Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

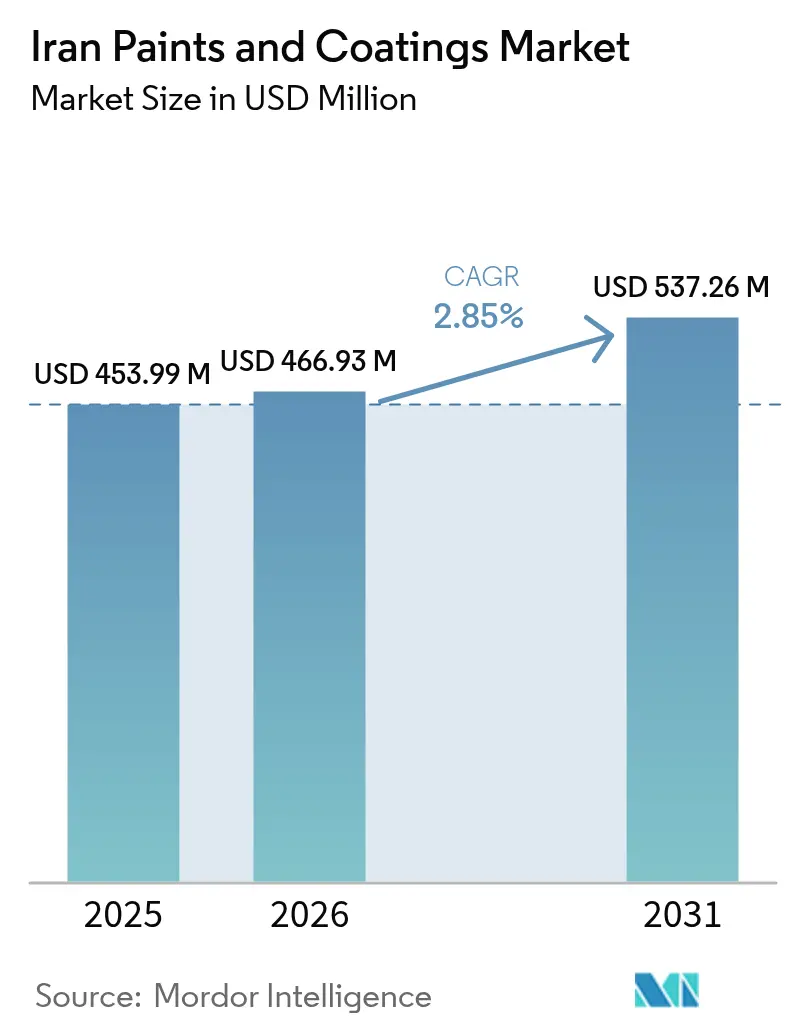

| Base Year Market Size (2025) | USD 453.99 Million |

| Market Size (2026) | USD 466.93 Million |

| Market Size (2031) | USD 537.26 Million |

| Growth Rate (2026 - 2031) | 2.85% CAGR |

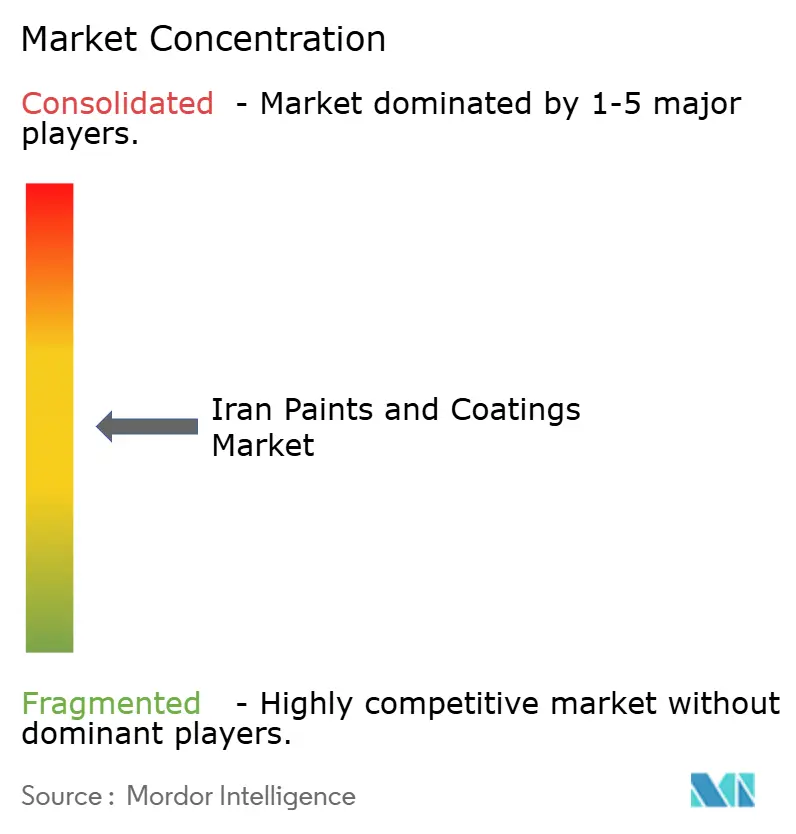

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iran Paints And Coatings Market Analysis by Mordor Intelligence

The Iran Paints And Coatings Market size was valued at USD 453.99 million in 2025 and estimated to grow from USD 466.93 million in 2026 to reach USD 537.26 million by 2031, at a CAGR of 2.85% during the forecast period (2026-2031). Demand resilience reflects a mix of state-led housing initiatives, feedstock cost advantages from the domestic petrochemical chain, and rising technical specifications in heritage and industrial maintenance coatings. Foreign investors committed USD 900 million to Iran’s chemicals and polymers sector in 2024-2025, signaling confidence in downstream processing despite sanctions-related headwinds. The market continues to benefit from acrylic and polyurethane resin integration, while compliance with Iran’s National Clean-Air Law accelerates a gradual shift toward water-borne technologies. Energy supply vulnerabilities that surfaced during the December 2024 nationwide industrial shutdown underscore the importance of operational diversification and efficiency upgrades.

Key Report Takeaways

- By resin type, acrylic resins accounted for 34.85% of Iran paints and coatings market size in 2025, while polyurethane resins represent the fastest-growing category with a 2.91% CAGR to 2031.

- By technology, solvent-borne formulations retained 64.40% revenue share in 2025; water-borne technologies are expanding at a 3.09% CAGR to 2031.

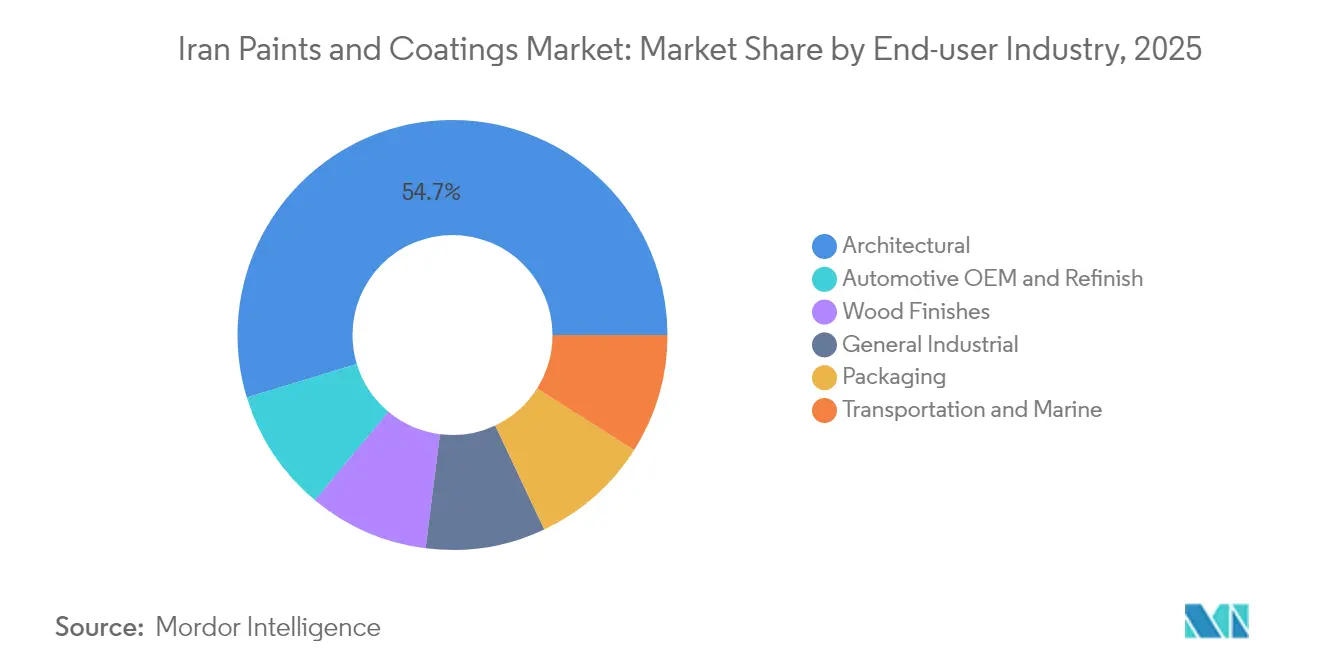

- By end-user industry, architectural applications held 54.70% of Iran paints and coatings market share in 2025, whereas automotive OEM and refinish coatings are forecast to advance at a 3.00% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iran Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government housing-led construction boom | +0.8% | National; Tehran, Isfahan, Shiraz | Medium term (2-4 years) |

| Surge in furniture exports to Iraq and Turkey | +0.3% | Border provinces, export zones | Short term (≤ 2 years) |

| Petrochemical feedstock cost advantage | +0.5% | Khuzestan, Fars petrochemical hubs | Long term (≥ 4 years) |

| Domestic nano-coating research and development for conservation | +0.2% | Tehran, Isfahan, Shiraz heritage sites | Long term (≥ 4 years) |

| Energy-efficiency upgrades for public assets | +0.4% | Nationwide government facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Housing-Led Construction Boom

State policy aims to deliver 1 million new housing units annually, sustaining baseline demand for architectural coatings across Iran’s largest cities. The 25th International Building Industry Exhibition attracted over 490 domestic exhibitors in August 2025, reflecting robust engagement between material suppliers and developers. Urbanization pressures combined with inflation-hedging behavior have elevated residential renovation activity, bolstering repaint cycles. While traditional masonry techniques prevail, interest in drywall systems and specialized interior finishes is gradually rising, creating educational opportunities for paint formulators and applicators. Continuation of the program hinges on controlling inflation and managing raw-material import costs denominated in foreign currency.

Surge in Furniture Exports to Iraq and Turkey

Greater furniture shipments are stimulating demand for performance wood coatings. Historic trade corridors facilitate outbound logistics, while localized research and development has enhanced adhesion and durability of beech, poplar, and fir substrates via nanosilver-assisted heat treatments. Compliance with importing countries’ emission standards is a prerequisite for sustained export growth. Opportunities center on low-formaldehyde clear coats and traditional decorative finishes aligned with Middle Eastern consumer preferences. Export obstacles include sanctions-related payment restrictions and limited domestic access to certain high-grade additives.

Petrochemical Feedstock Cost Advantage

Iran’s abundant ethane and condensate streams allow ethylene production costs near USD 110 per ton, roughly half European levels, underpinning competitive pricing for acrylic and polyethylene-based resins. Commissioning of the Setare Khalij Fars refinery is expected to raise naphtha and LPG supply for downstream units, further lowering variable costs for domestic coatings producers. However, allocation priorities occasionally shift toward export-oriented petrochemicals, pressuring local formulators during tight supply windows. Sanctions that curtail overseas sales can conversely redirect feedstock inward, temporarily easing pricing but limiting access to new equipment and catalysts.

Growth of Domestic Nano-Coating Research and Development for Heritage Conservation

Iranian universities and start-ups have produced hydrophobic titania–silica and bio-based nanocrystalline coatings suited to preserving historic tile and stone façades. Laboratory success has translated into pilot-scale commercialization with institutional backing from the Iran Nanotechnology Initiative Council, which supports 130+ companies nationwide. Successful heritage projects establish credibility for broader industrial applications such as anti-corrosive or self-cleaning façade paints. The niche nature of conservation limits immediate volume but yields premium margins and technology spillovers into mainstream product lines.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating U.S./EU sanctions on petrochemicals | -0.6% | Country-wide, import-dependent producers | Short term (≤ 2 years) |

| Stringent VOC and HAP limits under National Clean-Air Law | -0.4% | Major urban and industrial zones | Medium term (2-4 years) |

| Shortage of high-purity pigments and additives | -0.3% | Premium formulation facilities nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating U.S./EU Sanctions on Petrochemicals

Renewed sanctions restrict the import of titanium dioxide, specialty additives, and modern dispersion equipment, complicating high-performance formulation work. Secondary sanctions deter European suppliers from even non-restricted transactions, forcing Iranian manufacturers toward alternative Asian sources that may entail longer lead times and variable quality[1]U.S. Department of the Treasury, “Sanctions List Search,” treasury.gov. Banking hurdles elevate transaction costs, while limited access to state-of-the-art QC instrumentation hampers process optimization. Larger firms are partially insulated via diversified sourcing strategies, but small and medium producers face margin compression.

Stringent VOC and HAP Limits Under National Clean-Air Law

Iran monitors air quality at more than 200 stations, and PM2.5 readings exceeding WHO guidelines are driving regulators to tighten solvent-usage thresholds. Compliance necessitates water-borne or high-solids alternatives, demanding capital investment in resin synthesis, emulsification, and bake-oven modifications. Enforcement varies by province, creating uneven competitive pressure. International brands operating local plants must often meet dual standards, complicating supply chain planning. Smaller domestic players risk fines or market exclusion if they cannot upgrade in time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Reflects Feedstock Integration

Acrylic resins commanded 34.85% of Iran paints and coatings market share in 2025 thanks to low-cost ethylene feedstock derived from national gas resources. Polyurethane resins, while a smaller slice, are expanding at a 2.91% CAGR on the strength of oil-and-gas pipeline protection systems that exploit quick-cure polyurea chemistries. Pricing volatility in titanium dioxide and other pigments has pressured all resin categories, but acrylic formulations benefit from in-house monomer access that cushions cost spikes. The Iran paints and coatings market size accruing to polyurethane is poised to rise as local research institutes refine continuous water-borne polyurethane processes that meet both performance and VOC criteria.

Domestic producers are investing in alkyd upgrades to serve mid-tier architectural clients, while epoxy and polyester systems cater to marine, powder-coating, and industrial metal finishing lines. Emerging silicone and fluoropolymer blends serve aerospace and chemical-resistant niches, although uptake is limited by equipment constraints and premium raw-material costs. Certification under ISO 9001:2015 is becoming standard for resin suppliers targeting export- oriented OEMs.

By Technology: Water-Borne Transition Accelerates Despite Solvent-Borne Dominance

Solvent-borne coatings retained 64.40% value share in 2025, reflecting entrenched production lines and applicator familiarity. Nonetheless, water-borne systems are advancing at a 3.09% CAGR, propelled by Clean-Air compliance deadlines and rising consumer awareness of indoor air quality. Domestic surfactant and coalescent manufacture supports the cost-structure shift, reducing dependence on imported solvent packages. The Iran paints and coatings market size allocated to water-borne chemistries will broaden as urban enforcement tightens and as government procurement favors low-VOC products.

High-solids and powder coatings remain niche, partly due to capital expenditure requirements for electrostatic spray booths and curing ovens. Technical guidance from the Association of Paint and Resin Manufacturers of Iran is helping smaller producers navigate formulation hurdles. Collaborative research and development agreements with Asian technology licensors are further easing performance gaps between water-borne and conventional solvent-based products.

By End-User Industry: Architectural Leadership Meets Automotive Growth

Architectural uses generated 54.70% of segment revenue in 2025, driven by the national housing program and ongoing renovation work. Automotive OEM and refinish demand is projected to post a 3.00% CAGR to 2031 as domestic vehicle assembly plants ramp up protective and decorative finish lines. Furniture-related wood coatings benefit from export-led production clusters along border provinces, while general industrial and marine applications draw on Iran’s expanding steel, petrochemical, and port infrastructure.

Nano-enhanced traffic marking paints have entered service at Isfahan Airport, demonstrating local ability to commercialize research outputs. Packaging coatings remain modest but could scale alongside Iran’s food-processing expansion. Across all end users, ISO certification and documented VOC performance are rising procurement prerequisites.

Geography Analysis

Tehran, Isfahan, and Shiraz dominate consumption due to housing activity, industrial clusters, and heritage conservation needs. Khuzestan and Fars host petrochemical hubs that supply critical resins and solvents at competitive transfer prices. Coastal provinces specialize in marine and protective maintenance coatings for port and shipyard infrastructure, while interior regions focus on architectural and wood-finishing lines aligned with furniture export processing. Border provinces leverage overland corridors into Iraq and Turkey, creating demand pockets for export-grade finishes. The Iran Nanotechnology Initiative Council’s decentralized funding has stimulated nano-coating start-ups across multiple provinces, spreading technical capacity beyond traditional industrial centers. Energy-related factory shutdowns in late 2024 exposed logistical vulnerabilities, incentivizing producers to adopt captive power or dual-fuel solutions to mitigate future disruptions.

Competitive Landscape

The market remains moderately fragmented, with international brands such as Jotun, AkzoNobel, and Hempel competing alongside domestic leaders Alvan Paint, Rangsazi Iran, Pars Pamchal, and Daryarnag. Global players command premium industrial and marine niches, leveraging advanced corrosion-resistant and fire-protective technologies. Domestic firms rely on cost advantages, petrochemical integration, and familiarity with regulatory protocols.

Strategic focus areas include ISO 9001 certifications, product differentiation through nano-enabled functionalities, and partnerships with Iranian universities to commercialize proprietary resin and additive systems. Sanctions deter some European and North American entrants, effectively protecting local share but also limiting technology inflow. The emergence of 200 plus knowledge-based nano-technology companies is catalyzing a shift toward higher-margin specialty coatings, particularly in conservation, solar energy, and pipeline protection lines. Consolidation is expected among smaller producers lacking access to diversified energy supplies or export channels.

Iran Paints And Coatings Industry Leaders

Jotun

Alvan Paint Co.

Pars Pamchal Company

Peka Chemie

Rangsazi Iran Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: An acute national energy shortage forced widespread industrial shutdowns, interrupting production schedules for several paint and coatings plants and escalating discussions around on-site power generation strategies.

- July 2023: Iranian manufacturers launched nanoparticle-enhanced polymer paints aimed at boosting anti-corrosion performance in harsh environments.

Iran Paints And Coatings Market Report Scope

Paints and coatings are a homogeneous mixture of pigments, binders, and additives, which are applied to make a thin layer of the solid film once polymerization or evaporation occurs. Paint and Coatings are used in office buildings, warehouses, retail convenience stores, automotive bodies, interiors, and in various other industries.

Iran's paints and coatings market is segmented by resin type, technology, and end-user industry. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types. By technology, the market is segmented into water-borne and solvent-borne. By end-user industry, the market is segmented into architectural, automotive, wood, industrial coatings, transportation, and packaging.

For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

By End-user Industry

| Architectural |

| Automotive OEM and Refinish |

| Wood Finishes |

| General Industrial |

| Transportation and Marine |

| Packaging |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-user Industry | Architectural |

| Automotive OEM and Refinish | |

| Wood Finishes | |

| General Industrial | |

| Transportation and Marine | |

| Packaging |

Key Questions Answered in the Report

What is the current value of the Iran paints and coatings market?

The Iran paints and coatings market size stands at USD 466.93 million in 2026.

How fast is demand for water-borne technologies growing?

Water-borne coatings are registering a 3.09% CAGR in response to Clean-Air compliance rules.

Which resin segment is expanding the quickest?

Polyurethane resins exhibit the highest growth at a 2.91% CAGR due to pipeline protection and specialty uses.

Why do international sanctions matter to Iranian paint producers?

Sanctions restrict access to high-purity pigments, additives, and advanced equipment, raising procurement costs and tightening quality control.

Where is demand most concentrated geographically?

Tehran, Isfahan, and Shiraz dominate volume, while Khuzestan supplies key petrochemical inputs.

Page last updated on: