Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

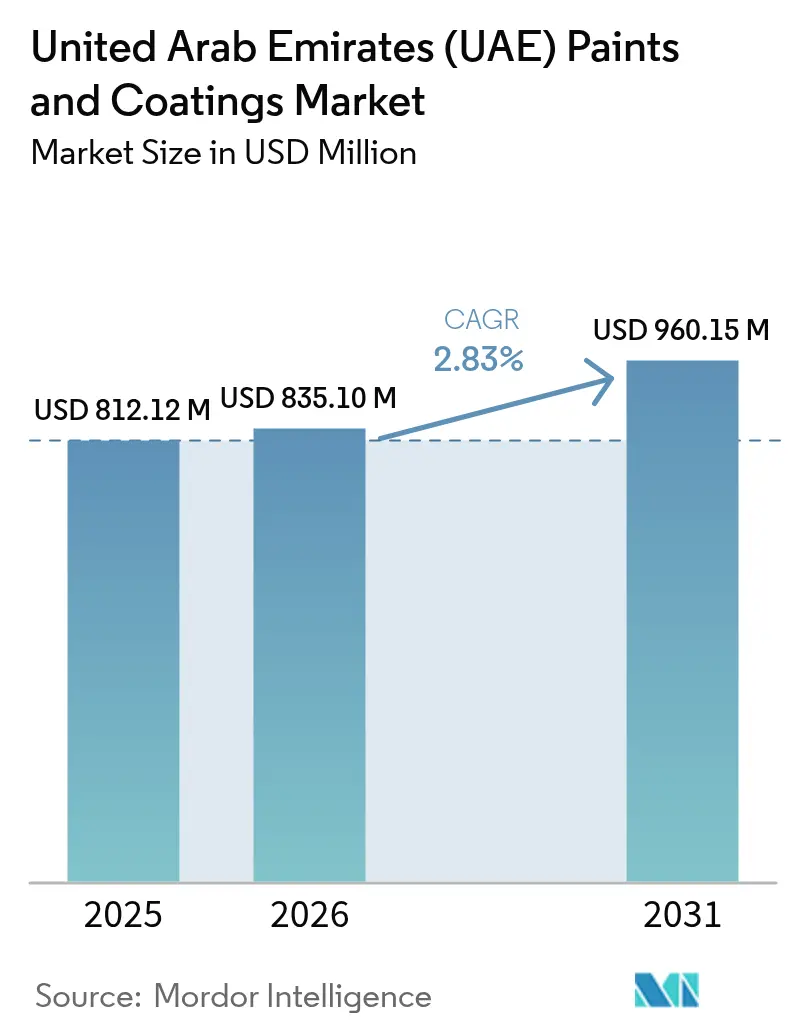

| Base Year Market Size (2025) | USD 812.12 Million |

| Market Size (2026) | USD 835.10 Million |

| Market Size (2031) | USD 960.15 Million |

| Growth Rate (2026 - 2031) | 2.83% CAGR |

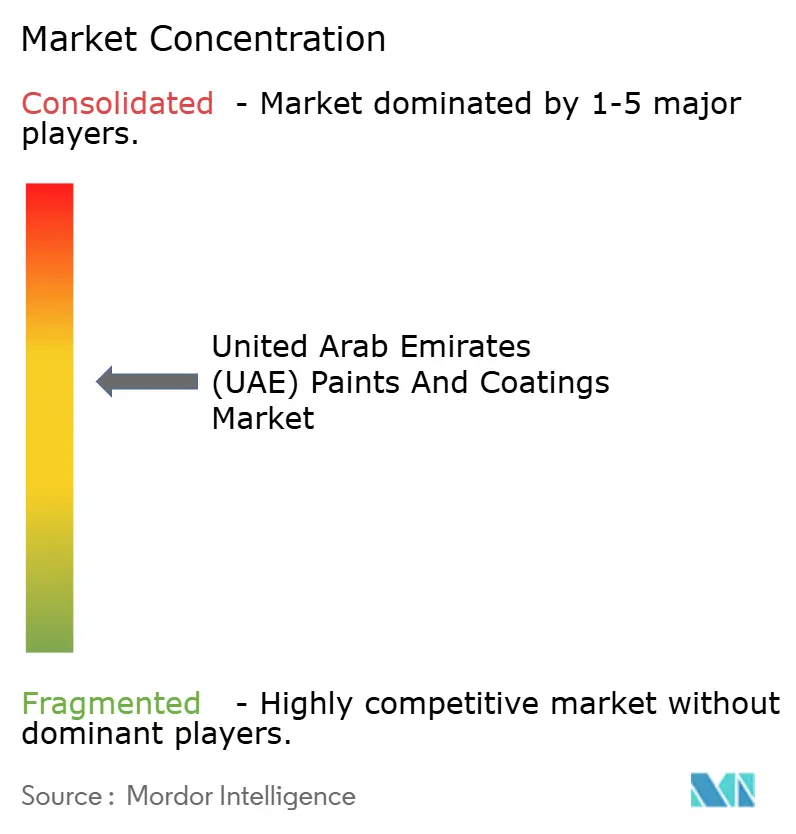

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates (UAE) Paints And Coatings Market Analysis by Mordor Intelligence

The United Arab Emirates Paints And Coatings Market size is expected to increase from USD 812.12 million in 2025 to USD 835.10 million in 2026 and reach USD 960.15 million by 2031, growing at a CAGR of 2.83% over 2026-2031. Operation 300bn and the In-Country Value (ICV) program are steering federal procurement toward domestic suppliers[1]U.AE, “Operation 300bn,” u.ae . As a result, global formulators are shifting from import models to setting up capital-intensive manufacturing bases in the UAE. Demand is further fueled by initiatives such as Dubai Municipality’s TG-04 VOC ceilings, certifications from the Abu Dhabi Quality and Conformity Commission, and a substantial infrastructure pipeline. This pipeline prioritizes water-borne systems and advanced protective technologies. ADNOC is also driving progress with a significant budget dedicated to extending asset life. This strategy is spurring a rise in the use of epoxy, polyurethane, and passive fire-protection coatings, known for their extended maintenance cycles. Moreover, industry leaders such as Jotun, Asian Paints, and Delta Coatings are increasing their capacities. This move highlights their confidence in the UAE's paints and coatings market, which is prepared to absorb a surge in local production while meeting strict environmental standards and project timelines.

Key Report Takeaways

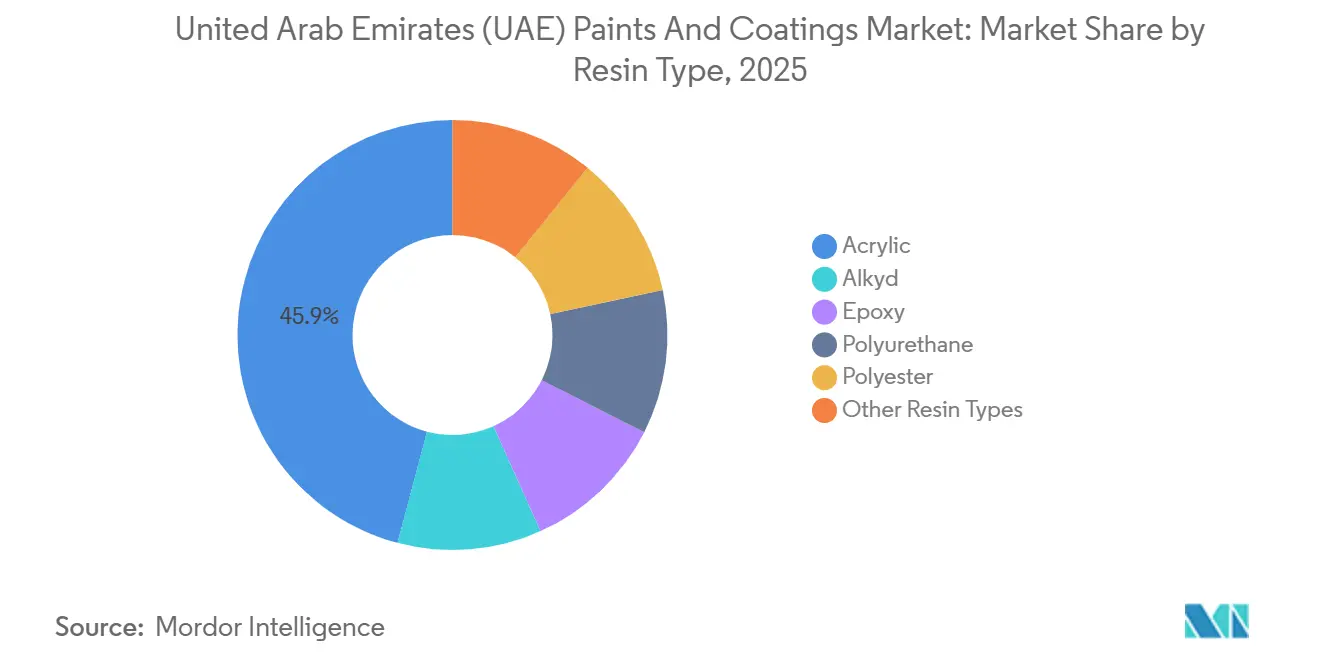

- By resin type, acrylic systems held 45.88% of the United Arab Emirates paints and coatings market share in 2025, whereas polyurethane formulations are projected to expand at a 2.86% CAGR through 2031.

- By technology, water-borne paints accounted for 47.22% of the 2025 volume and are advancing at the fastest 3.73% CAGR through 2031.

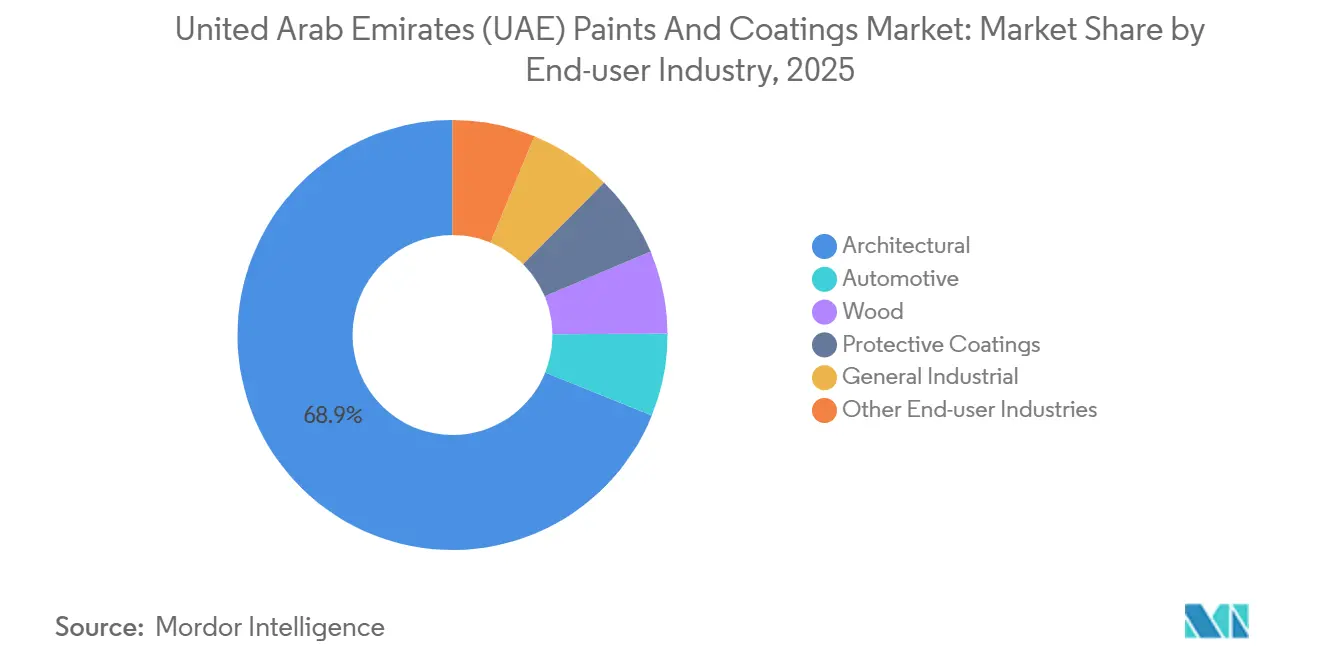

- By end-user industry, architectural applications generated 68.89% of 2025 revenue, while industrial coatings are set to lead growth at a 3.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates (UAE) Paints And Coatings Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil and gas asset-life-extension projects | +0.50% | Abu Dhabi, offshore zones, Northern Emirates industrial clusters | Medium term (2–4 years) |

| Regulation-driven shift to water-borne and low-VOC paints | +0.70% | Dubai, Abu Dhabi, Sharjah (municipal enforcement zones) | Short term (≤ 2 years) |

| Cultural-tourism mega-projects needing specialty finishes | +0.40% | Dubai, Abu Dhabi (landmark precincts) | Long term (≥ 4 years) |

| Luxury residential and DIFC fit-out boom | +0.30% | Dubai (DIFC, Palm Jumeirah, Dubai Marina, Downtown) | Medium term (2–4 years) |

| "Projects of the 50" incentives for local coating plants | +0.60% | National, with concentration in Abu Dhabi, Dubai, Sharjah free zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oil and Gas Asset-Life-Extension Projects

ADNOC is prioritizing the enhancement of offshore platforms, subsea pipelines, and storage tanks' service life over their outright replacement. The company is gravitating towards cutting-edge protective solutions, including nanotechnology-infused epoxies, self-repairing polyurethanes, and moisture-cure systems. These advanced solutions can be deployed in high-humidity conditions, avoiding dew-point limitations. Case studies from Belbazem and Fujairah underscore the success of petrolatum wraps and solvent-free epoxies in significantly extending inspection intervals. Additionally, ALOCIT’s underwater epoxies, a type of wet-curing coating, minimize downtime for repairs in the splash zone. This advantage is magnified when considering that expenses for scaffolding or dry-docking can eclipse material costs. As a result, the United Arab Emirates paints and coatings market is increasingly favoring products that promise lifecycle savings, particularly given the region's challenging operating conditions.

Regulation-Driven Shift to Water-Borne and Low-VOC Paints

Dubai Municipality's TG-04 regulation curbs VOC emissions for both interior and exterior applications[2]Dubai Municipality, “Technical Guide TG-04,” dm.gov.ae . Meanwhile, Abu Dhabi requires third-party certification for every batch sold. Compliance checks, along with penalties for retailers, pose challenges, especially for untested imports. In June 2025, Asian Paints secured TG-04 approval for its SmartCare CureAssure, enabling its entry into government housing projects. Terraco's EcoLife range not only adheres to stringent ultra-low-emission standards but also helps developers earn Al Sa'fat and LEED points, all while ensuring durability. Dow's Primal binders enable formulators to achieve very low VOC levels without sacrificing scrub resistance. These industry developments are bolstering the demand for water-borne products and fueling growth in the United Arab Emirates paints and coatings market.

Cultural-Tourism Mega-Projects Needing Specialty Finishes

Landmarks such as the Museum of the Future and the upcoming Dubai Creek Tower are increasingly turning to advanced coatings. These coatings are essential to combat challenges such as UV radiation, thermal swings from 10 to 50 degrees Celsius, and abrasive sandstorms. As a result, polyurethane and fluoropolymer topcoats, which come with long-term warranties, have emerged as the preferred choice. In recent years, Caparol has reported a surge in sales, largely attributed to its façade insulation systems that artfully blend energy efficiency with visual appeal. Terraco’s Flexicoat Thermo not only cools roof temperatures, thereby lessening air-conditioning needs, but also supports the UAE's ambitious Net Zero 2050 objective. On another front, Jotun's Jotachar 1709XT, with its hydrocarbon-fire safety certification, broadens the scope of passive fire protection solutions for airports and transport hubs, elevating safety benchmarks in the United Arab Emirates paints and coatings market.

Luxury Residential and DIFC Fit-Out Boom

In Dubai, premium homes and Grade A offices are increasingly choosing low-odor, rapid-recoat, and antimicrobial finishes. These selections not only boost aesthetics but also meet the air-quality benchmarks set by the WELL Building Standard. Terraco's polished plasters, crafted from recycled materials, are gaining attention for their visual allure. On the other hand, VIP Coatings provides VOC-free waterproofers, ensuring balconies remain protected - a crucial factor for maintaining resale values. Given the current labor constraints, contractors are leaning more towards prefabricated pods. This trend has led to a surge in demand for factory-applied coatings, designed to withstand transport shocks without requiring touch-ups. Handycoat's ready-mixed compounds enable swift Level 5 drywall finishes in a single shift. Such efficiencies not only accelerate project handovers but also strengthen the United Arab Emirates paints and coatings market, even in the face of workforce challenges.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ and petro-feedstock prices | -0.40% | National (affects all formulators and importers) | Short term (≤ 2 years) |

| Gulf humidity and heat-cycle failures | -0.20% | Coastal zones (Dubai, Abu Dhabi, Sharjah, Fujairah) | Medium term (2–4 years) |

| Skilled applicator shortages | -0.30% | National, acute in Dubai and Abu Dhabi construction zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ and Petro-Feedstock Prices

Spot titanium dioxide prices have experienced significant fluctuations, pressuring formulators locked into fixed-price tenders. This is due to tightened Chinese export quotas and rising sulfuric acid costs. In the United Arab Emirates' paints and coatings sector, smaller producers reliant on spot cargoes have seen their margins erode because of premium payments. While FP-Pigments’ new venture in Abu Dhabi aims to stabilize supply by 2027, many formulators are proactively reducing titanium dioxide usage, opting instead for extender pigments and optical brighteners. At the same time, fluctuations in propylene, ethylene, and aromatics are impacting the cost structures of acrylics, vinyl acetate, and alkyds, prompting a shift toward bio-based resins, despite their higher price tags.

Gulf Humidity, Heat-Cycle Failures, and Skilled Applicator Shortages

During the scorching summer months, when humidity levels soar above 90% and steel temperatures reach 50 degrees Celsius, traditional two-component epoxies and polyurethanes face severely restricted safe application windows. Single-component moisture-cure polyureas offer a solution to these challenges; however, their widespread adoption depends on retraining applicators. In the United Arab Emirates (UAE), contractors are utilizing digital tools, prefabrication, and robotics to address labor shortages. In December 2025, Delta Coatings launched a training center, while Jotun's Certified Applicator Scheme ensures quality oversight from the specification stage through to inspection. Considering these advancements, it is unsurprising that factory-applied finishes on modular panels are increasingly dominating the United Arab Emirates paints and coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Durability Drives Polyurethane Uptake

Polyurethane demand is rising at a 2.86% CAGR to 2031 as asset owners prioritize lifecycle performance for offshore steel and splash-zone environments. Acrylics retained 45.88% of 2025 revenue thanks to easy application and compliance with TG-04 VOC rules. While epoxies have established roles in tank linings and pipelines, they rely on polyurethane topcoats for UV protection. Meanwhile, alkyds have steadily lost ground to more favorable low-odor, water-borne alternatives. Recent investments highlight this trend: Delta Coatings has set up a solar-equipped site in Dubai, and Jotun has expanded its capacity for Jotachar in Oman. These moves emphasize suppliers' commitment to scaling polyurethane research, aiming to solidify their position in the UAE's paints and coatings market, particularly for protective applications. Although niche chemistries such as silicones and fluoropolymers command premium prices in extreme environments, they still represent a small portion of the overall revenue.

By Technology: Water-Borne Systems Cement Lead

Water-borne coatings captured 47.22% of 2025 revenue and are advancing at a 3.73% CAGR through 2031, reflecting municipal VOC enforcement and green-building schemes. Solvent-borne finishes maintain a foothold where chemical resistance and fast flash-off outweigh emissions limits; however, continuous improvements in water-borne binders are narrowing this gap. Powder coatings, supported by new production lines and acquisitions, provide local architects with more color options for aluminum profiles. High-solids and UV-cure variants remain specialized but are gaining visibility in the furniture and electronics sectors. As a result, the United Arab Emirates paints and coatings market size for water-borne technology is widening faster than any other formulation class through 2031.

By End-User Industry: Infrastructure Lifts Industrial Coatings

Industrial segments - protective, marine, and general manufacturing - are projected to outpace other end-users with a 3.05% CAGR during the forecast period of 2026–2031, supported by ADNOC investments and an AED 170 billion transport package. Architectural paints accounted for 68.89% of revenue in 2025, driven by high-rise residential and hospitality construction projects. However, growth is tapering as labor shortages delay certain projects. While automotive and wood finishes hold niche positions domestically, protective coatings for offshore and petrochemical assets stand out, often specified with premium features such as zinc-rich primers and high-build epoxies. As prefabrication gains traction, there is a heightened demand for factory-applied powders and fast-cure water-borne systems. These innovations not only ensure damage-free shipments but also amplify the momentum in the United Arab Emirates paints and coatings market.

Geography Analysis

Dubai's 2026–2028 budget and its projected construction growth highlight the city's dedication to mega-projects, including Palm Jebel Ali and the Metro Blue Line. In Abu Dhabi, ADNOC's capital projects boost protective volumes, and the Louvre Abu Dhabi underscores the demand for specialty façades that artfully merge aesthetics with durability. Sharjah, which has been home to National Paints since 1977, stands as a crucial distribution hub for the Northern Emirates, leveraging its seasoned technical service teams.

Manufacturing activities are increasingly gravitating towards economic zones. KEZAD has secured long-term leases with both Jotun and Asian Paints, each significantly expanding their presence near Khalifa Port. Concurrently, Dubai Industrial City has attracted Delta Coatings, which established a research and development facility located 20 minutes from World Central Airport. This prime location significantly reduces the time-to-dock for exports bound for Africa and South Asia. Furthermore, Umm Al Quwain and Ras Al Khaimah are drawing in energy-intensive powder coating lines with utility discounts, broadening the geographic supply spectrum.

Coastal humidity, which is known to hasten corrosion, drives a surge in demand for premium epoxies, polyurethanes, and fluoropolymers, particularly those boasting extended warranties. While inland areas still favor budget-friendly acrylics for residential uses, the logistical synergy allows production facilities in KEZAD or Dubai Industrial City to adeptly address both climatic demands. These shifting trends highlight that, despite the United Arab Emirates paints and coatings market being geographically concentrated, it is reinforced by a robust network of multisite, just-in-time supply chains.

Competitive Landscape

The United Arab Emirates paints and coatings market is moderately consolidated. Multinational giants such as Jotun, PPG, Akzo Nobel, Sherwin-Williams, Nippon Paint, and Asian Paints possess significant brand equity. However, they face challenges with procurement regulations that link federal tenders to local capabilities. Jotun's new plant in KEZAD is expected to increase production, streamline operations, and reduce cross-border delays for clients in construction and energy. Similarly, Asian Paints has invested in a second facility in the UAE, aligning with local strategies to meet ICV scorecards and expedite shipments.

Local players such as National Paints, RAK Paints, and Terraco maintain an advantage with their agility in color matching and on-site services. Meanwhile, emerging companies such as Delta Coatings and Qemtex are establishing niches, benefiting from technical expertise and export incentives. FP-Pigments is moving towards upstream integration with its new pigment project, aiming to protect itself from TiO₂ price fluctuations once operational. The digital landscape is evolving; with most contractors now seeking BIM objects and EPD data, suppliers are responding by incorporating compliance documentation into their product libraries. In the United Arab Emirates paints and coatings market, certifications such as Dubai's TG-04 and Abu Dhabi's QCC have become essential. Vendors without third-party test certifications risk exclusion from municipal projects, emphasizing the market's focus on quality.

United Arab Emirates (UAE) Paints And Coatings Industry Leaders

Jotun

Akzo Noble N.V.

Caparol Paints

NATIONAL PAINTS FACTORIES CO. LTD.

PPG Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Jotun Abu Dhabi has signed a 50-year land lease with Khalifa Economic Zones Abu Dhabi - KEZAD Group to develop a state-of-the-art paint and coatings manufacturing facility in KEZAD Musaffah. The project will involve an investment of EUR 113 million and will cover an area of 83,177 sq. meters, marking a substantial expansion of the company's presence in the region.

- November 2025: Asian Paints announced to invest INR 340 crore (~USD 38.04 million) to establish a new manufacturing facility in the United Arab Emirates, representing a significant step in its global expansion. The new facility, set to span 100,000 sq. meters, will have an annual production capacity of 55,800 kilolitres.

United Arab Emirates (UAE) Paints And Coatings Market Report Scope

Paints and coatings are utilized in the architectural, automotive, wood, industrial, transportation, and packaging industries. They are intended for several applications, such as corrosion resistance, damage prevention, decorative reasons, and others. The United Arab Emirates paints and coatings market is segmented by resin type, technology, and end-user industry. The market is segmented by resin type: acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, powder, and other technologies. By end-user industry, the market is segmented into architectural, automotive, wood, protective coatings, general industrial, and Other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyurethane |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coatings |

| Other Technologies |

By End-User Industry

| Architectural |

| Automotive |

| Wood |

| Protective Coatings |

| General Industrial |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyurethane | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder Coatings | |

| Other Technologies | |

| By End-User Industry | Architectural |

| Automotive | |

| Wood | |

| Protective Coatings | |

| General Industrial | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the projected value of the United Arab Emirates paints and coatings market in 2031?

The United Arab Emirates paints and coatings market size stands at USD 835.10 million in 2026, and it is projected to reach USD 960.15 million by 2031 at a 2.83% CAGR.

Which technology segment is expanding fastest?

Water-borne coatings are growing at a 3.73% CAGR, driven by VOC regulations and green-building incentives.

Which resin type commands the largest 2025 revenue share?

Acrylic resins led with 45.88% of 2025 revenue.

How are federal policies influencing local production?

Operation 300bn and the ICV program require suppliers to manufacture locally to access AED-168 billion in procurement, driving new factories in KEZAD and Dubai Industrial City.

What challenges do formulators face in Gulf climates?

High humidity and 50°C surface temperatures risk blistering and adhesion loss for conventional epoxies, prompting a shift to moisture-cure and water-borne systems.

Why are powder coatings gaining traction?

Energy-efficient lines in Umm Al Quwain and Sharjah supply architectural aluminum, while zero-VOC attributes help projects meet green-building standards.

Page last updated on: