Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.62 Billion |

| Market Size (2026) | USD 15.22 Billion |

| Market Size (2031) | USD 18.59 Billion |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Architectural Coatings Market Analysis by Mordor Intelligence

The China Architectural Coatings Market size was valued at USD 14.62 billion in 2025 and estimated to grow from USD 15.22 billion in 2026 to reach USD 18.59 billion by 2031, at a CAGR of 4.09% during the forecast period (2026-2031). The steady trajectory reflects demand anchored in large-scale housing renovation, energy-efficient new builds, and stricter environmental codes that reward low-VOC solutions. Waterborne systems now cover more than four-fifths of national consumption, confirming a structural shift away from solvent technologies to meet carbon peaking targets. Acrylic chemistry dominates formulation choices due to its balanced cost, durability, and compliance, while premium texture finishes and photovoltaic-ready roof coats add incremental growth niches. Supply risks tied to titanium dioxide and acrylic monomer pricing remain material, yet vertical integration and inventory hedging by leading producers have limited abrupt margin swings. Market participants are increasing research and development spending to enhance the functional value of coatings—such as heat reflection, self-cleaning, and fire protection—positioning them as enablers of China’s broader green-building agenda.

Key Report Takeaways

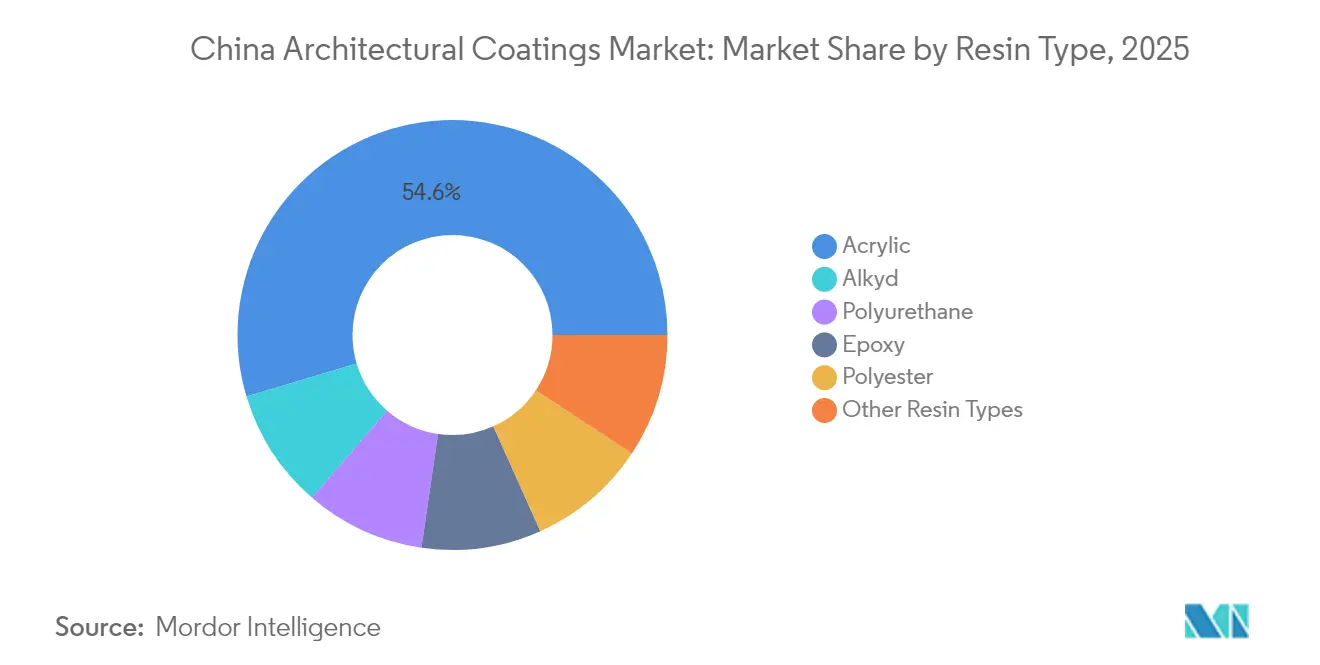

- By resin type, acrylic captured 54.62% of China architectural coatings market share in 2025 and is expected to grow at a 4.32% CAGR through 2031.

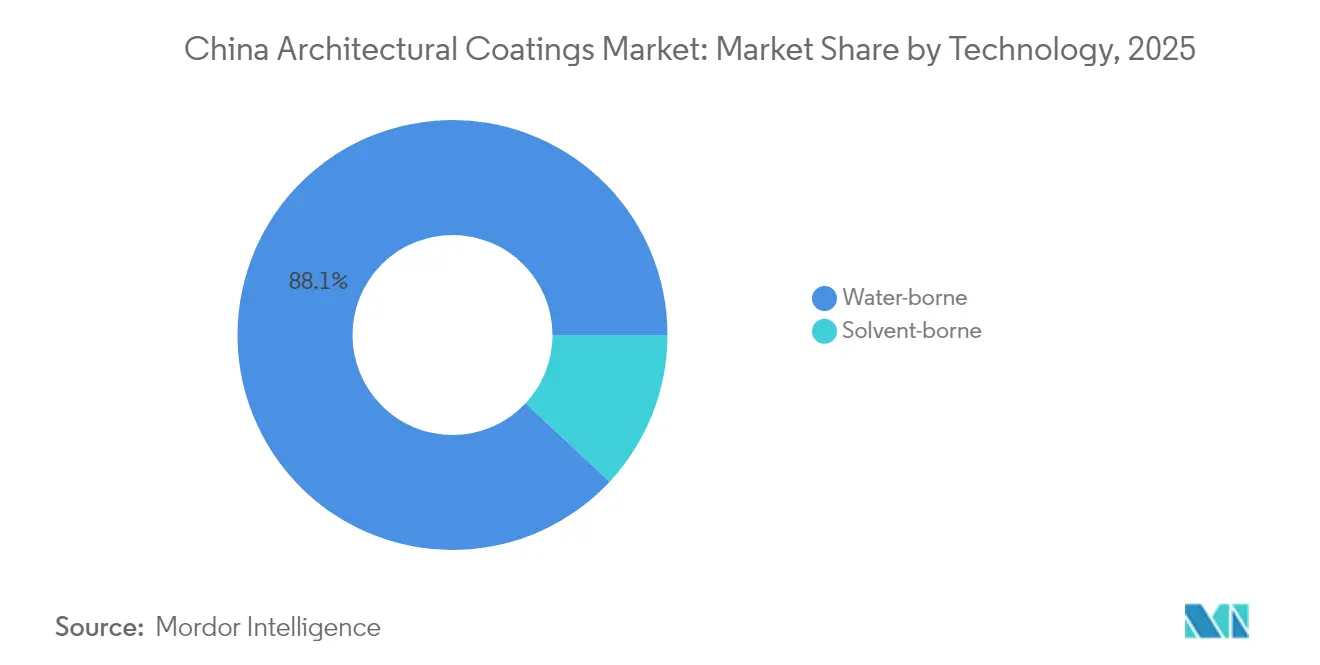

- By technology, waterborne systems accounted for an 88.05% share of the China architectural coatings market size in 2025 and are expected to grow at a 4.39% CAGR through 2031.

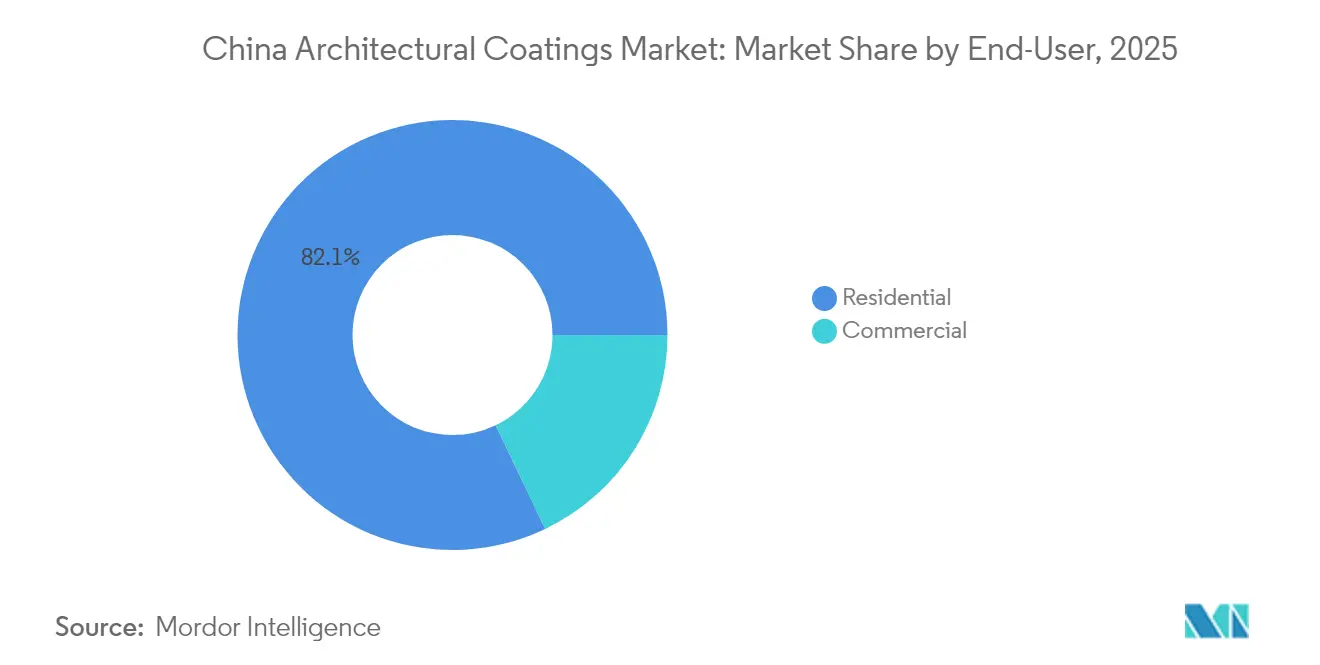

- By end-user, residential applications held 82.10% revenue share in 2025, while commercial projects are projected to post the fastest CAGR at 4.23% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC and carbon-peaking regulations driving waterborne shift | +1.2% | National, early adoption in Beijing, Shenzhen, Shanghai | Medium term (2-4 years) |

| Rapid growth in housing-stock repaint and renovation demand | +1.8% | National, strongest in East and Central China | Long term (≥ 4 years) |

| Government subsidies for certified green-building coatings | +0.7% | National, pilot schemes in tier-1 cities | Medium term (2-4 years) |

| Rising adoption of premium texture/stone-like façade systems | +0.9% | East and South China urban centers | Medium term (2-4 years) |

| Photovoltaic-ready reflective roof-coat demand surge | +0.6% | Solar-intensive provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter VOC and carbon-peaking regulations driving waterborne shift

China’s GB 30981.1-2025 standard caps interior wall VOC at 120 g/L and exterior at 140 g/L, compelling producers to retire most solvent lines. Beijing’s municipal rule is tighter at 80 g/L, while Shenzhen applies 100 g/L plus third-party audits. The framework aligns with national carbon-intensity goals, so waterborne coatings already represent 88.24% of overall consumption, resulting in a reduction of roughly 2.3 million tons of VOCs each year compared to legacy formulas. Suppliers rush to certify their products under compulsory green-building labels, aware that specification compliance now determines tender awards for public, commercial, and residential projects.

Rapid growth in housing-stock repaint and renovation demand

Buildings erected before 2010 span more than 40 billion square meters and require thermal upgrades and fresh finishes to align with current codes. Renovation absorbed a major portion of interior-paint tonnage in 2024, decoupling baseline demand from cyclical new-build volumes. State urban-renewal funds offer a rebate of up to RMB 2,000 per household when certified low-VOC products are used, expanding the addressable market for premium interior lines. The East China provinces accounted for a major portion of renovation gallons, thanks to their dense urban stock and elevated disposable income.

Government subsidies for certified green-building coatings

National incentive rules reimburse RMB 45-80/m² for projects deploying registered low-VOC systems and extend eligibility to residential works of 5,000 m² or more. Jiangsu and Guangdong top up with local bonuses that can add RMB 100/m², effectively offsetting differential pricing versus legacy paints. Compliance overlap with LEED and BREEAM has also prompted Chinese suppliers to design export-ready SKUs, broadening economies of scale and reinforcing innovation pipelines[1]China Coating Network, “2024 Resin Usage Report,” chinacoatingnet.com .

Rising adoption of premium texture/stone-like façade systems

Liquid stone coatings are gaining popularity as lighter, cost-effective substitutes for natural stone. These systems reduce façade weight by up to 75% and eliminate structural steel expenditures. Leading vendors maintain more than 200 palette options, matching provincial aesthetic codes and heritage guidelines. Demand clusters in Shanghai, Hangzhou, and Nanjing, where commercial landlords seek façade differentiation without incurring granite rates.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of TiO₂, acrylic and PU resins | -0.8% | National | Short term (≤ 2 years) |

| Prolonged real-estate downturn dampening new-build volumes | -1.1% | National, acute in tier-2/3 cities | Medium term (2-4 years) |

| Skilled applicator shortage for multi-layer spray systems | -0.4% | National, pronounced in fast-growing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile prices of TiO₂, acrylic and PU resins

Titanium dioxide costs oscillated in 2024 as energy and logistics inputs gyrated. Acrylic resin quotes rose due to a squeeze in petrochemicals and environmental retrofits at upstream crackers, as well as PU resins amid TDI outages. Raw materials account for roughly 60–65% of cash production costs, so even modest swings can quickly erode margins, especially for firms with a gross spread of 15–20%. Key producers are now adopting quarterly cost-plus contracts, widening captive feedstock sourcing, and staging staggered list-price resets to mitigate volatility.

Prolonged real-estate downturn dampening new-build volumes

Residential developers in tier-2 and tier-3 cities slowed ground-breaks in 2024 after tight credit and excess inventory triggered a multi-quarter sell-down. The slump compresses fresh exterior-paint demand although refurbishment helps offset part of the gap. Policy easing, such as lower mortgage thresholds, may steady new starts, yet cautious financing suggests moderate momentum recovery only from 2026 onward.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylics consolidate leadership

Acrylic binders commanded a 54.62% volume share in 2025 and are expected to rise at a 4.32% clip through 2031, securing the largest slice of the Chinese architectural coatings market. Balance of performance, weathering endurance, and waterborne compatibility secure acrylics in both interior eggshell and exterior satin grades. Alkyds retain specialty niches where price takes precedence over compliance, while polyurethanes cater to façade projects that demand 15-year warranties. Epoxies excel in heavy-duty floors and parking decks, while polyesters cater to the powder-coated metal segment. Innovation is now steering toward bio-based acrylics that reduce carbon footprint without eroding margins.

Premium acrylics underpin roughly half of interior-wall purchases and almost two-thirds of direct-to-metal façade repaints, reinforcing momentum. The Chinese architectural coatings market size for acrylic formulations is projected to swell in line with renovation subsidies. Cost rationalization via local monomer supply and scale is expected to preserve the China architectural coatings market share held by domestic champions, even as multinationals sharpen waterborne hybrid grades for mega-projects.

By Technology: Waterborne supremacy entrenched

Waterborne technologies held 88.05% of China's architectural coatings market share in 2025 and are projected to grow at a 4.39% CAGR, outpacing the overall field. Mandatory VOC testing, combined with Beijing’s sub-80 g/L cap, leaves limited room for solvent variants beyond industrial crews. Manufacturers migrate to zero-VOC coalescents, self-crosslinking acrylics, and nanostructured additives that accelerate cure at room temperature. Capital outlays in advanced polymer reactors and closed-loop water purification reflect long-term conviction.

Solvent-borne units soldier on in edge cases— such as steel bridges and heritage woodwork—under written waivers. Equipment suppliers co-develop low-pressure sprayers tuned to 55–70 KU viscosity spectra, improving finish consistency while trimming overspray.

By End-User: Residential segment dominates repaint cycle

Residential jobs consumed 82.10% of gallons in 2025, as 40 billion m² of aging apartments sought fresh aesthetics and healthier indoor air. Subsidized green-home upgrades and greater per-capita living space underpin demand durability. Commercial footprints—such as shopping malls, office towers, and hotels—represented 17.90% and grew marginally faster with agile service-sector investment.

Retail consumers now scrutinize formaldehyde and odor, prompting a surge in low-odor and antibacterial interior lines. In contrast, commercial specifiers purchase on lifecycle cost, awarding long-warranty matte and satin coats that cut repaint frequency. The Chinese architectural coatings industry is increasingly adopting turnkey “product + applicator” bundles to ensure workmanship in both customer sets.

Geography Analysis

East China generates significant demand, driven by the infrastructure and manufacturing strengths of Shanghai, Jiangsu, and Zhejiang. Provincial governments there enforce some of the country’s lowest VOC thresholds, thereby accelerating the adoption of premium waterborne blends. Central China, with provinces such as Hubei, Hunan, and Henan, is leveraging rising disposable income and the relocation of factories from coastal regions. Urbanization policies support subway, airport, and transit-oriented developments that require interior and exterior coatings that meet smoke-toxicity specifications.

Southwest China relies on the housing booms in Sichuan and Chongqing. The region’s humid, seismic terrain drives uptake of elastomeric and weather-resistant exterior solutions with crack-bridging resilience. North and Northeast combined delivered just under one-quarter of the national gallons, but Beijing and Tianjin skewed toward high-spec, low-VOC grades. Export-oriented plants cluster in Guangdong and Jiangsu, shipping price-competitive gallons to Southeast Asia and Belt and Road economies.

Future regional shifts hinge on continued real-estate stabilization, differential subsidy schemes, and inter-provincial environmental compliance. Provinces imposing sub-100 g/L caps sooner than the national code will accelerate the shift toward higher-value formulations, gradually increasing the blended China architectural coatings market size of premium tiers.

Competitive Landscape

The China Architectural Coatings Market is highly fragmented. Global players with broad China retail footprints, while domestic majors exploit shorter supply chains and agile local marketing. Market leaders prioritize research and development in waterborne innovation, functional additives, and vertical integration that secures access to titanium dioxide and acrylic monomers. Strategic capex examples include AkzoNobel’s EUR 14 million Suzhou upgrade that co-locates pilot reactors and application labs focused on sustainable formulas[2]AkzoNobel NV, “AkzoNobel Upgrades Suzhou Site,” akzonobel.com. Digital tools emerge as disruptors: online configurators and color-match apps deliver specification certainty for contractors and homeowners, embedding brand preference. Labor scarcity in multi-layer spray techniques triggers vendor-sponsored accreditation. Consolidation continues through CNBM’s reorganization with Carpoly, signaling a potential convergence of upstream materials and downstream finishing systems.

China Architectural Coatings Industry Leaders

Nippon Paint Holdings Co. Ltd.

Carpoly Chemical Group Co., Ltd.

Akzo Nobel N.V.

3TREESGROUP

Guangdong Maydos Building Materials Limited Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Akzo Nobel N.V. launched a thermal insulation coating system in China, designed to reduce building surface temperatures by up to 10% during the summer months. The system features a radiative cooling topcoat and an aerogel-based thermal barrier mid-coat, enabling passive heat emission and minimal solar absorption. Fully water-based and low-VOC, the coatings support China’s dual-carbon policy and urban sustainability goals.

- March 2025: Nippon Paint Holdings Co. Ltd. and Evonik Coating Additives entered a strategic partnership to co-develop next-generation, eco-friendly coating solutions tailored for the architectural sector. This collaboration combines Evonik’s advanced additive technologies with Nippon Paint’s market leadership, aiming to meet the growing demand for sustainable architectural coatings among consumers.

China Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

By End-User

| Residential |

| Commercial |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-User | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms