Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

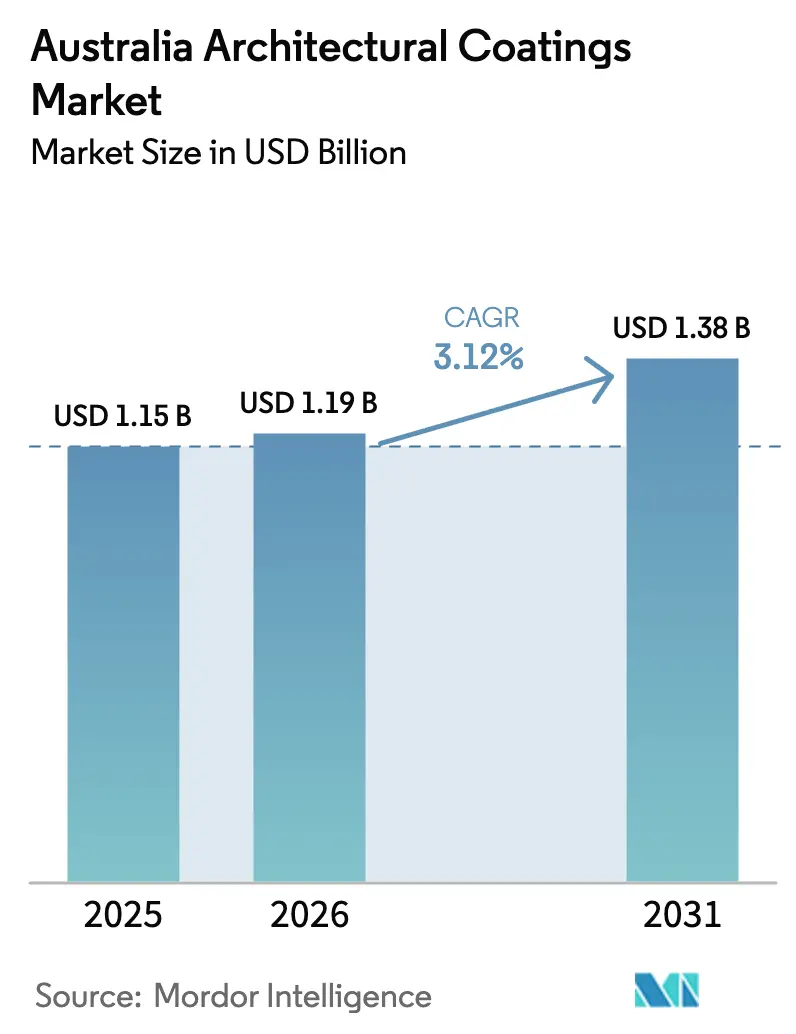

| Base Year Market Size (2025) | USD 1.15 Billion |

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

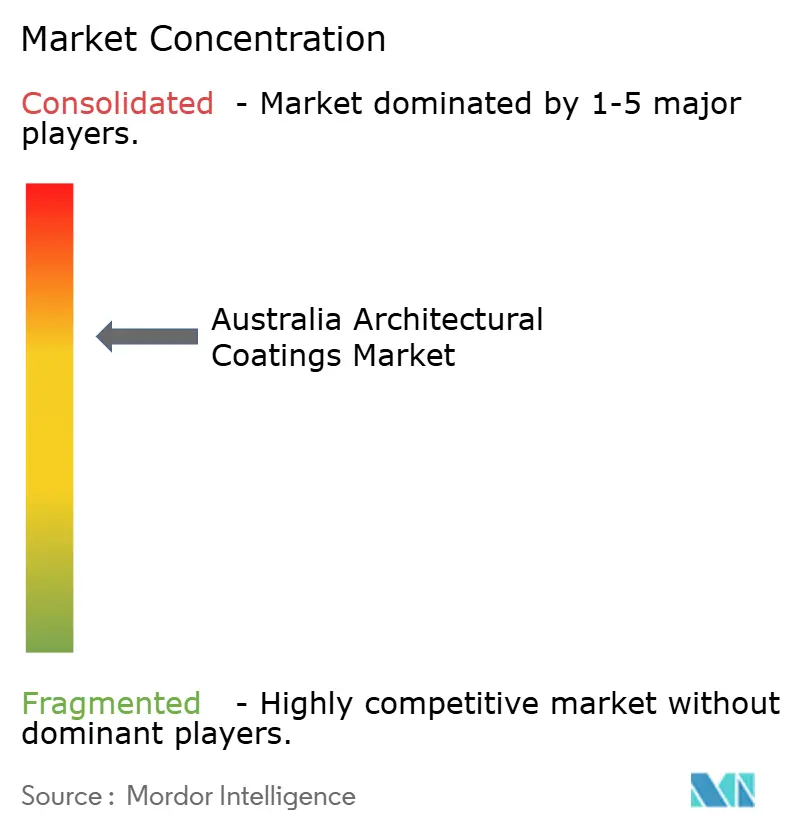

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Architectural Coatings Market Analysis by Mordor Intelligence

The Australia Architectural Coatings Market size is projected to grow from USD 1.15 billion in 2025 to USD 1.19 billion in 2026, and reach USD 1.38 billion by 2031, growing at a CAGR of 3.12% from 2026 to 2031. Intensifying renovation activity, tighter VOC limits, and a USD 32 billion federal housing stimulus are shifting demand toward low-emission, waterborne finishes specified for multi-family, build-to-rent, and public-sector projects. Skilled-labor shortages are catalyzing single-coat and factory-applied systems that reduce on-site complexity and help contractors maintain schedules despite a 30% shortfall in qualified painters. Escalating titanium-dioxide prices, coupled with higher petrochemical feedstock costs, are squeezing margins, yet premium brands with strong loyalty are successfully passing through mid-single-digit price increases. Over the forecast horizon, preference for Environmental Product Declaration (EPD)-backed products will accelerate penetration of powder coatings on façades and prefabricated panels, reinforcing the position of suppliers that can document low embodied carbon.

Key Report Takeaways

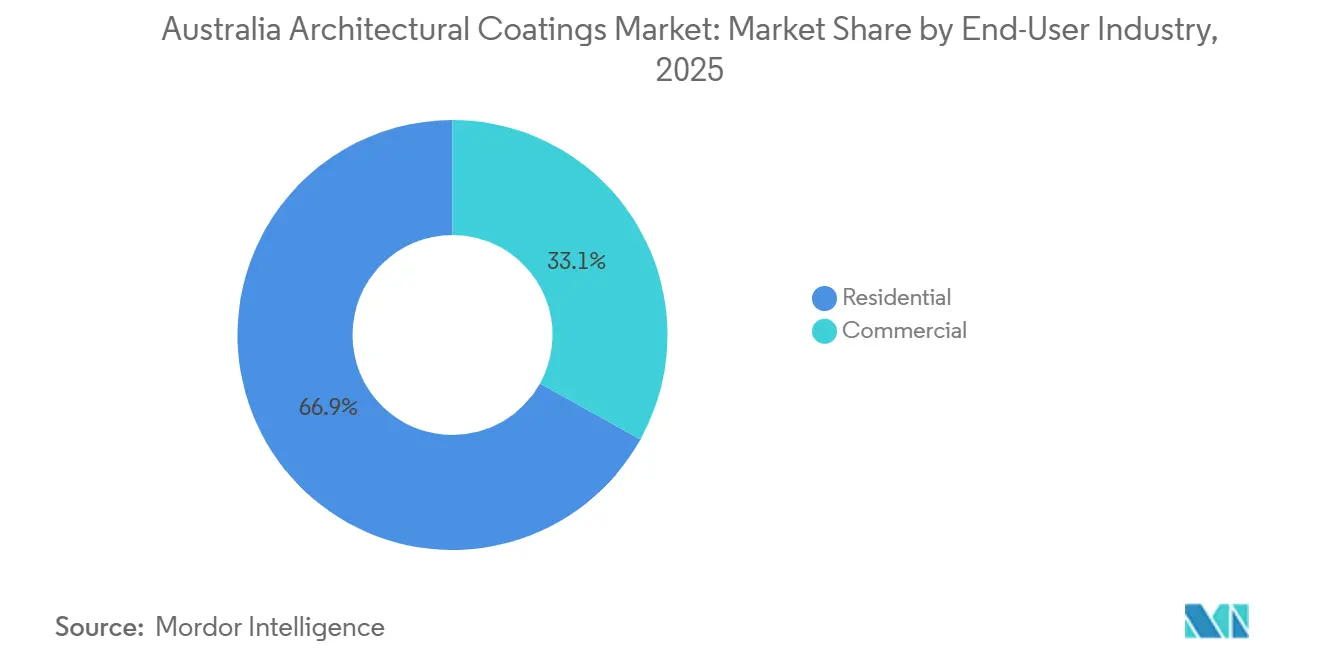

- By end-user industry, the residential segment led with 66.93% revenue share in 2025 and is advancing at a 4.14% CAGR through 2031.

- By technology, waterborne formulations captured 81.71% of the Australia architectural coatings market share in 2025 and will expand at a 4.35% CAGR to 2031.

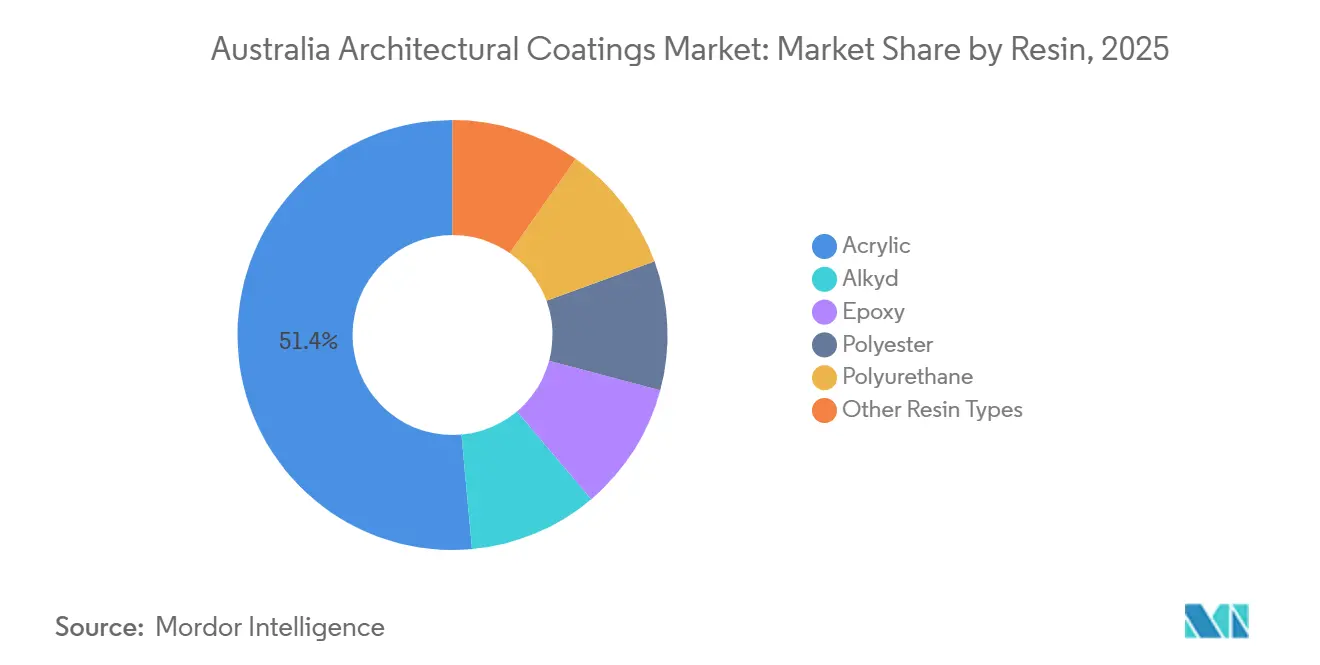

- By resin, acrylic systems accounted for 51.45% share of the Australia architectural coatings market size in 2025 and are projected to grow at a 4.21% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust public-sector housing and infrastructure pipeline | +1.2% | NSW, VIC, QLD growth corridors | Medium term (2-4 years) |

| Stricter VOC limits accelerating switch to water-based coatings | +0.8% | National; early adoption in SA and ACT | Short term (≤ 2 years) |

| Renovation and DIY boom from ageing housing stock and hybrid work | +0.9% | Urban NSW, VIC, coastal QLD, Perth | Medium term (2-4 years) |

| Net-zero building certifications driving EPD-backed powder coatings | +0.3% | Capital-city commercial hubs | Long term (≥ 4 years) |

| Prefab volumetric construction needing factory-finished panels | +0.2% | ACT, VIC, NSW social housing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Public-Sector Housing and Infrastructure Pipeline

Federal commitments totaling USD 32 billion aim to deliver 1.2 million well-located homes by mid-2029, of which 30,000 are earmarked for social and affordable housing through the Housing Australia Future Fund[1]Housing Australia, “Housing Australia Future Fund,” housingaustralia.com.au. The policy mix directs capital toward medium-density infill and build-to-rent developments that specify fire-rated façades and low-VOC interiors aligned with Green Star Buildings v1.1 benchmarks. State incentives, including a USD 1.5 billion Housing Support Program for enabling infrastructure, clear bottlenecks in water, power, and road access, and ensuring construction schedules remain intact. These factors collectively enlarge the addressable pool for premium waterborne and powder systems designed for long life cycles. As institutional investors consolidate procurement on multi-year frameworks, suppliers capable of furnishing EPD documentation and technical support gain pricing power.

Stricter VOC Limits Accelerating Switch to Water-Based Coatings

Australia’s January 2024 VOC regulations cap interior wall paints at 16 g/L and ultra-low-VOC products at 5 g/L, thresholds that most legacy solventborne formulations cannot meet[2]Department for Infrastructure and Transport (SA), “Low VOC Paint Requirements,” dit.sa.gov.au. Government fit-outs in South Australia and federal leasing rules effective July 2025 stipulate minimum 5.5-star NABERS Energy ratings, turning low-emission coatings from a value-add into a prerequisite. Waterborne acrylics employing self-crosslinking chemistries now equal or surpass solvent-based alkyds on scrub resistance and gloss retention while emitting negligible odors, a critical advantage for occupied refurbishments. Procurement guidelines under the Australian Paint Approval Scheme further rank products by VOC class, steering public buyers toward compliant brands. Early compliance has enabled manufacturers with ready portfolios to secure term contracts before late-moving competitors adjust formulations.

Renovation and DIY Boom from Ageing Housing Stock and Hybrid Work

Roughly 10 million dwellings, 70% of which are over 20 years old, require repainting every 5-7 years, locking in recurrent demand that insulates volumes from the cyclical swings of new-build approvals. Hybrid work keeps residents at home longer, prompting interior upgrades that favor washable, low-odor finishes. Interior projects now represent 40% of total residential construction spending, and bathrooms and kitchens alone average USD 19,000 and USD 27,500, respectively, raising attach rates for moisture-resistant topcoats. Sustainability attributes are moving into mainstream DIY decisions, with an estimated 40% of 2025 renovation projects specifying at least one eco-aligned product. Brands that offer color-matching plus third-party eco labels report double-digit growth in premium ranges.

Net-Zero Building Certifications Driving EPD-Backed Powder Coatings

Green Star Buildings v1.1, mandatory for new project registrations after May 1, 2026, boosts the Responsible Product Value awarded to products with product-specific EPDs from 5 to 7 points. Powder coatings, inherently solvent-free and capable of greater than 95% overspray recovery, help developers cut application-stage carbon emissions by up to 40%. NABERS launched a voluntary Embodied Carbon tool in December 2024 that is expected to integrate fully with Green Star scoring by 2027, further elevating material selection scrutiny. As façade packages frequently comprise over 15% of total building embodied carbon, architects specifying powder-coated aluminum panels can achieve immediate scoring benefits, driving double-digit growth in polyester-TGIC and fluoropolymer powders certified under ISO 14025.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TiO₂ and resin price volatility squeezing margins | -0.6% | Nationwide | Short term (≤ 2 years) |

| Import-price competition from Asian private-label paint brands | -0.3% | Value-tier retail channels | Medium term (2-4 years) |

| Skilled-applicator shortage for advanced multi-coat systems | -0.4% | Regional QLD, SA, WA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

TiO₂ and Resin Price Volatility Squeezing Margins

Closure of 600,000 tons per annum of titanium-dioxide capacity outside China in 2025 tightened global supply and lifted spot prices by USD 100-150 per ton in Q4 2025. Parallel jumps in acrylic-monomer and alkyd-resin prices compounded cost pressure. Australian manufacturers, heavily reliant on imports, faced gross-margin hits of 180-220 basis points unless able to push through price rises. Premium brands leveraged contractor loyalty to implement 5-6% annual list-price uplifts, while private-label suppliers risked volume erosion when attempting similar moves. With TiO₂ accounting for as much as 25% of total raw-material cost in white and pastel shades, formulators are experimenting with extender packages to reduce in-can pigment load without compromising opacity.

Skilled-Applicator Shortage for Advanced Multi-Coat Systems

Australia needs 83,000 additional construction workers to meet its 2029 housing target, yet the HIA Trades Availability Index fell to –0.48 in September 2025, signaling deep shortages. Painting trades (ANZSCO 332211) are flagged as in shortage nationwide, with regional South Australia worst at –1.35. Complex intumescent and epoxy-phenolic systems require controlled conditions that site crews struggle to maintain when understaffed, leading to rework and warranty claims. In response, specifiers are migrating to single-coat self-priming acrylics for interiors, and factory-applied powder finishes on exteriors, reducing on-site labor by up to 30%. Government measures—such as 20,000 fee-free TAFE spots and USD 10,000 apprenticeship incentives—will take up to two years to relieve pressure, making labor-saving products attractive through at least 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Renovation Resilience Anchors Residential Dominance

The residential segment accounted for 66.93% of Australia architectural coatings market size in 2025 and is forecast to expand at a 4.14% CAGR through 2031. Renovations command 40% of total dwelling investment, creating a stable replacement cycle that shields volumes from record-low new-build approvals. DuluxGroup positions 75% of its decorative revenue in this segment, emphasizing premium wash-and-wear interior paints that sustain pricing despite TiO₂ inflation.

Renovation intensity is highest in Sydney’s Inner West and Melbourne’s Boroondara, where permits for alterations exceed those for new construction. Aging stock, 70% older than 20 years, requires repainting every 5-7 years, securing a recurring demand floor. Hybrid work patterns elevate time spent at home and fuel discretionary interior upgrades, while rising eco-consciousness funnels consumers toward low-VOC and bio-based options. The commercial segment, though smaller, benefits from data-center expansion and tertiary-education refurbishments that specify intumescent and anti-graffiti systems, partially balancing weakness in new office builds.

By Technology: Waterborne Formulations Capture Regulatory and Institutional Tailwinds

Waterborne products dominated with 81.71% Australia architectural coatings market share in 2025 and are expected to expand at 4.35% CAGR to 2031. The January 2024 national VOC cap of 16 g/L for interior paints disqualifies most solventborne alkyds from government procurement, accelerating substitution across all price tiers. Self-crosslinking acrylic emulsions now achieve more than 5,000 scrub cycles without volatile coalescents, matching solvent alkyd durability while emitting minimal odor, a selling point for occupied refurbishments.

Solventborne coatings retreat to niche metal primers and high-gloss enamels that require rapid cure or extreme chemical resistance. Federal leasing mandates requiring NABERS 5.5-star Energy ratings from mid-2025 embed low-emission criteria into every large public tenancy, institutionalizing demand for waterborne systems. Combined with supply-chain investments such as a new 50 ML water-based resins plant by an international supplier opening in NSW in 2026, capacity is aligned to sustain the market shift.

By Resin: Acrylic Dominance Reinforced by Self-Crosslinking Innovation

Acrylic chemistries captured 51.45% of the Australia architectural coatings market size in 2025, expanding at 4.21% CAGR to 2031. Innovations integrating carbamate and silane functional groups create self-crosslinking lattices that harden during ambient cure, eliminating the need for VOC-rich coalescents. These products achieve ultra-low‐VOC levels below 5 g/L while meeting Class 1 scrub criteria under AS 3730.

Alkyds, historically prized for gloss, are transitioning into water-reducible alkyd-emulsion hybrids but still face perception challenges on drying time. Polyester-based powders, especially super-durable TGIC-free grades, are gaining share in exterior metal applications aligned with Green Star Responsible Finishes credits. Epoxy resins remain niche within garage floor and moisture-barrier primers, though demand for solvent-free epoxy DTM systems is emerging in hospital refurbishments where infection control curtails solvent use.

Geography Analysis

New South Wales and Victoria together account for more than half of the national construction value, and each records renovation shares above 40% of total dwelling investment, anchoring a dense network of paint retailers and trade center outlets in Sydney and Melbourne. Queensland’s coastal corridor attracts interstate migration that bolsters both new-build and lifestyle-driven repaint volumes, with subtropical humidity spurring uptake of mould-resistant exterior coatings.

Western Australia shows the steepest contractor shortfall; Perth’s Index of –0.89 leaves many mid-rise projects substituting multi-coat solvent systems with single-coat waterborne elastomerics to compress schedule risk. South Australia’s regional markets, facing the country’s deepest labor deficit at –1.35, increasingly specify factory-finished cladding panels shipped from interstate fabrication hubs, driving interstate powder-coating demand.

Tasmania prioritizes thermal-comfort upgrades, prompting sales of moisture-barrier primers and vapor-permeable exterior paints suited to cooler climates, while the Australian Capital Territory’s electrification incentives tilt specifications toward low-VOC, EPD-verified products across government projects. The Northern Territory, governed by cyclone-resilience standards, continues to demand UV-stable, high-build acrylics rated for extreme heat exposure. Emerging federal infrastructure allocations for rural and regional centers could redistribute volume toward these underserved geographies from 2027 onward.

Competitive Landscape

The Australia architectural coatings market is moderately consolidated. Multinationals, including PPG, AkzoNobel, Sherwin-Williams, Jotun, and Hempel, compete in protective and industrial niches, with Sherwin-Williams expanding U.S. coil-coating capacity by 60% in March 2026 to service export demand for metal roofing supplied into Australia.

Regional players such as Haymes Paint, Resene, and Porter's Paints differentiate via color consultancy and locally produced low-VOC ranges; Haymes’ Breathe Palette, certified GreenTag Level A, exemplifies this positioning. Powder-coating providers, including DECO Australia and Fairview, compete on AS 1530 non-combustibility compliance following façade-fire scrutiny. Litigation against AkzoNobel over alleged epoxy-phenolic failure on the Ichthys LNG project highlights warranty risk and underscores the value of field-testing before specification.

Australia Architectural Coatings Industry Leaders

Nippon Paint Holdings Co., Ltd.

PPG Industries, Inc.

Akzo Nobel N.V.

Haymes

Axalta Coating Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Jotun unveiled Jotachar 1709 XT, a patent-pending intumescent PFP coating tested on steel up to 50 °C and certified to UL1709 jet-fire standards.

- December 2024: The Green Building Council of Australia raised the Responsible Product Value for ISO 14025 EPDs from 5 to 7 points, immediately boosting the incentive for coating suppliers to publish product-specific declarations.

Australia Architectural Coatings Market Report Scope

Architectural coatings are specialized products designed for application on residential and commercial buildings to deliver aesthetic appeal, weather resistance, and long-term durability. These coatings protect structures from moisture, UV radiation, and corrosion, while enhancing the visual appearance of both interior and exterior surfaces.

The Australia architectural coatings market is segmented by end-user industry, technology, and resin. By end-user industry, the market is segmented into commercial and residential. By technology, the market is segmented into solventborne and waterborne. By resin, the market is segmented into acrylic, alkyd, epoxy, polyester, polyurethane, and other resin types. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By End-User Industry

| Commercial |

| Residential |

By Technology

| Solventborne |

| Waterborne |

By Resin

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

| By End-User Industry | Commercial |

| Residential | |

| By Technology | Solventborne |

| Waterborne | |

| By Resin | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms