Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

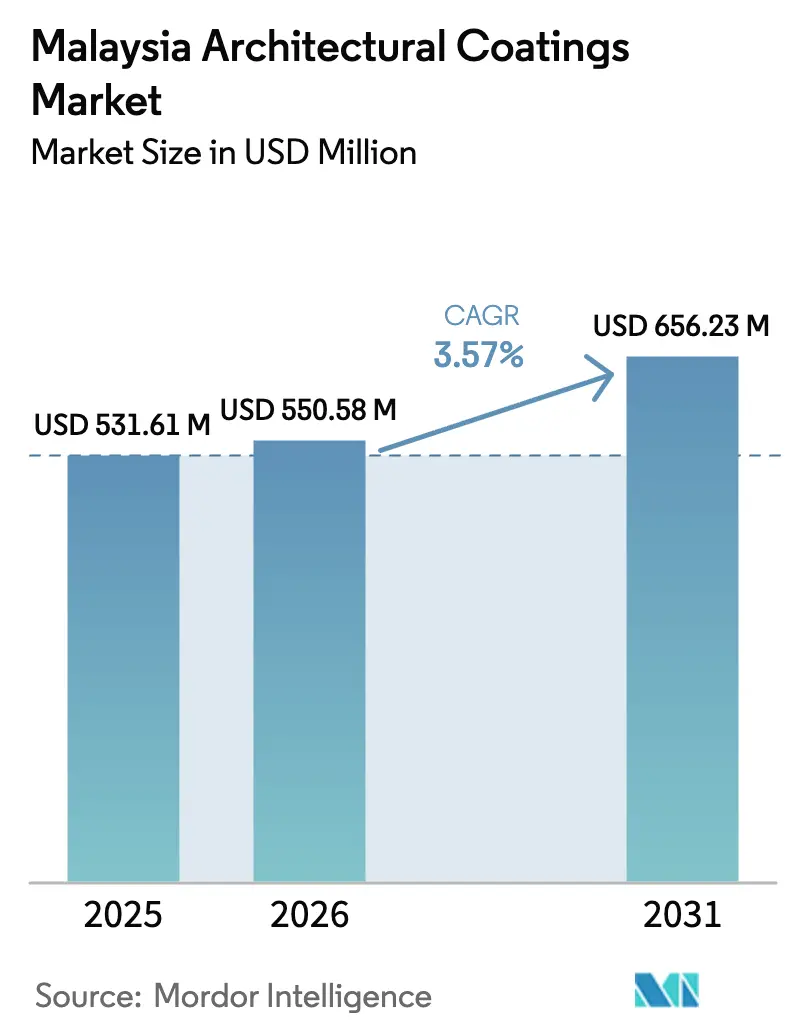

| Base Year Market Size (2025) | USD 531.61 Million |

| Market Size (2026) | USD 550.58 Million |

| Market Size (2031) | USD 656.23 Million |

| Growth Rate (2026 - 2031) | 3.57% CAGR |

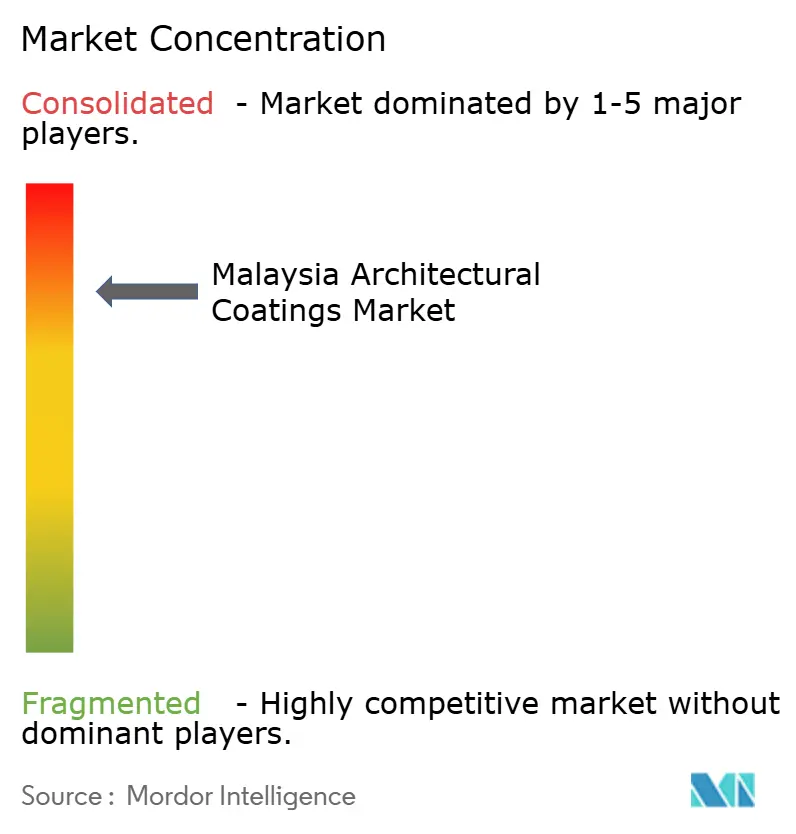

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Architectural Coatings Market Analysis by Mordor Intelligence

The Malaysia Architectural Coatings market size is expected to grow from USD 531.61 million in 2025 to USD 550.58 million in 2026 and is forecast to reach USD 656.23 million by 2031 at 3.57% CAGR over 2026-2031. Moderate growth reflects a maturing yet opportunity-rich sector supported by public infrastructure spending, rapid housing development, and tightening environmental rules that accelerate the shift toward sustainable water-borne formulations. Long-term demand also benefits from data-center construction by hyperscalers, revival of tourism-related commercial projects, and consumer willingness to pay premiums for specialty finishes with heat-reflective or antimicrobial properties. At the same time, volatile titanium-dioxide prices and office-space oversupply dampen profit margins and segment demand, pushing producers to streamline supply chains and diversify resin sourcing.

Key Report Takeaways

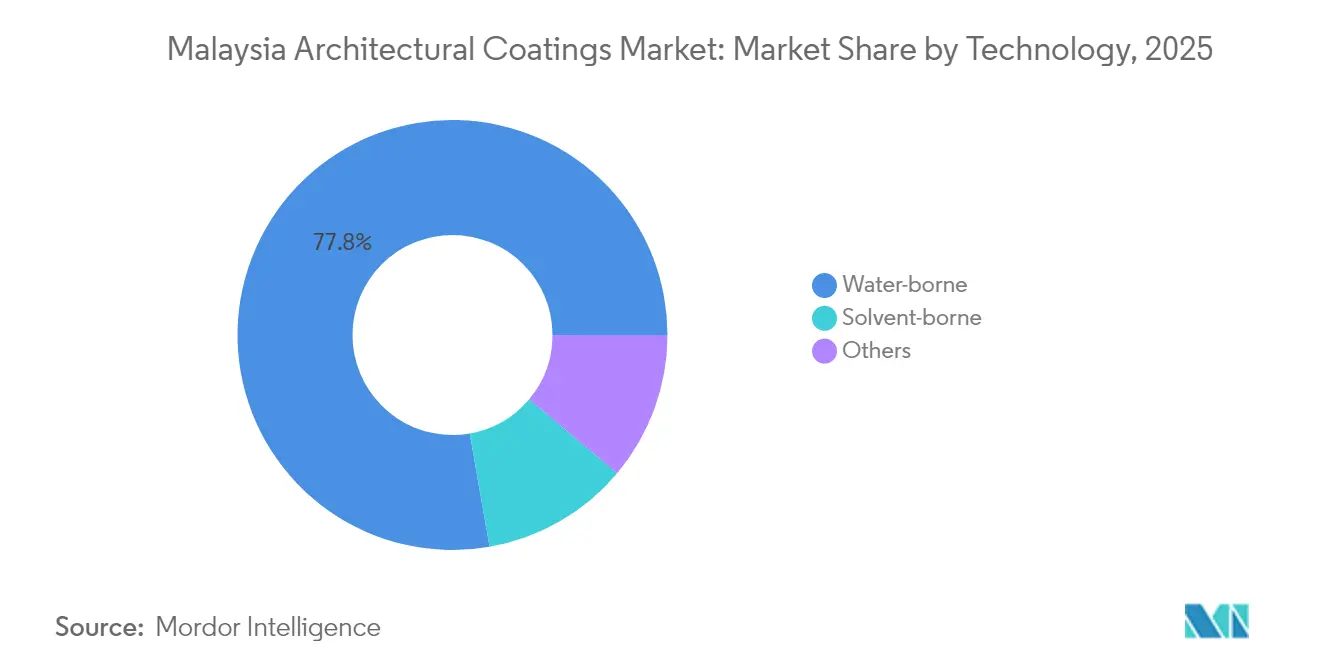

- By technology, water-borne coatings commanded 77.76% of Malaysia architectural coatings market share in 2025; solvent-borne formulations are projected to grow fastest at a 3.78% CAGR through 2031.

- By resin, acrylic products led with 46.30% revenue share of Malaysia architectural coatings market size in 2025, while polyurethane resins are on track for a 3.71% CAGR to 2031.

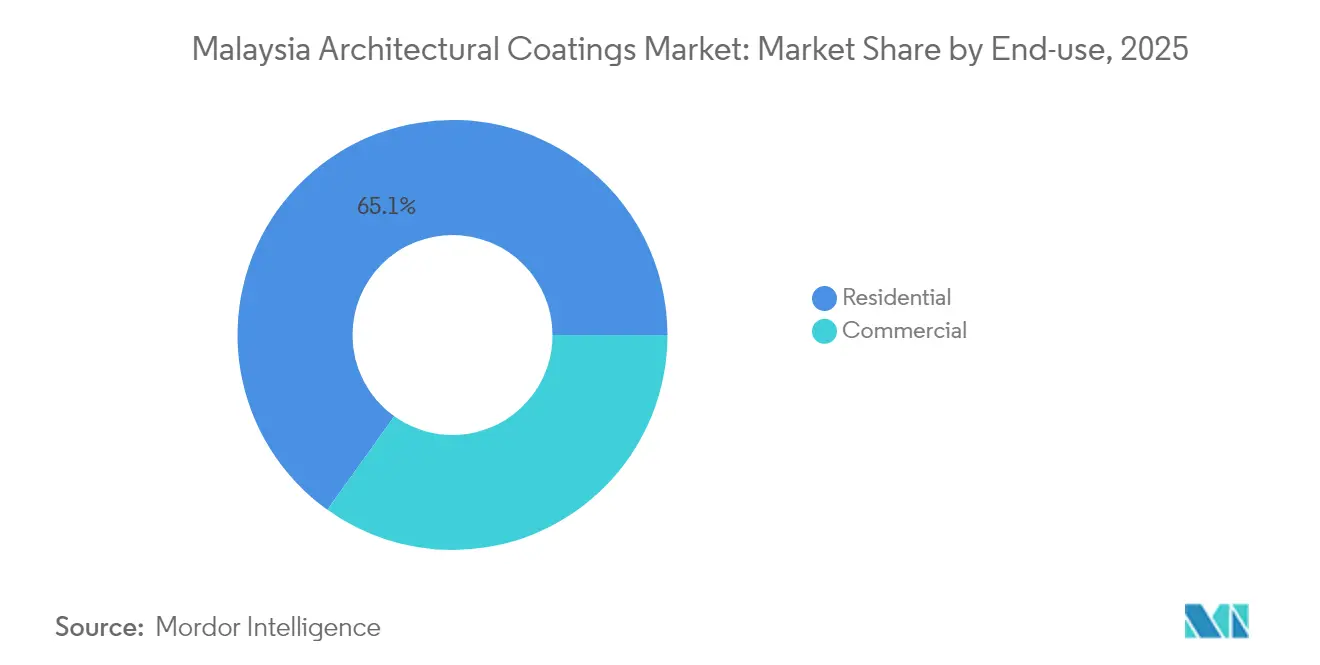

- By end-use, residential applications accounted for 65.11% of Malaysia architectural coatings market size in 2025; the commercial segment is advancing at a 3.66% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Architectural Coatings Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urbanisation and government housing push | +1.2% | Klang Valley, Johor, Penang, East Coast states | Medium term (2-4 years) |

| Rapid switch to low-VOC water-borne paints | +0.8% | Urban Malaysia; government procurement | Short term (≤ 2 years) |

| Tourism-led commercial projects revival | +0.4% | Melaka, Penang, Langkawi, Johor | Medium term (2-4 years) |

| Premium interior finishes demand | +0.3% | Klang Valley, Penang, Johor Bahru | Long term (≥ 4 years) |

| Cool-roof and heat-reflective coatings adoption | +0.2% | Nationwide, especially tropical heat-intense zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urbanisation and Government Housing Push

Accelerated federal and state housing schemes keep the Malaysia architectural coatings market on a solid growth path. The federal allocation of MYR 1.92 billion (USD 408 million) to Syarikat Perumahan Negara Berhad funds construction of 23,000 Rumah Mesra Rakyat units by 2025, well above the Twelfth Malaysia Plan target. State-led pipelines add another 15,000 affordable homes scheduled for completion across Kelantan, Sabah, and Selangor in 2024. Revival of 351 abandoned projects covering 43,738 units further boosts near-term coating demand. Government-backed mortgage guarantees worth MYR 10 billion (~USD 2.37 billion)in Budget 2025 are expected to sustain first-time buyer activity into the medium term. These initiatives collectively underpin consistent volume for interior and exterior paints in both new-build and refurbishment cycles.

Rapid Switch to Low-VOC Water-Borne Paints

Malaysia’s architecture and building codes increasingly target indoor-air quality and energy efficiency, accelerating adoption of water-borne technologies. The Uniform Building By-Laws require thermal-performance standards for large air-conditioned spaces, while the proposed Energy Efficiency and Conservation Bill introduces mandatory energy-management obligations for commercial buildings. Product approval directories maintained by the Public Works Department list hundreds of compliant water-borne paints, effectively steering public-sector procurement toward low-VOC formulations[1]Jabatan Kerja Raya, “JKR Green Product Directory,” jkr.gov.my. Smart Paint Manufacturing’s zero-VOC range and successful Bursa Malaysia listing validate commercial demand for healthier coatings. Large multinationals, including PPG and AkzoNobel, are expanding Malaysian production lines for water-borne systems, reinforcing the migration away from solvent technologies.

Tourism-Led Commercial Projects Revival

The rebound in international arrivals is reinvigorating hotel, retail, and mixed-use developments. YeaShin Construction’s MYR 500 million Birkin International Hotel in Melaka, featuring 526 luxury rooms within a UNESCO heritage zone, exemplifies premium hospitality investment. Data-center builders add an unconventional but sizable commercial opportunity: Knight Frank logged 429 MW of capacity take-up worth MYR 141.72 billion (USD 33.54 billion) through October 2024, driving demand for high-performance floor, wall, and roof coatings suitable for controlled environments. Together, hospitality and hyperscaler investments expand the customer base for specialty architectural systems.

Premium Interior Finishes Demand

Rising disposable incomes among urban households influence aesthetic choices and boost consumption of texture, effect, and antimicrobial paints. Klang Valley residential developers specify silk-finish acrylics and polyurethane topcoats to differentiate mid-to-high-end apartments. Global brands deploy design advisory teams, while local players partner with real-estate influencers to promote curated color palettes. Premiumization raises average selling prices and margins even as overall volume grows slowly, enhancing revenue stability for coating producers.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ and petro-derived resin prices | -0.6% | Nationwide | Short term (≤ 2 years) |

| Stricter VOC and HAP compliance costs | -0.3% | Nationwide; greater burden on small producers | Medium term (2-4 years) |

| Commercial office oversupply dampening demand | -0.4% | Klang Valley, Penang, Johor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ and Petro-Derived Resin Prices

Titanium-dioxide supply shocks remain the largest cost headwind for the Malaysia architectural coatings market. Top Chinese producers, including Lomon Group, executed three price hikes in 2024 that lifted export quotes by USD 100 per ton[2]Peijin Chemical, “Titanium Dioxide Price Increase For The Third Time in The Year,” peijinchem.com. At the same time, ongoing energy-intensity controls have crimped pigment output, while ocean-freight rates remain elevated. Acrylic, polyurethane, and alkyd resins derived from propylene and benzene streams exhibit similar volatility, forcing Malaysian manufacturers to adjust batch sizes, renegotiate annual blanket contracts, and intensify local sourcing.

Stricter VOC and HAP Compliance Costs

Malaysia’s Department of Environment aligns emission thresholds with ASEAN and EU benchmarks, requiring extensive reformulation and certification outlays. Smaller family-owned paint producers struggle with the capital expense of water-borne dispersion lines, testing chambers, and third-party auditing. Delays in obtaining SIRIM QAS International certification can sideline products from government tenders. Compliance costs thus widen the competitiveness gap between multinationals and domestic SMEs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Dominance Amid Regulatory Shifts

Water-borne formulations captured 77.76% Malaysia architectural coatings market share in 2025, underscoring decisive regulatory and consumer preference toward low-VOC systems. The segment’s scale benefits from broad application across interior walls, exterior facades, and trim, as well as from inclusion in public-sector tender lists that increasingly mandate water-borne compliance. Malaysia architectural coatings market size attributed to water-borne products is projected to grow steadily as multinational producers upgrade local lines and SMEs license dispersion technology.

Volume leadership is complemented by robust innovation. Smart Paint Manufacturing’s zero-VOC acrylics have gained market traction in post-pandemic fit-outs, while PPG expanded Petaling Jaya capacity to supply high-build wall and floor systems for energy facilities. Solvent-borne products, while accounting for a modest share, register the fastest CAGR at 3.78% because of niche demand in infrastructure steel, wood finishes, and heavy-duty coastal projects. Powder and specialty coatings round out the “other” category, drawing interest for architectural metal cladding and traffic-marking applications where overspray and film-build advantages outweigh higher equipment costs.

By Resin Type: Acrylic Leadership with Polyurethane Momentum

Acrylics retained a 46.30% footing in 2025 thanks to all-round performance in tropical conditions, good alkali resistance on fresh plaster, and compatibility with water-borne chemistry. Malaysia architectural coatings market size for acrylic systems is expected to rise in tandem with affordable housing starts, as value-engineering favors reliable exterior emulsions over specialty blends.

Polyurethane recorded the highest forecast CAGR at 3.71% through 2031, propelled by data-center floors, pharmaceutical clean-rooms, and upmarket residential cabinetry where abrasion and chemical resistance justify higher cost. Malaysia architectural coatings market share for polyurethane remains small but growing; local formulators increasingly source aliphatic isocyanates and bio-polyol blends to satisfy project sustainability metrics. Alkyd, epoxy, and polyester resins maintain presence in heritage building restoration and protective decks, while “other resin types,” including siloxane hybrids, gain ground in coastal high-rise applications requiring extended maintenance intervals.

By End-Use: Residential Dominance with Commercial Acceleration

Residential building retained 65.11% Malaysia architectural coatings market share in 2025 as public-sector and private developers handed over high-volume affordable and mid-segment units. Bulk interior emulsions and economical roof coatings constituted the majority of volume, making housing the anchor segment for paint producers. Malaysia architectural coatings market size linked to residential categories will continue to grow with federal mortgage support and revitalization of abandoned projects.

The commercial segment is accelerating at a 3.66% CAGR, energized by record hyperscaler investment and tourism infrastructure. Data-center shells demand antistatic floor toppings, intumescent fire-proofing, and low-emission wall paints, all of which command higher margins than mass housing products. Adaptive reuse of aging malls into mixed-use lifestyle hubs further fuels specialty coatings needs for reinforced concrete, exposed metal, and way-finding graphics. Despite office oversupply, selective speculative fit-outs in Klang Valley and Johor still procure premium finishes that enhance overall occupant-experience ratings.

Geography Analysis

Klang Valley’s consumption is growing based on the back of dense housing pipelines, transit-oriented development, and federal infrastructure such as the MRT3 Circle Line. The region’s concentration of government ministries and corporate headquarters magnifies maintenance painting cycles for public buildings and high-rise facades. Data-center clusters in Cyberjaya and Bukit Jalil further stimulate polyurethane floor and fire-retardant wall coatings.

Proximity to Singapore’s land-constrained tech ecosystem attracts data-center and advanced-manufacturing investment, boosting demand for high-performance interior and protective paints. Retail-tourism assets in Iskandar Malaysia add incremental volume.

Penang maintains solid growth through sustained semiconductor expansion, with the proposed Mutiara Line LRT spurring urban redevelopment. Coastal humidity drives specification of siloxane-modified acrylics for mildew resistance, creating a distinct sub-segment within the Malaysia architectural coatings market. East Coast states, notably Kelantan, absorbed significant residential coatings volume via RMR handovers, while Sabah and Sarawak derive steady demand from the Pan Borneo Highway and resource-based industrial parks. Uniform certification by SIRIM QAS International ensures product equivalency across regions and facilitates inter-state distribution logistics.

Competitive Landscape

Malaysia architectural coatings market competition is concentrated amongst major players. . Nippon Paint exploits an integrated “Total Coating and Construction Solutions” model that bundles architectural, waterproofing, and flooring systems, enabling cross-selling on megaprojects such as MRT stations and hospitals. Local SMEs enhance competitiveness via niche innovation. Smart Paint Manufacturing’s Bursa listing funds expansion of its zero-VOC line, while Trans-Ocean Coatings dominates government projects in Sabah and Sarawak through long-standing supply track records. Seamaster Paint markets heat-reflective acrylics important for tropical roof assemblies. Overall, differentiation hinges on compliance with VOC caps, specialty product breadth, and ability to manage raw-material volatility.

Malaysia Architectural Coatings Industry Leaders

Jotun

Akzo Nobel N.V.

Kansai Paint Co., Ltd.

Nippon Paint Holdings Co., Ltd.

TOA Paint Public Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AkzoNobel opened a regional research and development center in Nilai to develop water-borne decorative coatings for Southeast Asia.

- May 2024: Smart Asia Chemical Bhd inaugurated a plant in Batu Gajah, Malaysia, capable of producing 27 million liters of water-borne decorative paint annually.

Malaysia Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Technology

| Water-borne |

| Solvent-borne |

| Others |

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

By End-Use

| Residential |

| Commercial |

| By Technology | Water-borne |

| Solvent-borne | |

| Others | |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By End-Use | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms