Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 206.59 Billion |

| Market Size (2026) | USD 217.39 Billion |

| Market Size (2031) | USD 280.63 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Endoscopy Devices Market Analysis by Mordor Intelligence

The UAE endoscopy devices market size is expected to grow from USD 206.59 million in 2025 to USD 217.39 million in 2026 and is forecast to reach USD 280.63 million by 2031 at 5.23% CAGR over 2026-2031. Accelerating public- and private-sector health investment, rising medical tourism volumes, and a high burden of lifestyle diseases collectively sustain a steady pipeline of diagnostic and therapeutic endoscopic procedures. Obesity prevalence is forecast to reach 95% by 2050, while diabetes already affects more than 2.2 million residents, sharply lifting screening demand across gastroenterology and pulmonology. Government strategy places minimally invasive technology, UHD imaging, and AI-assisted platforms at the core of future care models, reinforcing the UAE endoscopy devices market as a regional innovation test-bed. Intensifying competition among premium hospitals, joint-venture clinics, and ambulatory centers further drives replacement cycles for sophisticated visualization systems and single-use scopes. Despite optimistic fundamentals, the market must navigate skilled-workforce shortages and complex device reprocessing protocols that can slow adoption of newer platforms.

Key Report Takeaways

- By product type, endoscopes led with 55.02% UAE endoscopy devices market share in 2025, while visualization equipment is forecast to expand at a 7.88% CAGR to 2031.

- By application, gastroenterology commanded 45.12% of the UAE endoscopy devices market size in 2025; pulmonology/bronchoscopy is advancing at a 7.02% CAGR through 2031.

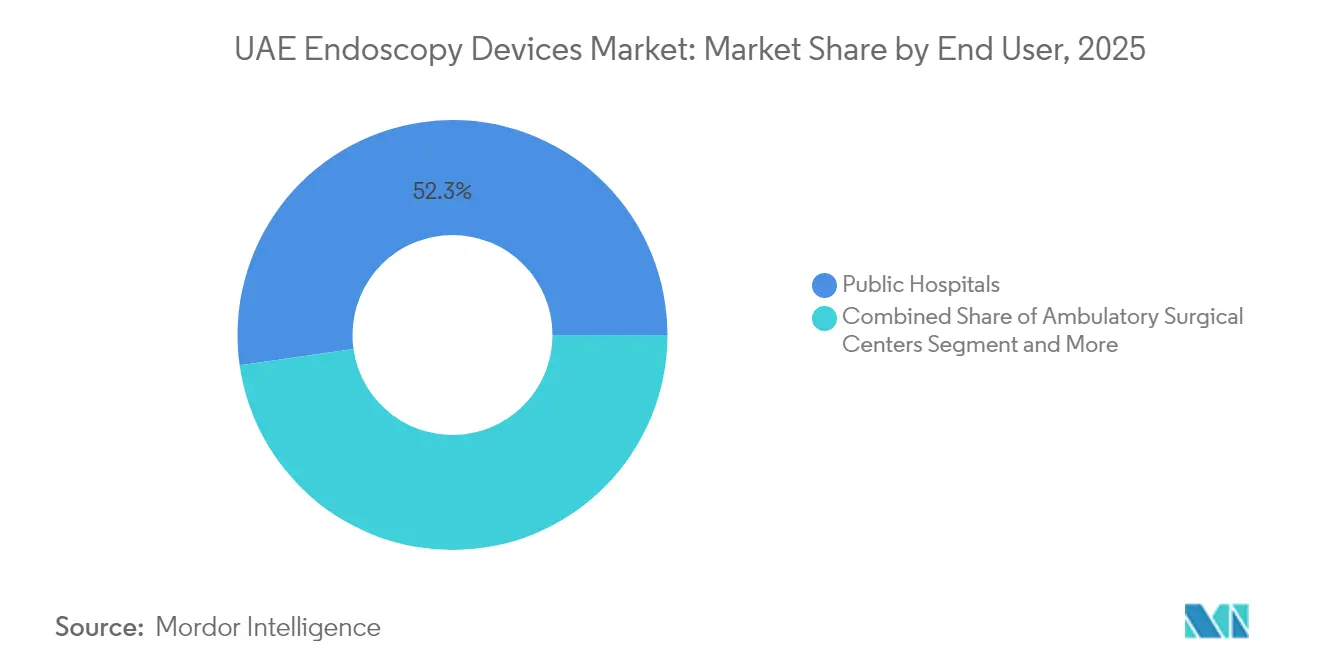

- By end user, public hospitals held 52.25% of 2025 revenue, whereas ambulatory surgical centers record the highest projected CAGR at 6.93% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of gastrointestinal disorders | +1.8% | National, urban centers | Long term (≥ 4 years) |

| Growing preference for minimally invasive surgeries | +1.2% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Rapid technological upgrades in UHD & AI imaging | +1.1% | Nationwide | Medium term (2-4 years) |

| Government investments in endoscopy capacity | +0.9% | Abu Dhabi & Dubai | Short term (≤ 2 years) |

| Surge in medical-tourism-driven bariatric demand | +0.7% | Key free-zone hospitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Minimally Invasive Surgeries

Patient demand for faster recovery and better cosmetic outcomes accelerates nationwide uptake of minimal-access procedures. Mediclinic City Hospital surpassed 1,500 robotic cases by late 2024, illustrating the pace of technology integration into routine practice[1]Gulf News, “Mediclinic City Hospital carries out 1,500th robotic surgery,” gulfnews.com. Gastroenterology units now default to endoscopic therapy for many lesions, reducing open surgical volumes. Tourism portals actively promote “scar-less” packages, reinforcing the UAE endoscopy devices market as a destination for specialty care. Regulatory bodies back the shift: the Department of Health Abu Dhabi has fast-tracked approvals for disposable scopes and AI-enabled colonoscopy platforms. Facility operators respond by expanding robotic-assisted endoscopy suites, bolstering procedural throughput and differentiating service portfolios.

Rising Burden of Gastrointestinal Disorders in UAE

Sedentary lifestyles and calorie-dense diets have raised overweight prevalence to 68% and obesity to 28%, with a future trajectory among the highest worldwide. Associated reflux disease, Barrett’s esophagus, and colorectal cancers demand ongoing endoscopic surveillance. Healthcare economists place current obesity-related spending near USD 12 billion annually, equal to 5% of GDP, giving hospitals strong incentive to detect and treat early. A multicenter pediatric study shows only 65% first-line eradication for Helicobacter pylori, underscoring the need for repeat diagnostic endoscopy. National health surveys now embed GI screening metrics, informing capacity planning for new centers. These dynamics underpin sustained procedure growth and additional equipment procurement across the UAE endoscopy devices market.

Government Investments in Endoscopy Capacity (SEHA, DHA)

SEHA, MOHAP, and Pure Health collectively channel multibillion-dirham budgets into localized sourcing of advanced towers, processors, and training programs. Pure Health alone earmarked AED 10 billion for domestic procurement over ten years, accelerating fleet renewal in public hospitals. Tele-endoscopy capabilities have expanded through RoboDoc installations, linking peripheral clinics with tertiary experts for real-time consultations. Foreign-ownership allowances of up to 100% under Federal Law 16 attract OEMs to assemble and service devices locally, shortening lead times[2]Department of Health Abu Dhabi, “Technology Registry,” doh.gov.ae. Virtual-nurse and AI triage pilots further integrate imaging with e-health ecosystems. Together, these policies enlarge the addressable base for the UAE endoscopy devices market.

Rapid Technological Upgrades in UHD & AI Imaging

Manufacturers race to embed artificial intelligence that flags polyps, grades inflammation, and guides biopsies in real time. Fujifilm’s CAD EYE and Olympus’s Extended Depth-of-Field scopes represent early commercial rollouts adopted by UAE flag-ship centers. National 6G roadmaps promise millisecond-latency imaging streams, enabling remote mentoring and cross-border referrals. Joint platforms from Oracle, Cleveland Clinic, and G42 bring nation-scale analytics that benchmark endoscopy outcomes and optimize device utilization. Early cancer-detection algorithms under the HCFL alliance complement UHD optics to elevate diagnostic precision[3]Ministry of Health and Prevention, “Innovation Health Strategy,” mohap.gov.ae. Cumulatively, technology upgrades reinforce premium positioning of the UAE endoscopy devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection risk from complex device reprocessing | -1.2% | Nationwide | Medium term (2-4 years) |

| Shortage of skilled endoscopy technicians | -0.8% | Northern Emirates | Short term (≤ 2 years) |

| High import tariffs on single-use scopes | -0.6% | Private facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Endoscopy Technicians

Rapid procedure expansion has outpaced personnel supply, especially in outer emirates. In response, Dubai Health Authority now issues three-month temporary permits to attract visiting technologists. However, strict Professional Qualification Requirements across federal regulators slow permanent recruitment. A 2025 workforce study found 35% of healthcare staff themselves suffer non-communicable diseases, raising absenteeism and turnover. Advanced procedures such as endoscopic submucosal dissection need specialized skill sets rarely available in smaller cities. Wage inflation therefore increases operating costs and may defer capital expenditure, tempering near-term gains in the UAE endoscopy devices market.

Infection Risk from Complex Device Reprocessing

High-level disinfection of flexible scopes involves dozens of precise steps, and any deviation carries significant liability under the Federal Decree-Law on Medical Liability. Duodenoscopes and bronchoscopes present particular challenges due to elevator mechanisms and narrow lumens. The Department of Health Abu Dhabi regularly audits hospitals for compliance with its sterilization policy, citing penalty provisions for failure to meet standards. Some facilities pivot to single-use devices, but import tariffs and the absence of local manufacturing create cost pressure. Balancing safety, cost, and environmental waste remains a strategic hurdle across the UAE endoscopy devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Device: Visualization Equipment Drives Innovation

Endoscopes represented the largest revenue block in 2025, accounting for 55.02% of the UAE endoscopy devices market size, underscoring their irreplaceable diagnostic role. Flexible models dominate given their cross-specialty utility, while capsule and robot-assisted formats capture niche demand in small-bowel and complex resections. Disposable scopes gain ground as infection-control policies tighten. Visualization equipment posted the fastest revenue trajectory at an 7.88% CAGR and is central to procurement plans of both public and private chains. UHD camera heads, AI-ready processors, and 3-chip sensors elevate mucosal pattern recognition during colonoscopy. Cloud connectivity enables instant second opinions, a key differentiator for facilities courting inbound medical travelers. As AI algorithms mature, visualization systems transition from passive imaging to active diagnostic partners, anchoring future growth in the UAE endoscopy devices market.

Momentum for endoscopic operative devices remains linked to procedure complexity. Irrigation pumps with programmable flow, articulating retrieval baskets, and hemostatic clips integrate seamlessly with modern towers. National investment programs favor suppliers that localize service centers, cutting downtime for critical tools. Meanwhile, next-generation robotic platforms such as EndoMaster and EndoQuest move through evaluation phases, promising higher precision in submucosal dissections. These developments broaden the value proposition of the UAE endoscopy devices market beyond basic diagnosis toward full therapeutic intervention suites.

By Application: Pulmonology Procedures Accelerate Growth

Gastroenterology retained a 45.12% revenue share in 2025, reflecting high lesion prevalence and established reimbursement pathways. Routine screening colonoscopies, therapeutic ERCP, and bariatric revision studies underpin stable device utilization. Surgeons increasingly integrate endoluminal suturing and balloon therapies to manage obesity, reinforcing the UAE endoscopy devices market where volumes are forecast to rise in line with rising BMI profiles. Cross-functional care pathways between endocrinology and GI units further expand patient throughput.

Pulmonology and bronchoscopy lead incremental growth with a 7.02% CAGR as lung-cancer screening programs gain traction. AI-enabled navigation bronchoscopy systems improve reach to peripheral nodules, reducing the need for surgical wedge biopsies. Cardiovascular, orthopedic, and urologic applications also diversify device usage. In cardiology, transesophageal echo probes and endoscopic mitral-valve repair tools enter routine practice at tertiary centers. Such procedural diversification supports resilient revenue streams for vendors active in the UAE endoscopy devices industry, tempering risk tied to individual specialty cycles.

By End User: Ambulatory Centers Lead Growth Trajectory

Public hospitals remained the primary procurement channel in 2025, commanding 52.25% of the UAE endoscopy devices market size, buoyed by federally funded capacity expansion and population coverage mandates. SEHA’s capital expenditure program refreshes aging towers with UHD systems, ensuring uniform diagnostic quality across its network. AI-driven scheduling platforms optimize room allocation to reduce waiting lists, thereby raising device turn-over rates.

Ambulatory surgical centers, however, deliver the fastest expansion at a 6.93% CAGR as payers reward same-day discharge models. Purpose-built units inside Dubai Healthcare City and Abu Dhabi’s free zones target self-pay and insurance patients seeking convenience. Portable towers and single-use scopes lower initial CapEx and sidestep complex reprocessing rooms, aligning with lean operating models. Specialty clinics offering combined gastro-pulmonary screenings capture cross-referral synergies, supporting continued proliferation of facilities equipped for advanced procedures. The evolving end-user mix diversifies revenue channels within the UAE endoscopy devices market.

Geography Analysis

Dubai and Abu Dhabi anchor premium care delivery, together accounting for the majority of high-definition towers, robotic platforms, and AI-aided processors installed to date. Competitive clustering around Dubai Healthcare City, Cleveland Clinic Abu Dhabi, and Sheikh Shakhbout Medical City reinforces global referral networks. These hubs benefit from direct flight connectivity and streamlined patient-entry visas, sustaining elevated case volumes that justify continual upgrades. The UAE endoscopy devices market therefore registers its highest average selling prices in these two emirates.

Northern emirates such as Sharjah, Ajman, and Ras Al Khaimah present emerging opportunity pockets. Population growth and industrial diversification raise healthcare demand, prompting private investors to build mid-tier hospitals capable of advanced scoping. Government co-funding for equipment, often tied to local-content rules, accelerates procurement cycles. The UAE endoscopy devices market consequently broadens beyond historical metropolitan confines, although reimbursement and staffing remain tighter outside flagship cities.

The nation’s transcontinental logistics advantage positions it as a re-export hub for Gulf and African markets. Medtronic and Olympus maintain regional distribution centers in Jebel Ali Free Zone, reducing lead times for neighboring countries. Upcoming 6G networks will enable real-time tele-operation, extending premium procedural expertise to remote GCC clinics. Multilateral initiatives, including the GCC unified procurement framework, may further inflate shipment volume through UAE ports, cementing the country’s role in the wider Middle East endoscopy supply chain. Consequently, geography continues to shape vendor strategies within the UAE endoscopy devices market.

Competitive Landscape

Global majors remain the cornerstone of the competitive arena. Olympus leads flexible endoscopes, Medtronic commands hemostatic and energy devices, and Boston Scientific excels in therapeutic accessories. Each leverages local training academies to embed workflows and drive brand loyalty among clinicians. Recent FDA clearance of Olympus’s EZ1500 series prompted immediate tender activity in key UAE public hospitals, illustrating rapid technology diffusion cycles. Parallel alliances with cloud providers, exemplified by the Microsoft-G42 tie-up, underscore a pivot toward data-centric differentiation.

Regional conglomerates amplify competitive intensity. The 2024 merger of G42 Healthcare and Mubadala Health created a vertically integrated giant that influences procurement standards and accelerates local manufacturing pilots. Pure Health’s long-term supply contracts and domestic-value targets increasingly direct tender awards to vendors willing to invest in assembly lines on UAE soil. Smaller entrants differentiate via single-use innovations and robotics; EndoQuest Robotics’ partnership talks with Dubai-based investors typify this niche race. Overall, moderate consolidation persists as the UAE endoscopy devices market balances incumbent dominance with agile newcomers.

Strategic imperatives now revolve around AI validation datasets, post-market surveillance, and service uptime. Vendors pair warranty packages with remote diagnostics to satisfy stringent Ministry of Health uptime requirements. Training initiatives extend beyond physicians to include reprocessing technicians, addressing infection-control concerns that could otherwise impede sales. Suppliers that integrate hardware, software, and education offerings are poised to capture disproportionate share as hospitals upgrade toward fully digital, minimally invasive operating ecosystems within the UAE endoscopy devices industry.

UAE Endoscopy Devices Industry Leaders

Boston Scientific Corporation

Stryker Corporation

Richard Wolf GmbH

Medtronic PLC

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Burjeel Holdings and Colombia’s Keralty formed AL KALMA to roll out value-based gastroenterology programs across MENA with embedded advanced endoscopy services.

- January 2025: Oracle Health, Cleveland Clinic, and G42 agreed to co-develop an AI platform that enhances nation-scale analytics for endoscopic care planning.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the UAE endoscopy devices market as the annual revenue generated from new endoscopes, endoscopic operative tools, and dedicated visualization systems that support diagnostic or therapeutic procedures performed through natural orifices or minimal incisions within licensed healthcare facilities. Devices used solely for open surgery or independent robotic surgery platforms fall outside this boundary.

Scope exclusion: reprocessing equipment, standalone imaging towers sold for laparoscopy only, and general surgical consumables are not counted.

Segmentation Overview

- By Type of Device

- Endoscopes

- Rigid Endoscopes

- Flexible Endoscopes

- Capsule Endoscopes

- Robot-assisted Endoscopes

- Disposable/Single-use Endoscopes

- Endoscopic Operative Devices

- Irrigation / Suction Systems

- Access Devices & Trocars

- Wound Protectors & Specimen Retrieval

- Other Operative Devices

- Visualization Equipment

- Camera Heads & Processors

- Monitors & Display Systems

- Light Sources

- Recording / Data Management

- Endoscopes

- By Application

- Gastroenterology

- Pulmonology / Bronchoscopy

- Urology

- Gynecology

- Cardiology

- Bariatric & Metabolic Endoscopy

- ENT & Laryngology

- Orthopedics / Arthroscopy

- Other Applications

- By End User

- Public Hospitals (MOHAP & SEHA)

- Private Multi-specialty Hospitals

- Ambulatory Surgical Centers

- Specialty & Diagnostic Clinics

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed gastroenterologists, biomedical engineers, supply-chain chiefs, and procurement officers across Dubai, Abu Dhabi, and Sharjah. These conversations clarified in-use device lifecycles, emerging demand for single-use scopes, and pricing spreads, allowing us to resolve gaps detected in secondary data.

Desk Research

We began with open data sets from sources such as UAE's Ministry of Health & Prevention procedure registers, Federal Competitiveness & Statistics Center trade codes, and Dubai Health Authority capital-equipment tenders. Clinical incidence trends were cross-checked against peer-reviewed journals hosted on PubMed, while import values were reconciled with UN Comtrade HS-codes 9018.19 and 9018.90. Company filings and investor decks enriched average selling-price insights, which were further bookmarked in D&B Hoovers and Dow Jones Factiva feeds. The sources named are illustrative; many other public documents assisted our desk analysis.

Market-Sizing & Forecasting

A top-down reconstruction started with 2024 procedural volumes by application segment, then applied weighted device penetration rates and validated ASPs to reach a value pool, which is subsequently pressure-tested through sampled supplier roll-ups. Key model inputs include colorectal-cancer screening throughput, obesity-linked bariatric endoscopy growth, hospital bed additions, replacement cycles (5-7 years), disposable-scope adoption, and import duty shifts. A multivariate regression, updated annually, projects demand to 2030. Bottom-up checks from channel audits correct deviations above a 5% variance threshold.

Data Validation & Update Cycle

Outputs run through anomaly checks, peer review within the analyst team, and variance reconciliation versus fresh trade and procedure statistics. The report refreshes every twelve months, with interim updates if regulatory or reimbursement events materially alter the baseline.

Why Mordor's UAE Endoscopy Devices Baseline Commands Reliability

Published estimates often diverge because publishers pick different device baskets, years, and refresh cadences. We address these pitfalls through a clearly stated scope, live primary inputs, and annual recalibration.

Gaps elsewhere generally stem from focusing on either core scopes alone or projecting from historic growth without in-country validation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 206.59 mn (2025) | Mordor Intelligence | - |

| USD 134 mn (2023) | Regional Consultancy A | narrower product mix; two-year older base; limited clinical interviews |

| USD 54.5 mn (2023) | Global Consultancy B | measures endoscopes only; excludes visualization and operative devices; no tender cross-checks |

Readers can therefore trust that Mordor's figures reflect the full device ecosystem, are grounded in local evidence, and remain repeatable for subsequent decision cycles.

Key Questions Answered in the Report

What is the current value of the UAE endoscopy devices market?

The market is valued at USD 217.39 million in 2026 and is expected to reach USD 280.63 million by 2031.

Which device category holds the largest market share?

Endoscopes hold the leading 55.02% revenue share, driven by widespread use across multiple medical specialties.

Why are ambulatory surgical centers growing so quickly?

Outpatient centers offer shorter stays and lower costs; they therefore post the highest 6.93% CAGR as patients and insurers favor efficient care settings.

How does obesity influence endoscopy demand in the UAE?

With projections showing obesity affecting 95% of residents by 2050, demand for diagnostic and therapeutic GI procedures is rising sharply, sustaining equipment purchases.

What technological trends are shaping future market growth?

Ultra-high-definition imaging, AI-based real-time polyp detection, and emerging robotic platforms are redefining procedure accuracy and driving replacement demand.

Are single-use endoscopes becoming common in the UAE?

Yes, infection-control and workflow efficiency concerns push many private and ambulatory centers toward disposable scopes, though tariffs and cost remain adoption hurdles.

Page last updated on: