Building Inspection Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

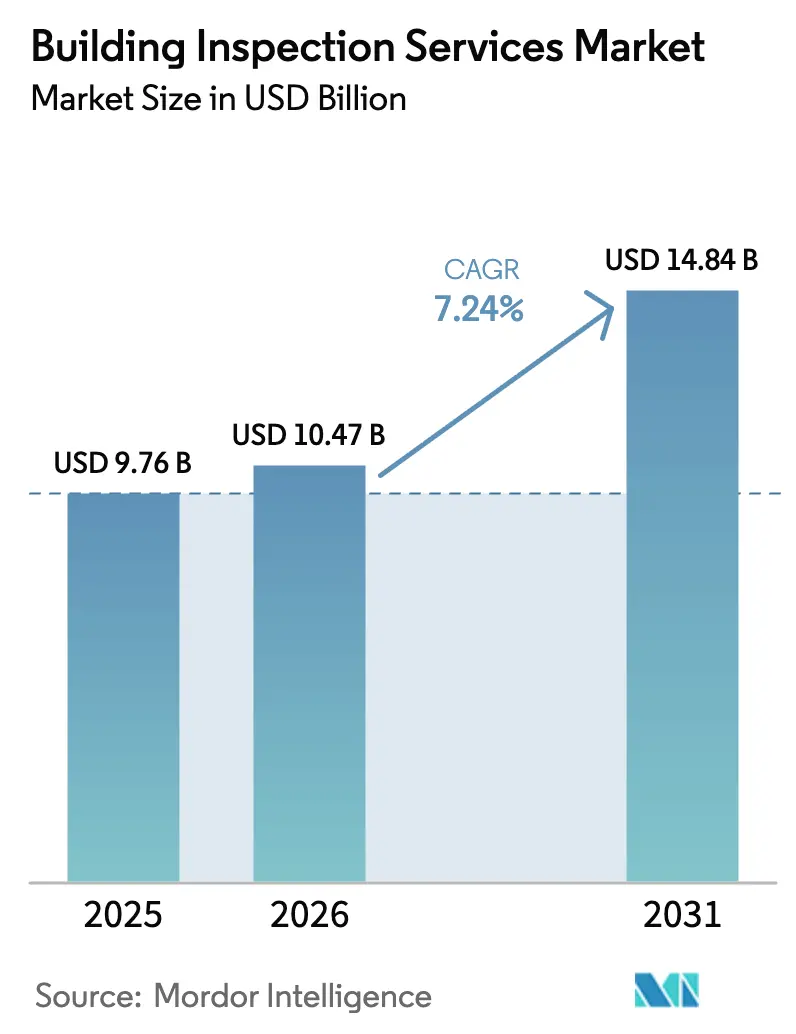

| Market Size (2026) | USD 10.47 Billion |

| Market Size (2031) | USD 14.84 Billion |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

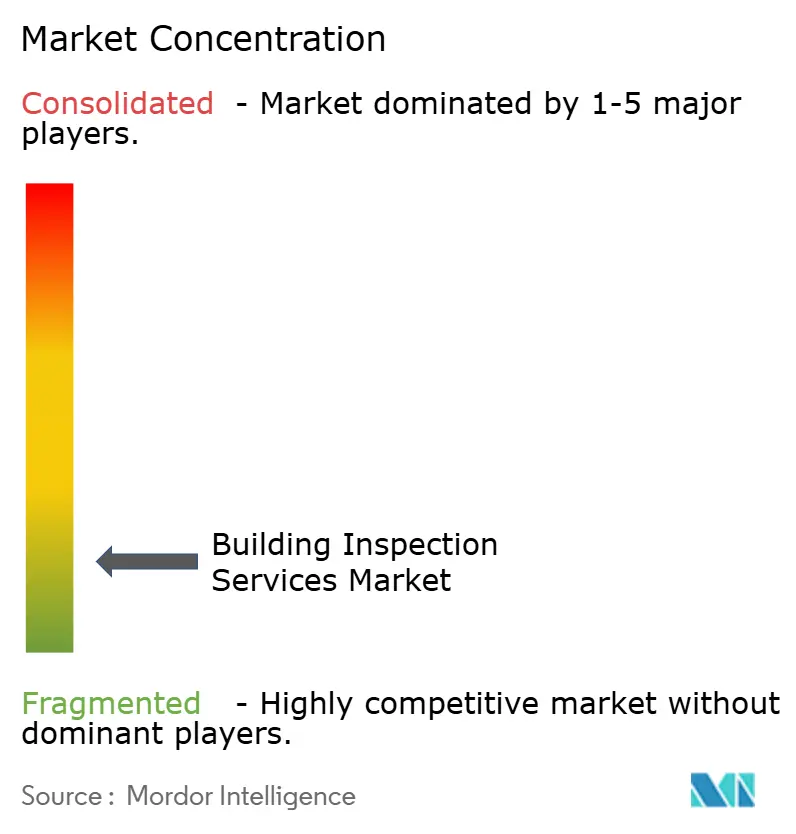

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Building Inspection Services Market Analysis by Mordor Intelligence

Building Inspection Services market size in 2026 is estimated at USD 10.47 billion, growing from 2025 value of USD 9.76 billion with 2031 projections showing USD 14.84 billion, growing at 7.24% CAGR over 2026-2031.

Rising real-estate transaction volumes, tightening safety codes, and rapid uptake of digital tools such as drone imagery and AI-assisted defect analytics are the primary growth catalysts. The European Union’s net-zero building mandate, effective in 2024, is accelerating demand for energy-audit inspections, while North America retains leadership thanks to mature mortgage markets and early technology adoption[1]European Commission, “Energy Performance of Buildings Directive Revision,” europa.eu. The competitive intensity remains high because thousands of local operators coexist with global testing, inspection, and certification (TICC) firms. Market participants who invest in automation, advanced sensors, and data analytics are capturing premium contracts and improving operating margins.

Key Report Takeaways

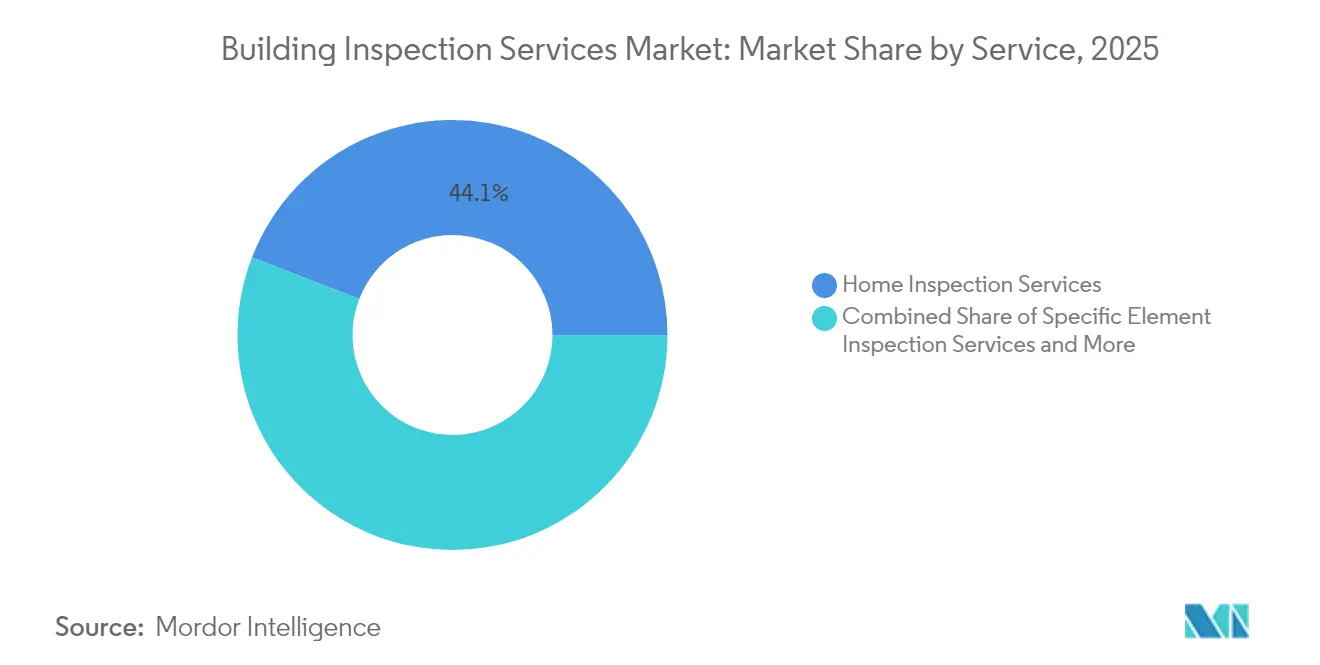

- By service, Home Inspection Services led with 44.12% of the building inspection services market share in 2025, whereas Other Specialised Services are projected to expand at an 8.74% CAGR through 2031.

- By sourcing type, In-House Services accounted for 56.21% of revenue in 2025, while Outsourced Services are forecast to grow at an 8.25% CAGR between 2026 and 2031.

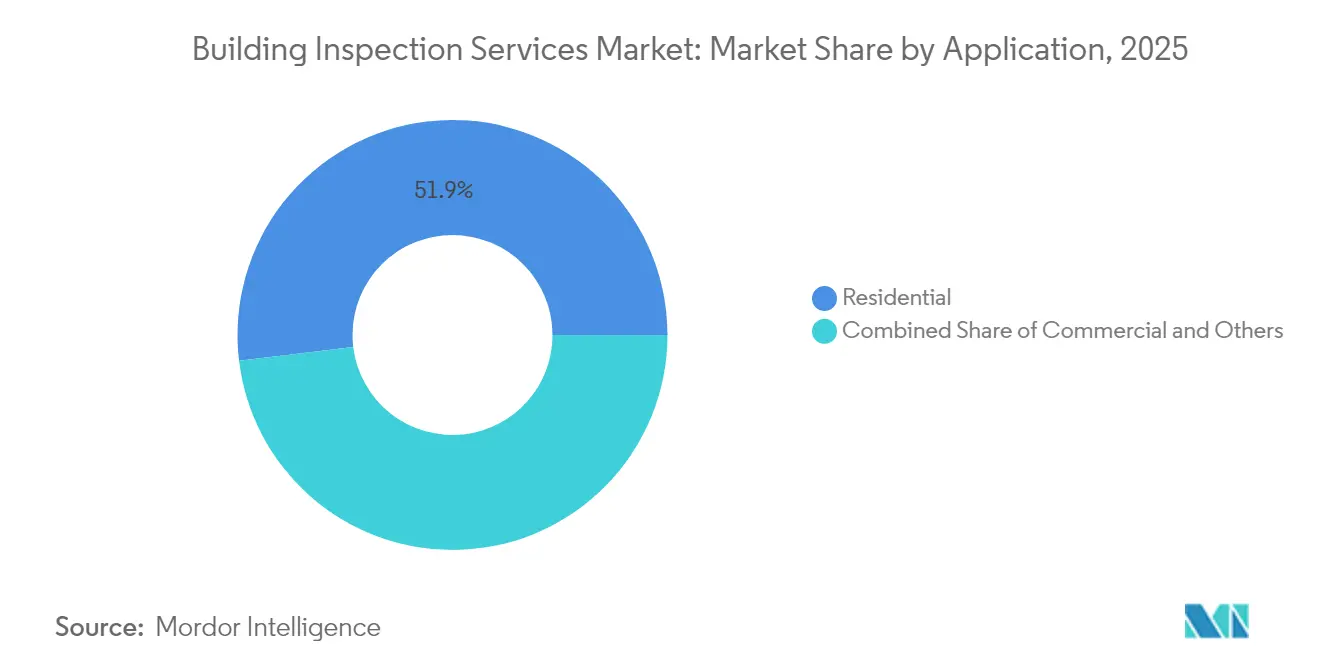

- By application, Residential accounted for 51.92% of the building inspection services market size in 2025, and Others (industrial, infrastructure, data centers) are poised for an 11.05% CAGR by 2031.

- By end user, Real-Estate Agencies & Brokers commanded 38.22% of revenue in 2025; Government & Municipalities represent the fastest expansion at 8.74% CAGR to 2031.

- By geography, North America remained the largest regional contributor in 2025, while Europe is projected to register the highest growth rate through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Building Inspection Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter building-safety regulations & codes | +2.1% | Global, led by EU and North America | Medium term (2-4 years) |

| Growing volume of real-estate transactions | +1.8% | Global, with concentration in North America & APAC | Short term (≤ 2 years) |

| Net-zero mandates driving energy-audit demand | +1.5% | EU leading, North America following | Long term (≥ 4 years) |

| Ageing building stock in OECD economies | +1.2% | North America & EU primarily | Long term (≥ 4 years) |

| Rapid uptake of drone-based aerial inspection | +0.9% | Global, early adoption in North America & EU | Short term (≤ 2 years) |

| AI-enabled defect analytics in smart buildings | +0.7% | APAC core, spill-over to North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Building-Safety Regulations & Codes

The 2024 International Building Code introduces tornado load metrics, higher wind-resistance thresholds, and universal carbon-monoxide detection, raising baseline inspection complexity[2]International Code Council, “2024 I-Code Suite,” iccsafe.org. Ontario eliminated 1,730 provincial code variations in 2024, streamlining compliance while keeping rigorous safety checks. California’s SB-721 requires deck inspections for multifamily properties by January 2025, generating a new niche for specialists. These policies increase the value of third-party inspection certificates and encourage continual professional development among providers.

Growing Volume of Real-Estate Transactions

Stabilizing mortgage rates are reviving housing turnover; the National Association of REALTORS projects a 9% increase in U.S. home sales during 2025.[3]National Association of REALTORS, “2025 Housing Market Forecast,” nar.realtor Canadian home sales advanced 10% in 2024 despite regulatory shifts that eased stress-test rules and raised insured mortgage caps. State legislation, such as the pending Massachusetts bill that disallows inspection waivers, underscores regulatory momentum for mandatory assessments. Commercial real-estate deals in data-center and renewable-energy assets add incremental inspection demand. The surge tightens capacity because certified inspectors remain in short supply, nudging service prices upward in tight local markets.

Ageing Building Stock in OECD Economies

Many North American and European structures exceed 30-year lifespans, demanding regular condition assessments that go beyond basic code compliance. The 2024 International Existing Building Code emphasizes cost-effective repair and alteration pathways, turning recurring inspections into a strategic asset-management tool. Australian studies show that proactive maintenance raises tenant satisfaction and property values, validating inspection ROI for owners. Non-destructive testing and predictive analytics allow owners to extend building life cycles without disruptive renovations.

Rapid Uptake of Drone-Based Aerial Inspection

Global drone inspection revenue is projected to hit USD 23 billion within three years as automated platforms slash cost and risk. Research shows median savings of USD 5,043 per bridge inspection when drones replace scaffolding and snooper trucks. AI-enabled platforms create 3D models, detect micro-cracks, and auto-populate defect logs, shortening report turnaround time. Privacy rules and flight-path approvals still limit residential use, but commercial and infrastructure owners embrace the technology for routine maintenance schedules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly fragmented provider landscape & price pressure | -1.4% | Global, most acute in North America | Short term (≤ 2 years) |

| Shortage of certified inspectors | -1.8% | Global, severe in North America & EU | Medium term (2-4 years) |

| Rising liability-insurance premiums | -0.6% | Global, led by North America | Short term (≤ 2 years) |

| Privacy concerns around drone/remote inspections | -0.4% | EU leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Highly Fragmented Provider Landscape & Price Pressure

Thousands of sole proprietors and small regional firms compete on commodity home inspection work, keeping average ticket prices flat in many U.S. metros. Private equity funds continue to consolidate niche providers, aiming to build national footprints with data-driven scheduling and cross-selling synergies. Despite ongoing deals, the top five firms still account for well under one-third of global revenue, so price competition remains intense for routine assignments. Operators differentiate by investing in specialized services such as energy auditing, façade safety certifications, and drone-enabled façade scans that command premium rates. Customers reward end-to-end platforms that blend on-site data capture with cloud-based analytics and digital report delivery.

Shortage of Certified Inspectors

Oregon reported a deficit of 115 residential inspectors in 2024, delaying permitting timelines for new housing starts. Certification pathways require classroom instruction, supervised field hours, and continuing education, making capacity expansion slow. The U.S. labor gap in construction trades exceeded 500,000 workers in 2024, increasing defect risks and potential liability claims. Rising professional liability premiums, 75% of underwriters raised rates by 5% in 2024, further squeezing independent contractors. Technology aids productivity, yet seasoned inspectors remain indispensable for final sign-offs under most codes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Specialization Drives Premium Growth

Home Inspection Services captured 44.12% of the building inspection services market share in 2025 as transaction-driven demand rebounded. Many U.S. states are revoking waiver clauses, so every residential deal now requires a certified report, lifting unit volumes. Commercial Building Inspection Services grew steadily because data center, logistics, and renewable-energy projects incorporate inspection milestones tied to financing schedules. The building inspection services market size for Other Specialised Services is projected to widen at an 8.74% CAGR, fueled by energy audits, drone surveys, and AI-enabled façade analytics.

Providers are bundling thermal imaging, blower-door testing, and carbon-intensity calculations to meet Europe’s zero-emission mandates. California’s deck safety checks and Denver’s mandatory ANSI/ASHRAE/ACCA 211-2018 Level 2 energy audits illustrate how niche regulations spark high-margin assignments. Firms that combine structural engineers with software developers create defensible competitive moats.

By Sourcing Type: Outsourcing Gains Momentum

In-house inspection teams retained 56.21% of revenue in 2025 because large real-estate owners and facility managers prefer direct oversight. Yet the building inspection services market size for Outsourced Services is projected to climb at an 8.25% CAGR through 2031 as codes grow more complex and technologies evolve rapidly. External specialists spread tech costs across a diverse client base, making high-resolution lidar or AI platforms affordable for mid-sized owners.

Insurers and lenders increasingly require third-party certifications to reduce conflict-of-interest exposure. The Co-operators’ 2024 acquisition of Carson Dunlop illustrates how insurance groups are vertically integrating to secure inspection expertise that handles more than 200,000 assignments annually. Outsourcing also mitigates labor shortages because national providers redeploy staff to hotspots, smoothing capacity imbalances.

By Application: Diversification Beyond Residential

Residential assets generated 51.92% of 2025 revenue, but the Others segment, which bundles industrial facilities, bridges, and data centers, is set to register the fastest 11.05% CAGR to 2031. Owners of hyperscale data centers demand real-time thermal mapping and computational fluid dynamics validation at each construction milestone. NV5 Global secured USD 14 million in 2024 contracts to deliver AI-driven MEP designs exceeding one gigawatt of capacity, underscoring non-residential momentum.

Infrastructure authorities adopt continuous health-monitoring sensors, translating into recurring subscriptions rather than one-time reports. This annuity model boosts average client lifetime value and insulates revenue from housing-cycle volatility. The building inspection services market continues to diversify as specialty engineers target petrochemical plants, water-treatment facilities, and offshore wind platforms.

By End User: Government Sector Emerges

Real estate Agencies & Brokers accounted for 38.22% of 2025 spend because agents rely on timely inspections to close deals. Government & Municipalities exhibit the highest 8.74% CAGR through 2031, propelled by infrastructure-upgrade programs and mandated performance standards. The U.S. Department of Housing and Urban Development’s NSPIRE framework standardizes physical inspections across public housing stock, creating predictable workstreams for qualified contractors.

Maryland’s Building Energy Performance Standards oblige owners of buildings above 35,000 ft² to submit annual energy data, reinforcing public-sector inspection pipelines. Insurers and lenders also commission inspections to calibrate underwriting models, and private-equity asset managers order deep-dive due diligence checks before portfolio acquisitions. Diverse end-user demand cushions providers against cyclical shocks in any single segment.

Geography Analysis

North America remained the largest regional contributor in 2025, underpinned by stringent codes, a high replacement rate for aging stock, and technology-friendly regulators. The 2024 International Building Code update, plus state ordinances such as California’s Title 24 revisions requiring solar and battery systems in new construction, expand inspection scope. The U.S. Department of Energy’s formal definition of a zero-emissions building sets uniform guidance that inspection firms must validate before occupancy permits are issued. Capacity constraints, exemplified by the Oregon inspector shortfall, keep utilization rates high and support pricing.

Europe is the fastest-growing market because the Energy Performance of Buildings Directive mandates zero-emission status for all new structures by 2030 and for public buildings by 2028. Minimum energy-performance standards force upgrades on the worst-performing 16% of the stock, unlocking steady retrofit inspection work. Enhanced Energy Performance Certificates and building-renovation passports embed inspection checkpoints through the asset lifecycle, creating multi-year revenue visibility. Providers with thermal-imaging drones and lifecycle-carbon calculators are winning cross-border frameworks.

Asia-Pacific is experiencing robust expansion led by infrastructure spending and smart-city initiatives. Japan’s construction output reached USD 609.27 billion in 2024 and is projected at USD 716.66 billion by 2029, sustaining demand for compliance verification and quality control. Bureau Veritas’ acquisition of Australia-based APP Group in 2024 strengthened its footprint across large-scale transport projects, illustrating the region’s consolidation trend. Disparate national codes still hamper cross-border standardization, but pan-regional clients favor firms that can navigate local requirements while deploying uniform digital platforms.

Note: Segments share of all individual segments available upon report purchase

Competitive Landscape

The building inspection services market is highly fragmented; the top five companies account for less than 30% of worldwide revenue, leaving ample space for regional challengers. Global TICC majors, including Bureau Veritas, SGS, and Intertek, use bolt-on acquisitions to add niche skills and fill geographic gaps. Bureau Veritas posted EUR 6,240.9 million in revenue in 2024, up 6.4% year-over-year, and completed 10 deals that expanded its Buildings & Infrastructure practice. These platforms leverage centralized R&D to deploy AI crack-detection modules and cloud-based reporting across diverse markets.

Mid-cap specialists pursue technology differentiation. NV5 Global finalized multiple buys in geospatial and fire-protection engineering to create bundled service lines that integrate lidar collection, computational fluid-dynamics modeling, and life-safety design. Acuren Corporation’s planned merger with NV5 will form a USD 2 billion revenue entity with a projected USD 350 million adjusted EBITDA, highlighting investor appetite for scale efficiencies in inspection and engineering. Firms such as Mistras Group apply acoustic-emission sensors for continuous structural monitoring, converting episodic inspections into subscription contracts.

Start-ups focus on AI analytics, leveraging high-resolution imagery from drones and fixed sensors to generate automated compliance dashboards. Venture investment favors SaaS-enabled inspection models that promise rapid scalability with modest field staff additions. However, rigorous accreditation requirements and rising liability insurance premiums create hurdles to market entry. Strategic partnerships between software developers and established inspection firms are emerging as a pragmatic route to combine domain expertise with cutting-edge algorithms.

Building Inspection Services Industry Leaders

Amerispec Inspection Services

HouseMaster

National Property Inspections

Pillar to Post

WIN Home Inspection

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bureau Veritas reported 2024 revenue of EUR 6,240.9 million (6.4% growth) and closed 10 acquisitions under its LEAP|28 strategy.

- January 2025: Acuren Corporation and NV5 Global announced a merger creating a global TICC and engineering firm with over USD 2 billion combined revenue and projected USD 350 million adjusted EBITDA, pending approvals.

- December 2024: NV5 Global agreed to acquire Global Fire Protection Group, expanding recurring fire-safety engineering services across North America.

- November 2024: Bureau Veritas signed to acquire The APP Group, deepening Buildings & Infrastructure capabilities in Asia-Pacific.

Global Building Inspection Services Market Report Scope

The building inspection services market consists of the sales of building inspection services by entities (organizations, sole traders, and partnerships) that evaluate all aspects of the building structure and component systems and prepare a report on the physical condition of the property, generally for buyers or others involved in real estate transactions. The Global building inspection services market is segmented by Service (Home Inspection Services, Specific Element Inspection Services, Commercial Building Inspection Services, and Others), by Application (Residential, Commercial, and Others), by Sourcing Type (In-House Services and Outsourced Services) and by Geography. The report offers market size and forecasts for the Global building inspection services market in value (USD Billion) for all the above segments. The report also covers the impact of COVID -19 on the market, technological trends, market dynamics, etc.

| Home Inspection Services |

| Specific Element Inspection Services |

| Commercial Building Inspection Services |

| Other Specialised Services |

| In-House Services |

| Outsourced Services |

| Residential |

| Commercial |

| Others |

| Real-Estate Agencies & Brokers |

| Property Owners & Investors |

| Government & Municipalities |

| Insurance & Financial Institutions |

| Facility-Management Firms |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific |

| By Service | Home Inspection Services | |

| Specific Element Inspection Services | ||

| Commercial Building Inspection Services | ||

| Other Specialised Services | ||

| By Sourcing Type | In-House Services | |

| Outsourced Services | ||

| By Application | Residential | |

| Commercial | ||

| Others | ||

| By End User | Real-Estate Agencies & Brokers | |

| Property Owners & Investors | ||

| Government & Municipalities | ||

| Insurance & Financial Institutions | ||

| Facility-Management Firms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the building inspection services market in 2026?

It is valued at USD 10.47 billion in 2026 and is projected to reach USD 14.84 billion by 2031.

Which service category holds the biggest share of the building inspection services market?

Home Inspection Services led with 44.12% of revenue in 2025.

What is the fastest-growing segment in the building inspection services market?

Other Specialised Services, including energy audits and drone inspections, is forecast to expand at an 8.74% CAGR through 2031.

Which region is expected to grow the quickest?

Europe will post the highest regional CAGR as the EU enforces zero-emission building mandates.

How are drones influencing the building inspection services industry?

Drone-enabled surveys cut median inspection costs by more than USD 5,000 per assignment and improve safety by removing personnel from hazardous locations.

Why is the shortage of certified inspectors a concern?

Labor gaps delay permitting and raise liability exposure; Oregon alone reported a deficit of 115 inspectors in 2024, reflecting wider North American constraints.

Page last updated on: