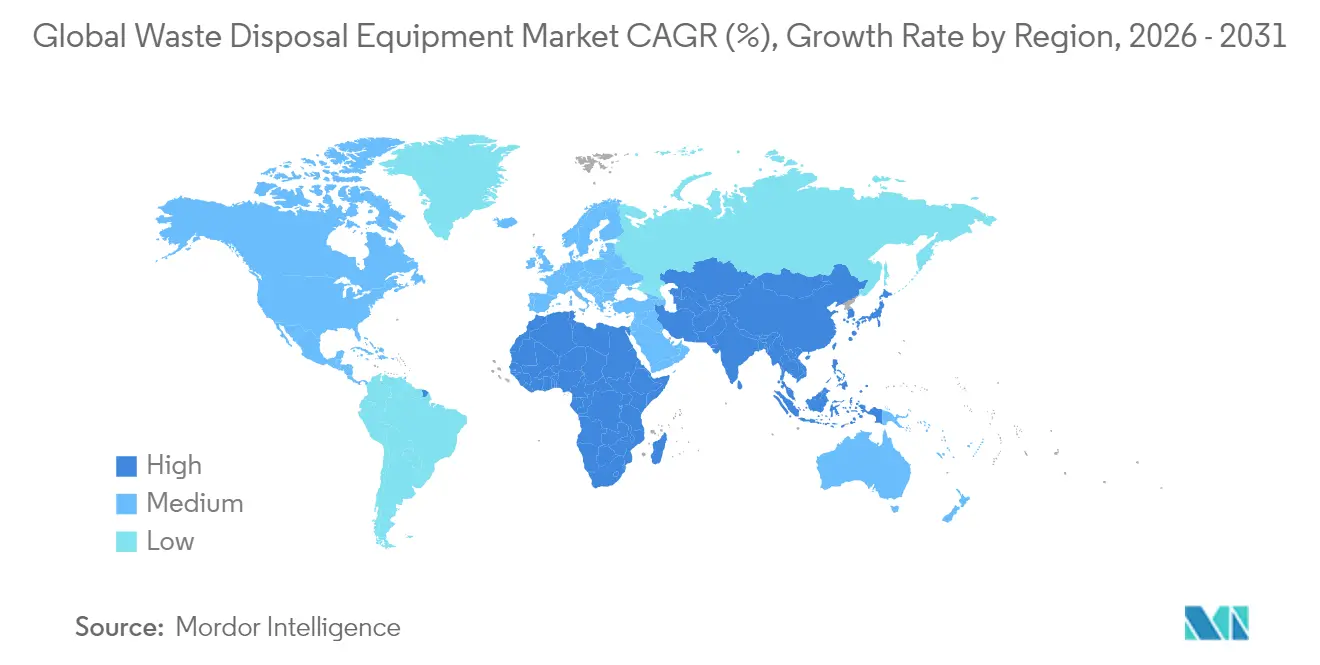

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Waste Disposal Equipment Market Analysis by Mordor Intelligence

Global Waste Disposal Equipment Market size in 2026 is estimated at USD 4.7 billion, growing from 2025 value of USD 4.46 billion with 2031 projections showing USD 6.08 billion, growing at 5.30% CAGR over 2026-2031. Demand resilience stems from rising waste volumes, stricter environmental rules, and continuous upgrades in collection, sorting, and processing technology. The Asia-Pacific region, holding the largest 47% revenue share, benefits from rapid urban growth and industrial expansion, while the Middle East and Africa post the fastest 7.2% CAGR as infrastructure spending and public environmental awareness accelerate equipment purchases. Waste recycling equipment currently leads with a 36% share of the Global waste disposal equipment market, although AI-enabled sorting systems are reshaping competitive dynamics. Manufacturers are adding electrified drivetrains and smart controls across product lines, and municipal buyers, now 45.1% of all end users, are prioritizing systems that facilitate source segregation and circular economy goals.

Key Report Takeaways

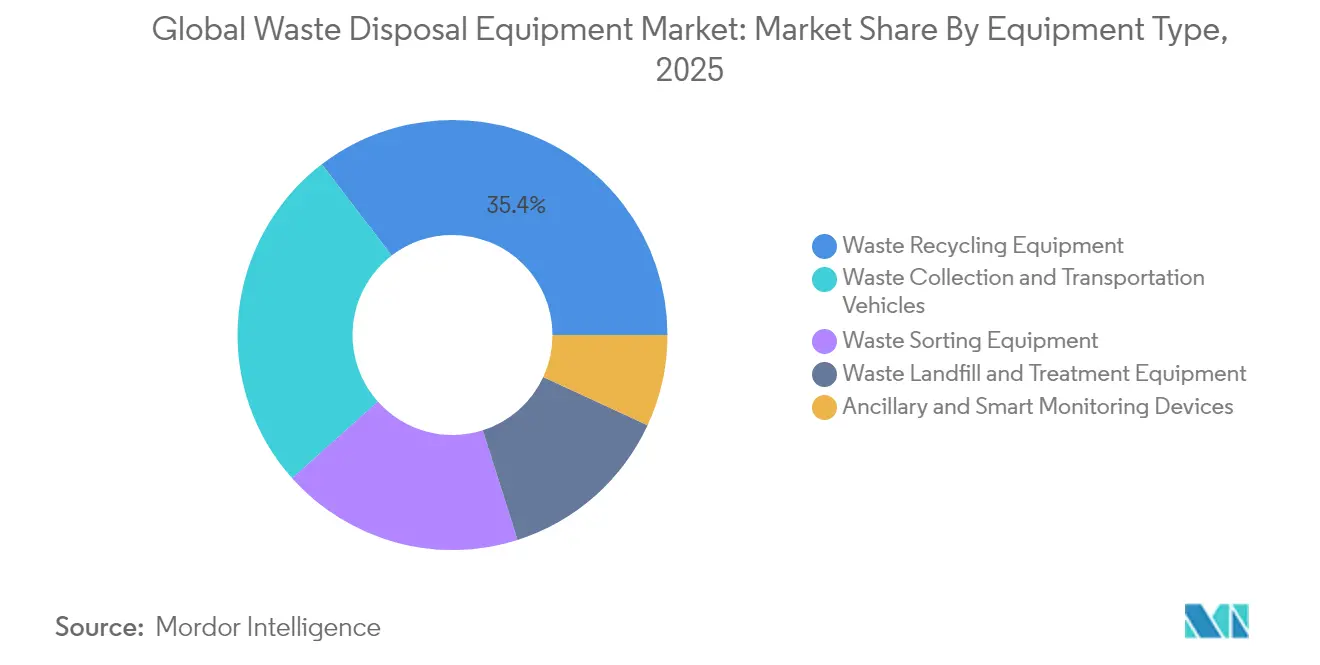

- By equipment type, waste recycling machinery led with 35.40% Global waste disposal equipment market share in 2025; AI-powered sorting solutions are projected to rise at a 11.9% CAGR through 2031.

- By waste type, non-hazardous streams accounted for 69.80% of the Global waste disposal equipment market size in 2025, while hazardous-waste systems are advancing at an 7.7% CAGR to 2031.

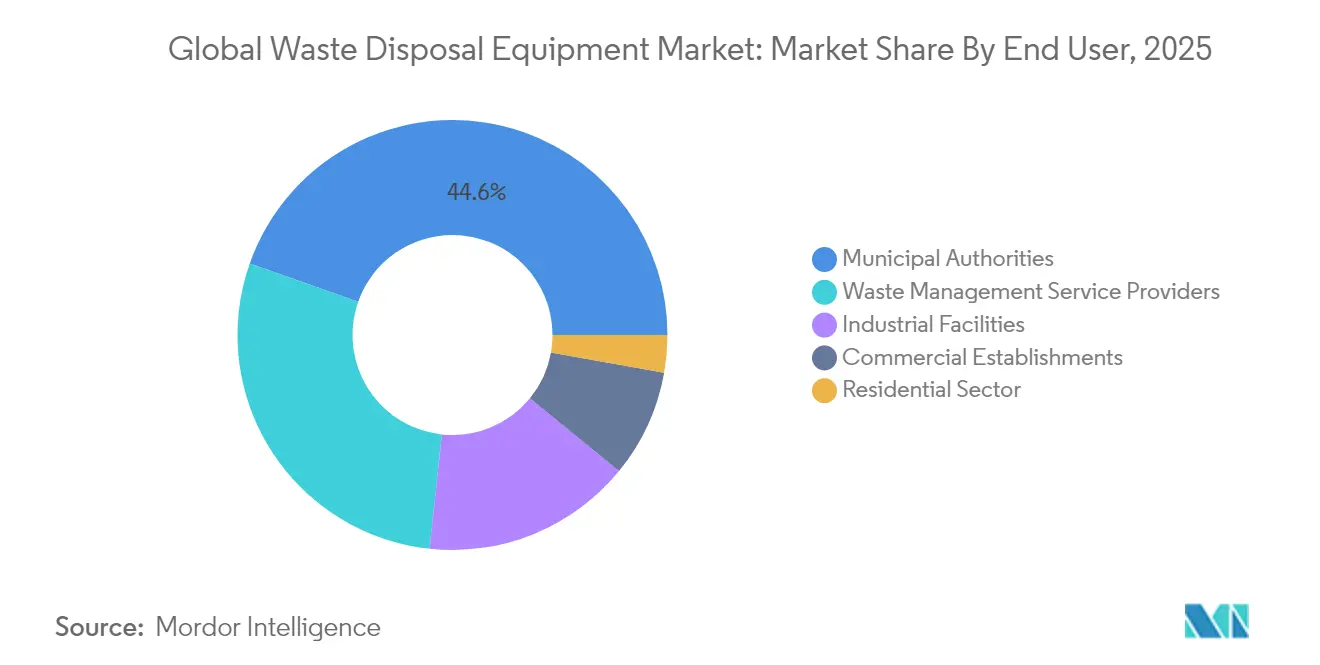

- By end user, municipal authorities commanded 44.60% of the 2025 revenue pool, yet industrial facilities are registering the quickest 6.05% CAGR over the forecast period.

- By mode of operation, stationary units held 77.60% share in 2025, while mobile equipment will grow 8.25% annually through 2031.

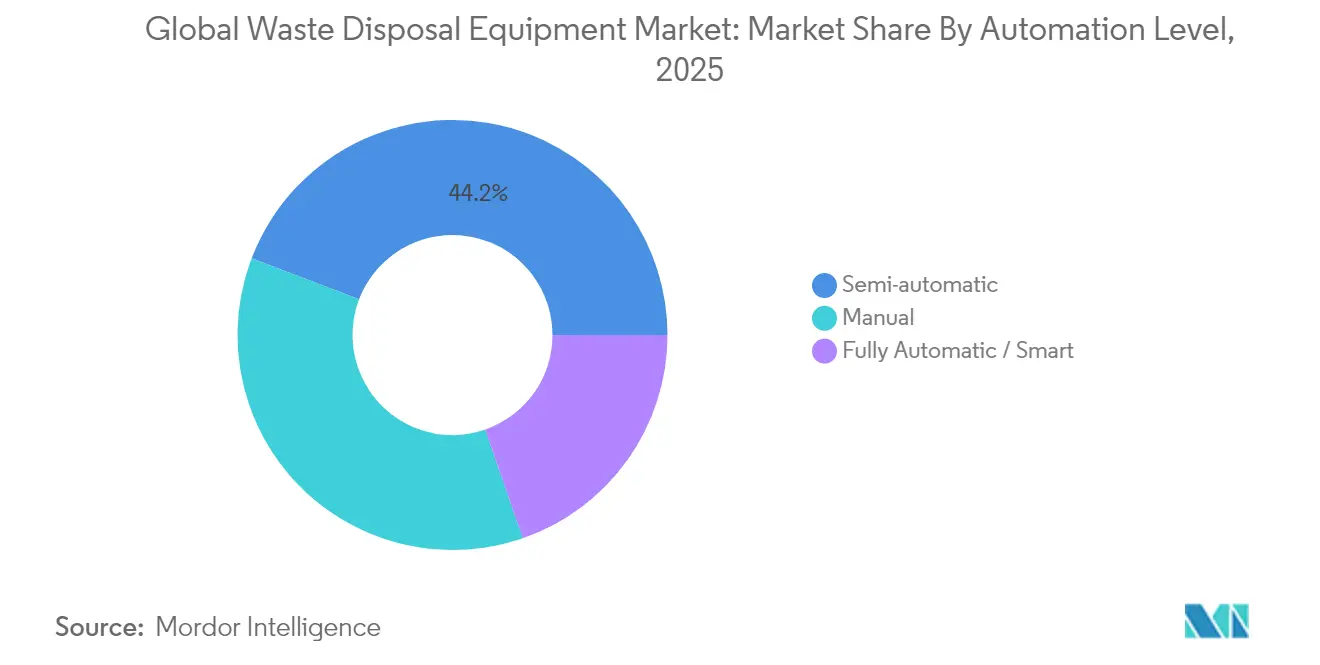

- By automation level, semi-automatic led the market with 44.20% share in 2025, while fully automatic / smart equipment is projected to grow at a 9.45% CAGR through 2031.

- By power source, diesel-powered units dominated with 66.90% share in 2025, whereas electric are expected to expand the fastest, registering a 9.8% CAGR over 2026-2031.

- By geography, Asia-Pacific controlled 46.50% of 2025 revenue, and Middle East Africa is forecast to expand 6.95% annually to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Waste Disposal Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated adoption of AI-enabled optical sorters | +1.2% | Europe, North America, early uptake in Asia-Pacific | Medium term (2-4 years) |

| Post-ban e-waste recycling stimulus | +1.0% | Asia-Pacific, global spillover | Short term (≤ 2 years) |

| Escalating landfill-tax regimes | +0.9% | Nordic region, wider Europe | Short term (≤ 2 years) |

| Transition to electric refuse-collection fleets | +0.8% | North America, Europe | Medium term (2-4 years) |

| Mandatory source-segregation laws | +0.7% | South-Asian metros | Medium term (2-4 years) |

| EPR funds driving baler upgrades | +0.6% | Latin America, later Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of AI-enabled Optical Sorters

AI-guided optical sorters now reach 99% material-recognition accuracy, unlocking higher recovery rates for metals and wood and trimming operating budgets for large material-recovery facilities. A seven-year cost comparison shows an automated plant all-in expense of USD 14.0 million, versus USD 23.6 million for a similarly sized manual operation, translating to a 40.6% life-cycle saving.[1]Clean the Sky "AI Waste-Sorting Machines - Clean the Sky." cleanthesky.comThese financial gains, coupled with labor-shortage relief and tighter purity mandates, are propelling deployment across Europe’s high-labor-cost markets and spilling into North America and advanced Asian hubs.

Post-ban E-waste Recycling Stimulus

Regional bans on electronic waste imports and the domestic generation of 2.9 million tons of obsolete devices have galvanized Asia-Pacific governments to expand local processing. The Global e-Waste Monitor notes USD 62 billion in recoverable resources locked in unprocessed scrap.[2]UNITAR "Global e-Waste Monitor 2024: Electronic Waste Rising Five Times Faster Documented e-Waste Recycling." unitar.org Investment is flowing into shredders, depollution lines, and robotic dismantlers capable of safely extracting lithium batteries, encouraging faster uptake of specialized equipment across the region.

Transition to Electric Refuse Collection Fleets

Electric refuse trucks achieve 40-62% lower running costs than diesel units, as consistent stop-start routes exploit regenerative braking. Early fleets from leading OEMs demonstrate weekly route parity with diesel trucks while cutting maintenance through reduced brake wear. Municipal carbon-reduction targets and tighter urban air-quality standards hasten the procurement of battery-electric or hydraulic-hybrid drivetrains in cities from California to Scandinavia.

Mandatory Source Segregation Laws

Major South Asian metro areas are rolling out strict household separation rules. Dual-compartment collection vehicles and modular transfer stations capable of handling presorted streams lower downstream treatment expenses by up to 20%. This legislative push is expanding demand for compatible collection bodies, onboard bin sensors, and streamlined conveyor layouts that keep segregated fractions intact.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long payback for robotic pickers | -0.5% | Global, small & midsize MRFs | Short term (≤ 2 years) |

| Semiconductor shortages | -0.7% | Global, highest in emerging markets | Short term (≤ 2 years) |

| Fragmented municipal procurement | -0.3% | Africa, parts of Asia & Latin America | Long term (≥ 4 years) |

| Costly EU battery-safety certification | -0.4% | Europe, global spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long Payback for Robotic Pickers

Smaller facilities struggle to justify multi-robot systems where throughput is modest and capital budgets are tight, prolonging break-even horizons beyond five years. Financing programs and equipment-as-a-service models are gradually easing this barrier, but uptake remains slow in developing regions.

Semiconductor Shortages

Persistent chip supply disruptions constrain deliveries of advanced sensors, drives, and control boards. Lead times have doubled for optical sorters and vehicle telematics units, complicating project schedules and inflating costs, especially in regions with limited inventory buffers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Recycling Machinery Maintains Lead while AI Sorting Surges

Waste recycling equipment held a 35.40% revenue share of the Global waste disposal equipment market in 2025. Manufacturers are integrating near-infrared sensors, machine learning, and robotics to raise purity and reduce labor costs. AI-driven systems are projected to post a 11.9% CAGR, outpacing conventional screen-and-magnet lines as facilities chase higher commodity yields and automate low-value tasks. Traditional brands are retrofitting optical detection kits into existing sorters to protect installed bases, while specialized startups push modular, trailer-mounted units for smaller municipalities.

The electric shift in collection and transfer vehicles mirrors broader decarbonization trends; battery packs, electric PTOs, and regenerative braking are now standard in new refuse-truck tenders. Ancillary smart devices, fill-level sensors, route-optimization software, and compactor-pressure monitors extend digital oversight beyond the tipping floor. Early adopters report preventive-maintenance savings and clearer material-flow data that underpin circular economy targets inside the Global waste disposal equipment market.

By Waste Type: Hazardous Streams Drive Specialized Technology Uptake

Non-hazardous streams generated 69.80% of 2025 revenue, yet hazardous-waste solutions are advancing fastest at 7.7% CAGR through 2031. Regulatory focus on medical, chemical, and electronic residues boosts demand for sealed shredders, negative-pressure feeding systems, and thermal destruction units. The Global waste disposal equipment market size for hazardous-waste treatment is expected to expand as lithium-battery recovery plants and solvent-recapture lines come online.

E-waste, with only 22.3% formal recycling, underlines a widening opportunity. Robotic depollution stations now remove batteries and capacitors at 98% purity, alleviating safety risks and retrieving high-value metals. Construction-and-demolition debris also prompts investments in mobile crushers and automated density-based separators, which reclaim concrete and metals for reuse.

By End User: Industry Investments Accelerate Automation

Municipal entities represented 44.60% of 2025 revenue owing to statutory waste-collection duties. However, industrial facilities are rapidly upgrading on-site processing to cut disposal fees and recover raw materials, delivering a 6.05% CAGR through 2031. Manufacturers in food, electronics, and chemicals are installing compactors, balers, and solvent-recovery units tailored to their specific waste profiles.

Waste-management service companies continue to broaden fleets with smart collection bodies and region-specific treatment hubs. Commercial premises—retail chains, office parks, and hotels—opt for vertical balers and small-foot-print compactors to curb hauling costs. Community-level drop-off points and decentralized composting illustrate how residential stakeholders now participate in source-segregated streams that feed into the wider Global waste disposal equipment market.

By Mode of Operation: Mobile Platforms Strengthen Logistical Flexibility

Stationary systems control 77.60% of revenue, reflecting entrenched capital assets at transfer stations, MRFs, and landfill sites. Yet mobile equipment registers an 8.25% CAGR, favored for disaster cleanup, rural deployments, and temporary project sites. Trailer-mounted sorters, skid-mounted compactors, and containerized balers reduce upfront civil works and enable redeployment as waste flows shift.

For waste-oil recovery, portable suction rigs offer fleet-maintenance shops an easy path to compliance, minimizing downtime compared with fixed pits. Real-time sensor suites installed on both stationary and mobile units feed asset-performance dashboards, steering predictive-maintenance schedules and fuel-saving initiatives across the Global waste disposal equipment market.

By Automation Level: Smart Systems Enhance Efficiency

The transition from manual to semi-automatic and fully autonomous systems gathers pace. Comparative studies show autonomous configurations trimming fuel use to 5 L/day and cutting overflows, while boosting carbon-emission reductions to 67%. Facilities unable to finance full automation embrace semi-automatic retrofits—optical sensors added to existing conveyors or hydraulically actuated gates that improve throughput for moderate cost.

Fully automated e-waste lines record 83-fold productivity versus hand-dismantling, with material-purity rates reaching at least 98%. These performance gains are compelling for processors handling hazardous fractions, where labor-safety benefits reinforce the spending case.

By Power Source: Battery and Hybrid Drivetrains Gain Ground

Diesel remains the dominant propulsion across heavy trucks and self-powered compactors, yet battery-electric and hydraulic-hybrid models are winning new tenders. Field data reveal refuse trucks achieving fuel-equivalent 3.2 mpg, 2,500 gal annual fuel savings, and up to 100% CO₂ reduction when electricity is derived from renewables. Hydraulic-hybrid units provide an interim step, posting 25% fuel-economy gains by storing braking energy in accumulators.

Lifecycle assessments caution that electric benefits vary by grid mix, prompting fleet managers to match technology choices with local power profiles. Smart-grid integrations and depot-level energy-storage systems are emerging to buffer peak-charging loads and lock in renewable electricity for vehicle charging.

Geography Analysis

Asia-Pacific held 46.50% of the Global waste disposal equipment market revenue in 2025. China and India anchor this leadership as urban populations climb and industrial activity intensifies, fostering investments in MRF networks, source-segregated collection, and e-waste dismantling. National subsidies and technology partnerships drive AI-enabled sorters and lithium-battery recovery lines, enlarging the regional Global waste disposal equipment market size at above-average speed.

The Middle East and Africa represent the most dynamic growth trajectory at 6.95% CAGR through 2031. The continent generated 125 million tons of municipal solid waste in 2024 and faces a projected 244 million tons load next year. Recycling lags at 4%, yet an 80-90% recyclable content signals latent demand. East African economies endorsed a ten-point action plan in 2025 to boost e-waste infrastructure, encouraging capital inflows and technology transfer that widen African participation in the Global waste disposal equipment market.

Europe maintains a robust stance thanks to stringent directives on landfill diversion, producer responsibility, and carbon neutrality. Escalating landfill taxes and circular-economy policy packages fund compactor, baler, and depot refurbishment programs. Regions within Scandinavia lead adoption of high-density presses and electric refuse trucks, setting performance benchmarks that ripple across the continent.

North America continues steady equipment renewal, guided by a C+ infrastructure grade that highlights deferred asset replacement. Federal zero-emission vehicle targets and expanding extended-producer-responsibility statutes sustain investment in electrified fleets and smart MRF upgrades. The Middle East, led by GCC nations, channels oil-revenues into waste-to-energy plants, automated sorting, and advanced composting, adding a noteworthy niche within the Global waste disposal equipment market.

Competitive Landscape

Competition is moderate, with diversified conglomerates and regional specialists sharing space across equipment niches. TOMRA Systems retains a lead in sensor-based sorting through continuous algorithm refinement and multi-spectral hardware offerings. In collection vehicles, Volvo CE and Mack Trucks rolled out production-ready electric platforms that support municipal decarbonization agendas.

Strategic mergers deepen product breadth; established players acquire AI-vision startups to shortcut development cycles. For example, firms targeting the recycling segment enhanced portfolios by integrating robotic end-of-arm tooling for lightweight packaging, safeguarding their 36% foothold within the Global waste disposal equipment market.

Startups introduce mobile and modular concepts that undercut civil works costs and bring advanced sorting to underserved areas. Early pilots show ton-per-hour output from trailer-based AI separators, encouraging municipal managers to test pay-by-ton service models. In response, incumbents adopt subscription pricing, remote-diagnostics platforms, and factory-trained service programs to defend share.

R&D budgets tilt toward electrification, autonomous operations, and predictive analytics. Component suppliers collaborate on next-generation battery packs and high-voltage safety systems suited to refuse-truck duty cycles. This innovation race nudges the Global waste disposal equipment market toward higher technological entry barriers, gradually consolidating share among players able to finance continuous upgrades.

Waste Disposal Equipment Industry Leaders

-

Wastequip

-

CP Manufacturing Inc.

-

Dover Corporation

-

Morita Holdings Corporation

-

JCB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Volvo CE and Mack Trucks delivered a fleet of battery-electric collection vehicles to Coastal Waste & Recycling, demonstrating full-shift operational parity with diesel models.

- March 2025: The 7th EACO E-Waste Conference adopted a regional plan to improve formal recycling across East Africa.

- February 2025: Metro Waste Authority published its 2024-2025 strategy prioritizing hazardous-waste acceptance and higher household participation in recycling.

- January 2025: Glacier deployed AI-enabled sorting robots in Seattle, lifting recyclable-material capture rates in a municipal facility.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the waste disposal equipment market as all factory-built machines, compactors, balers, shredders, crushers, incinerators, and smart conveying or sorting units, whose primary role is to collect, reduce, transport, treat, or thermally destroy solid municipal, commercial, and industrial waste streams before final discharge or resource recovery.

Scope Exclusions: Stand-alone services, consumables, rental fleets, and aftermarket spare parts are excluded.

Segmentation Overview

-

By Equipment Type

-

Waste Sorting Equipment

- Mechanical Sorting Systems

- Optical / AI-based Sorting Systems

- Robotic Picking Systems

-

Waste Recycling Equipment

- Shredders

- Balers & Compactors

- Crushers & Pulverizers

- Conveying & Screening Systems

-

Waste Collection & Transportation Vehicles

- Refuse Collection Trucks

- Hook-lift & Skip Loaders

- Automated Vacuum Collection Systems

-

Waste Landfill & Treatment Equipment

- Landfill Compactors & Dozers

- Incinerators & Thermal Treatment Units

- Composting & Anaerobic Digestion Units

-

Ancillary & Smart Monitoring Devices

- Smart Bins & Fill-level Sensors

- Software & Digital Platforms

-

Waste Sorting Equipment

-

By Waste Type

- Municipal Solid Waste

- Industrial Waste (Non-Hazardous)

- Hazardous Waste

- Medical & Bio-hazardous Waste

- Electronic Waste (E-waste)

- Construction & Demolition Debris

-

By End-user

- Municipal Authorities

- Waste Management Service Providers

- Industrial Facilities

- Commercial Establishments

- Residential Sector

-

By Mode of Operation

- Stationary Equipment

- Mobile / Portable Equipment

-

By Automation Level

- Manual

- Semi-automatic

- Fully Automatic / Smart

-

By Power Source

- Diesel

- Electric

- Hybrid

- Hydraulic / PTO-driven

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Colombia

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

-

Middle East and Africa

- GCC

- Israel

- Turkey

- South Africa

- Egypt

- Rest of Middle East and Africa

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- Australia & New Zealand

- Rest of Asia-Pacific

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed equipment OEM managers, municipal procurement officers, and integrated waste-management contractors across Asia-Pacific, North America, and Europe. Dialogs validated utilization rates, emerging automation preferences, and realistic replacement cycles, while short surveys of registered recyclers clarified average selling prices and delivery lead times.

Desk Research

We begin with a literature sweep across open institutional datasets such as UN-Habitat's Solid Waste Indicators, World Bank "What a Waste 2.0," Eurostat waste statistics, and EPA Advancing Sustainable Materials Management reports, complemented by industry codes from customs databases like UN Comtrade and voluntary disclosures on landfill-tax collections. Company filings, procurement portals, sectoral trade journals, and news archives accessed through Dow Jones Factiva and D&B Hoovers supply price curves, capacity additions, and M&A clues. These illustrate market drivers and boundary conditions; many other reputable sources were also reviewed for cross-checks and contextual depth.

Market-Sizing & Forecasting

A top-down build starts with country-level waste generation, collection coverage, and disposal route shares; these volumes are converted into addressable equipment pools through penetration coefficients that reflect machinery stock per thousand metric tons processed. Selective bottom-up roll-ups, sampling listed OEM revenues, channel checks, and ASP × unit shipments, calibrate the totals. Key variables weighed in our multivariate regression forecast include urban population growth, landfill-gate fees, mandatory source-segregation laws, average equipment service life, and electrification uptake in refuse fleets. Where bottom-up samples are thin, gaps are bridged by triangulating regional import data with confirmed ASP corridors.

Data Validation & Update Cycle

Outputs pass anomaly checks against independent indicators, then undergo senior analyst review. Reports refresh annually, and mid-cycle events, major regulatory shifts, large public tenders, or material currency swings, trigger expedited model updates before client delivery.

Why Mordor's Waste Disposal Equipment Baseline Commands Reliability

Published estimates often diverge because studies mix dissimilar equipment classes, apply varied currency conversions, or stretch refresh cadences. By locking scope to true disposal machinery and refreshing figures every twelve months, Mordor delivers a balanced baseline decision-makers can trace back to public waste volumes and verified OEM revenues.

Key gap drivers include:

1. Some publishers fold recycling, collection trucks, and service revenue into equipment totals, inflating values.

2. Others extrapolate limited import statistics without validating local fabrication or refurbish flows.

3. Currency and ASP progressions vary; certain studies freeze exchange rates or assume linear price growth, whereas we apply year-specific averages vetted through supplier calls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.46 B (2025) | Mordor Intelligence | - |

| USD 13.53 B (2024) | Regional Consultancy A | Combines disposal with recycling machinery; undisclosed ASP multipliers |

| USD 18.51 B (2024) | Global Consultancy B | Adds refuse trucks and service contracts; constant-currency assumption |

| USD 14.34 B (2024) | Industry Association C | Extends partial import data; single-factor trend projection |

Taken together, the comparison shows that when scope discipline, variable selection, and timely refreshes are applied, Mordor's numbers remain the most reproducible and, therefore, the soundest reference point for strategic planning.

Key Questions Answered in the Report

What is the current value of the Global waste disposal equipment market?

The current value of the Global Waste Disposal Equipment Market in 2026 is USD 4.7 billion.

Which region leads Global waste disposal equipment market revenue?

Asia-Pacific holds 46.50% of 2025 revenue due to rapid urbanization and industrial growth.

What equipment category has the highest Global waste disposal equipment market share?

Waste-recycling machinery led with a 35.40% share in 2025, supported by upgrades to AI-enabled sorters.

How fast is hazardous-waste equipment expected to grow?

Hazardous-waste processing systems are projected to expand at an 7.7% CAGR from 2026 to 2031.

Why are electric refuse trucks gaining popularity?

They provide 40-62% operating-cost savings and meet tightening emission targets, making them attractive to municipalities and private haulers.

What role do AI-powered optical sorters play in the industry?

They raise material-recovery accuracy to 99% and lower lifecycle costs by over 40%, accelerating automation in recycling facilities.

Page last updated on: