Sealing And Strapping Packaging Tapes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

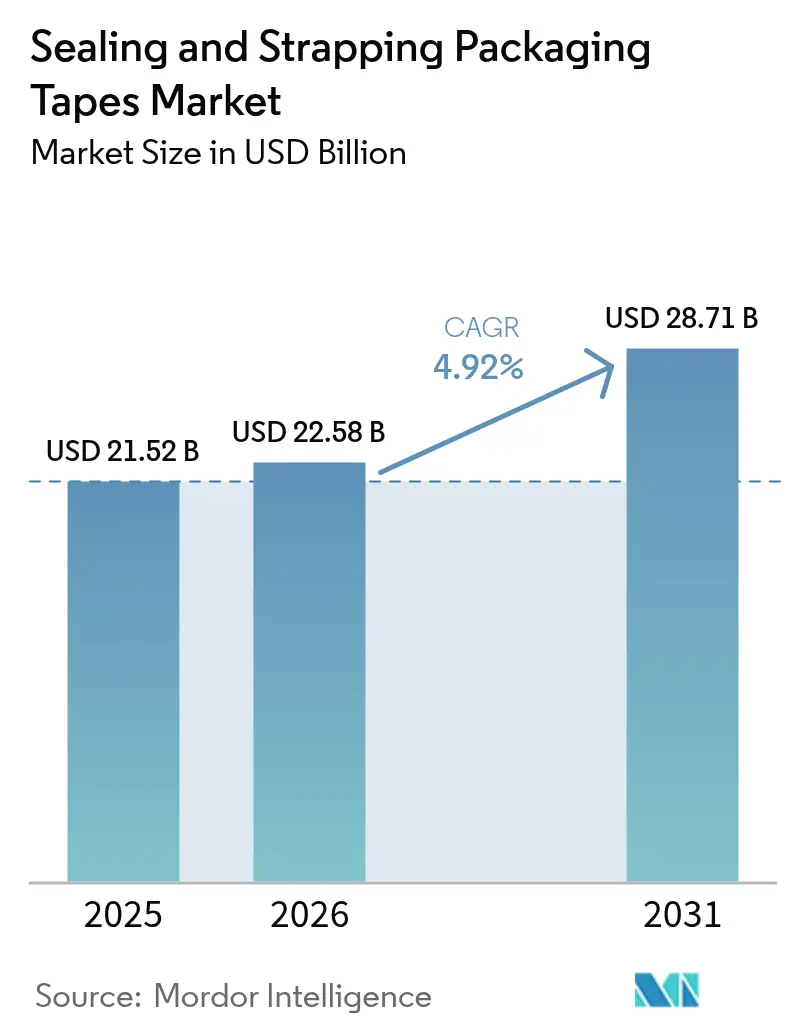

| Market Size (2026) | USD 22.58 Billion |

| Market Size (2031) | USD 28.71 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sealing And Strapping Packaging Tapes Market Analysis by Mordor Intelligence

The sealing and strapping packaging tapes market size is expected to grow from USD 21.52 billion in 2025 to USD 22.58 billion in 2026 and is forecast to reach USD 28.71 billion by 2031 at 4.92% CAGR over 2026-2031. Consistent demand from e-commerce fulfillment centers, automated logistics hubs, and consumer-goods brands positions the sealing and strapping packaging tapes market as a critical component of global supply-chain continuity. Growth stems from surging parcel volumes, rapid warehouse automation, and rising requirements for tamper-evidence and track-and-trace features that enhance shipment integrity. Material reformulations that lower carbon footprints and improve recyclability expand the addressable customer base, while smart tapes equipped with RFID and QR technologies add value through real-time inventory visibility. Competitive dynamics favor companies that balance cost efficiency, technical performance, and sustainability credentials in line with tightening regulatory standards.

Key Report Takeaways

- By end-use industry, logistics and warehousing held 55.02% of the sealing and strapping packaging tapes market share in 2025, whereas pharmaceuticals and medical devices are projected to grow at an 8.12% CAGR through 2031.

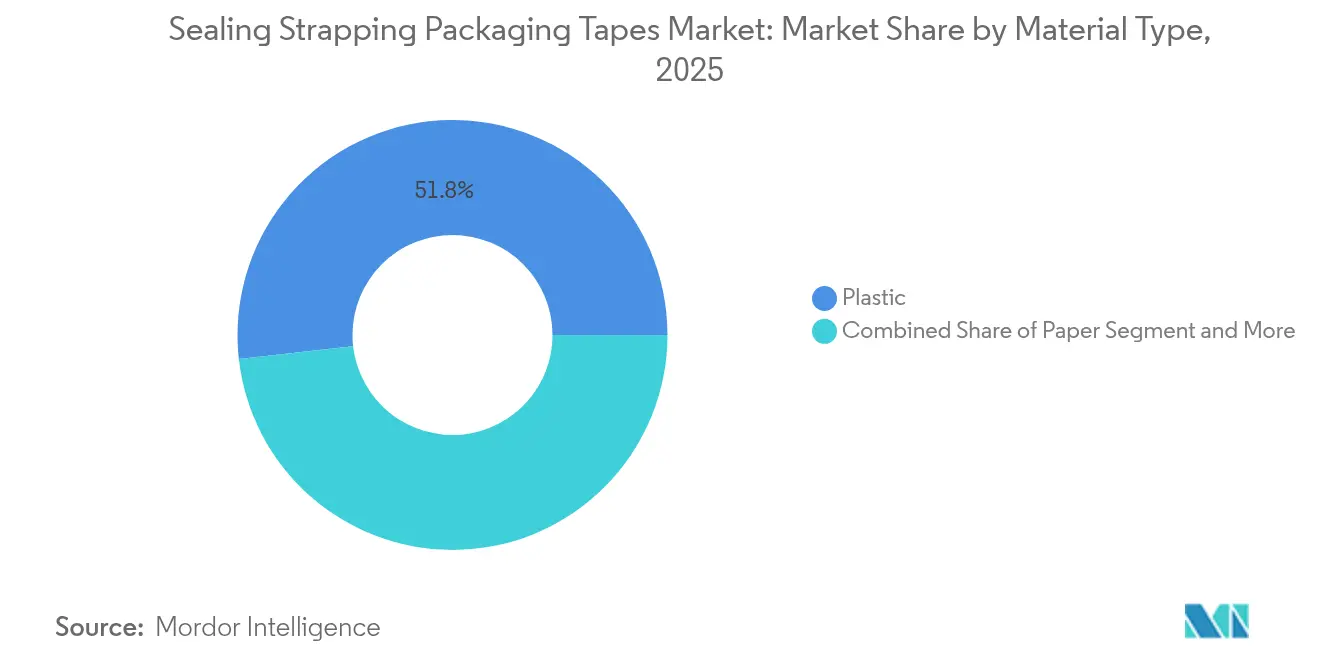

- By material type, plastic tapes captured 51.78% of revenue in 2025, while paper tapes are expected to climb at a 8.78% CAGR to 2031.

- By adhesive chemistry, acrylic formulations accounted for 46.92% of the sealing and strapping packaging tapes market size in 2025; rubber-based systems represent the fastest trajectory with an 7.94% CAGR through 2031.

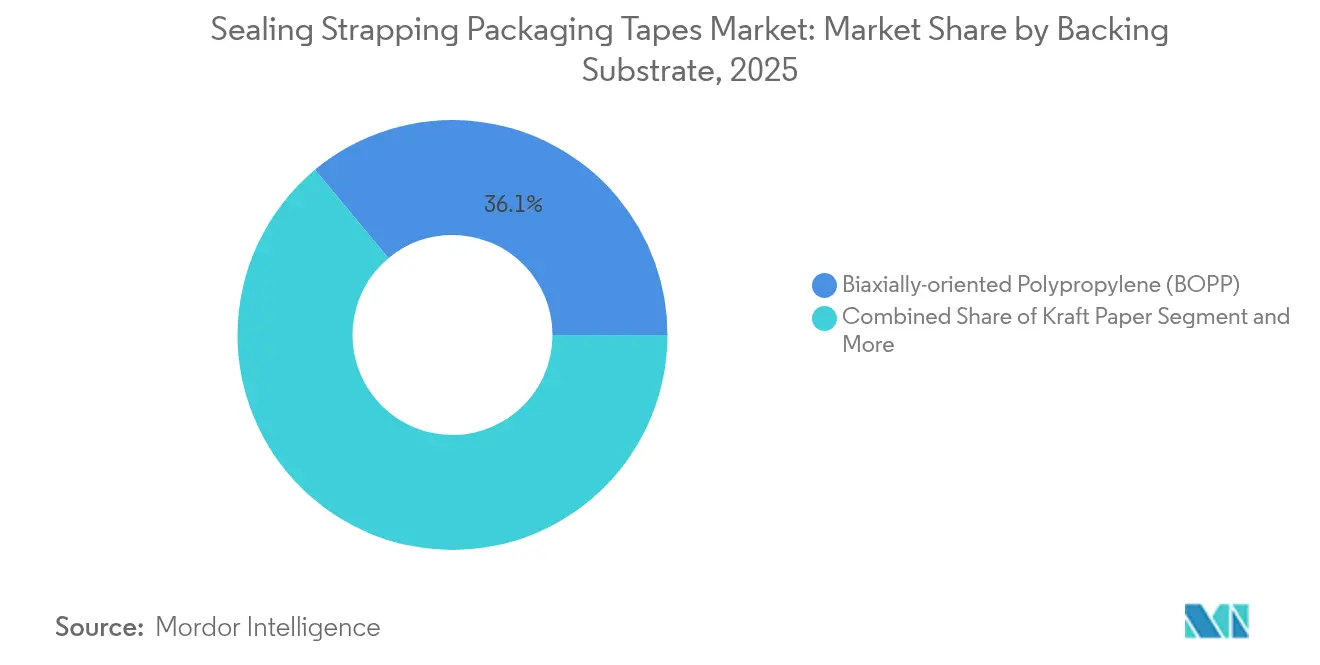

- By backing substrate, biaxially oriented polypropylene (BOPP) led with 36.05% revenue share in 2025; PVC backings are forecast to register a 7.05% CAGR to 2031.

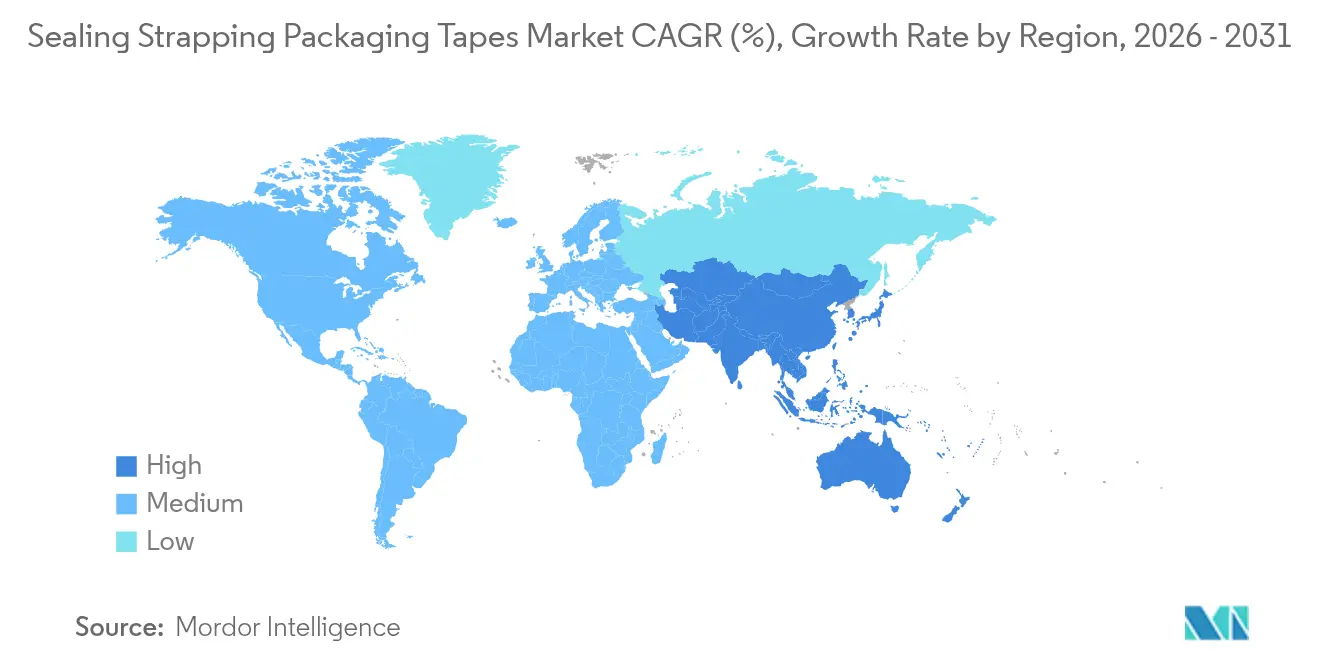

- By geography, Asia-Pacific dominated with 38.10% revenue share in 2025 and is poised for an 8.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sealing And Strapping Packaging Tapes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom boosting carton-sealing tape consumption | +1.80% | Global, with Asia-Pacific and North America leading | Medium term (2–4 years) |

| Expansion of global logistics and warehousing hubs | +1.20% | Global, concentrated in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Cost-performance shift toward BOPP and PET tapes | +0.90% | Global, particularly in emerging markets | Medium term (2–4 years) |

| Smart tamper-evident tapes with RFID/QR for traceability | +0.60% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth in recyclable water-activated paper tapes | +0.50% | Europe and North America, driven by regulations | Short term (≤ 2 years) |

| Rise of automated packaging lines increasing demand for machine-grade tapes | +0.70% | North America, Europe, and rapidly in Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

E-commerce boom boosting carton-sealing tape consumption

Digital retail accelerates parcel counts, multiplying tape usage per shipment as each box requires primary sealing, reinforcement, and tamper evidence. High-speed fulfillment centers specify low-noise, high-adhesion tapes capable of withstanding temperature swings from cold-chain nodes to desert delivery routes. Custom-printed tapes double as security devices and brand assets, supporting direct-to-consumer marketing strategies. Cross-border sellers demand multi-certified products that comply with food-contact and pharmaceutical rules, creating premium niches for suppliers able to verify conformity.[1]3M, “Scotch Brand celebrates 100 years of innovation and reliability,” 3m.com The sealing and strapping packaging tapes market is therefore tightly coupled to the volume and sophistication of last-mile delivery operations.

Expansion of global logistics and warehousing hubs

Automated warehouses rely on robotic taping systems that require substrates with consistent unwind profiles and controlled adhesion curves. Investments in cold-storage and pharma distribution centers spur demand for low-temperature adhesives that avoid brittleness at sub-zero conditions. Regional hubs in the UAE and Saudi Arabia broaden supply footprints, lifting tape consumption in the Middle East and Africa. Meanwhile, just-in-time inventory models shorten production lots, driving smaller but more frequent tape orders that benefit converters with flexible scheduling capabilities. Through 2030, the sealing and strapping packaging tapes market is expected to shadow global warehouse square-footage growth.

Cost-performance shift toward BOPP and PET tapes

Scale economies in Asian film manufacturing keep BOPP price points attractive, while new resins deliver stronger tensile strength and better printability. PET backings gain favor in electronics and automotive packaging, where chemical resistance and dimensional stability are mission-critical.[2]Ahlstrom, “Ahlstrom Completes Paper Machine Conversion at Thilmany Mill,” paperage.com As these films better withstand strapping tension and environmental stress, users transition away from PVC, cutting material costs without sacrificing security. Performance improvements, coupled with developing recycling streams for polyolefin films, reinforce BOPP and PET adoption across the sealing and strapping packaging tapes market.

Smart tamper-evident tapes with RFID/QR for traceability

Retail mandates from major chains accelerate uptake of RFID-enabled tapes that broadcast SKU-level data and detect pilferage. QR-coded variants connect consumers to authentication portals, supporting anti-counterfeit programs in pharmaceuticals compliant with ISO 21976 requirements. Partnerships such as DataLase–TamperTech embed security pigments directly into tape substrates, trimming waste while raising barrier properties. As printing costs decline and smartphone scanning becomes universal, smart tapes transition from niche to mainstream, underpinning digital supply-chain strategies throughout the sealing and strapping packaging tapes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petroleum-based raw-material prices | -1.4% | Global, particularly affecting Asian producers | Short term (≤ 2 years) |

| Strict regulations on single-use plastics | -0.8% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Adhesive-VOC emission compliance costs | -0.6% | North America and EU, with Asia-Pacific adoption | Medium term (2-4 years) |

| Automation bottlenecks in paper-tape dispensing lines | -0.4% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile petroleum-based raw-material prices

Propylene and ethylene cost swings squeeze converters’ margins as polypropylene and polyethylene account for a significant slice of input spnd. Cracker shutdowns in Southeast Asia heighten supply risk, forcing producers to hedge inventories or negotiate formula-based contracts. Adhesive ingredients follow similar volatility, particularly natural rubber used in high-tack tapes. Short-term price spikes strain smaller manufacturers with limited purchasing leverage, potentially slowing capacity additions in the sealing and strapping packaging tapes market.

Strict regulations on single-use plastics

Europe’s Packaging and Packaging Waste Regulation compels 100% recyclability and minimum recycled content, triggering reformulation costs for conventional polyolefin tapes.[3]European Commission, “New rules for more sustainable and competitive packaging economy,” environment.ec.europa.eu Extended Producer Responsibility schemes shift disposal fees onto material suppliers, altering total delivered costs. Parallel plastic-tax initiatives and labeling mandates add administrative burdens, accelerating customer migration to paper or hybrid substrates. While compliance fuels innovation, near-term capex requirements can deter investment, tempering growth in regulated regions of the sealing and strapping packaging tapes market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastic Leads as Paper Accelerates

Plastic tapes retained 51.78% of revenue in 2025 thanks to durable BOPP and PET films that combine moisture resistance and competitive pricing. The sealing and strapping packaging tapes market size attributed to plastics is set to climb alongside e-commerce corrugated box usage, though its share gradually erodes as regulations favor fiber-based products. Paper tapes, especially water-activated varieties, post a 8.78% CAGR to 2031, buoyed by recyclability mandates and brand owners’ zero-plastic pledges. European rules calling for fully recyclable packaging by 2030 catalyze paper adoption, while North American retailers promote fiber-based sealing options to meet corporate ESG targets. Hybrid substrates that apply thin poly coatings onto kraft backings emerge, marrying barrier performance with easy repulpability. Material innovators target carbon-neutral formulations by blending recycled content with bio-resins, positioning paper to capture incremental share across premium consumer segments. Over the forecast horizon, plastic producers focus on downgauging and chemical-recycling alliances to maintain relevance within the sealing and strapping packaging tapes market.

By Adhesive Type: Acrylic Dominance Meets Rubber-Based Momentum

Acrylic chemistries delivered 46.92% of 2025 sales, favored for UV stability and storage durability in hot and cold supply chains. Rubber-based systems, including synthetic variants, grow 7.94% annually as high-speed automated lines demand instant tack for faster case-forming cycles. Hot-melt grades gain traction in refrigerated environments, avoiding condensation-related failures. Silicone adhesives, though niche, serve automotive battery and electronics assemblies that face extremes from -300°F to 1000°F. Water-activated starch glues resurge alongside paper backings, with converters investing in precision dispensers to improve cycle times. Partnerships such as Dow–Henkel pursue bio-based polymer designs to cut cradle-to-gate emissions by 25% Dow. Suppliers therefore segment offerings by application, optimizing resin blends to capture diverse opportunities within the sealing and strapping packaging tapes industry.

By Backing Substrate: BOPP Still in Front as PVC Rises in Niche Roles

BOPP represented 36.05% of 2025 revenue, capitalizing on thin-gauge films that lower gram-per-meter costs while maintaining tear resistance. PVC gains market traction at a 7.05% CAGR through 2031, primarily in wire harnessing and heavy-duty industrial wrapping where chemical shields justify higher cost per roll. Kraft paper continues a steady climb as recyclability pressures intensify, particularly in Europe. Polyester backings cater to high-precision electronics and automotive environments requiring dimensional stability. Fiberglass-reinforced tapes dominate pallet strapping and metal-coils bundling, trading volume for margin. Substrate suppliers leverage multi-layer coextrusion technologies to deliver matte finishes for quieter unwinds and ink-receptive surfaces for branding. Continuous film innovation ensures the sealing and strapping packaging tapes market offers tailored solutions for both budget-constrained shippers and highly regulated industries.

By End-Use Industry: Logistics Rules while Pharma Gains Pace

Logistics and warehousing consumed 55.02% of global revenue in 2025, reflecting parcel-based fulfillment’s appetite for dependable sealing. Temperature-sensitive pharmaceuticals emerge as the fastest-moving vertical at an 8.12% CAGR through 2031, propelled by vaccine distribution and biologic drugs requiring validated cold chains. Food-and-beverage producers specify FDA-compliant adhesives resistant to humidity shifts, while electronics shippers demand static-dissipative coatings that shield microchips from electrostatic discharge. Automotive suppliers use filament and specialty masking tapes for component bundling, and renewable-energy assemblers adopt high-performance tapes for solar-panel packaging. Sector-specific regulations drive product diversification, with tape makers offering SKUs fine-tuned for chemical compatibility, temperature profiles, and audit documentation—all supporting continuous expansion of the sealing and strapping packaging tapes market.

Geography Analysis

Asia-Pacific dominated the sealing and strapping packaging tapes market with 38.10% share in 2025 and is projected to advance at 8.55% CAGR to 2031. China sustains volume demand through export-oriented manufacturing, while India’s digital commerce boom elevates parcel counts and paper-tape penetration. Regional governments channel infrastructure spending toward smart warehouses and 5G-enabled logistics corridors, stimulating demand for RFID-compatible tapes. Cross-border e-marketplaces intensify service-level competition, prompting carriers to standardize on global adhesives to minimize in-transit failures. Local suppliers benefit from proximate resin and film capacity, yet multinationals scale up regional plants, as evidenced by tesa’s new Mumbai and Bengaluru hubs that bolster technical support and cut lead times.

North America, though mature, remains lucrative due to premium adoption of smart and sustainable solutions. Tariff dynamics with Canada and Mexico influence raw-material flows and sourcing strategies, pushing converters to balance domestic and imported substrate. Retail consolidation amplifies vendor qualification hurdles, but it also rewards suppliers capable of nationwide service and data-driven performance reporting. Smart-packaging mandates from big-box chains accelerate RFID tape rollouts, turning warehouses into real-time visibility nodes for omnichannel inventory.

Competitive Landscape

The sealing and strapping packaging tapes market shows moderate fragmentation, with global leaders exploiting scale economies in resin procurement, coating technology, and distribution. Companies such as 3M, tesa, Avery Dennison, and Intertape Polymer Group maintain broad product portfolios, international customer-support networks, and dedicated R&D centers. Mid-tier regional firms specialize in application-specific niches—such as cold-chain labels or filament strapping—leveraging localized service to compete on responsiveness

Merger and acquisition activity intensifies as players seek technology additions and geographical reach. Berry Global’s USD 540 million divestiture of its specialty tapes business to Nautic Partners and Atlas Tapes’ acquisition of PPM Industries expand their combined scale and product breadthe. The February 2025 Amcor–Berry Global merger further elevates competitive thresholds as the new entity targets USD 650 million in synergies through integrated resin sourcing and innovation pipelines.

Sealing And Strapping Packaging Tapes Industry Leaders

3M Company

Tesa SE (Beiersdorf)

Nitto Denko Corporation

Intertape Polymer Group

Amcor Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Amcor and Berry Global shareholders approved their merger, targeting USD 650 million in synergies

- February 2025: European Union enacted Packaging and Packaging Waste Regulation mandating 100% recyclable packaging by 2030

- January 2025: tesa launched an AI transformation initiative with Snowflake to establish digital twins for production assets

- December 2024: Atlas Tapes completed the acquisition of PPM Industries Group, expanding its specialty tape footprint

Global Sealing And Strapping Packaging Tapes Market Report Scope

Sealing-strapping-packaging-tapes are pressure-sensitive tapes that consist of a pressure-sensitive adhesive coated onto a backing material which is usually a polypropylene or polyester film, and fiberglass filaments This report segments the market by Material Type(Plastic, Paper, Cellophane), By Adhesive Type (Rubber-based, Acrylic, Hot-melt Adhesive), by End-user Industry(Pharmaceutical, Food Services, Logistics) and Geography.

| Plastic | BOPP |

| PP | |

| PET | |

| PVC | |

| Paper | |

| Foil and Filament | |

| Others |

| Acrylic (Water-/Solvent-/UV) |

| Rubber-based (Natural and Synthetic) |

| Hot-melt |

| Silicone |

| Water-activated Starch-based |

| Biaxially-oriented Polypropylene (BOPP) |

| Kraft Paper |

| Polyester (PET) |

| PVC |

| Glass-fibre Filament |

| Logistics and Warehousing |

| E-commerce and Retail Fulfilment |

| Food and Beverage |

| Pharmaceuticals and Medical Devices |

| Electronics and Electricals |

| Automotive and Industrial |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Plastic | BOPP | |

| PP | |||

| PET | |||

| PVC | |||

| Paper | |||

| Foil and Filament | |||

| Others | |||

| By Adhesive Type | Acrylic (Water-/Solvent-/UV) | ||

| Rubber-based (Natural and Synthetic) | |||

| Hot-melt | |||

| Silicone | |||

| Water-activated Starch-based | |||

| By Backing Substrate | Biaxially-oriented Polypropylene (BOPP) | ||

| Kraft Paper | |||

| Polyester (PET) | |||

| PVC | |||

| Glass-fibre Filament | |||

| By End-use Industry | Logistics and Warehousing | ||

| E-commerce and Retail Fulfilment | |||

| Food and Beverage | |||

| Pharmaceuticals and Medical Devices | |||

| Electronics and Electricals | |||

| Automotive and Industrial | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the sealing and strapping packaging tapes market?

The sealing and strapping packaging tapes market size stands at USD 22.58 billion in 2026 and is projected to reach USD 28.71 billion by 2031.

Which sector uses the most sealing and strapping tapes today?

Logistics and warehousing leads demand, accounting for 55.02% of 2025 global revenue because of rising e-commerce parcel volumes.

Which region is growing the fastest?

Asia-Pacific is the growth engine, forecast at an 8.55% CAGR to 2031 due to manufacturing expansion and digital commerce adoption.

How are regulations affecting material choices?

Europe’s Packaging and Packaging Waste Regulation mandates fully recyclable packaging by 2030, steering many buyers toward paper or hybrid tapes.

Page last updated on: