United Arab Emirates Data Center Storage Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

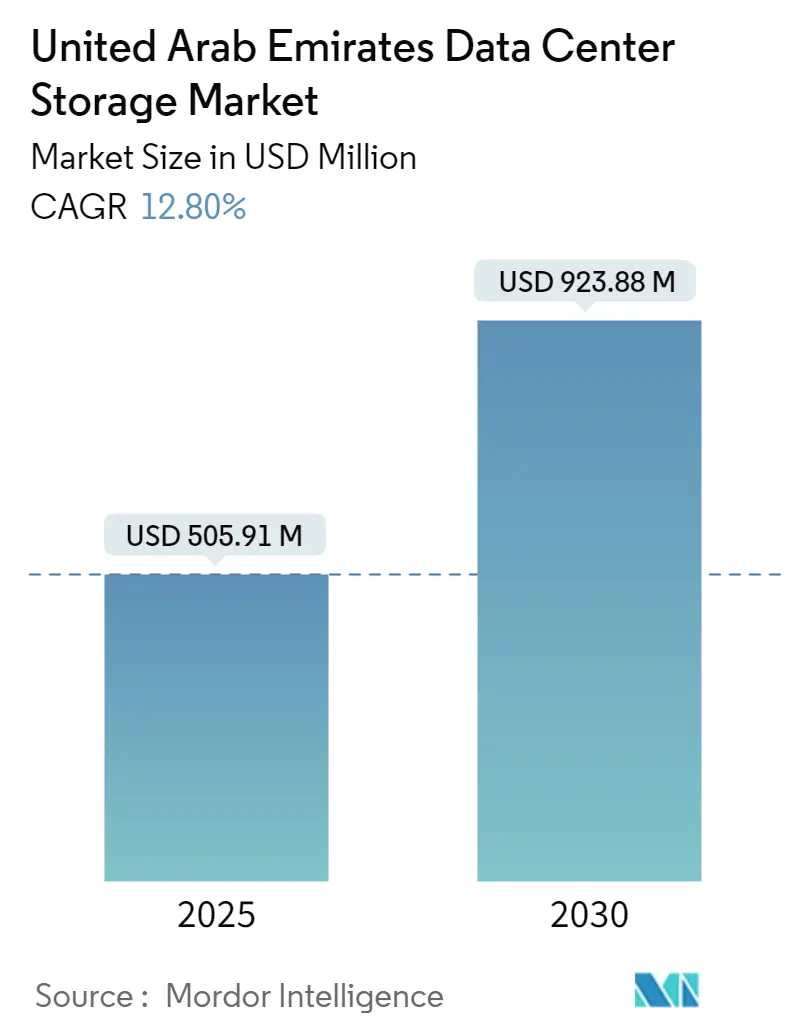

| Market Size (2025) | USD 505.91 Million |

| Market Size (2030) | USD 923.88 Million |

| Growth Rate (2025 - 2030) | 12.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Data Center Storage Market Analysis by Mordor Intelligence

The United Arab Emirates data center storage market size is expected to be valued at USD 505.91 million in 2025 and is forecast to advance to USD 923.88 million by 2030, registering a 12.8% CAGR. This growth trajectory confirms the country’s status as a regional digital hub that connects Asia, Europe, and Africa, while reinforcing the strategic goal of national data sovereignty set out in UAE Vision 2071 u.ae. Government-led diversification away from hydrocarbons, combined with rising enterprise investments in cloud, analytics, and artificial intelligence workloads, amplifies demand for dependable, high-performance storage capacity. Cooling-efficient facilities, strong subsea cable connectivity, and well-defined free-zone incentives continue to attract global hyperscalers that need local residency for regulated data categories. At the same time, emerging edge sites in industrial zones help oil and gas operators process sensor data closer to the point of generation, reducing latency and backhaul costs. The net effect is a layered storage demand curve that ranges from metro-scale colocation halls to compact, ruggedized edge appliances, each adding momentum to the United Arab Emirates data center storage market.

Key Report Takeaways

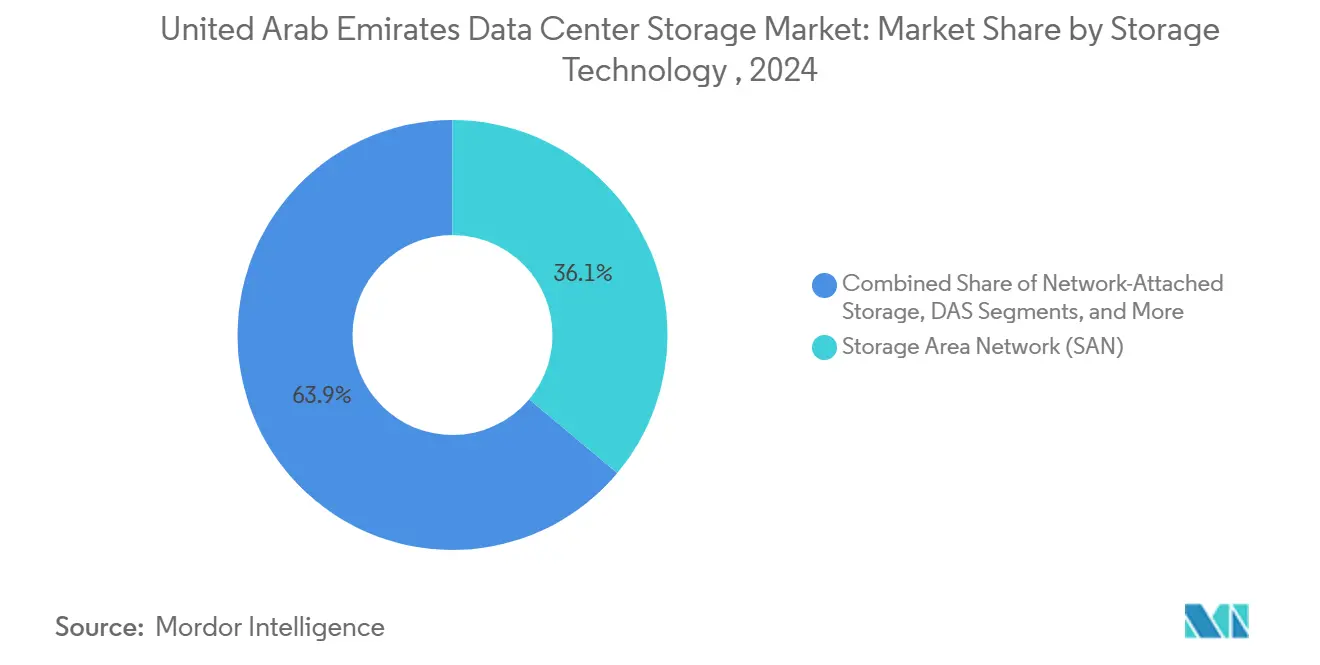

- By storage technology, Storage Area Network held 36.1% of the United Arab Emirates data center storage market size in 2024, whereas Network Attached Storage is projected to grow at a 12.9% CAGR through 2030.

- By storage type, traditional HDD arrays accounted for 42.3% of the United Arab Emirates data center storage market size in 2024, while all-flash arrays are on track for a 14.2% CAGR to 2030.

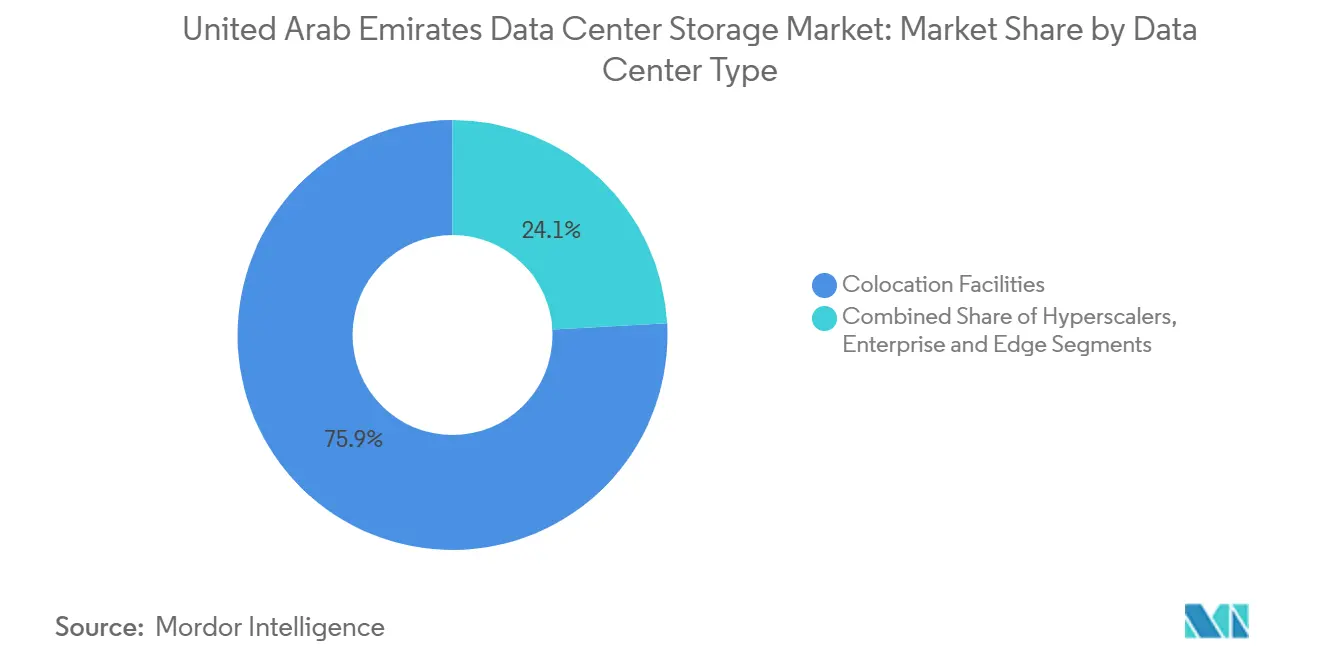

- By data center type, colocation facilities led with 45.6% of the United Arab Emirates data center storage market size in 2024; hyperscalers and cloud service providers are forecast to grow the fastest at 14.5% CAGR.

- By end user, the IT and telecommunications segment captured 24.5% of the United Arab Emirates data center storage market size in 2024, and BFSI is expected to expand at a 13.1% CAGR through 2030.

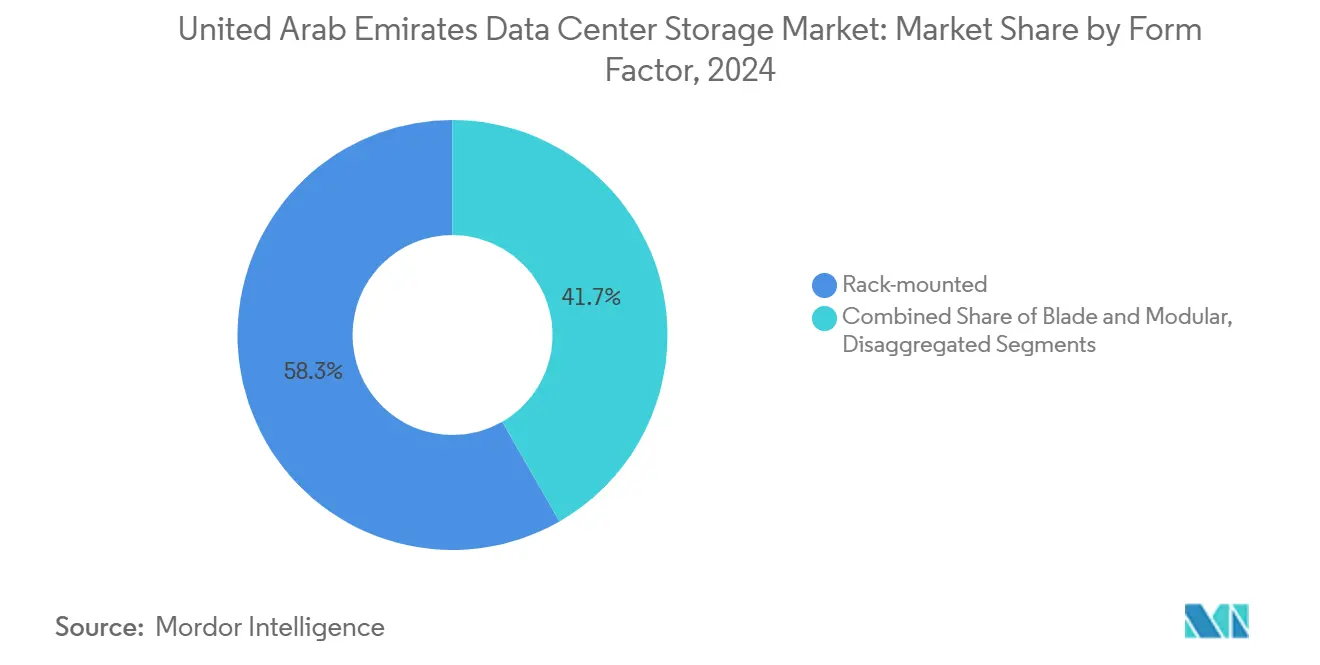

- By form factor, rack-mounted systems dominated with 58.3% of the United Arab Emirates data center storage market size in 2024, while composable storage shows an 11.7% CAGR outlook.

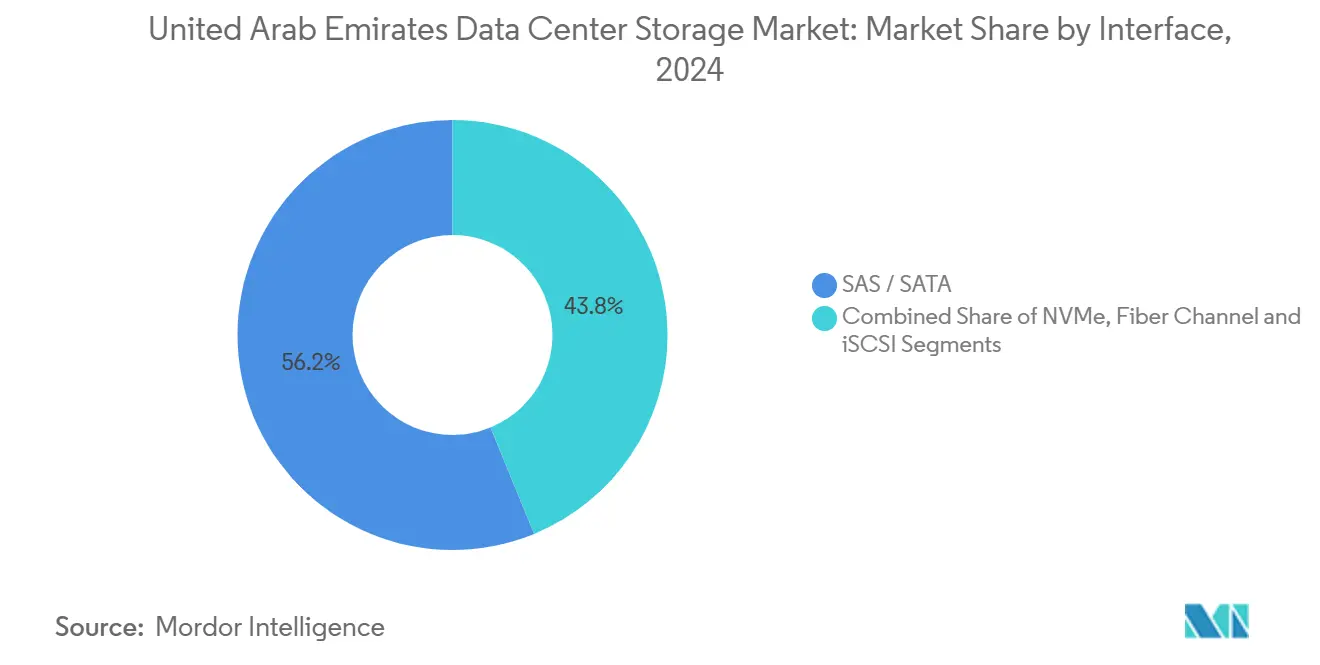

- By interface, NVMe is the fastest-rising protocol with a 14.8% CAGR to 2030, although SAS/SATA connections still hold 56.2% of the United Arab Emirates data center storage market size in 2024.

United Arab Emirates Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing digitalization and data-centric applications | +3.2% | UAE national, with concentration in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Evolution of hybrid flash arrays | +2.8% | UAE national, particularly enterprise corridors | Short term (≤ 2 years) |

| Nationwide smart city / 5G roll-outs boosting data volume | +2.1% | UAE national, with early deployment in major emirates | Long term (≥ 4 years) |

| Enterprise cloud and hybrid-cloud adoption surge | +2.4% | UAE national, with spillover to GCC region | Medium term (2-4 years) |

| Stringent UAE data-localization compliance | +1.8% | UAE national, with regulatory precedent for GCC | Long term (≥ 4 years) |

| Edge data-center buildouts in oil and gas corridors | +1.3% | UAE national, concentrated in industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Digitalization and Data-Centric Applications

Federal cloud-first directives spark continuous growth in structured and unstructured data volumes, especially within government and financial services. The Mohammed bin Rashid Innovation Fund’s USD 2 billion pool earmarked for digital infrastructure encourages private-sector alignment with national technology priorities.[1]Mohammed bin Rashid Innovation Fund, “Fund Overview,” mbrif.aeIslamic banking workflows, which require immutable audit trails to meet Sharia compliance, add unique object-storage demand. As artificial intelligence pilots move into production, enterprises increasingly pair AI inference clusters with high-throughput storage platforms, straining legacy architectures and accelerating refresh cycles across the United Arab Emirates data center storage market.

Evolution of Hybrid Flash Arrays

Hybrid flash arrays resonate with UAE enterprises that weigh performance against power and cooling overheads. Automated tiering moves hot data to flash and colder data to disk without human intervention, cutting service tickets by almost 60%, according to regional systems integrators. The approach reduces downtime risk in a country where 24/7 online services have become the norm, sustaining momentum in the United Arab Emirates data center storage market.

Nationwide Smart City/5G Roll-outs Boosting Data Volume

Smart lampposts, connected traffic controls, and environment sensors in Dubai and Abu Dhabi generate terabytes of real-time data that must be ingested locally while archived centrally for trend analytics. Autonomous vehicle field tests further stretch capacity planning. These use-cases prompt operators to deploy multi-tier storage architectures spanning edge nodes and core facilities, reinforcing demand across the United Arab Emirates data center storage market.

Enterprise Cloud and Hybrid-Cloud Adoption Surge

Seventy-three percent of large UAE enterprises now run multi-cloud strategies, blending global hyperscale capacity with on-premises stacks. Storage platforms therefore need seamless data mobility, consistent policy enforcement, and unified management panes. Vendors that excel at software-defined storage orchestration gain an edge as organizations modernize without breaching UAE data-localization statutes enforced by the Telecommunications and Digital Government Regulatory Authority.[2]Telecommunications and Digital Government Regulatory Authority, “Data Localization Guidelines 2024,” tdra.gov.ae

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compatibility and optimum-performance issues | -1.4% | UAE national, particularly affecting legacy enterprise environments | Short term (≤ 2 years) |

| High upfront CAPEX and TCO for flash arrays | -2.1% | UAE national, with particular impact on SME adoption | Medium term (2-4 years) |

| Shortage of advanced storage-virtualization talent | -1.8% | UAE national, with spillover effects across GCC | Long term (≥ 4 years) |

| Cooling-water scarcity inflating OPEX in desert climate | -1.6% | UAE national, concentrated in inland data center locations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and TCO for Flash Arrays

All-flash platforms can cost 3-4 times more than disk-based systems at purchase, a challenge for SMEs that operate on tight budgets. Financing options remain narrow compared with conventional assets, prompting procurement teams to extend disk refresh cycles. Although flash drives lower long-term power expense, initial sticker shock constrains some buyers, moderating adoption across portions of the United Arab Emirates data center storage market.

Cooling-Water Scarcity Inflating OPEX in Desert Climate

Cooling can account for 40% of total data-center operating expenses, and open-loop systems can consume 1.5 liters of water per kWh of IT load. Government conservation targets add scrutiny, amplifying pressure on operators to deploy closed-loop or liquid-immersion technologies that carry higher capital costs.[3]Emirates Water and Energy Company, “Water Use in Critical Infrastructure 2024,” ewec.ae The resulting financial burden can deter smaller entrants from expanding footprints within the United Arab Emirates data center storage market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: NAS Ascends While SAN Retains Core Stronghold

SAN systems commanded 36.1% United Arab Emirates data center storage market share in 2024, owing to entrenched installations in banking and federal agencies that demand ultra-low latency and redundant pathways. NAS, however, posts the highest growth curve at 12.9% CAGR through 2030. Many UAE enterprises prefer Ethernet-based NAS because it sidesteps the scarcity of Fibre Channel expertise. NVMe-over-TCP upgrades now allow NAS to emulate SAN-like responsiveness, encouraging IT teams to migrate mission-critical volumes without overhauling entire fabrics. Distributed file protocols also support cloud bursting, aligning with hybrid goals prevalent across the UAE data center storage industry. Direct-attached storage remains indispensable at remote oil-field and utilities sites where WAN links can be intermittent, ensuring real-time processing despite sporadic connectivity. Tape and object systems complete the tier for archival compliance, especially among Islamic finance institutions that mandate immutable storage.

SAN’s resilience originates from historical capex already sunk into Fibre Channel switches and host bus adapters. Nonetheless, suppliers now bundle SAN controllers capable of presenting block and file services simultaneously, giving customers phased migration routes toward flexible NAS estates. Vendors that articulate smooth roadmaps without forklift upgrades are well-positioned to grow wallet share inside the United Arab Emirates data center storage market.

By Storage Type: Flash Momentum Gains Against HDD Persistence

Traditional hard-disk arrays held 42.3% of United Arab Emirates data center storage market size in 2024, a testament to their cost-per-terabyte advantage for seldom-accessed datasets. All-flash arrays lead the growth ranking at 14.2% CAGR to 2030, driven by AI inference, real-time analytics, and high-frequency trading tasks. Flash’s power draw is lower than disk, trimming cooling bills by roughly 30%, a welcome relief in desert conditions. Although purchase prices remain higher, falling NAND costs narrow the gap yearly. Hybrid arrays that integrate SSD tiers with bulk SATA drives offer a transitional platform, automating cold-data demotion and keeping capex in check. Such balance resonates with procurement teams mandated to minimize total cost of ownership while chasing performance SLAs, cementing hybrid arrays as a bridge technology across the United Arab Emirates data center storage market.

By Data Center Type: Colocation Stability Meets Hyperscaler Velocity

Colocation halls delivered 45.6% United Arab Emirates data center storage market share in 2024, favored by enterprises that want physical control but outsource facility management. Hyperscaler and cloud-service-provider footprints, although smaller, are growing at a 14.5% CAGR, accelerated by regional expansion plans from Amazon Web Services, Microsoft Azure, and Alibaba Cloud. These hyperscalers cater to multi-national clients that must satisfy residence rules yet interface with global workloads. Government departments, BFSI, and healthcare agencies continue to mix strategies, blending on-premises equipment in regulated domains with leased capacity for burstable analytics. Edge and micro-data centers emerge in petrochemical corridors, where ruggedized racks withstand heat and vibration. Each model feeds incremental demand into the United Arab Emirates data center storage market.

By End User: BFSI Surges Ahead of Telecommunications Anchor

IT and telecommunications players held 24.5% share in 2024, underpinned by network modernization and 5G backhaul requirements. Banking, financial services, and insurance sectors will grow the quickest at 13.1% CAGR. Digital-only banks, Sharia-compliant products, and cross-border payments engines all require persistent, low-latency storage that supports encryption and tamper-proof logging. Government smart-city dashboards, public-sector e-services, and national ID databases generate mixed workloads that straddle transactional and analytical demands. Medical tourism initiatives boost imaging and electronic health records, widening the technology footprint in hospitals. Manufacturing adds steady though smaller increments as factories integrate Industry 4.0 sensors. Collectively, these diverse verticals fortify the United Arab Emirates data center storage market.

By Form Factor: Composable Rises Beside Rack-Mounted Mainstay

Rack-mounted platforms represented 58.3% United Arab Emirates data center storage market share in 2024 because they fit existing cabinets and airflow patterns. Disaggregated or composable architectures, where storage pools can be dynamically carved and reassembled, are tracking 11.7% CAGR. They appeal to cloud-native developers who want API-driven infrastructure that scales granularly. Blade and modular enclosures occupy high-density colocation suites where square-meter pricing in central Dubai is premium. Meanwhile, hyperconverged appliances blur form-factor boundaries by embedding storage and compute in the same chassis, simplifying operations for mid-tier enterprises eager to consolidate vendors. These overlapping trends create a diversified equipment mix within the United Arab Emirates data center storage market.

By Interface: NVMe Fast-Tracks Modern Workloads

SAS/SATA held 56.2% share in 2024 thanks to existing disk arrays and moderate-performance SSDs that employ legacy connectors. NVMe protocol adoption is accelerating at a 14.8% CAGR because it harnesses PCIe lanes directly, bypassing SCSI overhead. Financial institutions running real-time fraud detection and AI developers training language models welcome the latency reductions afforded by NVMe. NVMe-over-Fabrics extends these benefits across Ethernet and Fibre Channel networks, letting administrators link flash shelves over distances without sacrificing throughput. Fibre Channel and iSCSI remain relevant for specific backup and archival layers yet face gradual displacement as organizations modernize. Interface upgrades therefore represent a potent catalyst within the United Arab Emirates data center storage market.

Geography Analysis

Dubai anchors the United Arab Emirates data center storage market through its status as a global finance and logistics hub. Colocation campuses in Dubai Internet City and Jebel Ali Free Zone host multinational corporates that require sub-millisecond access to Middle East consumer traffic. Abu Dhabi contributes strategic depth by housing federal ministries, defense research, and sovereign-wealth investment entities that mandate sensitive data residency. Both emirates intertwine submarine cable landing sites with terrestrial fiber loops, ensuring high-availability routes toward Europe, India, and East Asia. Secondary emirates—Sharjah, Ras Al Khaimah, and Fujairah, are witnessing new industrial parks where oil, gas, and manufacturing operators deploy localized edge clusters. These remote deployments enlarge the physical scope of the United Arab Emirates data center storage market and facilitate compliance with provincial environmental regulations.

National data-sovereignty laws dictate that critical health, financial, and personal data stay inside the country, so hyperscalers have invested in in-country availability zones. This requirement crates hybrid topologies in which replicated volumes remain in Emirates-based vaults even when applications burst into overseas instances for compute elasticity. The United Arab Emirates data center storage market therefore benefits from both inward and outward traffic flows: regional users rely on UAE sites for low-latency services, while international firms leverage Emirates nodes to reach wider Gulf Cooperation Council audiences.

Competitive Landscape

The United Arab Emirates data center storage market exhibits moderate consolidation. Dell Technologies, Hewlett Packard Enterprise, and NetApp hold entrenched positions through multi-year enterprise agreements and certified local service centers. Pure Storage and Nutanix disrupt by promoting software-defined architectures that lower lock-in risk and enable granular upgrades. Huawei, Lenovo, and Cisco use joint ventures with domestic system integrators to navigate procurement preferences that favor technology transfer and Emirati talent development. Vendors differentiate through pre-validated reference designs tailored to desert climates, including dust-filtering bezels and elevated thermal thresholds.

Strategic priorities cluster around hybrid models that blend on-premises hardware with cloud tiering. Suppliers bundle toolsets for automatic data classification, encryption, and replication across hyperscale endpoints. Edge-to-core convergence is another battleground; ruggedized flash arrays certified for 55 °C ambient operations cater to oil rigs and solar farms. Meanwhile, white-box entrants pursue niche projects where commodity hardware hosts open-source storage stacks, offering cost-effective choices for SMEs. While price sensitivity influences initial selection, long-term service quality and regulatory compliance seal repeat contracts within the United Arab Emirates data center storage market.

United Arab Emirates Data Center Storage Industry Leaders

Dell Technologies

Hewlett Packard Enterprise

NetApp

NetApp

NetApp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Dell Technologies announced a USD 150 million expansion of its regional manufacturing facility in Dubai, focusing on PowerStore and Unity systems optimized for desert operations.

- February 2025: Pure Storage set up a joint venture in Abu Dhabi with Advanced Technology Investment Company to localize FlashArray assembly and skills development.

- January 2025: HPE secured a USD 200 million contract with Dubai Municipality to supply edge and core storage for the city’s smart-city program.

- December 2024: NetApp opened a regional cloud operations center in Dubai Internet City to support hybrid deployments and offer in-country data residency.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Arab Emirates data-center storage market as the value generated inside UAE facilities by purpose-built hardware, enclosures, and system software that store, manage, protect, and retrieve digital data for enterprise, colocation, hyperscale, and edge workloads. Solutions covered span SAN, NAS, DAS, object, and tape systems across HDD, SSD, and hybrid media.

Scope exclusion: Temporary on-premise disaster-recovery rentals and standalone consumer external drives are not considered.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Primary Research

Conversations with data-center operators, storage architects, and channel partners across Dubai, Abu Dhabi, and Sharjah validated utilization rates, refresh cycles, and NVMe adoption. Follow-up surveys with BFSI and telecom buyers refined price tiers and capacity mix, enabling us to reconcile secondary signals with ground reality.

Desk Research

Mordor analysts began with macro indicators from sources such as the UAE Telecommunications and Digital Government Authority, Dubai Statistics Center, and UN Comtrade to size data traffic, import volumes, and equipment ASP shifts. We then reviewed white papers from the Open Compute Project, trade data from Volza for storage chassis shipments, and patent trends via Questel to capture technology diffusion. Company filings, investor decks, and reputable press helped cross-check vendor unit placements. This list is illustrative; several other public and paid sources informed our evidence base.

Market-Sizing & Forecasting

A top-down build starts with installed MW capacity and average gigabytes per watt, which are then linked to storage attach-rate assumptions. Results are stress-tested through selective bottom-up cross-checks, supplier roll-ups, and sampled ASP × volume before adjustments. Key variables include 5Gsubscriber growth, flash cost per GB, hyperscale floor-space additions, data-sovereignty compliance milestones, and edge site count. Multivariate regression, supported by expert consensus, projects how each driver affects capacity and value through 2030. Gap areas in bottom-up inputs (e.g. private upgrades) are bridged using normalized ratios from comparable sites.

Data Validation & Update Cycle

Outputs undergo variance checks against historical shipments, analyst peer review, and anomaly flags. Reports refresh every twelve months, with mid-cycle updates if material events, large capex, or policy shifts alter baseline assumptions. Before delivery, an analyst performs a fresh pass so clients receive the latest viewpoint.

Why Mordor's United Arab Emirates Data Center Storage Baseline Commands Reliability

Published figures often differ because firms choose distinct scope lines, refresh cadences, and price-mix assumptions.

Key gap drivers include whether flash software licenses are booked, how colocation upgrades are counted, and the frequency at which exchange-rate resets flow into models. Mordor's page reflects quarterly ASP sampling and a study period fixed to 2019-2030, while several peers rely on blended infrastructure ratios or one-off surveys.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 505.9 M (2025) | Mordor Intelligence | - |

| USD 448 M (2024) | Global Consultancy A | Excludes object storage and uses biennial refresh, leading to lower total value |

| USD 256.5 M (2023) | Industry Association B | Captures only enterprise on-prem systems; omits colocation and flash premium, understating market |

Taken together, the comparison shows that Mordor's disciplined scope, annually refreshed inputs, and dual-track validation furnish decision-makers with a balanced, traceable baseline they can rely on when budgeting capacity or courting investors.

Key Questions Answered in the Report

What is the current value of the UAE data center storage market?

The UAE data center storage market size is USD 505.91 million in 2025.

How fast is the market expected to grow?

It is projected to register a 12.8% CAGR, taking value to USD 923.88 million by 2030.

Which storage technology is growing the quickest?

Network Attached Storage is the fastest-growing technology segment, advancing at a 12.9% CAGR through 2030.

How do UAE data-localization rules influence storage investment?

Regulations that mandate in-country residency of sensitive data push both local enterprises and global hyperscalers to expand UAE-based storage capacity and adopt hybrid architectures for compliance.

Page last updated on: